July 18, 2026

The $200 Million Question Sitting at the Heart of Tasmania's Industrial Liability Crisis

When a major industrial facility closes after decades of operation, the question of who bears the cost of environmental cleanup rarely has a simple answer. For sites established before modern regulatory frameworks existed, the answer is often found not in the company's accounts, but in the fine print of insolvency law — and ultimately, in the public purse. The closure of the Liberty Bell Bay manganese alloy smelter in northern Tasmania has placed this uncomfortable reality in sharp focus, raising one of the most consequential Liberty Bell Bay remediation costs questions the state has faced in a generation.

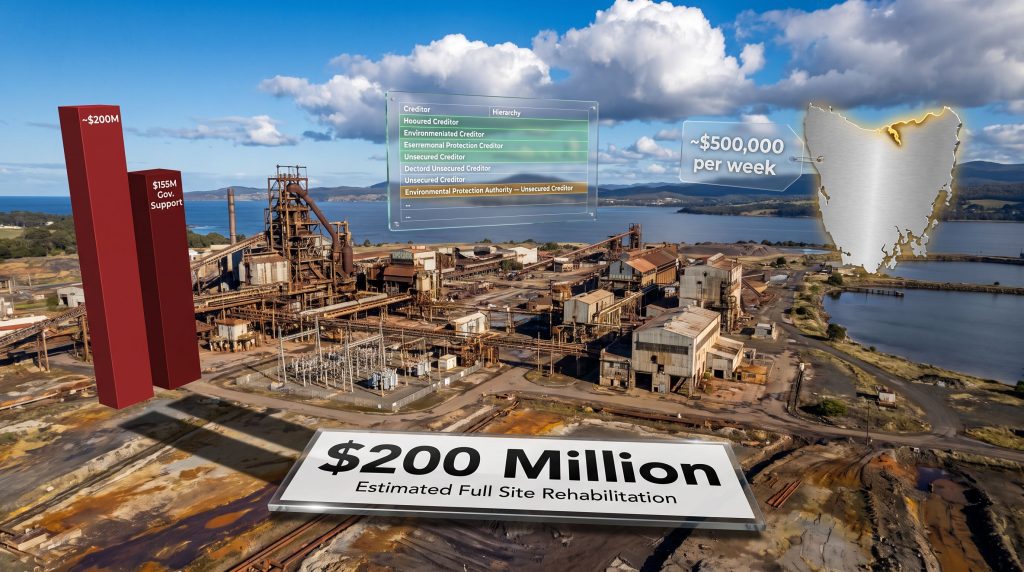

The Liberty Bell Bay remediation costs now being discussed are not hypothetical projections invented by critics. In October 2025, administrator William Buck produced an estimate of approximately $200 million as part of the Whyalla Ports administration process, covering the full rehabilitation of the Liberty Bell Bay site in the event of permanent closure. When Tasmanian Minister for Business, Industry and Resources Felix Ellis was asked directly whether that figure was accurate, he confirmed it was around that mark, while noting the final cost would depend on the scale of rehabilitation ultimately required.

That single qualifier — scale of rehabilitation — carries enormous financial weight. The difference between partial site reuse and full environmental remediation could represent tens of millions of dollars in either direction.

Breaking Down What $200 Million Actually Covers

Understanding where this figure comes from requires an appreciation of what full site remediation for a smelting operation actually involves. This is not simply a matter of switching off equipment and walking away. For a facility that has been processing manganese alloys since the 1960s, the remediation scope is considerable.

| Cost or Funding Element | Estimated Value | Notes |

|---|---|---|

| Full site rehabilitation (permanent closure) | ~$200 million | Estimated by administrator William Buck, October 2025 |

| Ongoing administration fees | ~$500,000 per week | Accumulating during insolvency process |

| Federal-state emergency loan (wages/admin) | $3 million | Does not cover remediation costs |

| Government support provided over past decade | $155 million | Electricity subsidies and related concessions |

| Environmental rehabilitation bond | $0 | No bond mechanism was in place at closure |

