July 12, 2026

The World's Most Fragile Energy Artery: Mapping the Hormuz Crisis Across Three Scenarios

Every energy market crisis eventually reveals which geographic constraints were always there, hiding in plain sight. Iran says Hormuz shut after fresh US attacks, and the Strait of Hormuz — a 33-kilometre-wide bottleneck through which approximately 20% of global oil supply flows on any given day — has been converted from theoretical vulnerability into operational reality. This forces energy markets, shipping operators, and import-dependent governments to confront a question they have long deferred: what actually happens if Hormuz stops functioning?

The answer is not simple, and it does not arrive in a straight line. It unfolds across time horizons, institutional responses, and the cascading decisions of producers, importers, insurers, and military commands operating simultaneously under conditions of profound uncertainty.

When big ASX news breaks, our subscribers know first

Why Hormuz Is Structurally Irreplaceable

Understanding the depth of this crisis requires more than knowing the passage is narrow. It requires grasping the full range of commodities that flow through it and the economies that depend on their uninterrupted arrival. Furthermore, it demands close attention to the OPEC's influence on oil markets and how that influence is being tested in real time.

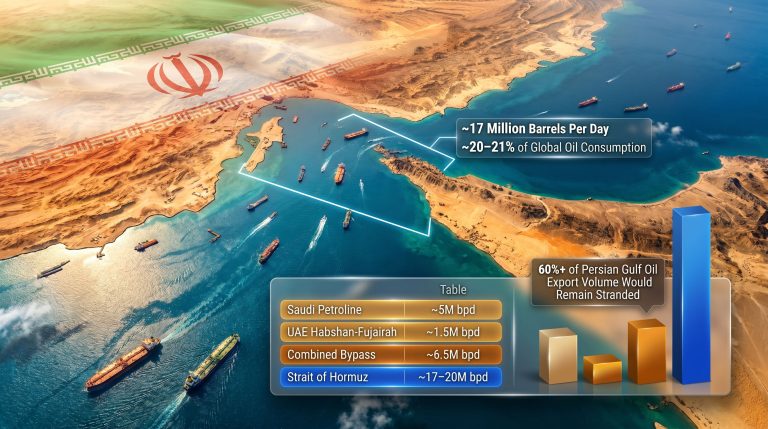

Under normal operating conditions, roughly 21 million barrels per day of crude oil, condensate, liquefied natural gas, liquefied petroleum gas, and refined petroleum products transit the strait. The primary receiving economies include China, Japan, South Korea, India, and the European Union, collectively representing a substantial share of global industrial output.

What makes Hormuz uniquely dangerous as a chokepoint is not just its volume but its irreplaceability for certain commodity categories:

- Crude oil from Saudi Arabia, Iraq, Kuwait, Iran, and the UAE has no full alternative routing at scale

- Qatar's LNG exports, which account for a significant share of the global LNG supply outlook, have no viable pipeline bypass whatsoever

- Refined products and petrochemical feedstocks bound for Asian markets face the same routing constraint

- LPG shipments destined for cooking fuel use across South and Southeast Asia transit the same narrow corridor

The only partial land alternatives are Saudi Arabia's East-West Pipeline, with a capacity of approximately 5 million b/d, and the UAE's Habshan-Fujairah Pipeline, capable of moving roughly 1.8 million b/d around the strait entirely. Combined, these bypass routes cover less than 35% of normal Hormuz transit volumes and offer zero relief for LNG exporters.

From Diplomatic Threat to Kinetic Reality: What Changed in 2026?

The current situation is structurally distinct from every prior Hormuz standoff in the modern era. Previous Iranian closure threats, most prominently during 2011–2012 and again in 2018–2019, functioned as leverage instruments deployed during diplomatic negotiations. Commercial shipping continued throughout those periods, and the threats were ultimately absorbed by markets as elevated risk premiums rather than physical disruptions.

