July 29, 2026

Why Most Junior Mining Investors Are Playing the Wrong Game

The history of speculative markets is littered with investors who were right about the asset and wrong about the price. They identified the trend, understood the geology, believed in the management team, and still lost money. This is not a paradox unique to mining. It is the defining feature of probabilistic markets, and it is the reason that Howard Marks You Bet junior mining investing offers one of the most rigorous frameworks ever written for thinking about uncertainty and decision quality.

The principles explored in Howard Marks' memo You Bet, published by Oaktree Capital Management in January 2020, offer an accessible framework for thinking about uncertainty, decision quality, and the relationship between process and outcome. Although Marks wrote the memo through the lens of credit and distressed debt investing, every concept maps directly onto the mechanics of junior mining speculation, where information asymmetry is high, outcomes are volatile, and the gap between a good decision and a good outcome can be enormous.

When big ASX news breaks, our subscribers know first

The Core Flaw: Judging Decisions by Their Results

Why a Winning Trade Is Not Proof of Sound Thinking

The most deeply embedded cognitive error in speculative investing is what Marks identifies at the very opening of You Bet: the assumption that outcome quality reflects decision quality. Marks traces this insight to the first book he read as a Wharton freshman in 1963, a text focused on decision-making under uncertainty in the oil and gas drilling industry. The central lesson he carried from that book through six decades of investing is that a decision and its outcome are not the same thing, and conflating them is one of the most dangerous habits a speculator can form.

Every investment result is the product of two independent forces: the quality of the reasoning that went into the decision, and the randomness of events that occurred after that decision was made. The problem is that in any single instance, these two contributors cannot be cleanly separated. A well-researched position in a junior uranium explorer can be cut in half if sentiment turns and commodity prices fall, despite every element of the original thesis remaining intact.

Conversely, a poorly reasoned purchase of a promotional penny stock can triple on the back of a speculative wave that has nothing to do with fundamentals. Understanding junior mining risks and rewards at this foundational level is what separates durable performers from those who mistake luck for skill.

The Decision Quality Matrix

The distinction between process and outcome can be visualised through a simple framework. This matrix, popularised in probabilistic decision-making literature and referenced in Annie Duke's Thinking in Bets, identifies four possible combinations of decision quality and outcome:

| Decision Quality | Outcome | Interpretation |

|---|---|---|

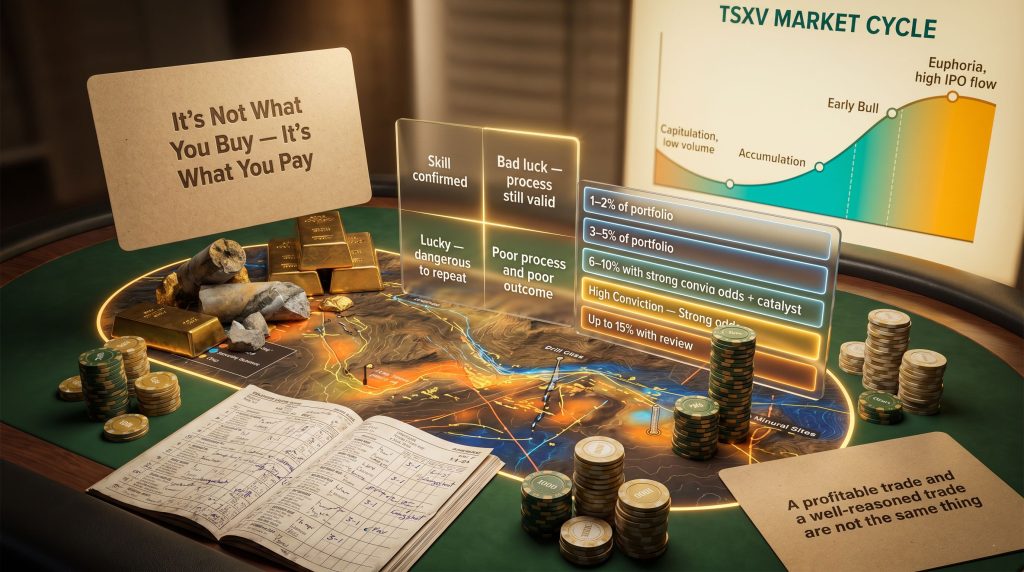

| High | Positive | Skill confirmed — process working |

| High | Negative | Bad luck — process still valid |

| Low | Positive | Lucky — dangerous if repeated |

| Low | Negative | Poor process and poor result |

The most dangerous cell in that table is the bottom-left: a poor decision that produces a positive outcome. This is the cell that destroys long-term performance, because it teaches investors the wrong lesson. The speculator who buys a stock based on a rumour, watches it triple, and concludes they have found a repeatable process is building their strategy on a foundation of noise.

The most dangerous investor in junior mining is not the one who loses capital on a flawed thesis. It is the one who profits from a flawed thesis and concludes the process was sound.

Tracking Thesis Quality Separately From Returns

The practical implication of this framework is straightforward: keep a written investment journal that records not just position sizes and returns, but the reasoning at entry, the probability assigned to success, and a post-mortem analysis of whether any error that occurred was a process failure or simply bad luck. Over time, this practice builds genuine calibration, the ability to assign probabilities to outcomes that actually reflect reality.

Annie Duke's work on probabilistic thinking, which Marks quotes extensively in the memo, argues that intellectual honesty about uncertainty is a foundational skill. Statements like I assign roughly a 60% probability to this thesis working out are not expressions of weakness. They are honest representations of the available information, and they are far more useful than the false certainty that characterises most junior mining promotion.

What Game Theory Reveals About Junior Resource Markets

Three Dimensions That Separate Investment Environments

Marks uses a taxonomy of games and gambling to distinguish between different types of investment environments. He argues that games, and by extension markets, differ along three dimensions: the presence of hidden information, the role of luck, and the degree to which skill can produce consistent outperformance.

Chess involves no hidden information and no luck, only skill. Roulette involves no hidden information and no skill, only chance. Poker sits in the middle: hidden information, meaningful luck in any single session, but a significant skill premium over a large sample of hands. These distinctions matter because they determine whether consistent outperformance is even possible in a given environment.

Applied to investing, the framework produces a clear hierarchy of market efficiency:

| Market Type | Hidden Information | Luck Component | Skill Premium |

|---|---|---|---|

| Large-cap US equities | Low | Moderate | Minimal |

| Index funds | None | Low | None |

| Junior mining (TSXV/CSE) | High | High | Significant |

| Distressed debt | Moderate | Moderate | High |

Why Junior Mining Is an Alpha Market

The efficient market hypothesis holds that prices rapidly incorporate all available information, making consistent outperformance through active management essentially impossible. Marks does not fully accept this view, and for good reason: market efficiency is not uniform across all asset classes. Large-cap US equities are analysed by hundreds of professionals with access to the same data, earnings calls, and management teams.

Junior resource stocks on the TSX Venture Exchange and the Canadian Securities Exchange operate in a fundamentally different environment. Analyst coverage is sparse or nonexistent for the majority of listed companies. Many micro-cap explorers are followed by no institutional research at all. Pricing frequently reflects sentiment, momentum, and narrative rather than probability-weighted fundamental value. Information asymmetry is high. Emotional pricing is common.

These are precisely the conditions under which a disciplined, well-informed speculator can generate genuine alpha. A contrarian junior mining approach, focused on doing work the market has not yet done, is structurally advantaged in this environment.

It is worth noting that the skill premium in junior mining is real but not evenly distributed. Industry data consistently supports the view that only a low single-digit percentage of exploration projects advance to the development stage, and a far smaller fraction ever reach profitable production. The base rate for success is low, which makes the quality of the proposition at the time of purchase the dominant variable in long-run outcomes.