The physical work involved in full closure would include:

- Demolition of industrial plant infrastructure across the smelting complex

- Scrap steel salvage from decommissioned furnace structures and associated equipment

- Soil contamination assessment and active remediation, given decades of smelting byproduct accumulation

- Decommissioning of high-voltage electrical substations and ancillary power infrastructure

- Long-term environmental monitoring obligations stretching years beyond the initial cleanup phase

Ray Mostogl, chief executive of the Tasmanian Minerals, Manufacturing and Energy Council, has described the industrial plant component as the most problematic element. His assessment is that the smelting infrastructure itself would effectively need to be demolished and processed as scrap steel, after which the contaminated soil beneath would require active remediation. Portions of the broader site — including the electrical substation, administrative buildings, and workshops — hold more realistic prospects for sale and reuse by alternative operators.

When big ASX news breaks, our subscribers know first

How Australian Insolvency Law Determines Who Ultimately Pays

The legal architecture governing who bears the Liberty Bell Bay remediation costs is rooted in a distinction most people outside the insolvency profession rarely encounter: the difference between administration and liquidation, and the specific powers that attach to each.

The Administration Phase and Its Limits

During the current administration period, the appointed administrators hold legal responsibility for the site and its associated environmental obligations. This means they must manage the property and comply with existing regulatory requirements. However, administrators do not have the power to shed that responsibility by formally walking away from the land itself.

That power belongs exclusively to liquidators.

Property Disclaimer: The Legal Mechanism That Could Transfer the Burden to Tasmania

Under Australian corporations law, liquidators hold the right to formally disclaim property. When a liquidator exercises this power over an industrial site, legal ownership does not simply evaporate — it reverts to the Crown, meaning the relevant state government assumes responsibility for whatever environmental obligations are attached to that land.

Jason Harris, Professor of Corporate and Insolvency Law at the University of Sydney, has explained this mechanism clearly in public commentary on the Liberty Bell Bay situation. His analysis indicates that if the company enters liquidation, liquidators would be able to disclaim the property, at which point the land would revert to the state government as the ultimate owner of land that no private party is willing to hold. The state would then bear responsibility for the site and its associated liabilities.

This is not a remote legal scenario. It is a well-established mechanism that has played out across industrial and mine reclamation insolvencies in Australia. Furthermore, the absence of a buyer for Liberty Bell Bay makes this pathway materially more likely with each passing week.

Where Environmental Claims Rank in the Creditor Hierarchy

Even before the property disclaimer question arises, there is a structural problem with how environmental remediation obligations are treated under Australian corporations law. The Environment Protection Authority does not enjoy any special priority status in a liquidation. It is classified as an unsecured creditor — the lowest rung in the payment priority ladder.

Christopher Symes, Emeritus Professor of Insolvency Law at the University of Adelaide, has addressed this point directly. His analysis of the Corporations Act framework makes clear that liquidators are legally required to follow the statutory priority order, and that unsecured creditors — including environmental authorities — are typically reached only after all higher-ranking claims have been satisfied. In most corporate insolvencies of meaningful complexity, funds are exhausted long before that point.

This is not an accident of drafting. It reflects a long-standing tension in Australian corporate law between the efficiency goals of insolvency administration and the environmental protection objectives embedded in state regulatory frameworks. The two systems were designed largely in isolation from each other, and Liberty Bell Bay is now exposing the consequences of that disconnect.

The Missing Mechanism: Why No Rehabilitation Bond Existed

Perhaps the most striking feature of the Liberty Bell Bay remediation cost situation is not the size of the potential liability — it is the complete absence of any dedicated funding mechanism to cover it.

| Regulatory Mechanism | Mining Operations | Liberty Bell Bay |

|---|---|---|

| Mandatory rehabilitation fund | Required | Not required |

| Environmental bond | Standard condition | Not imposed |

| EPA closure obligations | Embedded in licence | Environmental protection order in place |

| Government backstop liability | Limited | Potentially full |

Minister Ellis has acknowledged this directly, noting that unlike mining operations — which are required to contribute to government rehabilitation funds as a condition of their licence — Liberty Bell Bay was not subject to the same requirement. His explanation places the blame squarely on the historical period in which the site was established, describing it as a question for people of generations past.