The present conflict operates on an entirely different logic. However, several factors distinguish this escalation from its predecessors:

- Active kinetic engagement between U.S. and Iranian military forces has been ongoing since 28 February, now extending beyond eight weeks

- The U.S. military completed a third round of strikes against Iranian military targets on 11 July, hitting approximately 140 installations

- The IRGC has issued a formal closure declaration through affiliated state media, rather than diplomatic signalling through back channels

- AIS tracking data from MarineTraffic confirmed an absence of visible vessel movement through the strait following the closure announcement

- The Cyprus-flagged containership GFS Galaxy was physically attacked while transiting the strait via the southern route near the Omani coast, sustaining significant engine-room damage and an onboard fire, with one crew member reported missing

Critical Distinction: The GFS Galaxy incident represents the transition from threats against shipping as a deterrent tool to actual interdiction as operational policy. Once commercial vessels are physically struck, underwriting markets respond regardless of what official statements claim about navigability.

The crew abandoned the stricken vessel in a lifeboat after it was hit approximately nine nautical miles east of the Omani coastline, with its AIS tracking system reported as inactive at the time. The lifeboat was subsequently recovered by local Omani authorities, according to the UK Maritime Trade Operations (UKMTO), which has been coordinating monitoring efforts with commercial operators throughout the conflict. For a broader understanding of how oil prices and geopolitics interact during flashpoints like this, the wider regional context proves essential.

The Military Exchange: Scale, Targets, and Counter-Escalation

U.S. Central Command confirmed that the third round of strikes commenced at 19:15 ET (23:15 GMT) on 11 July, engaging approximately 140 Iranian military targets across multiple categories:

| Target Category | Strategic Purpose |

|---|---|

| Missile and drone launch sites | Neutralises offensive maritime interdiction capability |

| Naval infrastructure | Degrades IRGC capacity to threaten commercial shipping |

| Ammunition storage facilities | Reduces sustained operational endurance |

| Communication networks | Disrupts command-and-control coordination |

| Coastal surveillance positions | Limits targeting intelligence for vessel interdiction |

Iranian health authorities reported at least 17 fatalities and 115 injuries, with at least 12 explosions confirmed in Bushehr province. Iran's IRGC aerospace arm simultaneously claimed strikes on logistics support centres and refuelling platforms linked to U.S. carrier operations at Duqm port in Oman.

Separately, drone strikes were reported across Oman's Musandam governorate, the northernmost territory strategically positioned at the mouth of the strait. Oman publicly condemned these attacks, a significant diplomatic signal given the country's traditional role as an intermediary between Washington and Tehran. Iranian strikes were also reported against U.S. military installations in Qatar, Bahrain, and Kuwait, prompting heightened security alerts from all four Gulf states.

Competing Claims and the Practical Reality of Closure

The IRGC's declaration, carried by the Tasnim news agency, stated that the strait would remain closed until American military interventions in the region ended. U.S. Central Command directly contradicted this position, asserting that the strait remained open to all vessels seeking lawful transit.

Both claims contain elements of truth, and their contradiction is precisely what makes the situation so commercially damaging:

- The legal position: Under UNCLOS Article 38, all vessels enjoy the right of transit passage through internationally recognised straits. Iran cannot unilaterally abrogate this right under international maritime law.

- The practical position: The ability to interdict shipping through military force operates independently of legal frameworks. When a commercial vessel has been physically struck and disabled, the legal right to transit becomes commercially irrelevant for risk-averse operators.

- The insurance position: War risk underwriters respond to actuarial reality, not legal arguments. The moment vessels face credible interdiction risk, premiums spike to levels that make transit economically unviable for many operators.

- The AIS evidence: Real-time tracking data showed no visible vessel movement following the closure declaration.

Market Psychology Note: The ambiguity between the IRGC's declaration and Centcom's rebuttal does not cancel out the market impact. In energy markets, unresolved uncertainty is itself a price driver. Traders do not wait for clarity before adjusting positions.