The Concept Most Retail Investors Completely Ignore: The Proposition

Identifying the Favourite Is Only Half the Work

The single most important concept in You Bet is what Marks calls the proposition. It is also the concept most consistently overlooked by retail investors in junior mining stocks. Identifying which company has the better project, the more experienced management team, or the stronger jurisdiction is what most investors focus on. Marks argues this is only half the task, and probably the less important half.

The more critical question is whether the current price adequately reflects the full probability-weighted range of outcomes, including both the upside potential and the realistic probability of loss. A world-class asset at a price that already reflects the best-case scenario is not a good investment. An unremarkable asset at a price that implies failure may be an exceptional one.

In investment decision-making, the proposition refers to whether the price being paid for an asset adequately reflects the probability-weighted range of outcomes, including both upside potential and downside risk. Identifying the best company is only half the task. The more critical question is whether the market's current pricing creates a genuine edge.

The Racetrack Analogy and Its Direct Application to Mining

Marks illustrates the proposition using a horse racing analogy drawn from a speech by Charlie Munger. The crowd at a racetrack knows which horse carries the best record, the lightest weight, and the most favourable post position. That information is priced into the odds. The horse with the best form pays 3 to 2. The crowd has correctly identified the favourite.

However, whether betting on the favourite or the long shot produces better expected returns depends entirely on whether those odds are fair given the actual probabilities involved. The same logic applies directly to junior mining. Consider two explorers:

- Company A holds a high-grade deposit in a Tier-1 jurisdiction, is covered by multiple analysts, and trades at a market capitalisation that already reflects a successful feasibility outcome.

- Company B holds a lower-grade deposit in an underfollowed region, carries no analyst coverage, and trades below the implied cost of replacing its existing resource through new drilling.

Which is the better investment? The answer has nothing to do with project quality. It depends entirely on whether the current price creates a genuine margin of safety relative to the realistic range of outcomes.

Historical Case Studies: The Nifty 50 and the Junk Bond Paradox

When the Best Companies Destroyed Capital

When Marks arrived at Citibank in the late 1960s, the institution's investment policy was to hold the Nifty 50, widely regarded as the 50 greatest growth companies in America. IBM, Xerox, Coca-Cola, Polaroid, and Kodak were among them. The prevailing view was that these companies were so superior that no price was too high to pay for them.

The result was catastrophic. Investors who purchased the Nifty 50 at peak valuations and held through the following five years lost the large majority of their capital, not because the companies were bad, but because the proposition was disastrous. Some of those companies, Kodak and Polaroid among them, eventually ceased to exist entirely. The quality of the asset was irrelevant once the price had absorbed all possible optimism.

When Junk Bonds Outperformed Blue Chips

The mirror image of the Nifty 50 story arrived a decade later. In 1978, Marks was asked to manage a high-yield bond fund at Citibank, investing in the bonds of the weakest public companies in America. Every sophisticated investor in his circle regarded the strategy as reckless.

The outcome told a different story. Approximately 4% of the portfolio by dollar value defaulted each year. But the yields on those bonds were so elevated, the proposition so favourable, that investors absorbed those losses and still generated consistently strong returns. Moody's literally defined a B-rated bond as one that fails to possess the characteristics of a desirable investment. Marks observed that Moody's was right that the companies were inferior. The rating agency simply never asked whether the price compensated investors for that inferiority.

Two principles every junior mining investor should internalise:

- Investment success does not come from acquiring great assets. It comes from acquiring assets at prices that justify the risk.

- The quality of what you buy matters far less than the terms on which you buy it.

Eight Gambling Principles That Reframe Junior Mining Speculation

1. Game Selection: Fish in the Right Pond

Andrew Marks, contributing to his father's memo, argues that the first question any serious speculator should ask is whether they have a genuine skill advantage in the game they are playing. Professional poker players seek out tables where the competition is weak. They avoid tables full of other professionals where the edge is minimal.

