June 4, 2026

The Investor Psychology Behind Discounted Transformation-Phase Miners

There is a well-documented pattern in commodity equity markets where investor capital flows most aggressively toward companies that distribute cash rather than deploy it. During periods of elevated commodity prices, this behavioural tendency intensifies. Fund managers who weathered years of margin compression, write-downs, and broken project promises become acutely sensitive to capital discipline signals. When a producer announces a buyback or raises its dividend, institutional money follows. When a producer announces a major greenfield build, the opposite frequently occurs, regardless of the strategic logic underpinning the decision.

This psychological dynamic sits at the heart of why Harmony Gold ignored by investors has become a legitimate question in precious metals equity circles. The company is profitable, operationally consistent, and actively reshaping its commodity exposure in a way that, over a multi-year horizon, could substantially enhance its earnings quality. Yet its share price tells a very different story.

When big ASX news breaks, our subscribers know first

The Valuation Paradox: Strong Operations, Weak Equity Performance

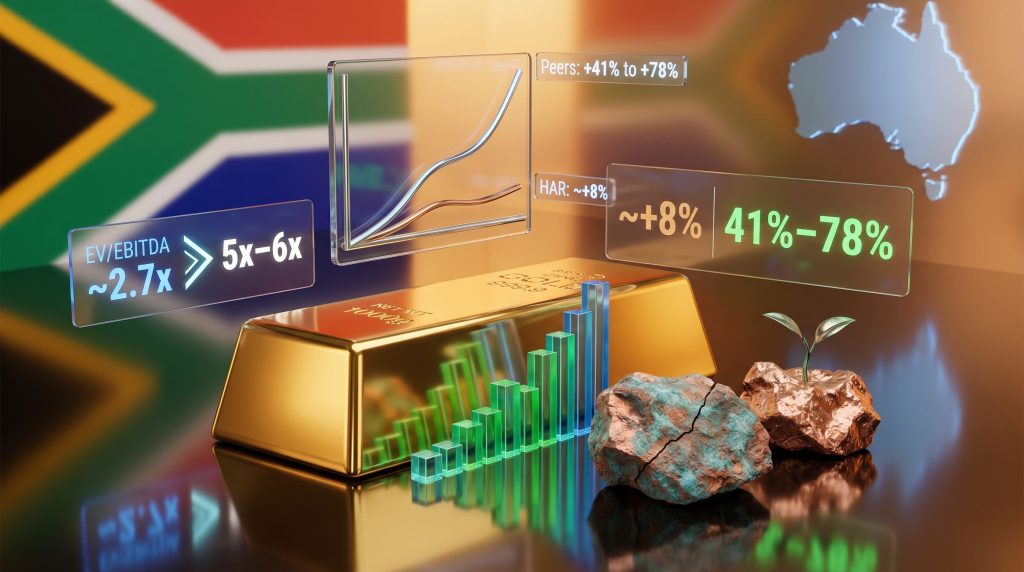

Harmony Gold trades on the Johannesburg Stock Exchange under the ticker HAR and on the New York Stock Exchange under HMY. Over the past twelve months, its shares have appreciated by roughly 8%. That number becomes striking when placed alongside the performance of its immediate peers: Gold Fields advanced approximately 41% over the same period, and AngloGold Ashanti surged close to 78%, according to analysis published by David McKay in Miningmx and the Financial Mail in June 2026.

The underperformance is not explained by operational failure. Harmony has delivered on production guidance for eleven consecutive years, a track record that is statistically rare within the global mining industry. Furthermore, current metrics across costs, ore grades, and production volumes are all tracking in line with stated targets. This is a company doing what it said it would do.

What the market is reacting to is not what Harmony is producing today, but what it is spending to build for tomorrow. The gold price outlook for miners in this environment adds further complexity to how investors are choosing to allocate capital.

The more precise question analysts are asking is not whether Harmony is being overlooked, but whether the risk discount being applied to its equity is proportionate to the actual execution challenges it faces, or whether that discount has overshot into genuine undervaluation territory.

