May 16, 2026

The Architecture Behind One of the World's Most Strategically Positioned Aluminium Companies

Few industrial commodities tell a more complex structural story than aluminium. Unlike steel or copper, aluminium's end-use profile spans an unusually wide range of sectors, from aerospace-grade sheet to everyday beverage cans, and from automotive body panels to electrical conductor cables. This breadth means that companies positioned across multiple downstream applications are inherently more resilient than those tied to a single demand vertical. For investors evaluating the Hindalco Novelis growth outlook, this multi-sector exposure is not incidental. It is the entire strategic thesis.

Understanding Hindalco's trajectory requires moving past the lens of a conventional Indian metals producer and examining instead how the company has engineered a globally integrated aluminium enterprise, with its wholly owned US-headquartered subsidiary Novelis functioning as the primary international growth engine.

When big ASX news breaks, our subscribers know first

Why Novelis Is the Defining Variable in Hindalco's Global Ambitions

Hindalco Industries, part of the Aditya Birla Group, operates across the complete aluminium and copper value chain. This includes bauxite and coal mining, alumina refining, primary smelting, and a broad range of downstream rolled and fabricated products. That vertical integration is significant. However, what has genuinely transformed Hindalco's risk-reward profile for global capital allocators is Novelis, and the broader Hindalco metals transformation that has taken shape over recent years.

Novelis is the world's largest aluminium rolling and recycling company by volume, with manufacturing operations across North America, Europe, Asia, and South America. Its contribution to Hindalco's consolidated revenue and earnings is disproportionately large relative to its asset base, largely because it operates in higher-margin, value-added segments rather than commodity-grade primary metal.

The subsidiary's three principal product areas reflect a deliberate positioning in structurally growing demand pockets:

| Novelis Business Segment | Primary End Markets | Strategic Relevance |

|---|---|---|

| Beverage Can Sheet | Packaging, FMCG | Stable, high-volume demand base |

| Automotive Aluminium Sheet | EV and ICE lightweighting | Margin-accretive, structurally growing |

| Specialty Rolled Products | Industrial, aerospace | Premium pricing, lower cyclicality |

| Recycled / Low-Carbon Aluminium | ESG-aligned supply chains | Regulatory tailwind, OEM demand pull |

This product architecture gives Novelis a significantly different earnings quality compared to upstream aluminium producers, whose margins track London Metal Exchange prices with far less insulation.

The Bay Minette Project: Why a Greenfield US Facility Changes the Equation

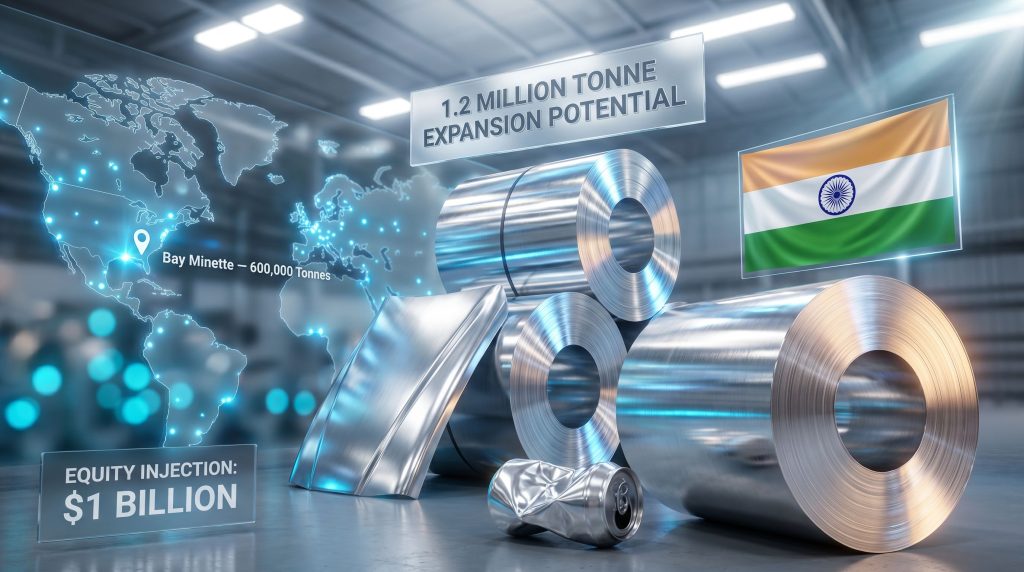

No single development is more central to the long-term Hindalco Novelis growth outlook than the Bay Minette project in Alabama. This greenfield aluminium rolling and recycling facility represents one of the largest capital commitments in North American aluminium manufacturing in recent decades.