For junior mining investors, this means honestly identifying where your analytical edge is real. Developing genuine expertise in a specific deposit type, a particular jurisdiction, or an underfollowed commodity sub-sector creates the kind of asymmetric information advantage where real returns are possible. Furthermore, focusing on smaller, uncovered companies amplifies that structural advantage considerably.

2. Market Adaptation: Yesterday's Edge Erodes

The strategies that generated outsized returns during the 2003-2007 junior mining cycle or the 2009-2011 recovery look different today. Information flows faster. AI tools are narrowing historic advantages. What worked in an earlier, less connected market environment may not produce the same results in the current one. Staying aware of where new inefficiencies are forming, and where old ones are closing, is an ongoing discipline.

3. Circle of Competence: Know Where Your Knowledge Ends

The junior mining sector spans gold, silver, copper, uranium, lithium, rare earths, potash, phosphate, and dozens of other commodities. Each has its own demand structure, cost profile, technical vocabulary, and cyclical dynamics. Bull market enthusiasm in one metal pushes investors into adjacent sectors they do not understand, which is precisely when costly mistakes are made.

Honest self-assessment of where your knowledge genuinely ends is a risk management tool, not a limitation. In addition, being alert to management red flags within unfamiliar sectors is especially important when operating at the edge of one's competence.

4. Selective Participation: Not Playing Is Often the Highest-Value Move

There is no rule requiring a position in every opportunity that crosses a watchlist. Disciplined speculators build deep knowledge of a concentrated set of companies and wait for the proposition to become genuinely favourable before deploying capital. The investor who deeply understands 20 companies and waits for one or two of them to reach a compelling valuation almost always outperforms the investor who is permanently fully invested in the latest narrative.

5. Asymmetric Position Sizing: Scale Bets to the Quality of the Edge

Position sizing is one of the most underappreciated disciplines in junior mining investing. Spreading capital equally across 15 positions is not diversification. It is a failure to differentiate between the quality of research and conviction across holdings. Munger's formulation, as quoted in the memo, is direct: the wise ones bet heavily when the world offers them that opportunity.

| Conviction Level | Edge Assessment | Suggested Allocation |

|---|---|---|

| Speculative / Exploratory | Low, limited data | 1-2% of portfolio |

| Moderate conviction | Reasonable proposition | 3-5% of portfolio |

| High conviction | Strong odds and near-term catalyst | 7-10% of portfolio |

| Exceptional edge | Rare, deep primary research done | Up to 15% with review |

6. Ruin Avoidance: The Six-Foot River Problem

Andrew Marks includes a vivid warning that deserves its own emphasis. A river averaging five feet deep can still drown a six-foot-tall person in the wrong section. A portfolio that performs well on average can still be catastrophically damaged by a single over-concentrated position in a company that reaches zero.

In junior mining, survival is not a conservative instinct. It is the prerequisite for compounding. Being right on average is insufficient if concentrated positions in zero-outcome companies eliminate the capital needed to participate in future opportunities.

Liquidity management, hard position limits, and avoiding maximum-leverage situations are not timid strategies. They are the structural conditions that allow a speculator to remain in the game long enough for their edge to manifest across a meaningful sample size.

7. Environmental Calibration: Match Aggression to Market Conditions

The appropriate level of portfolio aggressiveness is not fixed. It should vary with the observable conditions of the junior mining market. During periods of deep capitulation, when sentiment is at historic lows and quality companies are trading near or below cash value, increasing selective exposure is rational. Your risk appetite and decisions should shift deliberately in response to these conditions rather than remain static.

| Market Condition | Sentiment Indicator | Recommended Posture |

|---|---|---|

| Deep bear market | Capitulation, low volume | Increase selective exposure |

| Early recovery | Improving but cautious | Build core positions |

| Mid-cycle bull | Positive momentum | Maintain, trim outliers |

| Late-cycle bull | Euphoria, high IPO flow | Raise standards, reduce size |

8. Emotional Discipline: The Behavioural Errors That Cost the Most

The emotional errors that destroy junior mining returns are well-documented and consistently repeated. Averaging down on a broken investment thesis because admitting error is psychologically uncomfortable is one of the most common. Selling a multi-bagger at a 30% gain out of unfamiliarity with being substantially right is another. Increasing position sizes in declining stocks to chase losses compounds the original mistake.

