July 12, 2026

The Geography That Holds Global Energy Hostage

Every few years, a narrow strip of water roughly the width of a mid-sized city reminds the world just how fragile the global energy system truly is. The Strait of Hormuz, a passage so geometrically modest that its navigable shipping lane in each direction spans only approximately 3.2 kilometres, functions as the central artery of global petroleum supply. When Iran closes the Strait of Hormuz, or even credibly threatens to do so, the economic consequences ripple across every oil-importing nation on earth within hours.

Understanding why this chokepoint commands such outsized strategic importance requires moving beyond headlines and into the underlying arithmetic of global oil dependency, the mechanics of maritime interdiction, and the escalation patterns that have defined U.S.-Iran confrontation for decades. Furthermore, the oil price movements triggered by these events illustrate just how deeply interconnected global energy markets have become.

When big ASX news breaks, our subscribers know first

The Arithmetic Behind the World's Most Dangerous Waterway

How Much Oil Actually Flows Through the Strait?

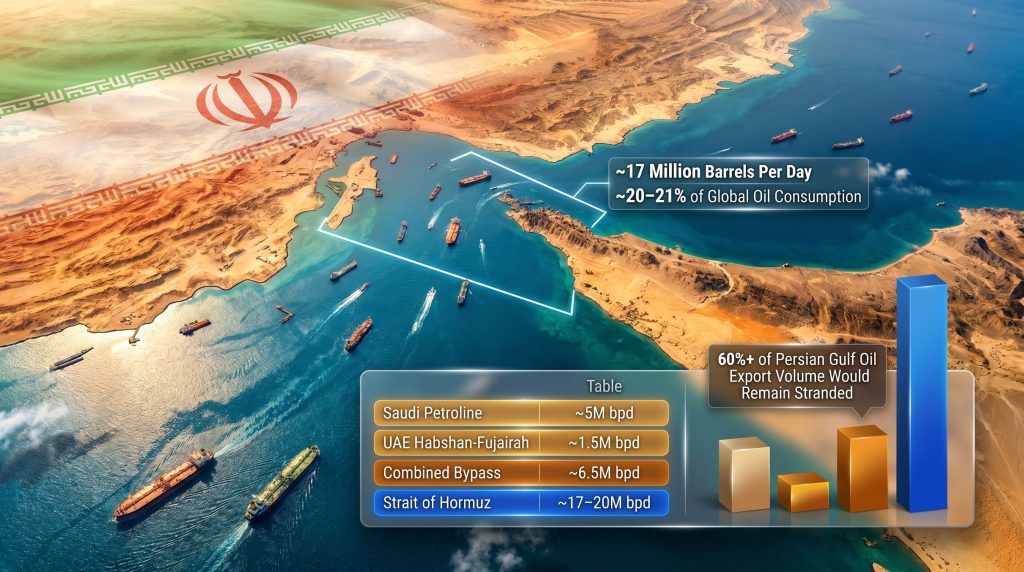

The numbers are staggering in their concentration. Under normal operating conditions, approximately 17 to 20 million barrels of crude oil and petroleum products transit the strait daily, representing roughly 20 to 21% of total global oil consumption moving through a single, physically constrained corridor. Qatar's liquefied natural gas exports, which make that nation one of the world's dominant LNG suppliers at approximately 77 to 80 million tonnes per annum, face identical exposure. The LNG supply outlook for the region consequently remains deeply tied to conditions in the strait.

No engineering solution has fully neutralised this vulnerability. The two principal bypass alternatives, Saudi Arabia's East-West Pipeline (Petroline) and the UAE's Habshan-Fujairah pipeline, provide meaningful but severely limited relief:

| Route | Max Capacity (bpd) | Operational Status | Coverage of Strait Volume |

|---|---|---|---|

| Strait of Hormuz (normal) | ~17-20 million | Active (contested) | 100% baseline |

| Saudi Petroline | ~5 million | Active | ~25-30% |

| UAE Habshan-Fujairah | ~1.5 million | Active | ~7-9% |

| Combined Bypass Capacity | ~6.5 million | Active | ~32-38% |

Even if every alternative pipeline operated at full capacity simultaneously, more than 60% of normal Persian Gulf oil export volume would remain stranded in the event of a genuine, sustained closure. The bypass infrastructure gap is not a policy failure; it is a structural reality that no realistic near-term investment program can close.

Both pipeline systems also require significant lead time to ramp toward maximum throughput and face their own operational bottlenecks, meaning the theoretical capacity ceiling is rarely achievable under crisis conditions.

How a Closure Actually Works: Declaration vs. Physical Blockade

The Gap Between Political Announcement and Military Reality

One of the most consequential distinctions in energy security analysis is the difference between a formal closure declaration and an actual physical blockade. Iran's formal announcement that the Strait of Hormuz is closed carries enormous market weight even when physical enforcement remains selective or incomplete. Historical episodes confirm that the threat of closure, rather than its realised form, is sufficient to trigger oil price volatility, insurance premium surges, and tanker rerouting decisions.

