May 23, 2026

The convergence of global supply chain vulnerabilities and geopolitical tensions has fundamentally altered how nations approach critical mineral security. As traditional supply networks face unprecedented disruption, Arctic territories have emerged as pivotal elements in reshaping industrial resource flows. Greenland approves mining permit for EU-backed graphite project, marking a significant milestone in this transformation, which reflects deeper structural changes in how advanced economies conceptualise strategic autonomy and technological sovereignty.

Resource diversification strategies now extend beyond conventional market considerations to encompass national security frameworks and alliance-building mechanisms. The integration of defence industrial base requirements with commercial mining operations represents a paradigm shift in how governments evaluate resource projects. This evolution has created unique opportunities for regions previously considered peripheral to global supply chains.

What Makes Arctic Resource Development Strategically Critical in 2025?

Arctic mineral development has gained strategic significance as Western economies seek alternatives to traditional supply sources. The convergence of climate accessibility improvements and technological advances has opened previously inaccessible deposits to commercial exploitation. These developments coincide with heightened awareness of supply chain concentration risks among NATO allies and European Union member states.

Resource security frameworks developed over the past decade now prioritise geographic diversification and alliance-based sourcing structures. The emphasis on "friend-shoring" has elevated Arctic territories from marginal prospects to core components of strategic mineral planning. This shift reflects broader recognition that industrial capacity and defence capabilities depend fundamentally on secure access to critical materials, particularly in light of the US–China trade war impact on global supply chains.

Three Major Permits Issued in 2025: A Pattern Analysis

Greenland approves mining permit for EU-backed graphite project represents one of three major exploitation licenses issued in 2025, signalling a coordinated approach to resource development rather than isolated project decisions. This pattern suggests systematic policy changes designed to accelerate responsible mining investment while maintaining environmental and social safeguards.

The permits span multiple critical minerals including graphite, gold, and molybdenum, indicating diversified resource development strategies. Each approval represents extensive regulatory review processes that balance commercial viability with Arctic-specific operational requirements. The timing of these permits reflects coordinated international pressure to establish alternative supply chains for Western industrial needs.

EU Strategic Project Designation Under Critical Raw Materials Act

The European Union's Strategic Project designation for Greenlandic mineral development represents a significant policy evolution in critical materials procurement. Under the Critical Raw Materials Act implemented in 2025, qualifying projects receive preferential regulatory treatment and enhanced funding access through the European Raw Materials Alliance framework.

This designation establishes formal EU commitment to Arctic resource development as a core component of industrial strategy. The recognition extends beyond financial support to encompass technical assistance, infrastructure development coordination, and preferential market access arrangements. Such comprehensive backing demonstrates how critical mineral projects now integrate with broader geopolitical and economic security objectives, particularly as part of a comprehensive critical minerals strategy.

When big ASX news breaks, our subscribers know first

Why Is the Amitsoq Graphite Project a Game-Changer for European Energy Security?