The site was built in the 1960s, predating the environmental bonding frameworks that would later become standard for Australian mining operations. It changed ownership multiple times — most recently acquired by Sanjeev Gupta's GFG Alliance in 2020 following a period under South32 — without any of those transactions triggering a reassessment of bonding obligations.

Documents reveal that the site is subject to an existing environmental protection order that includes decommissioning and rehabilitation requirements, as confirmed by an Environment Protection Authority spokesperson. The EPA is participating in a coordinated government response to assess environmental liability options. However, the existence of regulatory obligations does not create funding. The order establishes what must be done; it says nothing about where the money comes from if the responsible party is insolvent.

This gap between regulatory obligation and financial assurance is not unique to Liberty Bell Bay. Older industrial sites across Australia — particularly those established before the 1980s and 1990s environmental legislation reforms — frequently operate under legacy frameworks that impose cleanup obligations without requiring the financial security to back them up.

Four Scenarios for the Site's Future

The range of possible outcomes for Liberty Bell Bay spans from fiscally benign to deeply costly for Tasmanian taxpayers. Legal and industry experts have pointed to four realistic pathways.

Scenario 1: Successful Asset Sale

A new operator acquires the site, absorbing the environmental obligations as part of the transaction. Government financial exposure is avoided or substantially reduced. This is the most favourable outcome for Tasmanian taxpayers, but it requires a buyer willing to accept the site's legacy liabilities — likely only achievable with significant commercial concessions on energy pricing or other costs.

Scenario 2: Partial Asset Realisation with Mothballing

Sellable components — the substation, offices, workshops — are divested to third parties. The industrial plant is mothballed pending a longer-term decision. Mostogl has described mothballing as a plausible interim position, but also noted an important deterioration dynamic: the longer a smelter sits idle and cold, the greater the structural damage and the higher the eventual restart or demolition cost. This makes mothballing a short-term stabilisation measure, not a solution.

Scenario 3: Controlled Demolition and Soil Remediation

The industrial structures are demolished and processed as scrap steel. Contaminated soil is remediated to EPA standards. Portions of the land are repurposed for alternative industrial or commercial uses. Estimated cost approaches or exceeds the $200 million benchmark.

Scenario 4: Full Government Liability via Property Disclaimer

Liquidators formally disclaim the property. The land reverts to the Tasmanian Crown. The state government assumes complete responsibility for remediation and all associated costs. Tasmanian taxpayers bear the entire burden.

Professor Harris has noted that the EPA and state government have strong incentives to facilitate a sale — even at meaningful financial cost — to avoid the far larger liability of full site remediation falling to the public. The arithmetic is straightforward: if contributing additional financial support to a sale saves the state from a $200 million remediation bill, the cost-benefit calculation favours the former. Consequently, government intervention remains a key consideration in how this situation ultimately resolves.

Energy Economics: The Factor That Derailed the Sale

Understanding why no buyer has yet been secured requires understanding the economics of manganese smelting itself. This is one of the most energy-intensive industrial processes in the metals sector. Electricity is not simply a significant operating cost — it is the dominant variable cost that determines whether a smelter in a high-cost jurisdiction can compete against operations in markets with cheaper power.

The consortium that came closest to acquiring Liberty Bell Bay reportedly sought a two-year deferral of electricity and transmission charges, plus tens of millions of dollars in subsidies beyond already-discounted power rates. The state government, which had already provided $155 million in support over the preceding decade, declined to meet these terms.

Unions have argued that the failure to bridge this specific gap was the decisive factor in the sale collapsing. Whether that assessment is accurate or not, it highlights a structural challenge for energy-intensive industry in jurisdictions without access to extremely low-cost electricity. Without competitive power pricing, the economics of smelting simply do not work against lower-cost international producers, and broader mining sector pressures only compound this challenge further.