The facility has been designed with an initial rolling capacity of 600,000 tonnes per annum, with an engineered expansion pathway that could take total output to 1.2 million tonnes, effectively doubling its footprint as demand warrants. The project is specifically calibrated to serve two high-growth demand pools: beverage can sheet for the North American packaging market and automotive aluminium sheet for domestic vehicle manufacturers.

What makes Bay Minette particularly notable from an investor perspective is its timing relative to the US trade policy environment. The impact of US aluminium tariffs has created structural cost disadvantages for importers of rolled products, meaning domestically produced can sheet and auto sheet commands both a logistics and cost advantage. A US-based rolling facility, furthermore, insulates Novelis from the import cost escalation that affects competitors relying on cross-border supply.

To fund this expansion, Hindalco has committed a total equity injection of approximately $1 billion into Novelis to support growth capital and ongoing working capital requirements. Of this, a tranche of $200 to $250 million has been specifically allocated to support near-term operational recovery and maintain project continuity during a period of elevated capital expenditure.

The Oswego Disruption: Separating Cyclical Noise from Structural Signal

Any credible analysis of the Hindalco Novelis growth outlook must address the operational disruption at the Oswego rolling mill in New York. A series of mill fires at this facility created a measurable near-term earnings headwind, compressing EBITDA, tightening free cash flow, and creating working capital pressure across Novelis' North American operations.

The critical investor distinction here is between a structural impairment and a time-bound operational setback. Analysts broadly characterise the Oswego disruption as the latter, provided that insurance recovery proceeds on projected timelines and production normalisation follows management's guidance.

Hindalco's equity injection of $200 to $250 million is a direct response to this disruption, providing balance sheet support while the facility recovers. The insurance recovery process is underway, and once completed, the proceeds are expected to accelerate cash flow reconstruction across the Novelis consolidated entity. For a deeper understanding of near-term noise versus long-term structural strength, analyst commentary highlights that FY27 remains the key inflection horizon.

The three-horizon outlook framework that most investment analysts apply to this situation is structured as follows:

| Time Horizon | Novelis Outlook | Key Drivers |

|---|---|---|

| Near Term (FY26) | Cautious | Oswego disruption, tariff costs, elevated capex |

| Medium Term (FY27) | Constructive | Oswego restart, insurance proceeds, cash flow recovery |

| Long Term (FY28+) | Positive | Bay Minette ramp-up, volume growth, higher-value product mix |

FY27 is shaping up as the pivotal inflection point where near-term headwinds transition into a more normalised, cash-generative operational environment.

India Operations: The Consolidated Earnings Floor That Often Gets Overlooked

A less discussed but critically important element of the Hindalco investment thesis is the performance of its India-based aluminium and copper operations. These businesses span the full value chain from mining through to downstream products, and they have repeatedly demonstrated the capacity to deliver record-level profitability during periods when Novelis absorbs external shocks.

This is structurally different from pure-play international aluminium companies that carry no domestic offset. When Novelis faces operational disruption or LME price compression, Hindalco's India operations provide a consolidated earnings cushion that prevents disproportionate downside impact at the group level.

The copper operations within Hindalco's India portfolio add a further layer of multi-metal diversification. Copper demand is independently driven by electrical infrastructure, renewable energy installations, and electric vehicle powertrains, meaning it does not move in lockstep with aluminium pricing cycles.

Structural Demand Drivers: Why the Long-Term Growth Story Remains Intact

The macroeconomic forces supporting sustained aluminium demand are well understood at a headline level. However, examining them in the context of Novelis-specific product positioning reveals a more precise picture of where the earnings growth is actually coming from.

| Macro Theme | Aluminium Application | Novelis Exposure Level |

|---|---|---|

| EV Adoption | Automotive body sheet, battery enclosures | High |

| Sustainable Packaging | Beverage can sheet | Very High |

| Grid Infrastructure | Conductor-grade aluminium | Moderate |

| Low-Carbon Supply Chains | Recycled / green aluminium | High |

| Construction and Urbanisation | Rolled products, facades | Moderate |

Several of these themes deserve closer examination:

Is Electric Vehicle Lightweighting a Volume Story or a Margin Story?