The Production Collapse That Already Happened: OPEC+ Data

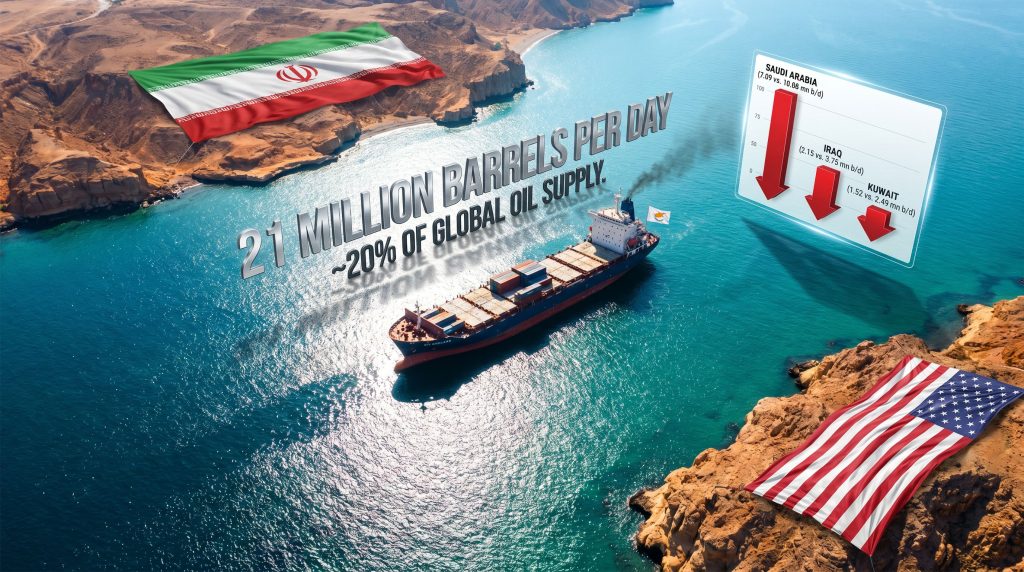

To understand the stakes of the current escalation, it is necessary to first understand the damage already done. When the U.S.-Iran conflict commenced on 28 February, OPEC+ production fell by a record 8.1 million b/d in the following month — the largest single-month production decline in the alliance's history. The OPEC demand forecast revisions during this period reflected the severity of the shock across global supply chains.

| Producer | June Output (mn b/d) | Pre-War Output (mn b/d) | Gap Remaining |

|---|---|---|---|

| Saudi Arabia | 7.09 | 10.88 | -3.79 |

| Iraq | 2.15 | 3.75 (est.) | -1.60 |

| Kuwait | 1.52 | 2.49 (est.) | -0.97 |

| Iran | 2.75 | 3.20 (pre-sanctions est.) | -0.45 |

| UAE | 3.82 (record) | ~3.46 | +0.36 |

Total OPEC+ production recovered to 31.95 million b/d in June, up 2.25 million b/d from May, but remained approximately 7.2 million b/d below pre-war levels. The June recovery was driven almost entirely by Mideast Gulf members ramping exports through the strait under the interim peace deal's brief window of relative stability. That window has now closed.

The UAE Exception: A Market Share Dynamic With Long-Term Implications

One of the less-examined dimensions of the current production landscape is the UAE's strategic positioning. Having formally departed OPEC+ prior to the current escalation, the UAE has ramped production to a record 3.82 million b/d, approximately 360,000 b/d above the quota it would have held under the alliance framework.

The UAE's Habshan-Fujairah pipeline provides direct export capability bypassing the strait entirely, meaning UAE production economics are insulated from Hormuz risk in a way that Saudi, Iraqi, and Kuwaiti output is not. Consequently, a sustained closure paradoxically strengthens the UAE's relative competitive position. This structural advantage raises a speculative but analytically serious question: does the UAE's post-OPEC strategic positioning reflect a longer-term calculation about its comparative advantage in a world where Hormuz instability becomes a recurring feature?

