June 24, 2026

The Architecture of North American Copper Supply Is Being Redrawn

Few commodity sectors are experiencing the kind of structural transformation currently underway in copper. Decades of underinvestment in domestic U.S. production capacity, combined with accelerating electrification demand and tightening critical minerals policy, have created conditions where scale, geography, and processing technology are converging into a single investment thesis. The completion of the Hudbay Arizona Sonoran acquisition sits at the intersection of all three forces, and understanding why requires more than reading the deal terms in isolation.

What has unfolded in southern Arizona is not simply a corporate transaction. It is a deliberate reconfiguration of where North American copper will come from, how it will be processed, and which companies will control the supply infrastructure that underpins the energy transition. Furthermore, the copper supply crunch now reshaping global markets makes this kind of strategic consolidation increasingly urgent.

When big ASX news breaks, our subscribers know first

From Two Development Assets to a Unified Copper District

Prior to the acquisition closing, both Hudbay's Copper World project and Arizona Sonoran Copper Company's Cactus project existed as separate development-stage assets occupying the same geological corridor in southern Arizona. Each carried standalone merit, but neither could independently achieve the scale, shared infrastructure potential, or capital efficiency that their geographic proximity made possible.

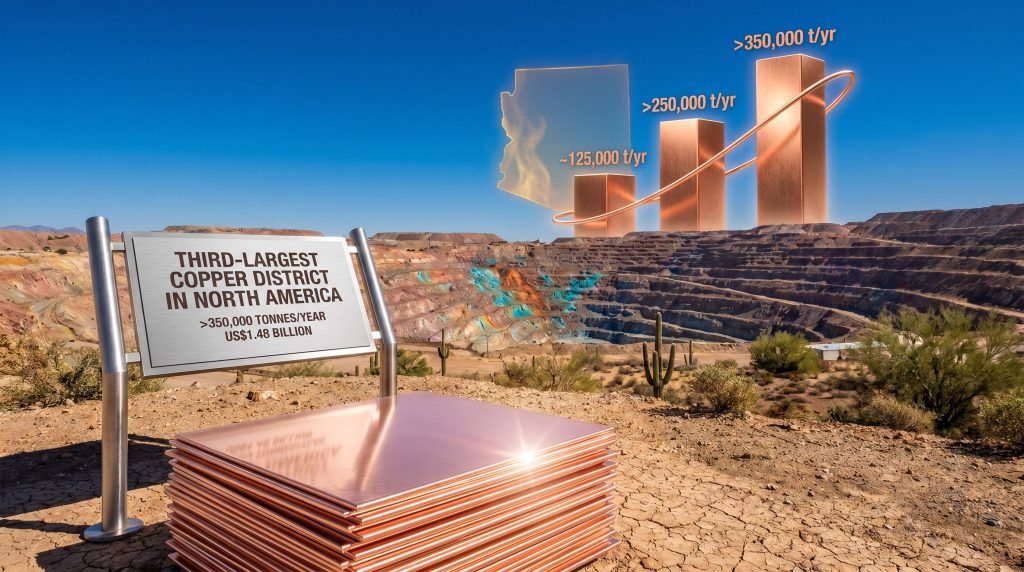

The combination changes the calculus entirely. Hudbay Minerals (TSX, NYSE: HBM) has now assembled what the company describes as the third-largest copper district in North America, a designation that reflects not just resource tonnage but the operational and logistical synergies available when two projects within the same region fall under unified management.

Southern Arizona is not an accidental location for this kind of consolidation. The region hosts a well-documented suite of porphyry and sediment-hosted copper systems, geological environments characterised by large-tonnage, lower-grade mineralisation that lends itself to bulk open-pit extraction methods. The Cactus deposit fits this profile, and its mineralogy is particularly well suited to hydrometallurgical processing, the technical foundation for why SX-EW is the chosen processing route.

The Cactus Project: Processing Technology and Why It Matters

The Cactus project is designed as an open-pit copper cathode operation using solvent extraction-electrowinning (SX-EW) processing. This is a critical distinction that often goes underappreciated by generalist investors. SX-EW produces copper cathode directly at site, a refined, market-ready product that does not require shipment to an offshore smelter before it enters the industrial supply chain.