Electric vehicle lightweighting is not simply a volume story. Automakers transitioning to battery-electric platforms face a fundamental weight management challenge. Battery packs are significantly heavier than combustion drivetrains, which means aluminium content per vehicle must increase substantially to maintain overall vehicle weight targets and extend driving range. For Novelis, which already supplies automotive body sheet to leading global manufacturers, this structural demand acceleration represents a margin-accretive volume growth pathway.

How Is Beverage Can Sheet Demand Evolving?

Beverage can sheet demand is being simultaneously driven by two independent forces: volume growth in non-alcoholic ready-to-drink beverages across emerging markets, and the substitution of plastic packaging with aluminium across established markets due to ESG mandates from FMCG brands. Aluminium cans carry a significantly stronger sustainability profile than plastic bottles precisely because of aluminium's high recyclability. Industry data consistently shows that aluminium can be recycled indefinitely without quality degradation, a property that plastics cannot match.

What Role Does Low-Carbon Aluminium Play?

Low-carbon aluminium procurement is emerging as a separate commercial premium category within the industry. Large OEMs and beverage companies are increasingly specifying recycled-content or low-carbon-footprint aluminium in their procurement frameworks. Novelis, which operates one of the world's most extensive aluminium recycling networks, is structurally advantaged in meeting this demand. In addition, broader mining decarbonisation trends are reinforcing investor expectations that low-carbon credentials will increasingly command pricing premiums across the metals sector.

The energy economics underlying this advantage are striking. Aluminium recycling consumes approximately 95% less energy than primary smelting from bauxite. For Novelis, this is not merely a sustainability credential but a genuine cost structure advantage that becomes more commercially powerful as carbon pricing mechanisms expand and OEM supply chain decarbonisation requirements tighten.

The next major ASX story will hit our subscribers first

Bull Case vs. Bear Case: Framing the Asymmetry

Investors approaching the Hindalco Novelis growth outlook need to hold both scenarios in view simultaneously, without letting near-term noise distort the structural signal.

The bull case rests on:

- Bay Minette reaching full operational capacity at 600,000+ tonnes of North American rolling output, with the expansion pathway to 1.2 million tonnes providing a multi-year volume growth runway

- Oswego normalising ahead of schedule, with insurance proceeds accelerating cash flow recovery into FY27

- Automotive and beverage can demand sustaining multi-year volume growth as EV penetration accelerates and sustainable packaging mandates intensify

- Low-carbon aluminium commanding pricing premiums as OEM ESG mandates tighten procurement specifications globally

The bear case centres on:

- Oswego recovery timelines extending further than current management guidance, compressing FY27 earnings beyond consensus expectations

- US tariff escalation disrupting North American aluminium supply chains and squeezing margin structures for rolled product manufacturers

- LME price weakness driven by global demand softness reducing commodity-linked profitability across the aluminium sector

- Bay Minette capex overruns or construction delays straining Hindalco's balance sheet and increasing equity injection requirements beyond the current $1 billion commitment

Key Risks Every Investor in This Thesis Must Understand

The financial risks associated with this investment thesis are multi-dimensional and extend well beyond the operational disruptions at Oswego.

LME aluminium price sensitivity remains a background risk even for a downstream-focused business like Novelis. While Novelis operates on a conversion premium model where its margin is largely independent of the metal price itself, extreme commodity price dislocations can still affect customer purchasing behaviour and volume commitments.

Currency risk is particularly relevant for Hindalco shareholders who hold INR-denominated equity but whose consolidated earnings are substantially generated in USD and EUR. USD/INR movements directly affect the translated value of Novelis earnings in Hindalco's reported financials.

Tariff and trade policy uncertainty in North America represents a genuine medium-term risk variable. While Bay Minette's domestic production profile provides partial insulation, the broader North American aluminium supply chain remains exposed to policy shifts affecting raw material costs and competitive dynamics. Furthermore, broader aluminium sector consolidation across global markets may reshape competitive dynamics in ways that affect Novelis' positioning.