All of these behaviours are emotionally driven responses to the discomfort of uncertainty. They substitute feeling certain for being accurate, and over a full market cycle, they extract an enormous toll on portfolio performance.

The next major ASX story will hit our subscribers first

Second-Level Thinking: The Meta-Skill That Creates Real Edge

What the Market Currently Believes vs. What Is Actually True

The ninth concept Marks adds to the memo goes beyond the eight gambling principles to address how superior investors think about consensus and mispricing. Second-level thinking means asking not just whether a company is good, but what the market currently believes about that company, whether that belief is accurate, and whether you possess information or analysis that the consensus lacks.

Second-level thinking in junior mining means asking not just 'is this a good company?' but 'what does the market currently believe about this company, and is that belief wrong?' The edge in speculative resource markets comes from identifying gaps between consensus expectations and probable reality, not from confirming what everyone already knows.

This is precisely why underfollowed, under-covered junior miners with legitimate technical merit can offer superior propositions even when their assets appear modest by comparison to headline projects. The market's belief about them is incomplete, and that incompleteness is the source of potential alpha. Consequently, interpreting drill results accurately — before the market has had time to fully digest them — is one of the most direct expressions of second-level thinking available to a retail speculator.

A Practical Pre-Investment Checklist for Junior Mining Speculators

Six Questions to Ask Before Every Position

- What is the realistic base case outcome, stripped of promotional framing?

- What is the probability-weighted range of outcomes, including the scenario of total loss?

- How much dilution is likely required before value is realised, and does the current price account for it?

- Is there a genuine margin of safety embedded in the current market capitalisation?

- What is the maximum downside, and can the portfolio absorb it without impairing future opportunities?

- Is this position sized to reflect genuine analytical conviction, or emotional attachment to the narrative?

Investment Journal Framework

Tracking process quality separately from returns is the most direct way to improve decision-making over time. A structured journal that captures the following elements creates a feedback loop that builds genuine calibration:

| Decision Factor | What to Record | Why It Matters |

|---|---|---|

| Thesis at entry | Core reasoning in writing | Separates process from outcome |

| Probability assigned | Estimated odds of success | Builds calibration over time |

| Proposition assessment | Price vs. risk/reward balance | Identifies valuation discipline |

| Outcome | Final return | Compare to thesis, not just P&L |

| Post-mortem | Was error process or luck? | Improves future decision quality |

The Current Environment: When Probabilistic Thinking Matters Most

How 2025 Market Conditions Amplify the Importance of Odds-Based Evaluation

Volatile commodity prices, elevated financing costs for development-stage companies, and a selective investor risk appetite have created a widening gap between junior miners with genuine technical merit and those sustained primarily by promotional momentum. In this environment, the ability to evaluate propositions rigorously rather than narratives emotionally is not a theoretical advantage. It is a practical survival requirement.

Higher cost-of-capital environments compress the runway available to explorers and developers alike. Companies that cannot demonstrate clear near-term catalysts toward cash flow face sustained capital market pressure. This dynamic rewards investors who have done the work to distinguish between genuine optionality and promotional storytelling, and it punishes those who rely on sentiment alone.

Geopolitical risk in mining jurisdictions adds another layer of complexity that defies easy quantification. Assigning probability-weighted adjustments to jurisdictional risk, permitting uncertainty, and sovereign resource nationalism requires the same probabilistic framework that applies to geological outcomes. The investor who approaches these variables with calibrated uncertainty is structurally better positioned than one who dismisses them as unlikely or ignores them entirely.

Frequently Asked Questions: Howard Marks' You Bet Applied to Junior Mining

What does Howard Marks mean by the proposition in investing?