The Workforce and Regional Economy Caught in the Middle

The immediate human cost of the closure is the displacement of approximately 200 workers — the people who operated Australia's only manganese alloy smelter. A reduced workforce is being retained in the short term to safely demobilise the site, manage the sale of assets, and maintain compliance with environmental and regulatory obligations.

The broader economic significance extends beyond direct employment. As the country's sole manganese alloy smelter, Liberty Bell Bay's closure increases Australia's dependence on imported manganese alloys for domestic steel production. This is not merely a Tasmanian industrial story — it has national supply chain implications for the steel sector.

The site has been a fixture of northern Tasmanian industry since the 1960s. Its closure removes not just jobs but an entire category of industrial expertise from the regional economy. In addition, the federal and state funding lifeline of $3 million provided to cover wages and administration costs underscores just how urgently a longer-term resolution is needed.

The next major ASX story will hit our subscribers first

What the Liberty Bell Bay Case Reveals About Australia's Regulatory Architecture

The broader policy lesson embedded in this crisis is about systemic design failure rather than individual corporate misconduct. Several structural problems have converged to produce this outcome, and mining sustainability advocates have long argued that legacy industrial sites represent one of the most overlooked risks in the sector.

| Jurisdiction | Environmental Liability Mechanism | Applicability |

|---|---|---|

| Australian mining sector | Mandatory rehabilitation bonds | Mining operations only |

| United States (CERCLA/Superfund) | Federal cleanup fund with polluter liability | Broad industrial application |

| European Union | Environmental Liability Directive | Covers industrial operators |

| Australia (heavy industry, non-mining) | Environmental protection orders | Site-specific, no universal bond |

Australia's mining sector has, over several decades, developed a relatively robust system of financial assurance through mandatory rehabilitation bonds. That system does not extend to heavy industrial operations that are not classified as mines. The result is an uneven liability landscape where the public's financial exposure depends largely on which regulatory category a facility was assigned when it was first licensed — decades before anyone anticipated the current situation.

Potential reforms that could prevent similar situations emerging at other legacy industrial sites include:

- Extension of mandatory financial assurance requirements to all heavy industrial operations, not just those classified as mining

- Mandatory reassessment of environmental bonding obligations each time an industrial site changes ownership

- Legislative reform to give environmental remediation claims higher priority status in corporate insolvency proceedings

- Regular third-party assessment of remediation liability for long-operating industrial sites, regardless of their operational status

Furthermore, a robust definitive feasibility study framework applied at the point of each ownership transfer could have flagged these liabilities far earlier, giving regulators the opportunity to impose appropriate bonding conditions before insolvency became a risk.

Key Takeaways on Liberty Bell Bay Remediation Costs

- The estimated cost of fully rehabilitating the Liberty Bell Bay site stands at approximately $200 million, confirmed by the Tasmanian government as broadly accurate

- No environmental bond or dedicated rehabilitation fund exists to cover these costs, unlike the standard framework applied to Australian mining operations

- Under Australian corporations law, liquidators can disclaim the property, potentially transferring the full liability to the Tasmanian state government

- The EPA is classified as an unsecured creditor in liquidation proceedings — a position that historically results in little to no financial recovery

- A successful sale remains the fiscally prudent outcome for Tasmania, but negotiations have failed to produce a buyer willing to accept the site's obligations

- The case exposes a significant and largely unaddressed regulatory gap in Australia's approach to environmental liability for legacy heavy industrial facilities

- Administration fees are accumulating at an estimated $500,000 per week, adding urgency to the resolution timeline

Disclaimer: This article is based on publicly available reporting and expert commentary. Forward-looking statements regarding remediation costs, legal outcomes, and government liability are subject to change depending on decisions made during administration and any subsequent liquidation process. Nothing in this article constitutes legal or financial advice.

Want to Capitalise on Significant ASX Mineral Discoveries Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — explore the historic returns major discoveries have generated to understand the opportunity, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.