The next major ASX story will hit our subscribers first

Three Scenarios: How a Sustained Closure Unfolds Over Time

Scenario 1: Short-Term Disruption (1–4 Weeks)

In a brief disruption scenario, the global system has established mechanisms capable of absorbing the shock. Strategic petroleum reserve drawdowns by IEA member states, who collectively hold approximately 1.2 billion barrels of public emergency oil reserves, provide a meaningful buffer. At a partial disruption rate of 10–15 million b/d, coordinated SPR releases could theoretically sustain markets for 80–120 days before structural demand rationing becomes necessary.

India's ONGC has already initiated anticipatory hedging, expanding strategic petroleum reserve capacity at Mangalore by 1.75 million tonnes (12.83 million barrels). Abu Dhabi's ADNOC is simultaneously pursuing a doubling of its crude storage presence in India, targeting up to 4 million tonnes (30 million barrels) across Mangalore and Padur underground storage facilities. Historical patterns suggest short-duration Hormuz threats have added $5–$15 per barrel in risk premium to Brent crude pricing.

Scenario 2: Medium-Term Closure (1–3 Months)

A closure extending beyond four weeks begins to expose the structural inadequacy of bypass alternatives. The combined capacity of Saudi Arabia's East-West Pipeline and the UAE's Habshan-Fujairah route covers less than 35% of normal Hormuz transit volumes. The residual 65% has no alternative routing.

LNG markets face the most acute exposure in this scenario. Qatar, the world's largest LNG exporter, has no pipeline alternative whatsoever. In addition, Asian LNG spot prices, which already reflect elevated risk premiums, would face severe upward pressure. Japan, South Korea, and Taiwan collectively depend on Gulf LNG for substantial portions of their power generation and industrial feedstock supply.

Scenario 3: Extended Closure (3+ Months)

An extended closure exceeding three months would represent a peacetime energy shock with no modern historical parallel. Historical modelling suggests sustained closure of 60 or more days could push Brent crude to $120–$180 per barrel depending on the scale of SPR intervention. A closure exceeding 90 days would likely constitute the most severe peacetime energy disruption since the 1973 Arab oil embargo.

Secondary consequences in this scenario extend well beyond oil prices:

- Global refining capacity utilisation contracts sharply as feedstock availability diminishes

- Energy-intensive industries including petrochemicals, aluminium smelting, and fertiliser production face input cost shocks severe enough to trigger facility curtailments

- Fertiliser supply disruptions carry downstream consequences for agricultural commodity markets and food security in import-dependent developing economies

- Energy-importing nations face compounding fiscal stress, currency depreciation, and social stability pressures

OPEC+ Target Adjustments and the Russia Complication

Seven core OPEC+ members agreed on 5 July to a further 188,000 b/d increase in their collective production ceiling for August. This leaves only 188,000 b/d of voluntary cuts remaining, which could be fully unwound as early as September. However, that ambition faces a second complicating variable entirely separate from Hormuz.

Russia's output remained approximately 760,000 b/d below its OPEC+ target in June, attributable to ongoing Ukrainian strikes against Russian energy infrastructure. Russia cannot compensate for Gulf production shortfalls even if strategically willing to do so. Furthermore, the compounding effect of Gulf Hormuz disruption and continued Russian output constraints creates a supply deficit that the alliance's production ceiling adjustments cannot resolve through administrative decisions alone.

The Fragility of Diplomatic Off-Ramps

The interim peace deal of 18 June, which enabled the June production recovery, has effectively unravelled. The revocation of Iran's sanctions waiver signals that the deal's foundational terms are no longer operative. Oman's traditional backchannel role between Washington and Tehran has been complicated by the Iranian drone strikes on Musandam governorate, eroding precisely the diplomatic infrastructure that any de-escalation pathway would require.