Concentration risk is a structural consideration. Because Novelis contributes such a disproportionate share of consolidated international earnings, any prolonged operational or market-driven weakness at the subsidiary level creates outsized impact at the Hindalco group level.

Because Novelis operates predominantly in North America and Europe, Hindalco's consolidated performance is increasingly correlated to global industrial demand cycles, US trade policy, and LME pricing dynamics that extend well beyond India's domestic economic trajectory.

Frequently Asked Questions: Hindalco Novelis Growth Outlook

What Is Novelis and Why Is It So Important to Hindalco's Investment Thesis?

Novelis is Hindalco's wholly owned subsidiary headquartered in the United States and is the world's largest aluminium rolling and recycling company by volume. It contributes a disproportionately large share of Hindalco's consolidated revenue and international earnings, with operations spanning North America, Europe, Asia, and South America. Its focus on beverage can sheet, automotive aluminium, and recycled low-carbon products gives it structural exposure to multiple long-cycle demand growth themes simultaneously.

What Is the Bay Minette Project and Why Does It Matter?

Bay Minette is a major greenfield aluminium rolling and recycling facility being developed by Novelis in Alabama, with an initial designed capacity of 600,000 tonnes per annum and a potential expansion pathway to 1.2 million tonnes. It is strategically critical because it positions Novelis with domestic US production capacity in an increasingly tariff-sensitive North American trade environment. Comparable low-carbon aluminium operations being developed elsewhere in the industry underscore just how significant the global shift toward sustainable production has become.

How Serious Is the Oswego Plant Disruption?

The Oswego mill fires have created real near-term EBITDA compression and cash flow pressure. Hindalco has committed approximately $200 to $250 million in fresh equity specifically to support operational recovery. The prevailing analytical view treats this as a time-bound setback rather than a permanent impairment, with FY27 identified as the expected recovery inflection point. Brokerages remain divided on Hindalco's near-term outlook as a result of the Novelis fire, reflecting the genuine uncertainty around recovery timelines.

Is Hindalco's Growth Story Entirely Dependent on Novelis?

No. While Novelis is the primary international growth engine, Hindalco's India operations spanning the full aluminium and copper value chain have consistently demonstrated independent earnings strength, including record profitability during periods when Novelis absorbs external headwinds.

Strategic Outlook: Three Horizons, One Coherent Investment Thesis

The most useful framework for evaluating the Hindalco Novelis growth outlook is a three-horizon model that avoids conflating near-term operational disruption with long-term structural positioning.

In the near term, FY26 is characterised by elevated caution. The Oswego disruption, combined with tariff-related cost pressures and peak capital expenditure on Bay Minette, creates a compressed earnings environment that makes short-term valuation comparisons misleading.

In the medium term, FY27 functions as the recovery inflection point. Oswego's normalisation, combined with insurance proceeds flowing back into the balance sheet and initial Bay Minette ramp-up activity, positions Novelis for a meaningful cash flow and earnings recovery that current consensus estimates are beginning to price in.

In the long term, FY28 and beyond represents the full thesis payoff horizon. Bay Minette at capacity, sustained automotive and beverage demand growth, and the accelerating commercial premium on low-carbon recycled aluminium collectively position Novelis as a structural growth asset within a consolidated group that also benefits from India's own industrial expansion trajectory.

For investors capable of tolerating near-term volatility while maintaining conviction in the structural demand thesis underpinning global aluminium consumption, the Hindalco Novelis growth outlook represents a multi-dimensional investment case built on operational recovery, capacity expansion, and the irreversible shift toward lower-carbon industrial supply chains.

This article is intended for informational purposes only and does not constitute financial advice. Readers should conduct their own due diligence or consult a qualified financial adviser before making investment decisions. Forward-looking statements, forecasts, and scenario analyses involve inherent uncertainty and actual outcomes may differ materially from projections discussed herein.

Want to Identify the Next Major Mineral Discovery Before the Broader Market Does?

While Hindalco and Novelis operate at the large-cap end of the metals and materials spectrum, some of the most compelling returns in the commodities sector have historically come from early-stage ASX mineral discoveries — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant discoveries hit the exchange. Explore Discovery Alert's dedicated discoveries page to see the historic returns that major mineral discoveries have generated, and begin a 14-day free trial to ensure you're positioned ahead of the market when the next transformative discovery is announced.