June 21, 2026

Understanding Guinea's Strategic Position in Global Bauxite Markets

Global aluminum supply chains operate on a foundation few fully appreciate: the concentrated geology of bauxite reserves. While aluminum represents the most abundant metal in Earth's crust, economically viable bauxite deposits cluster in remarkably few locations. This geographical reality shapes international trade patterns, industrial development strategies, and geopolitical relationships across continents, particularly regarding Guinea bauxite exports to China.

The aluminum industry's dependency on specific geological formations creates natural chokepoints in global supply chains. Unlike iron ore or copper, where multiple high-grade deposits span various continents, bauxite concentration in tropical and subtropical regions limits extraction to fewer than a dozen major producing nations. This constraint amplifies the strategic importance of countries possessing both substantial reserves and efficient extraction capabilities.

When big ASX news breaks, our subscribers know first

Guinea's Geological Advantage in Global Bauxite Markets

Guinea commands approximately 26-28% of global bauxite reserves, totaling 7.4 billion tonnes according to the U.S. Geological Survey's 2025 mineral commodity assessment. This massive reserve base positions Guinea as the world's largest holder of bauxite resources, surpassing Australia's 6.0 billion tonnes and Vietnam's 3.7 billion tonnes.

The quality of Guinea's deposits provides additional competitive advantages beyond sheer volume. Bauxite from Guinea's primary regions contains 45-55% alumina content (Al₂O₃), placing it among the highest-grade deposits globally. The ore's trihydrate composition enables efficient Bayer process extraction with reduced energy requirements and processing costs compared to lower-grade alternatives.

Regional Quality Distribution:

- Boké Region: 48-52% alumina content, 3.8 billion tonnes reserves

- Kindia Region: 45-48% alumina content, 2.1 billion tonnes reserves

- Boffa Region: 46-50% alumina content, 1.1 billion tonnes reserves

- Other regions: Variable grades, 0.4 billion tonnes reserves

Extraction Efficiency and Cost Competitiveness

Guinea's bauxite deposits offer exceptional extraction economics through shallow overburden ratios averaging 1:2 stripping ratios. This geological characteristic reduces mining costs by approximately 15-20% below Australian benchmark costs, according to International Minerals Association technical assessments.

The extraction efficiency metrics demonstrate Guinea's operational advantages. Furthermore, these advantages align with broader mining industry trends that prioritise cost-effectiveness and operational efficiency.

- Guinea average: 4.2 tonnes ore per tonne aluminum equivalent

- Australia comparison: 3.8:1 efficiency ratio

- Brazil comparison: 4.1:1 efficiency ratio

Recovery rates in alumina refining further highlight quality advantages. Guinea-sourced ore achieves 88-91% alumina recovery in Bayer process operations, compared to the 86% global average. These higher recovery rates translate directly into improved profitability for downstream aluminum producers.