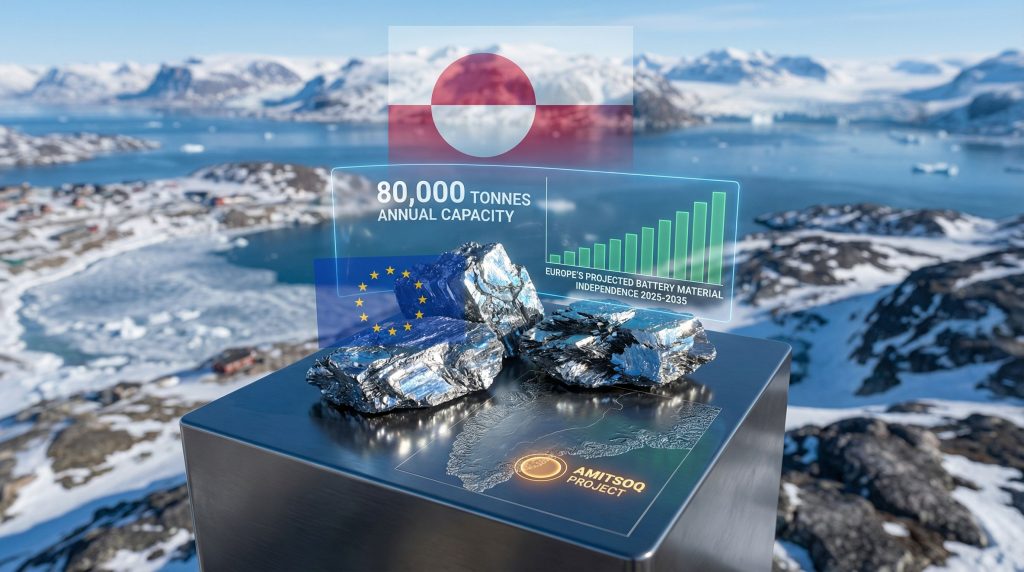

The Amitsoq deposit represents a unique combination of geological excellence and strategic positioning that addresses fundamental vulnerabilities in European industrial supply chains. Located in southern Greenland, this historically significant site offers technical specifications that meet the most demanding requirements of modern battery manufacturing and defence applications.

From a geological perspective, Amitsoq's graphite formation demonstrates exceptional grade characteristics developed through optimal metamorphic conditions over millions of years. The deposit's flake graphite structure exhibits high crystallinity levels essential for lithium-ion battery anode performance. These technical attributes, combined with substantial tonnage potential, position Amitsoq as a globally significant resource asset, particularly as the mining industry evolution continues to prioritise strategic resource development.

Historical Production Data and Grade Analysis

The Amitsoq graphite deposit operated commercially until 1922, establishing a production history that spans over a century of dormancy. Historical records indicate substantial ore reserves with exceptional grade characteristics that attracted early 20th-century mining investment despite primitive extraction technologies and remote location challenges.

| Deposit Comparison | Amitsoq | Global Average |

|---|---|---|

| Annual Concentrate Production | 80,000 tonnes | Varies by deposit |

| Ore Processing Volume | 400,000 tonnes | Varies by grade |

| Grade Classification | Highest global tier | Variable |

| Crystallinity Level | High | Variable |

| Last Operation | 1922 | Varies by deposit |

The concentration ratio of approximately 5:1 (ore to concentrate) demonstrates favourable processing economics compared to lower-grade deposits requiring more intensive beneficiation processes. This efficiency translates to reduced environmental impact per unit of graphite produced and improved project economics over the 30-year license period.

Flake Graphite Quality Specifications for Battery Applications

Modern lithium-ion battery manufacturing requires graphite with specific crystalline structures and purity levels that few global deposits can provide without extensive processing. Amitsoq's natural flake graphite exhibits crystallinity characteristics that minimise processing requirements whilst maximising electrochemical performance in battery applications.

The deposit's graphite formation process created large flake sizes with minimal structural defects, essential for maintaining battery capacity over multiple charge cycles. These technical specifications align precisely with automotive battery requirements where performance degradation directly impacts vehicle range and lifespan. Defence applications require even higher purity standards, which Amitsoq's geological formation naturally provides.

European Raw Materials Alliance Backing and Funding Structure

The European Raw Materials Alliance has provided comprehensive project backing that extends beyond traditional financing to encompass technical support, market development, and supply chain integration. This alliance structure represents coordinated EU policy to establish secure critical mineral supply chains independent of geopolitically sensitive sources.

Alliance support includes risk mitigation mechanisms that reduce private investor exposure to Arctic operational challenges. The funding structure combines public sector guarantee programs with private equity participation, creating hybrid financing models specifically designed for strategic resource projects. This approach enables commercially viable development whilst maintaining European control over critical supply chains, supporting broader energy transition security objectives.

How Does This Development Address China's Export Control Restrictions?

China's December 2024 implementation of tightened graphite export controls fundamentally altered global supply dynamics for battery and defence industries. These restrictions encompass both raw graphite materials and processed products, creating immediate supply security concerns for Western manufacturers dependent on Chinese sources. The measures represent strategic use of resource dominance to influence geopolitical relationships and industrial policy decisions.