Real-time Automatic Identification System (AIS) data provides analysts with a window into actual vessel behaviour, frequently revealing a significant divergence between declared closures and observed traffic patterns. During recent escalation cycles, ship-tracking data has shown extremely limited visible traffic through the strait following closure announcements, with only isolated tanker movements recorded in the immediate aftermath. Critically, very large crude carriers (VLCCs) have been observed disappearing from tracking systems and subsequently reappearing inside the Persian Gulf, a phenomenon consistent with covert transits conducted with AIS transponders switched off.

This practice, known in maritime intelligence circles as vessels "going dark," creates genuine analytical uncertainty. Military radar, satellite imagery, and allied naval surveillance fill portions of this visibility gap but introduce latency that markets cannot fully absorb in real time. The uncertainty itself becomes a priced risk. According to Seatrade Maritime, Iran's formal declaration of closure has already prompted significant concern across the global shipping community.

Iran's Military Interdiction Toolkit

Iran's Islamic Revolutionary Guard Corps (IRGC) Navy possesses a layered suite of interdiction capabilities concentrated along the strait's northern coastline:

- Fast-attack craft swarms: Designed to overwhelm larger naval vessels through sheer numbers and speed

- Anti-ship missile batteries: Coastal defence systems positioned at sites including Bandar Abbas and the Sirik area provide overlapping fields of fire across the navigable channel

- Underwater mine-laying capability: Strategically the most disruptive tool available, as even the threat of mines forces commercial vessels to halt pending clearance operations

- Anti-ship ballistic missiles: Increasingly precise and capable of threatening large commercial and naval targets at extended range

U.S. Naval Forces Central Command (NAVCENT) and the Combined Maritime Forces maintain a persistent presence in the region specifically designed to counter these capabilities, but Iranian interdiction tools are calibrated to impose risk and cost rather than to achieve outright victory in a conventional naval engagement.

What Triggers an Iranian Closure Threat?

The Strategic Logic of the Strait as a Coercive Instrument

Iran has historically invoked strait closure threats during periods of maximum external pressure, deploying the waterway as a bargaining mechanism rather than a military endpoint. Across multiple escalation cycles, a consistent pattern has emerged:

- External military action against Iranian territory, allied forces, or energy infrastructure

- Formal closure declaration issued by Iranian authorities

- Selective enforcement against commercial vessels attempting transit

- Parallel diplomatic engagement through back-channel intermediaries

- Interim framework negotiations, frequently conducted through Oman

The current episode conforms precisely to this template. Following U.S. strikes targeting Iran's interdiction capabilities, including reported explosions at energy hubs in Bushehr and Asalouyeh, as well as port infrastructure at Bandar Abbas, Bandar-e Dayyer, and the Sirik area, Iran declared the strait closed to vessel traffic. Iranian Foreign Minister Abbas Araghchi subsequently travelled to Oman for discussions, even as military operations continued, illustrating the characteristic Iranian practice of running diplomatic and military tracks simultaneously. Reporting from ABC News Australia confirms that further U.S.-Iran talks are scheduled to take place in Switzerland.

The Negotiating Framework and Its Structural Fragility

Tehran's publicly articulated demand framework includes cessation of foreign military operations, fulfilment of prior commitments relating to Iranian oil export normalisation, and formal guarantees of freedom of navigation defined on Iran's terms. Washington's counter-position has centred on public Iranian guarantees of free commercial passage and an end to attacks on commercial vessels.

Interim agreements structured around these parallel tracks, sometimes called Memoranda of Understanding covering shipping access and sanctions relief simultaneously, have repeatedly provided temporary stabilisation before fracturing at one of their multiple potential failure points. The recurring 60-day conversion window concept, wherein interim arrangements are expected to evolve into permanent frameworks, has become a structural feature of U.S.-Iran negotiations that reliably generates a secondary escalation risk when the conversion deadline approaches without resolution.