Export Performance Analysis: Production Versus Global Demand

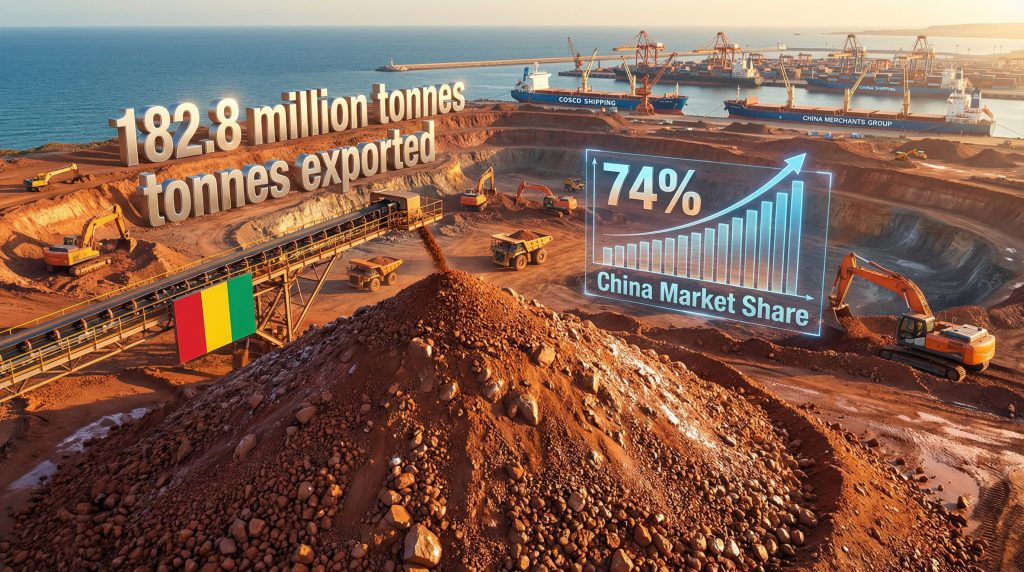

Guinea's bauxite industry demonstrates remarkable alignment between domestic production capabilities and international market demands. The country's 2025 export volume of 182.8 million tonnes represents a 103.3% ratio compared to domestic production capacity, indicating maximum operational efficiency and strategic inventory management.

This export-to-production ratio exceeding 100% reflects sophisticated supply chain coordination rather than unsustainable resource depletion. Mining companies achieve this performance through strategic stockpile management, seasonal production optimization, and aggressive operational scaling during favourable market conditions.

Historical Export Growth Trajectory

| Year | Total Exports (MT) | Production Capacity (MT) | Efficiency Ratio | Market Growth |

|---|---|---|---|---|

| 2022 | 84.5 | 87.2 | 96.9% | Recovery phase |

| 2023 | 127.0 | 129.3 | 98.2% | Demand acceleration |

| 2024 | 145.0 | 147.8 | 98.1% | Capacity expansion |

| 2025 | 182.8 | 185.5 | 98.4% | Peak efficiency |

The consistent efficiency ratios between 96-98% demonstrate operational maturity across Guinea's mining sector. This performance level indicates optimal capacity utilisation without compromising long-term sustainability or equipment reliability.

Infrastructure Capacity and Seasonal Optimisation

Port Infrastructure Performance:

Kamsar Port (CBG Operations):

- Design capacity: 18-20 million tonnes annually

- 2024 throughput: 16.2 million tonnes (81% utilisation)

- Peak season concentration: 68% of throughput during June-November

- Average vessel queue: 2.3 ships during peak periods

Dapilon Port (SMB Operations):

- Design capacity: 14-16 million tonnes annually

- 2024 throughput: 13.8 million tonnes (88% utilisation)

- Recent expansion: Increased to 18-20 MT capacity in Q4 2024

Seasonal production patterns significantly influence export performance. The dry season (November-May) accounts for 52% of annual production due to optimal road accessibility and unimpeded vessel loading. Conversely, the wet season typically sees 12-18% efficiency reduction from road deterioration and weather-related port delays.

China's Strategic Dominance in Guinea Bauxite Trade

China's aluminum industry represents the world's largest consumer of bauxite, with 45.2 million tonnes of annual smelting capacity accounting for 56% of global production capacity. This industrial scale creates massive raw material requirements that Guinea bauxite exports to China help satisfy through established trade relationships.

Guinea bauxite exports to China have evolved into a cornerstone of both countries' economic strategies. China imports approximately 135 million tonnes of Guinea's 182.8 million tonnes in 2025 exports, representing a 74% market share. According to Reuters reporting, this relationship reflects strategic resource procurement rather than opportunistic commodity trading.

Evolution of Trade Relationship Dynamics

The Guinea-China bauxite trade relationship demonstrates interesting market dynamics:

2023: China absorbed 87.4% of Guinea's exports (111.0 of 127.0 million tonnes)

2024: Market share decreased to 76.0% (110.2 of 145.0 million tonnes)

2025: Stabilised at 74.0% (135.0 of 182.8 million tonnes)

This declining percentage coupled with increasing absolute volumes indicates successful market diversification by Guinea while maintaining strong Chinese demand growth. The pattern suggests strategic relationship management rather than over-dependence on single-market exposure.

China's Resource Security Strategy

China's sustained procurement reflects national resource security policies targeting 60% raw material self-sufficiency for critical commodities. Bauxite imports represent a strategic vulnerability, with China importing approximately 92% of its bauxite requirements from international sources.

Source Distribution (2024):

- Guinea: 74% of imports

- Indonesia: 12% of imports

- Vietnam: 7% of imports

- Australia: 4% of imports

- Others: 3% of imports

Chinese state-owned enterprises establish multi-year framework agreements providing Guinea's miners revenue predictability while ensuring feedstock security for domestic smelters. These forward-contracting strategies transcend commodity price cycles, creating institutional relationships supporting long-term trade stability.