The timing of Chinese export controls coincided with escalating trade tensions and technology transfer restrictions, indicating coordinated economic strategy rather than purely commercial considerations. Western nations recognised these controls as systematic attempts to leverage resource dependencies for broader geopolitical advantage, accelerating efforts to establish alternative supply sources.

December 2024 Chinese Graphite Export Tightening Impact

China's export control implementation affected multiple graphite product categories through licensing requirements, quota systems, and quality restrictions. The measures targeted high-purity graphite products essential for advanced battery applications whilst maintaining availability of lower-grade materials for traditional industrial uses.

Manufacturing sectors experienced immediate supply chain disruptions as Chinese suppliers reduced export volumes and increased pricing for available materials. European battery manufacturers reported supply shortages that threatened production schedules for electric vehicle programmes and energy storage projects. These disruptions demonstrated the vulnerability of Western industrial capacity to single-source dependencies, according to Mining.com's analysis of critical materials markets.

Both NATO and the European Union have designated graphite as critical raw material, particularly as China tightened export controls on the mineral, highlighting the strategic importance of securing alternative supply sources.

NATO and EU Critical Materials Designation Timeline

NATO's formal designation of graphite as a critical material reflects alliance-wide recognition of supply chain vulnerabilities that could compromise defence industrial capacity. This designation enables coordinated procurement strategies, joint stockpiling programmes, and shared technology development initiatives among member nations.

The EU's parallel designation under its Critical Raw Materials Act established regulatory frameworks that prioritise alternative source development and reduce dependence on geopolitically sensitive suppliers. These designations create formal policy mechanisms for supporting projects like Amitsoq through public funding, regulatory streamlining, and market access guarantees.

Supply Chain Diversification Scenarios for European Manufacturers

European industrial strategy now emphasises geographic diversification of critical material sources to prevent single-point-of-failure vulnerabilities. Greenland approves mining permit for EU-backed graphite project represents one component of broader diversification initiatives that include African graphite deposits, Australian sources, and North American production capacity.

- Short-term supply security: Emergency stockpiling and alternative sourcing arrangements

- Medium-term diversification: Multiple supplier relationships with NATO allies and partner nations

- Long-term strategic autonomy: Domestic and allied production capacity meeting 80% of requirements

- Technology development: Advanced processing capabilities reducing dependence on foreign value-added products

Manufacturers are implementing dual-sourcing strategies that balance cost optimisation with supply security requirements. These approaches include long-term contracts with multiple suppliers, strategic inventory management, and investment in alternative materials research to reduce overall graphite dependence.

What Are the Economic and Operational Projections for Greenland's Mining Sector?

Greenland's 30-year license framework represents a fundamental shift toward long-term resource development strategies that provide investors with sufficient time horizons for substantial capital investment recovery. This extended licensing approach enables comprehensive infrastructure development, community benefit programmes, and environmental management systems that support sustainable mining operations.

The operational timeline extends from initial development through full production capacity and eventual closure, requiring integrated planning across multiple decades. This comprehensive approach addresses Arctic-specific challenges including seasonal accessibility, extreme weather conditions, and remote location logistics that traditional mining projects rarely encounter, reflecting broader Greenland mineral strategy developments.

30-Year License Framework and Investment Implications

The extended license duration provides investors with sufficient certainty to justify substantial capital expenditures required for Arctic mining operations. Infrastructure development costs in Greenland exceed conventional mining projects due to remote location requirements, specialised equipment needs, and extreme weather preparation measures.

| License Comparison 2025 | Amitsoq Graphite | Gold Projects | Molybdenum Development |

|---|---|---|---|

| License Duration | 30 years | Various durations | Strategic timeline |

| Resource Type | Flake graphite | Precious metal | Strategic metal |

| Production Timeline | 2026-2056 | Varies by project | Varies by project |

| Strategic Designation | EU Strategic Project | National interest | Defence applications |

| Alliance Backing | European Raw Materials | Limited | Potential NATO interest |

Investment requirements encompass not only extraction and processing facilities but also comprehensive logistics infrastructure including port facilities, transportation networks, and worker accommodation systems. The 30-year timeframe enables staged development approaches that spread capital requirements over extended periods whilst generating revenue to support expansion phases.

