July 17, 2026

When Restraint Becomes Strategy: The Case for Pausing Production in Junior Graphite Mining

There is a persistent assumption in junior mining circles that production equals progress. Volume on the stockpile, tonnes through the plant, shipments to port — these are the visible signals investors and analysts often use as proxies for operational health. However, this framing breaks down quickly when the underlying geology is insufficiently understood, when infrastructure has not been sized for the ore body's true characteristics, or when a plant is being pushed through a resource with insufficient confidence in grade continuity.

In those scenarios, producing more is not building value — it is consuming it. This tension sits at the heart of the decision by Total Graphite to halt production at its Vatomina mine in Madagascar. Rather than continuing to run an operation that an independent technical review had identified as improvable across multiple dimensions, the company chose to stop, analyse, and rebuild from a stronger foundation.

The decision illustrates a broader principle that separates disciplined operators from those chasing short-term output metrics at the expense of long-term asset quality. Furthermore, understanding this principle is essential when evaluating any junior producer navigating the graphite industry challenges inherent in early-stage development.

When big ASX news breaks, our subscribers know first

Understanding What the Independent Technical Review Actually Found

An independent technical review at Vatomina identified improvement opportunities across four distinct operational domains: geological drilling, mine planning, physical infrastructure, and plant performance. Each of these domains is interconnected — a mine plan built on inadequate geological data will produce incorrect scheduling assumptions, which in turn places the wrong feed material through a plant at the wrong time.

Why Geological Variability Matters So Much

In graphite mining specifically, geological variability is a particularly significant risk factor. Natural flake graphite deposits, especially those found in East African metamorphic belts, can exhibit pronounced lateral and vertical grade variability. The size distribution of graphite flakes — which directly determines product value — can shift meaningfully across relatively short distances within a single orebody.

Without sufficient drill density to characterise this variability, a mine operator is effectively making blind sequencing decisions. Consequently, the independent review's findings at Vatomina are consistent with a pattern seen across junior graphite developers globally: early-stage operations often underestimate the geological complexity of their deposits until they begin physically interacting with the ore at production scale.

The restart period at Vatomina, rather than being a failure, has functioned as an extended geological learning exercise — one that has materially improved the company's understanding of what the deposit actually requires. Careful drill results interpretation will therefore be central to rebuilding confidence in the mine plan going forward.