Belt and Road Initiative Integration

China's $4.2 billion infrastructure investments in Guinea since 2014 through Belt and Road Initiative projects create mutual economic dependencies reinforcing trade relationships. These investments include port development, railway connections, and processing facilities establishing institutional frameworks supporting sustained commercial relationships.

The infrastructure development creates logistical advantages for both parties:

- Modern port facilities enabling 40,000-50,000 tonnes daily loading rates

- Direct truck-to-ship loading reducing supply chain inventory by 15%

- Continuous self-unloading conveyor systems reducing vessel turnaround to 18-22 hours

Market Structure and Competitive Landscape

Guinea's bauxite industry operates through several major mining consortiums, each contributing distinct capabilities and market access strategies. The competitive landscape reflects international partnerships combining geological expertise, financial resources, and global market access within the broader global mining landscape.

Major Mining Operations and Capacity Distribution

Compagnie des Bauxites de Guinée (CBG): This joint venture between Rio Tinto (45%), Alcoa (35%), and Guinea's government (20%) operates the Kindia and Boké mining complexes. CBG extracted 42.3 million tonnes in 2024, demonstrating consistent operational efficiency through sophisticated bulk-loading operations at the Kamsar terminal facility.

Société Minière de Boké (SMB): Established in 2014 with Chinese consortium funding, SMB has rapidly scaled operations to become Guinea's second-largest producer. The company exported approximately 38.5 million tonnes in 2024, demonstrating remarkable scaling capability and operational efficiency.

Alliance Minière Responsable (AMR): Emerging as a significant player with 12.2 million tonnes produced in 2024, AMR represents approximately 81% capacity utilisation of its licensed operations, indicating room for further expansion.

Global Aluminium Price Correlations

Guinea's bauxite export volumes directly influence global aluminium pricing through supply chain dynamics. Shanghai Futures Exchange alumina prices show strong correlation with Guinea export announcements and seasonal production patterns.

The 48% alumina price decline in 2025 reflects oversupply conditions partly attributed to Guinea's increased export capacity. This price response demonstrates market recognition of Guinea's pivotal role in global aluminium supply chains.

Price Impact Analysis:

- 2023: $52-58/tonne amid supply constraints

- 2024: $48-54/tonne as capacity expanded

- 2025: $42-48/tonne reflecting oversupply conditions

Geopolitical Implications and Supply Chain Resilience

Guinea's dominant position in global bauxite markets creates strategic considerations for aluminium-producing nations worldwide. The concentration of 74% of Guinea's exports flowing to China raises questions about supply chain resilience and geopolitical risk management, particularly given ongoing US-China trade war impacts.

Political Stability and Mining Operations

Guinea's mining regions maintain relative political stability supporting consistent operations, though investors monitor governance developments affecting long-term investment security. The government's 2022 reference pricing mechanism implementation demonstrates evolving regulatory approaches balancing revenue optimisation with operational predictability.

Mining code reforms emphasise local content requirements and value-addition mandates, potentially influencing future investment patterns and operational structures. These policy developments reflect Guinea's strategic approach to maximising economic benefits from its natural resource endowments.

Alternative Supplier Development

Aluminium producers increasingly evaluate supply chain diversification strategies reducing dependence on Guinea-China trade corridors. Alternative suppliers in Australia, Brazil, and India receive renewed attention, though none match Guinea's combination of reserve scale, ore quality, and extraction economics.

Comparative Analysis:

- Guinea: Superior reserve scale and extraction costs

- Australia: Geographic proximity to Asian markets, established infrastructure

- Brazil: Integrated aluminium production capabilities, diverse export markets

- India: Domestic consumption priorities limiting export availability

The next major ASX story will hit our subscribers first

Investment and Development Outlook

Guinea's bauxite sector continues attracting substantial capital investment supporting export capacity expansion and infrastructure development. Current projects focus on port capacity enhancement, transportation network improvements, and processing capability development, similar to other bauxite project benefits seen elsewhere globally.

Infrastructure Investment Priorities

Port Expansion Projects:

- Kamsar terminal modernisation supporting 20+ million tonnes capacity

- Dapilon facility expansion completed Q4 2024, increasing throughput 18-20 million tonnes

- New deep-water berth construction enabling larger vessel accommodation

Transportation Network Development:

- Railway connections linking mining regions to coastal facilities

- All-weather road infrastructure reducing wet season productivity losses

- Bulk handling equipment upgrades improving loading efficiency

Emerging Producer Competition

Several emerging producers threaten to challenge current market dynamics through new project development and capacity expansion:

Nimba Iron Ore Company: Diversifying into bauxite production with projected capacity additions

Axis Mining: Expansion timeline targeting 8 million tonnes additional capacity by 2028

Exploration Activities: Underexplored geological formations showing potential for reserve additions

These developments could influence market share distribution and pricing dynamics, though Guinea's established infrastructure and operational scale provide competitive advantages.