Infrastructure Development Requirements in Southern Greenland

Southern Greenland's mining development requires substantial infrastructure investment to support year-round operations in Arctic conditions. Transportation networks must accommodate heavy equipment and bulk materials transport between remote mining sites and shipping facilities. Power generation systems need redundant capacity to ensure continuous operations despite weather-related disruptions.

Port facility development presents unique challenges due to seasonal ice conditions and deep-water access requirements for large cargo vessels. Storage facilities must withstand extreme temperature variations whilst maintaining material quality standards essential for battery-grade graphite applications. Communication systems require satellite connectivity and backup protocols to maintain operational coordination and safety monitoring.

Employment and Local Economic Impact Modelling

The Amitsoq project will create direct employment opportunities across multiple skill levels from technical specialists to general labourers, with preference for Greenlandic residents where feasible. Training programmes will develop local expertise in mining operations, equipment maintenance, and environmental monitoring to maximise long-term employment benefits for communities.

Economic multiplier effects extend beyond direct mining employment to encompass service industries, transportation, accommodation, and local supply networks. Revenue sharing agreements with Greenlandic communities ensure equitable benefit distribution whilst supporting traditional lifestyle preservation and cultural continuity. These arrangements balance resource development benefits with indigenous rights and environmental protection requirements.

How Will This Project Influence Global Graphite Market Dynamics?

The Amitsoq project's 80,000 tonnes annual production capacity represents approximately 2-3% of current global graphite demand, creating meaningful supply diversification for Western markets. This production level, whilst significant, reflects the massive scale of global graphite consumption driven by expanding battery manufacturing and traditional industrial applications.

Market impact extends beyond volume contributions to encompass supply chain reliability, pricing stability, and technological advancement in graphite processing. Western manufacturers gain access to reliable, alliance-based supply sources that reduce exposure to geopolitical supply disruptions whilst maintaining competitive cost structures essential for commercial viability.

Current Global Production Leaders vs New Arctic Capacity

Global graphite production remains concentrated among a limited number of producing countries, with China maintaining dominant market position through both natural graphite mining and synthetic graphite manufacturing. Madagascar, Brazil, and Mozambique provide alternative natural graphite sources, but processing capacity limitations reduce their strategic value for high-specification applications.

Amitsoq's production capacity will position it among the top ten global graphite operations whilst providing the only significant Arctic-based supply source. This geographic diversification offers unique logistical advantages for European markets whilst reducing transportation distances compared to African or South American alternatives. Strategic positioning enables competitive delivered costs despite higher operating expenses associated with Arctic conditions.

Lithium-Ion Battery Industry Demand Projections Through 2030

Battery industry demand for graphite continues expanding rapidly driven by electric vehicle adoption, energy storage system deployment, and portable electronics growth. Industry projections indicate graphite demand could triple by 2030 as automotive electrification accelerates and grid-scale storage deployment increases to support renewable energy integration.

Automotive applications alone could consume over 2 million tonnes of battery-grade graphite annually by 2030, representing substantial growth from current consumption levels. Energy storage systems for renewable energy integration require additional graphite volumes, creating compound demand growth across multiple application sectors. Defence technology requirements add incremental but strategically critical demand components.

Defence Technology Applications and Strategic Stockpiling

Defence applications require the highest purity graphite specifications for specialised electronics, aerospace systems, and advanced manufacturing processes. These applications represent relatively small volumes compared to battery markets but carry disproportionate strategic significance due to national security implications and limited alternative materials options.