Oil Price Impact: How Markets Price Closure Risk

The Multi-Channel Transmission Mechanism

When Iran closes the Strait of Hormuz or credibly threatens to do so, oil markets respond through several simultaneous channels rather than through spot price movement alone. The crude oil geopolitical risks associated with this region consequently permeate every tier of the pricing structure:

- Spot price escalation: Brent crude typically spikes 3 to 8% on initial closure announcements under moderate escalation scenarios

- Futures curve steepening: Near-term contracts price in supply risk premium while longer-dated contracts reflect uncertainty about resolution timelines

- Options market volatility spikes: Implied volatility on crude oil options expands rapidly, reflecting the binary character of escalation outcomes

- War risk insurance premiums: Costs for vessels transiting contested waters can increase by an order of magnitude within days, adding directly to landed crude costs

- Tanker freight rate surge: Available tonnage contracts as operators withdraw vessels from risk zones, compressing supply of shipping capacity against a backdrop of unchanged cargo demand

Historical benchmarks provide useful reference points. During the 2019 Gulf of Oman tanker attack episode, Brent crude rose approximately 4% within 24 hours. The 1987 to 1988 Tanker War period saw freight rates for Persian Gulf voyages increase by several hundred percent at peak tension. War risk insurance premiums and tanker freight rates have consistently proven more persistently elevated than spot crude prices, which tend to normalise quickly once diplomatic signals emerge.

Regional Exposure: Who Bears the Most Risk?

| Region | Persian Gulf Oil Dependency | Primary Exposure |

|---|---|---|

| East Asia (Japan, South Korea, China) | 60-70% of crude imports via strait | Immediate supply disruption, refinery feedstock shortfall |

| South Asia (India) | ~40% of crude imports | Refinery margin pressure, fuel subsidy cost escalation |

| Europe | Moderate (diversified supply) | LNG price spike via Qatar exposure |

| United States | Low direct dependency | Indirect via global price benchmarks and allied exposure |

East Asian economies carry the most acute direct exposure. Japan and South Korea operate with limited crude import diversification and high dependency on Persian Gulf feedstock under long-term contract structures that provide no short-term flexibility. China's growing strategic petroleum reserve capacity provides a partial buffer but cannot substitute for sustained supply disruption across an extended closure scenario.

LNG Markets: Qatar's Unique Vulnerability

The World's Largest LNG Exporter Behind a Contested Chokepoint

Qatar's position as one of the world's dominant LNG exporters creates a supply chain vulnerability that extends well beyond the oil market. At approximately 77 to 80 million tonnes of LNG exported annually, the majority of Qatari cargoes must transit the Strait of Hormuz before reaching buyers in Europe and Asia.

European buyers who strategically diversified toward Qatari LNG following the 2022 Russian pipeline supply disruption now face an uncomfortable structural irony: their diversification strategy concentrated exposure at a different geopolitical chokepoint. Asian buyers, particularly Japan and South Korea, hold substantial volumes of Qatari LNG under long-term contract structures that provide purchasing security but no supply security in a physical closure scenario.

A sustained strait closure would likely push Asian LNG spot prices as measured by the Japan-Korea Marker (JKM benchmark) sharply higher within days of confirmed supply disruption. European TTF gas prices would follow through the mechanism of global cargo diversion, as LNG suppliers redirect flexible spot cargoes toward the highest-premium markets. Regasification terminal capacity constraints across European receiving infrastructure would then limit the speed at which alternative supply volumes could be physically absorbed, creating a bottleneck on the demand side of the relief equation.

The next major ASX story will hit our subscribers first

The U.S. Military Response Framework

CENTCOM's Freedom of Navigation Mandate and the Escalation Ladder

U.S. Central Command maintains an explicit operational mandate to preserve commercial freedom of navigation through the Strait of Hormuz, grounded in the provisions of the United Nations Convention on the Law of the Sea (UNCLOS). Under UNCLOS, the strait qualifies as an international waterway subject to transit passage rights that no coastal state possesses the legal authority to unilaterally suspend.

The practical escalation response framework moves through distinct levels:

- Enhanced surveillance: Naval monitoring, AIS tracking, and diplomatic communications

- Freedom of navigation operations (FONOPs): Naval escorts for commercial vessels and demonstrative transits

- Targeted kinetic response: Strikes on Iranian naval assets and coastal interdiction infrastructure

- Broader military operations: Strikes targeting command, energy, and logistics infrastructure

The current episode has already progressed into the kinetic response tier. CENTCOM confirmed that U.S. strikes targeted Iran's capacity to threaten commercial shipping following the attack on the Cyprus-flagged container vessel M/V GFS Galaxy, in which one civilian crew member was reported missing and the vessel sustained significant damage.

The Compounding Risk of Striking Iranian Energy Infrastructure

Targeting Iranian energy infrastructure creates a compounding strategic dilemma. Strikes on facilities at Bushehr, Asalouyeh, and Bandar Abbas simultaneously degrade Iran's interdiction capability and elevate the risk of retaliatory strikes against Gulf Cooperation Council (GCC) energy infrastructure. Saudi Aramco export terminals, UAE offshore production facilities, and Qatari LNG processing infrastructure all fall within range of Iranian ballistic missile systems and drone swarm capabilities.