Peer Group Cash Generation: The Scale of the Gap

To understand why investor attention has migrated away from Harmony, it is necessary to appreciate the extraordinary cash generation being delivered by its major competitors. According to data compiled by Metals Focus, a UK-based precious metals consultancy, Barrick Mining, Newmont, AngloGold Ashanti, and Gold Fields collectively generated $9.7 billion in fourth-quarter cash flow from operations after total capital expenditure.

That figure represented a 34% increase on the prior quarter and was nearly double the previous high-water mark of approximately $5 billion recorded in the third quarter of 2020 (McKay, Miningmx, June 2026). Consequently, the gold price impact on equities has been felt very differently across the sector depending on each producer's capital allocation posture.

| Metric | Harmony Gold | Major Peer Group |

|---|---|---|

| 12-Month Share Price Performance | ~+8% | +41% to +78% |

| Q4 Combined Peer Cash Flow (after Capex) | Not directly comparable | $9.7bn (34% QoQ increase) |

| Prior Cash Flow Peak (Q3 2020) | – | ~$5bn |

| Net Debt Post-Acquisition | R5.54bn | Net cash positive |

| Recovery to Net Cash (Q1 CY2026) | R1.3bn net cash | Sustained |

| Forward EV/EBITDA Multiple | ~2.7x-2.8x | 5x-6x (copper asset comparables) |

| Capex per Ounce | ~$760/oz | Sector avg. ~$600/oz (12-yr high, Q3 2025) |

The capital return behaviour accompanying this cash generation is equally significant. AngloGold Ashanti paid out more than half of a recent quarterly cash flow of R1.17 billion directly to shareholders, then followed that with a $2 billion share buyback announcement. For institutional fund managers managing risk-adjusted return mandates, these signals are powerful. Harmony, by contrast, is channelling capital into long-duration growth assets.

What Is Actually Driving the Risk Discount?

The Greenfield Problem and the McKinsey Baseline

The core of investor caution around Harmony sits in two Australian copper acquisitions. A 2024 study by McKinsey found that 80% of mining capital projects are delivered late and over budget, with cost overruns reaching as much as 43%. This baseline assumption is now embedded in how institutional investors price any miner that is actively building rather than producing. Understanding the broader copper market trends is essential context for why Harmony's Australian pivot carries strategic logic that markets are currently discounting.

Harmony's two Australian assets create a layered risk profile:

-

Eva Copper: A $1.55 billion greenfield development project in Queensland, classified as the highest-risk category in mining capital allocation. Greenfield builds require simultaneous execution across construction, procurement, permitting, and workforce mobilisation, with limited ability to draw on existing infrastructure.

-

CSA Mine: A $1.04 billion acquisition (completed October 2024) of an operating but aged underground copper-gold mine requiring meaningful rehabilitation. Harmony's CEO indicated publicly in February 2026 that derisking and debottlenecking CSA could take up to two years or potentially longer.

A particularly important disclosure gap is compounding analyst frustration. As RMB Morgan Stanley analyst Christopher Nicholson noted in coverage cited by Miningmx, the absence of quarterly Eva Copper project capex figures makes it genuinely difficult to determine whether the company's balance sheet recovery was running ahead of or behind internal expectations. When analysts cannot construct reliable forward cash flow models, institutional positioning becomes conservative by default.

The Hedge Book: Selling Forward in a Bull Market

Harmony holds the distinction of being the only major gold producer currently selling forward a significant portion of its output. Approximately 20% of production is hedged, and the mark-to-market loss on this position has reached an estimated R4.5 billion, representing a material drag on reported financial performance at precisely the moment when unhedged peers are capturing maximum gold price leverage.