The proposition refers to whether the price paid for an asset is justified by the full probability-weighted range of outcomes, not simply whether the underlying asset is high quality. It is the question of whether the odds are fair, not whether the favourite is correctly identified.

Can Howard Marks' You Bet principles apply to speculative junior mining stocks?

Yes. The principles of asymmetric payoffs, position sizing relative to conviction, selective participation, and process-over-outcome thinking are especially relevant in markets defined by high uncertainty and significant information asymmetry, both of which characterise junior resource markets. Howard Marks You Bet junior mining investing is not a superficial crossover — it is a direct mapping of probabilistic logic onto a sector defined by it.

Why do junior mining investors consistently overpay for good projects?

Because narrative-driven evaluation bypasses the proposition entirely. Investors assess asset quality without asking whether the current market capitalisation already prices in the best-case scenario. When it does, even genuinely excellent projects produce poor investment returns.

What is second-level thinking in the context of resource stocks?

It means going beyond whether a company is good to ask what the market currently believes, whether that belief is accurate, and whether you have analytical insight that the consensus lacks. The edge comes from identifying the gap between market expectations and probable reality.

How should position sizing work in a junior mining portfolio?

Position sizes should be proportional to the quality of the analytical work done and the favourability of the proposition. Equal-weighting across all holdings fails to differentiate between the depth of conviction and research quality across positions. High-conviction, deeply researched positions with strong risk/reward profiles warrant meaningfully larger allocations.

What is the single biggest behavioural error in junior mining speculation?

Confusing a lucky outcome with a sound process, and then repeating the same low-quality decision-making with increasing confidence. This is the error that compounds silently and is the most difficult to self-diagnose without a structured journal and honest post-mortem practice.

Building a Probabilistic Mindset for Long-Term Resource Speculation

Three Principles That Define Durable Success

The framework Marks constructs across You Bet reduces to three foundational principles that apply directly to Howard Marks You Bet junior mining investing:

- Process over outcome. Judge the quality of a decision by the reasoning and information available at the time it was made, not by the randomness of the result. Good process repeated consistently outperforms lucky outcomes over any meaningful time horizon.

- The proposition matters as much as the favourite. The best company at the wrong price is a bad investment. A modest company at a price that more than compensates for its weaknesses can be an excellent one. Most investors obsess over the first question and neglect the second entirely.

- Skill operates inside a probabilistic world. Being wrong a meaningful percentage of the time is not a failure of method. It is the nature of uncertain markets. The goal is not to be right every time. The goal is to be right more often than the market expects, and to size bets accordingly.

You will be wrong a meaningful percentage of the time in junior mining. That is not a failure of method. It is the nature of probabilistic markets. What separates long-term successful speculators from those who flame out is not a higher win rate. It is better odds assessment, more disciplined position sizing, stronger emotional control, and an unwavering commitment to evaluating decisions by the quality of the process, not the randomness of the outcome.

Readers who want to engage directly with the primary source can download Howard Marks' memo You Bet free of charge from the Oaktree Capital Management website. Annie Duke's Thinking in Bets, which Marks references extensively, offers a complementary and highly accessible treatment of probabilistic decision-making for anyone seeking to deepen their application of these frameworks to resource speculation.

Disclaimer: This article is intended for educational and informational purposes only and does not constitute financial advice, investment recommendations, or an endorsement of any specific security or strategy. Junior mining speculation carries significant risk of capital loss. All investment decisions should be made in consultation with a qualified financial adviser and based on an individual's own research and risk tolerance. Past performance of any strategy or framework does not guarantee future results. Any forward-looking statements or projections discussed in this article are speculative in nature and subject to change.

Want to Know Which ASX Discoveries Are Worth the Proposition?

Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries and delivers real-time alerts, giving subscribers the analytical edge to evaluate genuine opportunities before the broader market catches on — explore historic discoveries and their returns to see what early positioning can mean, then begin your 14-day free trial at Discovery Alert.