The SRK Competent Person's Report and Its Resource Implications

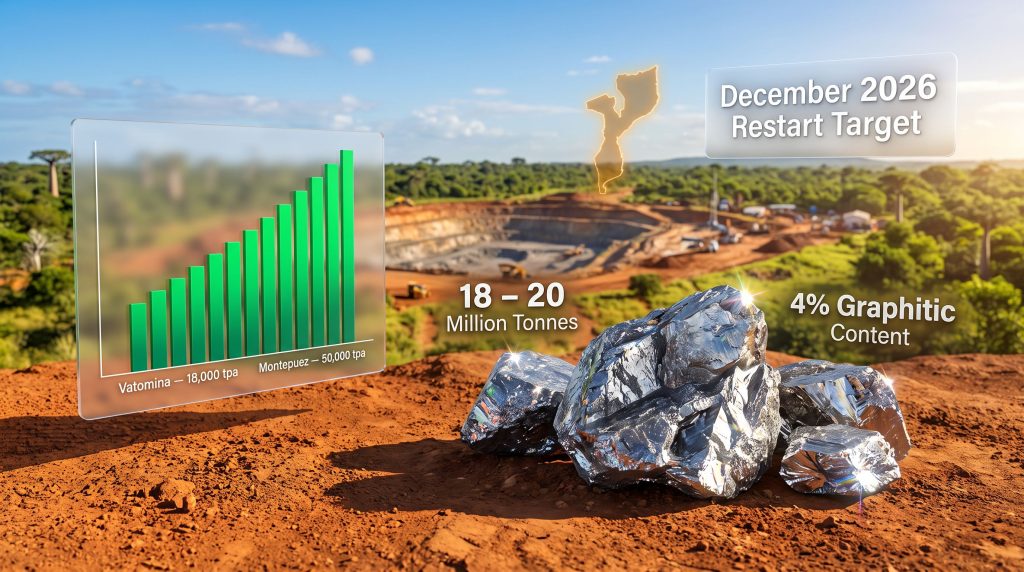

A critical piece of context is the SRK Consulting Competent Person's Report completed in March 2025, which estimated an exploration target of 18 million to 20 million tonnes at Vatomina with a 4% graphitic content grade. This stands in notable contrast to the existing mineral resource estimate of 6.20 million tonnes at 3.80% TGC (Total Graphitic Carbon).

The exploration target figure is not a mineral resource — it represents a conceptual quantity that requires further drilling to confirm. However, the gap between the existing resource and the SRK exploration target is substantial enough to fundamentally reframe how the deposit should be approached.

If even a portion of that target is converted to resource through the current drilling programme, the operational case for Vatomina changes considerably, supporting longer mine life estimates, improved infrastructure utilisation rates, and stronger offtake negotiation positions.

The distinction between a mineral resource and an exploration target is critical for investors. An exploration target is not JORC-compliant and carries significant uncertainty. It represents a geological hypothesis supported by available data, not a confirmed inventory. Investors should weigh this distinction carefully when assessing forward-looking resource statements.

The grade improvement from 3.80% TGC to 4% TGC implied by the SRK exploration target may appear modest in percentage terms, but in graphite processing economics, marginal grade improvements translate directly into reduced processing costs per tonne of product and improved recovery rates. For more on downstream processing economics, both are highly sensitive variables in project-level financial modelling.

Vatomina Mine: Key Operational Parameters at a Glance

| Metric | Detail |

|---|---|

| Location | Madagascar |

| Nameplate Production Capacity | 18,000 tonnes per annum |

| Product Purity | Up to 97% natural flake graphite |

| Existing Mineral Resource | 6.20 Mt at 3.80% TGC |

| SRK Exploration Target | 18 to 20 million tonnes at 4% graphitic content |

| Targeted Post-Restart Rate | Greater than 1,000 MT per month |

| Planned Production Restart | December 2026 |

Madagascar as a Graphite Province: Opportunity Alongside Complexity

Madagascar occupies a distinctive position within the global natural flake graphite landscape. The island's geology — dominated by Precambrian metamorphic rocks — is highly prospective for large-tonne, high-grade graphite deposits. Several significant graphite projects have advanced through various development stages in Madagascar over the past decade, reinforcing the jurisdiction's geological credentials.

However, Madagascar also presents genuine operational complexity for junior miners. Road infrastructure in graphite-producing regions can be challenging, port logistics require careful management, and the wet season imposes meaningful constraints on both mining and transport operations.

These factors mean that a mine operating with insufficient geological confidence faces compounding risks: grade variability in the pit interacts with logistical constraints to create unpredictable production profiles, which in turn complicates relationships with offtake partners and financial institutions. The decision to pause at Vatomina and invest in drilling and infrastructure upgrades is partly a response to these realities.

The Four-Pillar Optimisation Programme at Vatomina

The work being undertaken during the suspension is structured around four distinct workstreams, each addressing a specific weakness identified by the independent technical review:

- Targeted geological drilling — acquiring subsurface data at sufficient density to reduce grade uncertainty and support a materially improved resource model and mine plan.

- Mine plan revision — rebuilding the extraction sequence and scheduling framework using updated geological inputs, ensuring the right material is mined in the right order.

- Infrastructure upgrades — addressing physical bottlenecks and constraints identified during the operational restart period, covering access, water management, and site logistics.

- Plant optimisation — refining the processing circuit to improve consistency and recovery rates, with the goal of sustaining output reliably above the 1,000 MT per month threshold post-restart.