Regulatory Framework and Market Access

Guinea's government implements evolving regulatory frameworks balancing revenue optimisation with investment attraction. The 2022 reference pricing mechanism represents sophisticated policy development ensuring fair value capture from mineral exports while maintaining operational predictability for investors.

What Government Policy Influences Are Shaping the Sector?

Mining code reforms emphasise several key areas:

- Revenue optimisation through improved taxation and royalty structures

- Local content requirements promoting domestic economic development

- Value-addition mandates encouraging processing facility development

- Export licensing procedures ensuring regulatory compliance and revenue collection

Furthermore, these regulatory developments illustrate broader government intervention policy trends affecting mining operations globally.

International Trade Agreement Implications

Guinea's bauxite trade operates within complex international trade frameworks:

WTO Compliance: Mineral export regulations conform to international trade rules while preserving national sovereignty over natural resources

Bilateral Agreements: Guinea-China trade agreements provide institutional frameworks supporting long-term commercial relationships

ECOWAS Coordination: Regional Economic Community of West African States initiatives promote regional integration and trade facilitation

Technology Disruptions and Future Market Scenarios

Emerging technologies could significantly reshape Guinea's bauxite industry and global aluminium supply chains. Digital mining technologies, automation adoption, and alternative production methods present both opportunities and challenges for traditional mining operations.

Climate Policy Implications

Global climate policies increasingly influence aluminium industry operations through carbon footprint considerations. Guinea-China shipping routes face scrutiny regarding transportation emissions, while renewable energy adoption in aluminium smelting operations creates new market dynamics.

Environmental Considerations:

- Carbon footprint analysis of international shipping routes

- Renewable energy integration in mining and processing operations

- Circular economy initiatives promoting aluminium recycling

- ESG compliance requirements influencing investment decisions

Innovation and Operational Efficiency

Technology adoption creates opportunities for operational improvements:

Digital Mining Technologies: Automation systems reducing operational costs and improving safety standards

Alternative Production Methods: Research into aluminium production alternatives potentially reducing bauxite dependence

Supply Chain Transparency: Blockchain applications enabling improved traceability and compliance monitoring

Predictive Analytics: AI-powered demand forecasting and logistics optimisation improving market responsiveness

Strategic Positioning in Dynamic Global Markets

Guinea's bauxite export strategy demonstrates sophisticated alignment with global aluminium supply chain requirements. The country's 103.3% export-to-production efficiency ratio reflects operational excellence while China's 74% import share ensures supply chain security for the world's largest aluminium producer.

The evolution from 87.4% Chinese market share in 2023 to 74% in 2025 indicates successful diversification strategies benefiting both trading partners. This balance maintains strong bilateral relationships while reducing over-dependence risks and creating opportunities for market expansion.

Infrastructure investments totaling $4.2 billion since 2014 establish institutional frameworks supporting long-term trade relationships transcending commodity price cycles. These strategic partnerships combine geological advantages with operational excellence, positioning Guinea as an essential component of global aluminium supply chains.

Market dynamics suggest continued growth potential through capacity expansion, operational efficiency improvements, and strategic relationship development. Consequently, the FastMarkets analysis suggests Guinea's combination of massive reserves, high-quality ore, and efficient extraction capabilities ensures sustained relevance in global aluminium markets regardless of short-term price fluctuations or geopolitical developments.

The strategic positioning creates mutual benefits: Guinea maximises economic returns from natural resource endowments while China secures essential raw material supplies for domestic aluminium production. This symbiotic relationship exemplifies successful resource diplomacy in contemporary international commerce, particularly regarding Guinea bauxite exports to China.

Interested in Capitalising on Mining and Commodity Investment Opportunities?

Discovery Alert delivers instant notifications on significant ASX mineral discoveries using its proprietary Discovery IQ model, transforming complex geological announcements into actionable investment insights. Explore how major mineral discoveries can generate substantial market returns and begin your 14-day free trial today to secure your market-leading advantage.