The psychological impact of a visible hedge book loss during a bull market should not be underestimated. It signals, however unfairly, that the company is not fully participating in the upside that other producers are delivering to shareholders. Management's rationale is commercially defensible: providing cash flow certainty during a high-capex investment phase is standard risk management practice, and copper production is expected to eventually function as a natural portfolio hedge.

However, in a sector where peers are fully exposed to gold price upside and distributing that upside aggressively, hedging is perceived as a strategic misalignment regardless of its internal logic.

The Legacy Portfolio Consideration

Approximately 36% of Harmony's current production originates from what the company classifies as its optimised portfolio, a collection of higher-cost, lower-margin South African assets that were originally acquired at distressed valuations and restructured for cost efficiency. These assets are cash-generative when gold prices are elevated, but their margins compress rapidly in a price downturn.

This creates a category of conditional profitability that more sophisticated investors factor into their risk-adjusted valuations. Compared with peers operating higher-grade, lower-cost asset bases, this legacy exposure reinforces the perception that Harmony's earnings quality carries more commodity price sensitivity than its headline numbers suggest. Indeed, the relationship between commodity prices and mining performance is especially pronounced for producers with mixed-quality asset portfolios.

The Bull Case: Where the Valuation Argument Gets Interesting

A Copper Optionality Story Available at a Discount

The investment case for patient capital rests on a straightforward valuation arbitrage. Harmony's shares currently trade at a forward EV/EBITDA multiple of approximately 2.7x to 2.8x. Comparable copper asset transactions in the broader market are being priced at 5x to 6x EBITDA. The implication, articulated by Harmony's investor relations team in commentary reported by Miningmx, is that investors acquiring the stock at current levels are effectively purchasing a large, gold-price-leveraged business while receiving two copper development assets at negligible incremental valuation.

The copper story, in other words, is currently free. The scale of the copper ambition reinforces this argument. Harmony is targeting production of approximately 100,000 tonnes of copper per annum within three to five years, drawing on both Eva Copper and CSA. Achieving that target would position it as a meaningful participant in the global copper supply chain, with diversified commodity revenue that structurally changes how the company should be valued.

Dividend Policy Reform and Shareholder Returns

In March 2026, Harmony announced a revised dividend framework committing up to 50% of net free cash flow to shareholders, with the payout ratio linked to gross debt levels at the time of distribution. This was a direct response to sustained institutional pressure for improved capital return discipline and represents a meaningful shift in the company's stated priorities.

The effectiveness of the policy, however, is contingent on free cash flow remaining robust through the peak capex period associated with the Eva Copper build, introducing forward uncertainty that markets are pricing in with appropriate caution. Harmony's investor relations page provides further detail on the company's stated financial commitments and capital allocation framework.

What Would Trigger a Re-Rating?

For Harmony to close the valuation gap with its peer group, a convergence of specific conditions would likely be required:

-

Improved capex transparency: Regular, granular quarterly disclosure of Eva Copper project spending against budget, enabling analysts to model forward cash flows with greater confidence.

-

CSA rehabilitation milestones: Demonstrable, measurable progress on derisking the underground operation within the two-year window management has indicated.

-

Hedge book reduction pathway: A clearly communicated strategy for reducing or eliminating forward gold sales as copper production scales and provides natural cash flow diversification.

-

Sustained net cash position: Maintaining positive net cash through the peak capex window to demonstrate that balance sheet strength can coexist with aggressive capital deployment.

-

Continued gold price support: Elevated gold prices sustaining cash generation from the South African portfolio, which funds the Australian buildout without requiring additional debt.

| Scenario | Conditions | Likely Market Response |

|---|---|---|

| Bull Case | Eva on budget, CSA derisked, hedge wound down, gold sustained | Significant multiple expansion toward peer group |

| Base Case | Moderate capex overrun, CSA takes 2+ years, hedge maintained | Gradual re-rating as copper production scales |

| Bear Case | Material Eva overrun, CSA setbacks, gold price correction | Renewed net debt, dividend suspension, further de-rating |

The next major ASX story will hit our subscribers first

The Broader Pattern: Why Markets Systematically Misprice Transition-Phase Miners

Harmony's situation is not unique in mining history. The harvest-versus-reinvest bifurcation that defines institutional capital allocation during commodity price peaks has created systematic, recurring mispricing of miners in active transformation phases. Historical evidence from gold, copper, and iron ore cycles consistently shows that companies completing major capital programmes frequently deliver their strongest share price performance in the twelve to twenty-four months following project completion.