One analytically significant element involves the possibility that the GFS Galaxy attack was not a centrally commanded IRGC decision but rather an action by a factional element seeking to derail ongoing negotiations. If accurate, this would indicate that the IRGC is not operating as a fully unified command structure. It also introduces the inverse risk: that further unauthorised actions could occur regardless of what senior Iranian leadership may prefer diplomatically. The broader pressure on global oil markets from this uncertainty is already being felt across futures markets. For a live overview of the situation as it develops, real-time news coverage is tracking military movements and diplomatic signals closely.

Country-Level Exposure: Who Bears the Greatest Risk?

| Economy | Primary Exposure | Mitigation Capacity | Vulnerability Rating |

|---|---|---|---|

| Japan | LNG dependency (power generation) | Long-term contracts, some SPR | High |

| South Korea | LNG and crude dependency | SPR stocks, diversified suppliers | High |

| India | Crude import dependency | Expanding SPR, ADNOC partnership | Medium-High |

| China | Largest single crude importer | Large SPR, diplomatic neutrality | Medium-High |

| Taiwan | LNG for power generation | Limited domestic alternatives | Very High |

| Germany/EU | Diversified but residual Gulf exposure | IEA coordination, alternative suppliers | Medium |

China occupies a uniquely complex position. As the world's largest crude oil importer and a major destination for Gulf crude exports, Beijing has enormous economic exposure to Hormuz disruption. Simultaneously, China maintains formal diplomatic neutrality while having significant economic interests in Iranian oil flows, creating a policy environment where Beijing's incentives cut across multiple directions simultaneously.

Frequently Asked Questions: Iran Says Hormuz Shut After Fresh US Attacks

Does Iran have the legal right to close the Strait of Hormuz?

No. Under UNCLOS Article 38, all vessels enjoy the right of transit passage through internationally recognised straits used for international navigation. Iran is a signatory to UNCLOS and cannot unilaterally close the strait under international maritime law. However, the legal framework and the practical capacity to interdict vessels through military force are separate questions, and the latter operates independently of the former.

How much of global oil supply normally transits Hormuz?

Approximately 20–21 million barrels per day under normal conditions, representing roughly one-fifth of global oil consumption. This includes crude oil, condensate, refined products, LNG, and LPG. The strait also handles the vast majority of Qatar's and the UAE's LNG export volumes, for which no pipeline bypass alternative exists.

What alternative routes exist if Hormuz remains closed?

- Saudi Arabia's East-West Pipeline: approximately 5 million b/d capacity to the Red Sea port of Yanbu

- UAE's Habshan-Fujairah Pipeline: approximately 1.8 million b/d capacity, bypassing the strait to the Gulf of Oman

- Combined capacity covers less than 35% of normal Hormuz transit volumes; no LNG bypass exists

How long can strategic petroleum reserves sustain markets during a disruption?

IEA member states hold approximately 1.2 billion barrels of public emergency oil reserves. At a disruption rate of 10–15 million b/d, coordinated releases could theoretically maintain markets for 80–120 days before structural demand rationing becomes unavoidable.

What is the current status of OPEC+ production?

Total OPEC+ production reached 31.95 million b/d in June, up 2.25 million b/d from May, but remained approximately 7.2 million b/d below pre-war levels. The June recovery is now directly threatened by renewed military engagement and the revocation of Iran's sanctions waiver. Iran says Hormuz shut after fresh US attacks, and the consequences for production recovery timelines are significant.

This article contains forward-looking analysis, scenario projections, and market commentary based on publicly available information. Energy market conditions are subject to rapid change. Nothing in this article constitutes financial or investment advice. Readers should conduct their own due diligence before making any investment or commercial decisions based on the information presented here.

Want to Stay Ahead of Commodity Shocks Driven by Geopolitical Crises Like the Hormuz Closure?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly identifying actionable opportunities in commodities directly impacted by global supply disruptions — from crude oil to LNG and beyond. Start your 14-day free trial today and explore Discovery Alert's discoveries page to understand how major resource discoveries have historically generated substantial returns even during periods of profound market uncertainty.