The drilling programme is the critical path variable. Every other workstream depends in part on what the drilling reveals. If drill results confirm the upper range of the SRK exploration target, the revised mine plan will look substantially different — and the capital case for infrastructure and plant upgrades becomes correspondingly stronger.

Financial Position and Capital Allocation Priorities

As at July 16, 2026, Total Graphite held an unrestricted cash balance of USD $1.5 million, with total cash of USD $3.8 million including a $2.3 million bank guarantee supporting its Mozambique project pipeline.

| Financial Metric | Value |

|---|---|

| Unrestricted Cash (as at July 16, 2026) | USD $1.5 million |

| Total Cash Including Restricted Funds | USD $3.8 million |

| Bank Guarantee (Mozambique Projects) | USD $2.3 million |

For a junior developer running parallel programmes across two African jurisdictions, this cash position requires careful management. The company has identified the drilling programme at Vatomina and the Montepuez Definitive Feasibility Study update as its highest-priority uses of capital — a signal that management is prioritising geological knowledge creation and project de-risking over maintaining optics of continuous production.

The $2.3 million bank guarantee is worth examining separately. This is not available cash — it is a committed financial instrument supporting the Mozambique project pipeline. Its existence signals that the company has made binding commitments to its Mozambique development pathway, which is relevant context for understanding why the Montepuez DFS is progressing concurrently with the Vatomina optimisation work.

The company has also indicated that its optimisation programme has generated constructive dialogue with financial institutions focused on critical minerals, including discussions around offtake-linked trade financing. This financing structure — where export receivables from confirmed offtake agreements serve as collateral for working capital facilities — is increasingly used by junior graphite producers as a bridge between project development and project finance.

The next major ASX story will hit our subscribers first

Montepuez: The Large-Scale Growth Platform in Mozambique

While Vatomina undergoes its optimisation process, Total Graphite is simultaneously advancing the Definitive Feasibility Study for its Montepuez project in Mozambique. The planned first-phase operation targets a production capacity of 50,000 tonnes per year — approximately 2.8 times the nameplate capacity of Vatomina.

This scale difference is strategically significant. Vatomina, at 18,000 tpa nameplate, is a mid-scale flake graphite operation. Montepuez, at 50,000 tpa, would position Total Graphite in a different tier of the global graphite supply landscape entirely — one where the economics of downstream integration become viable and where offtake volumes are large enough to attract strategic partners with battery supply chain exposure.

The company's stated downstream processing ambitions are directly connected to Montepuez's scale. Purified spherical graphite — the anode material used in lithium-ion batteries — commands a significant price premium over run-of-mine flake graphite. However, the capital and technical requirements for downstream processing facilities are substantial, making the 50,000 tpa production base considerably more viable.

Natural Flake Graphite Market Dynamics Driving the Strategic Logic

The broader graphite market context reinforces why Total Graphite's dual-track approach makes sense. China currently accounts for the overwhelming majority of global graphite processing capacity, and recent export restriction measures have accelerated interest in developing alternative supply chains in Western and Japanese battery markets. Indeed, the global graphite shortage driven by these dynamics makes credible alternative producers increasingly valuable.

Madagascar and Mozambique are among the highest-profile alternative graphite jurisdictions globally. Both countries host large-tonne flake graphite deposits with the geological characteristics suited to battery anode applications. For battery manufacturers and EV producers seeking to diversify away from Chinese graphite supply, projects in these jurisdictions represent genuine strategic assets — provided they can demonstrate reliable production and geological credibility.

This is precisely why operational reliability matters more than production volume for junior graphite producers at this stage of the market cycle. An operation that demonstrates consistent, well-planned output against a well-characterised resource will attract far stronger offtake interest than one that produces erratically from a poorly understood deposit.