The information asymmetry between management and markets during major capital projects intensifies this dynamic. When disclosure quality is low, particularly around project-level capex, analyst confidence erodes and institutional positioning becomes defensively conservative. Harmony's disclosure gap around Eva Copper quarterly spending is not merely a technical reporting issue; it is a direct constraint on the company's ability to attract the institutional capital it needs to close the valuation gap.

UBS analyst Steve Friedman characterised Harmony's return to net cash as supporting confidence in financial year 2026 delivery, but the qualifier embedded in that assessment captures the market's mood precisely. Confidence is being rebuilt, not assumed. The distinction matters enormously in how fund managers weight the stock.

For different investor profiles, the implications diverge sharply. Contrarian mining investors in particular may find compelling logic in the gap between Harmony's current trading multiple and its embedded copper asset value. Furthermore, the broader picture for different investor categories breaks down as follows:

-

Yield-focused and short-duration funds will continue to favour peers with higher near-term cash returns and cleaner capital return frameworks.

-

Value and contrarian investors may find the gap between Harmony's trading multiple and the embedded copper asset value a compelling entry point, contingent on a tolerance for execution risk and a time horizon measured in years rather than quarters.

-

Long-term sector allocators seeking dual commodity exposure to both gold price leverage and structural copper demand driven by energy transition infrastructure may view Harmony as a differentiated vehicle unavailable elsewhere in the listed mining universe at comparable valuations.

Frequently Asked Questions

Why has Harmony Gold underperformed other gold stocks?

The primary driver is investor risk perception surrounding two large Australian copper acquisitions, one a greenfield development project and one an ageing operating mine requiring rehabilitation. In a gold bull market, institutional capital has strongly favoured companies generating and distributing near-term cash flow over those deploying capital into long-duration growth assets.

Is Harmony Gold in financial difficulty?

No. The company returned to a net cash position of approximately R1.3 billion in the first calendar quarter of 2026, having briefly entered net debt of R5.54 billion following its Australian acquisitions. Operational metrics including production, costs, and ore grades are all tracking in line with guidance.

What is Harmony Gold's copper production target?

The company is targeting approximately 100,000 tonnes of copper per annum within a three-to-five-year horizon, drawing on both the CSA operating mine and the Eva Copper greenfield project in Australia.

Why does Harmony Gold hedge its gold production?

Approximately 20% of gold output is sold forward as a risk management measure during its high-capital-expenditure investment phase. The hedge is designed to provide cash flow certainty while major project spending is elevated. Management has indicated that growing copper production will eventually provide a natural hedge, reducing reliance on forward gold sales.

How does Harmony Gold's valuation compare to peers?

On a forward EV/EBITDA basis, Harmony trades at approximately 2.7x to 2.8x, compared with 5x to 6x for comparable copper asset transactions. Its major gold peers have significantly outperformed on share price over the past twelve months, with gains of 41% to 78% versus Harmony Gold ignored by investors registering only approximately 8% appreciation.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forward-looking statements, scenario projections, and valuation comparisons involve inherent uncertainty. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. Past share price performance is not indicative of future results.

Want to Catch the Next Major Mineral Discovery Before the Market Does?

While transformation-phase miners like Harmony Gold navigate complex capital cycles, the most explosive returns in the resources sector often come from significant new discoveries — and timing is everything. Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements across more than 30 commodities, delivering real-time alerts the moment a major discovery is made, so subscribers can act ahead of the broader market. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position yourself at the forefront of the next significant find.