Strategic stockpiling programmes implemented by NATO allies and other Western nations create additional demand beyond commercial consumption. These stockpiles provide supply security buffers during geopolitical disruptions whilst supporting defence industrial base requirements. Stockpiling demand patterns differ from commercial markets, emphasising long-term contracts and quality assurance over cost optimisation.

What Regulatory and Environmental Frameworks Enable Responsible Arctic Mining?

Greenland's mining regulatory framework has evolved to address Arctic-specific operational challenges whilst maintaining international environmental standards and indigenous rights protections. The regulatory structure balances resource development opportunities with environmental conservation and community welfare requirements through comprehensive assessment and monitoring systems.

Environmental impact assessment requirements encompass traditional ecological considerations as well as Arctic-specific factors including permafrost stability, wildlife migration patterns, and marine ecosystem protection. Climate change impacts on Arctic environments require adaptive management approaches that respond to changing conditions over project lifecycles spanning multiple decades.

Greenland's Updated Mining Legislation and Approval Process

Recent legislative updates streamlined permitting processes whilst strengthening environmental protection requirements and community consultation mechanisms. The approval process now incorporates international best practices for Arctic mining operations whilst maintaining sovereignty over resource development decisions and revenue allocation.

Regulatory frameworks address unique Arctic challenges including seasonal accessibility, extreme weather operations, and environmental monitoring in remote locations. Permit conditions specify performance standards for environmental protection, community engagement, and operational safety that reflect Arctic-specific risks and opportunities. Compliance monitoring systems utilise remote sensing technology and periodic inspections adapted to Arctic conditions.

Environmental Impact Assessment Requirements for Arctic Operations

Arctic environmental impact assessments address ecosystems that exhibit extreme sensitivity to disturbance whilst supporting unique biodiversity adapted to harsh conditions. Assessment protocols evaluate potential impacts on marine environments, terrestrial wildlife, vegetation communities, and subsurface hydrology systems that differ substantially from temperate climate ecosystems.

Climate change considerations require long-term impact modelling that accounts for changing Arctic conditions over project lifecycles. Permafrost stability, sea ice patterns, and precipitation changes affect both operational feasibility and environmental protection measures. Assessment requirements include adaptive management protocols that respond to evolving environmental conditions and improved scientific understanding of Arctic ecosystem dynamics.

Indigenous Community Consultation and Benefit-Sharing Models

Community consultation processes recognise indigenous rights whilst facilitating responsible resource development that provides equitable benefit distribution. Consultation frameworks ensure meaningful participation in project planning, environmental protection measures, and employment opportunity development whilst respecting traditional land use patterns and cultural practices.

Benefit-sharing agreements provide direct financial returns to affected communities through revenue sharing, employment preferences, and local business development support. These arrangements balance immediate economic benefits with long-term community sustainability and cultural preservation requirements. Agreement structures adapt international best practices to Arctic conditions and indigenous governance systems.

The next major ASX story will hit our subscribers first

Which Investment and Partnership Opportunities Are Emerging?

GreenRoc Mining's London Stock Exchange listing provides institutional investors with exposure to Arctic critical mineral development through established capital market mechanisms. The company's structure enables European investors to participate in strategic resource projects whilst maintaining regulatory compliance and transparency standards required for public market participation.

Partnership opportunities extend beyond traditional mining investment models to encompass strategic alliances with battery manufacturers, defence contractors, and government agencies seeking secure supply chain access. These partnerships create hybrid business models that combine commercial returns with strategic value for industrial customers and national security stakeholders.

GreenRoc Mining's London Listing and Market Performance

Public market access through London listing provides GreenRoc with capital raising capabilities essential for Arctic project development whilst offering investors transparent reporting and governance standards. Market performance reflects investor appetite for critical mineral exposure combined with geopolitical risk considerations associated with Arctic operations and international market dynamics.

Institutional investor interest in ESG-compliant critical mineral projects has increased substantially as sustainability requirements integrate with supply chain security objectives. GreenRoc's operational approach emphasises environmental protection and community engagement standards that align with institutional investment criteria whilst maintaining commercial viability in challenging Arctic conditions, as highlighted by TipRanks' analysis of the company's prospects.