Iranian forces have demonstrated this intent, launching ballistic missiles toward U.S. military facilities in Jordan and Qatar while conducting drone attacks targeting military infrastructure in Kuwait, Bahrain, and Oman. Qatar reported successful interception of inbound missiles; air defence sirens activated across Bahrain and the UAE. The asymmetric risk is that Iranian retaliation against GCC infrastructure could generate supply disruption of comparable magnitude to a strait closure even if the waterway itself remains physically transitable. In addition, the trade war oil impact layered on top of these geopolitical tensions further complicates the global supply picture.

Strategic Scenarios for Resolution

Three Pathways Forward

Scenario A: Diplomatic De-escalation Within 30 Days

Oman-mediated back-channel diplomacy produces an interim agreement framework. Iran suspends closure enforcement in exchange for a U.S. commitment to pause military operations. Oil prices retreat 8 to 12% from peak levels, with insurance premiums normalising over three to four weeks and strait traffic resuming normal volumes within seven to ten days of agreement announcement.

Scenario B: Sustained Partial Interdiction Over 60 to 90 Days

Iran maintains selective enforcement, halting some vessels while permitting others to transit. Tanker operators adopt AIS-dark transit strategies; war risk premiums remain persistently elevated. Oil prices stabilise at a 15 to 25% premium above pre-crisis levels. GCC states accelerate bypass pipeline utilisation, with Saudi Arabia increasing Petroline throughput toward its approximately 5 million barrel per day capacity ceiling. Furthermore, OPEC market influence over production decisions would become a critical stabilising variable under this scenario.

Scenario C: Full Kinetic Escalation and Extended Closure

Sustained Iranian mining of the strait's navigable channel forces complete commercial vessel suspension. Global oil prices spike 30 to 50% above pre-crisis baseline within weeks. Coordinated Strategic Petroleum Reserve (SPR) releases are activated across International Energy Agency member states. Diplomatic resolution extends to a six-month or longer timeline; infrastructure damage to Iranian energy hubs compounds the supply-side disruption picture.

Scenario C represents the lowest-probability outcome based on decades of historical precedent, but it also carries the highest systemic risk for global energy markets, supply chains, and developing economies with limited foreign exchange reserves to absorb an oil price shock of that magnitude. The distinction matters for both policy planners and investors calibrating risk exposure.

Frequently Asked Questions: Iran and the Strait of Hormuz

Has Iran Ever Achieved a Complete Physical Blockade?

Iran has never sustained a complete physical closure of the Strait of Hormuz despite multiple formal declarations. The most operationally significant historical disruption occurred during the Tanker War of 1987 to 1988, when Iranian mining operations and naval attacks substantially reduced traffic volumes without achieving a full closure. In more recent episodes, AIS tracking data has consistently revealed that observed vessel traffic diverged meaningfully from declared closure conditions.

What Is the Difference Between a Legal Closure and a Commercial Blockade?

A closure declaration is a political and legal act announcing Iran's intent to restrict access. A functional commercial blockade requires sustained physical enforcement sufficient to deter vessel operators from transiting regardless of legal status. The gap between legal declaration and commercial deterrence is where both market volatility and diplomatic resolution are generated. Markets typically price the probability-weighted average of enforcement intensity rather than either extreme.

How Quickly Do Oil Markets Recover After Strait Tensions Ease?

Historical precedent indicates that oil spot prices begin normalising within days of credible diplomatic signals, often before physical reopening is confirmed. Full market normalisation, including meaningful reduction in war risk insurance premiums and tanker freight rate stabilisation, typically lags price recovery by several weeks as underwriters reassess voyage risk on updated actuarial bases.

The Long-Term Structural Question

Energy Transition and Strait Dependency: A Slow Divergence

Global oil demand growth is concentrated in developing economies where energy transition is advancing more slowly than in OECD nations, meaning Persian Gulf export volumes and structural strait dependency are unlikely to decline materially before the mid-2030s. The accelerating buildout of renewable energy capacity in East Asia reduces long-run vulnerability but offers no near-term relief during an acute crisis.

Counterintuitively, LNG dependency transiting the strait may actually increase over the medium term as European buyers continue diversifying their gas supply mix away from Russian pipeline deliveries. The geopolitical risk premium embedded in Persian Gulf crude is therefore likely to persist as a structural feature of energy markets across the foreseeable investment horizon, reinforcing the strategic case for expanding bypass pipeline capacity, diversifying crude import origins, and deepening strategic petroleum reserve buildout among high-dependency economies.

The current escalation cycle, whatever its diplomatic resolution, will accelerate those conversations. The underlying geography, however, will not change.

Want to Stay Ahead of the Next Major Resource Discovery Triggered by Geopolitical Shocks?

When energy market volatility reshapes commodity prices, the ripple effects often create significant opportunities in ASX-listed resource stocks — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries hit the ASX, ensuring subscribers can act before the broader market catches on. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position yourself ahead of the next major market-moving announcement.