Inconsistent production histories create significant problems in offtake negotiations. Potential off-takers seeking supply security will discount or avoid producers who cannot demonstrate grade consistency, volume predictability, and logistical reliability. The decision to temporarily pause production and optimise Vatomina is, in this context, also a commercial strategy — building the operational credibility that will support stronger offtake terms when production resumes.

Key Milestones to Monitor Through to the December 2026 Target

| Milestone | Significance | Expected Timing |

|---|---|---|

| Drilling programme results at Vatomina | Determines resource confidence and restart feasibility | Pre-December 2026 |

| Revised mine plan publication | Signals operational readiness and capital deployment plan | Q4 2026 |

| Montepuez DFS update | Defines scale, capex, and financing framework for flagship asset | 2026 ongoing |

| Production restart at Vatomina | Validates optimisation outcomes; first post-pause commercial signal | December 2026 (conditional) |

| Strategic partnership or offtake announcements | Could reshape capital structure and downstream processing pathway | Ongoing |

Indicators Worth Watching on the Downside

- Drill results that fall materially below the SRK exploration target range, reducing confidence in Vatomina's longer-term resource base.

- Cash runway compression without new financing commitments or partnership agreements that provide additional working capital.

- Delays to the Montepuez DFS that push the flagship project's timeline beyond current expectations.

Indicators That Would Signal Strengthening Execution

- Drill results confirming tonnages toward the upper bound of the 18 to 20 million tonne exploration target.

- Offtake-linked financing agreements formalised against the Montepuez DFS outcomes.

- Strategic partner announcements with credible downstream processing or battery supply chain credentials.

Frequently Asked Questions About the Vatomina Production Halt

Why has Total Graphite halts production at Vatomina mine?

The suspension follows an independent technical review that identified material improvement opportunities across geological drilling, mine planning, infrastructure, and plant performance. The company concluded that addressing these issues before resuming production would build a substantially stronger operational foundation.

When is production expected to restart at Vatomina?

Total Graphite is targeting a restart in December 2026, with a production rate exceeding 1,000 metric tonnes per month. This timeline is explicitly conditional on the progress and outcomes of the geological drilling programme currently underway.

Is this halt a sign of financial distress?

The suspension is a deliberate strategic decision rather than a distressed shutdown. The company held total cash of $3.8 million as at mid-July 2026 and is actively engaging with financial institutions around critical minerals financing mechanisms, including offtake-linked trade facilities.

What did SRK Consulting's report reveal about Vatomina's resource potential?

SRK Consulting's Competent Person's Report estimated an exploration target of 18 million to 20 million tonnes at a 4% graphitic content grade. This substantially exceeds the existing mineral resource estimate of 6.20 million tonnes at 3.80% TGC, though it remains subject to confirmation through further drilling and should not be treated as a JORC-compliant resource.

What is the Montepuez project and why does it matter?

Montepuez is Total Graphite's flagship development in Mozambique, with a planned first-phase capacity of 50,000 tonnes per year. A Definitive Feasibility Study is currently being updated and represents the company's primary long-term growth vehicle, as well as the platform most suited to supporting downstream processing and strategic partnership structures.

How should investors interpret the dual-track approach across Vatomina and Montepuez?

The parallel advancement of Vatomina optimisation and the Montepuez DFS reflects a capital allocation decision by the board to maximise geological knowledge and project bankability simultaneously. However, managing two significant work programmes against a $1.5 million unrestricted cash position requires careful monitoring of financing progress and milestone delivery.

This article is intended for informational purposes only and does not constitute financial advice. Statements regarding exploration targets, production timelines, and financial projections involve inherent uncertainty. Investors should conduct their own due diligence and consult a licensed financial adviser before making investment decisions. Exploration targets referenced in this article are conceptual in nature and require further drilling to establish whether they can be converted into mineral resources.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across graphite and more than 30 other commodities — turning complex data into actionable insights for investors at every level. Explore historic discoveries and their returns, then begin your 14-day free trial to position yourself ahead of the broader market.