European Raw Materials Alliance Funding Mechanisms

Alliance funding combines public sector risk mitigation with private sector efficiency through innovative financial structures designed for strategic resource projects. These mechanisms include loan guarantees, equity participation, and revenue sharing arrangements that reduce private investor risk whilst maintaining commercial incentive structures.

Funding availability extends beyond initial capital requirements to encompass expansion financing, technology development support, and market access facilitation. The Alliance approach creates coordinated European capability for critical mineral project development whilst reducing dependence on non-allied financing sources that could compromise supply chain security objectives.

Potential Joint Venture Structures with Battery Manufacturers

Battery manufacturer partnerships offer secured market access and technical specification guidance that enhance project viability whilst providing manufacturers with supply chain control and quality assurance. Joint venture structures enable shared investment in processing facilities, quality control systems, and logistics infrastructure optimised for battery industry requirements.

Partnership arrangements could encompass exclusive supply agreements, technology sharing, and co-investment in value-added processing capabilities that increase graphite product value whilst strengthening manufacturer supply chain security. These relationships create mutual dependencies that support long-term commercial relationships beyond traditional buyer-supplier arrangements.

How Do Trump Administration Interests Align with EU Arctic Strategy?

The Trump administration's renewed interest in Greenland resources reflects broader US strategic competition with China and efforts to secure critical mineral supply chains for American industrial and defence needs. This alignment with European Union Arctic strategies creates opportunities for transatlantic cooperation on resource development whilst addressing shared concerns about Chinese supply chain dominance.

Strategic convergence between US and EU approaches enables coordinated investment, technology sharing, and market development initiatives that strengthen Western alliance capabilities whilst reducing collective dependence on geopolitically sensitive supply sources. This cooperation extends beyond bilateral relationships to encompass NATO alliance frameworks and broader democratic coalition building.

US-Greenland Relations and Critical Mineral Security

American strategic interest in Greenland encompasses military positioning, Arctic sovereignty, and critical mineral access considerations that align with Greenlandic economic development objectives. US investment and technology transfer could accelerate mining sector development whilst providing Greenland with diversified international relationships beyond traditional European connections.

Critical mineral security represents shared interest areas where US defence industrial requirements align with Greenlandic revenue generation objectives and European supply chain diversification goals. Trilateral cooperation frameworks could optimise resource development benefits whilst maintaining Greenlandic sovereignty over resource management decisions and environmental protection standards.

Transatlantic Cooperation on China Alternative Sourcing

Coordinated Western response to Chinese export controls requires systematic cooperation on alternative supply source development, technology sharing, and market access arrangements. Transatlantic frameworks enable shared investment in high-risk Arctic projects whilst distributing benefits across alliance partners according to contribution levels and strategic requirements.

Alternative sourcing strategies encompass not only raw material access but also processing capability development, recycling technology advancement, and substitution research that reduces overall Chinese dependency across critical mineral value chains. Cooperation agreements could establish shared strategic reserves, coordinated procurement programmes, and joint research initiatives.

NATO Strategic Implications of Greenland Resource Development

NATO strategic planning increasingly incorporates critical mineral security as essential component of alliance defence capabilities and industrial base sustainability. Greenland approves mining permit for EU-backed graphite project contributes to alliance resilience whilst providing Denmark and European allies with enhanced strategic autonomy in defence industrial procurement.

Alliance benefits extend beyond material supply security to encompass Arctic presence, technological advancement, and economic strengthening of alliance members. Resource development creates infrastructure and capabilities that support broader NATO objectives whilst generating revenue streams that strengthen alliance member economic foundations and defence spending capacity.

What Are the Long-Term Scenarios for Greenland as a Mining Hub?

Greenland's potential evolution into a comprehensive mining hub depends on successful development of multiple critical mineral projects combined with infrastructure investment that creates synergistic operational benefits across the sector. The foundation established by early projects like Amitsoq enables subsequent developments to leverage shared infrastructure whilst reducing individual project development costs.

Long-term scenarios encompass 15-20 major mineral projects spanning rare earths, precious metals, base metals, and energy transition materials that collectively transform Greenland into a globally significant mining jurisdiction. This transformation requires coordinated planning, substantial infrastructure investment, and international cooperation frameworks that balance resource development with environmental protection and community welfare.

Pipeline of Additional Critical Mineral Projects

Greenland's geological diversity supports development of rare earth elements, lithium, cobalt, and other materials essential for renewable energy technology and defence applications. Project pipeline development requires systematic exploration, feasibility assessment, and regulatory approval processes that build on frameworks established for initial developments like Amitsoq.

Resource development sequencing enables infrastructure sharing, workforce development, and regulatory experience accumulation that reduces costs and risks for subsequent projects. Strategic planning coordinates project timing to optimise infrastructure utilisation whilst managing environmental impacts and community capacity for industrial development.

Infrastructure Investment Requirements for Sustained Development

Comprehensive mining hub development requires substantial infrastructure investment including port facilities, transportation networks, power generation systems, and telecommunications capabilities designed for year-round Arctic operations. Infrastructure development costs justify shared investment across multiple projects whilst creating economies of scale for operations and maintenance.

Investment requirements encompass not only physical infrastructure but also human capital development through education and training programmes that create skilled workforce capacity for sustained mining operations. Healthcare, housing, and community services infrastructure ensures worker safety and community welfare whilst supporting long-term industry development.

Climate Change Impacts on Arctic Mining Accessibility

Arctic climate change creates both opportunities and challenges for mining development through extended ice-free seasons, changing precipitation patterns, and permafrost degradation effects. Operational planning must address these changing conditions through adaptive infrastructure design and flexible operational protocols.

Longer ice-free seasons enable extended shipping windows and improved logistics flexibility, potentially reducing operational costs compared to current limited-season access. However, permafrost changes and extreme weather event increases require robust infrastructure design and emergency response capabilities that add complexity and cost to operations.

Hypothetical scenario analysis suggests that if Greenland successfully develops 5-7 major critical mineral projects by 2030, it could supply 15-20% of Europe's strategic material requirements, fundamentally altering global supply chain dependencies and strengthening Western alliance resource security.

FAQ: Understanding Greenland's Mining Revolution

Why is graphite considered a critical mineral?

Graphite serves as an essential component in lithium-ion battery anodes, steel production, nuclear reactor operations, and advanced electronics manufacturing. Its unique properties including electrical conductivity, thermal resistance, and chemical stability make it irreplaceable in many high-technology applications essential for modern industrial society and defence systems.

How does Arctic mining differ from traditional operations?

Arctic mining operations face extreme weather conditions, seasonal accessibility limitations, permafrost challenges, and remote location logistics that require specialised equipment, enhanced safety protocols, and adaptive operational planning. These factors increase costs but also provide unique advantages including stable geological conditions and reduced competition for skilled workforce.

What are the main challenges facing Greenland's mining development?

Primary challenges include infrastructure development costs, environmental protection requirements, skilled workforce availability, seasonal operational limitations, and balancing resource development with indigenous rights and traditional land use patterns. Regulatory complexity and international market access also present ongoing challenges for project developers.

When will the Amitsoq project begin commercial production?

Commercial production timelines depend on final permitting completion, infrastructure development, and equipment installation processes that typically require 24-36 months from license approval. Seasonal construction limitations in Arctic conditions may extend development timelines compared to temperate climate projects, with full production capacity expected by 2026-2027.

Disclaimer: This analysis contains forward-looking projections and scenario modelling based on current information and industry trends. Actual outcomes may vary significantly due to market conditions, regulatory changes, technological developments, environmental factors, and geopolitical influences beyond current forecasting capabilities. Investment decisions should consider comprehensive risk assessment and professional financial advice.

Looking to capitalise on critical minerals supply chain disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial returns by exploring historic examples of exceptional outcomes, and begin your 30-day free trial today to position yourself ahead of the market.