This matters for several reasons:

- Copper cathode commands a direct price reference to the London Metal Exchange (LME) copper price with minimal downstream processing costs deducted

- Domestic cathode production eliminates the smelting treatment charges and refining charges (TC/RCs) that erode margins for concentrate producers dependent on Asian smelting capacity

- In a policy environment focused on domestic supply chain security, cathode production represents a complete, onshore critical mineral product rather than a partially processed intermediate

- The copper leaching benefits associated with SX-EW operations are well established, and SX-EW operations are generally faster to commission than conventional concentrator circuits, providing a pathway to earlier cash generation

At full capacity, the Cactus project is projected to produce approximately 103,000 tonnes of copper cathode per year. When combined with Copper World's projected output of approximately 92,000 tonnes per year by 2030, the combined Arizona platform positions Hudbay to become a materially larger copper producer than its current baseline would suggest.

Deal Structure and Financial Architecture

The Hudbay Arizona Sonoran acquisition was structured as an all-stock transaction, a design choice with meaningful implications for how Hudbay plans to fund its development pipeline going forward.

| Transaction Parameter | Detail |

|---|---|

| Total Deal Valuation | US$1.48 billion |

| Implied Price Per ASCU Share | ~C$9.35 |

| Exchange Ratio | 0.242 Hudbay shares per ASCU share |

| Acquisition Premium | 29.5% to 36% above recent ASCU trading prices |

| Pre-Existing Hudbay Stake in ASCU | ~10% (via 2025 private placement) |

| Post-Completion Hudbay Ownership | 100% of Cactus project |

| Legacy Hudbay Shareholder Ownership | ~89% of combined entity |

| ASCU Shareholder Ownership | ~11% of combined entity |

| Transaction Completion | Q2 2026 |

The all-stock structure preserves Hudbay's balance sheet liquidity at a moment when the company faces significant capital commitments across its broader project portfolio. By avoiding a cash component, Hudbay sidesteps the need for debt financing or equity dilution at the corporate level, instead absorbing Arizona Sonoran shareholders as co-owners of the enlarged enterprise.

This approach is increasingly common in mid-tier copper M&A for a straightforward reason: the capital expenditure requirements for building and commissioning a copper mine routinely run into hundreds of millions of dollars. Spending cash on the acquisition before the development capital has been deployed would force a company to either dilute shareholders or increase leverage at precisely the wrong time in the project cycle.

The all-stock structure also creates an alignment of incentives. Former Arizona Sonoran shareholders now own 11% of a company with two Arizona projects advancing in parallel, meaning their financial outcome depends directly on Hudbay's ability to execute on both assets simultaneously.

Production Scaling: What the Trajectory Looks Like

The production growth story embedded in the Hudbay Arizona Sonoran acquisition is one of the more compelling quantitative narratives in the mid-tier copper space. Hudbay's pre-acquisition baseline of approximately 125,000 tonnes per year represents a solid mid-tier position, but the combined Arizona platform has the potential to transform that profile dramatically.

| Production Scenario | Estimated Annual Copper Output |

|---|---|

| Hudbay Baseline (Pre-Acquisition) | ~125,000 tonnes/year |

| With Copper World Online (2030) | >250,000 tonnes/year |

| Full Portfolio Including Cactus (2030+) | >350,000 tonnes/year |

A production base exceeding 350,000 tonnes per year represents more than a quantitative milestone. It marks a qualitative transition from mid-tier producer to a significant Americas-focused copper major, a shift that historically attracts a different class of institutional investor, enables inclusion in more index mandates, and provides the operating leverage that makes copper price appreciation substantially more impactful on earnings and cash flow.

For every US$0.10/lb move in the copper price, a company producing 350,000 tonnes per year experiences approximately US$77 million more in gross revenue annually than a company at 125,000 tonnes. That leverage is not incidental to the acquisition rationale; it is central to it.

Capital Allocation Scenarios: How Both Projects Advance

The sequencing question facing Hudbay is one of the most strategically interesting aspects of the combined Arizona platform. There are broadly three pathways the company could pursue:

Scenario A: Sequential Development

Copper World, which holds a more advanced permitting position, reaches production first. Cash flows from Copper World are then partially directed toward funding Cactus construction. This approach minimises near-term capital intensity and reduces financing risk, but delays full realisation of the 350,000 tonne production potential.

Scenario B: Parallel Development with External Financing

Both projects advance concurrently, with Cactus funded through a combination of project finance facilities, streaming arrangements, or royalty agreements. This path maximises production growth speed but carries higher execution risk and requires skilled capital markets navigation during a period when financing costs remain elevated.

Scenario C: Strategic Partnership or Anchor Offtake

A major U.S. copper consumer, whether from the automotive, utilities, defence, or manufacturing sector, provides an anchor offtake agreement or co-investment in exchange for guaranteed cathode supply. This structure has precedent in the U.S. lithium and rare earth sectors, where domestic supply security has driven industrial buyers to participate directly in upstream project financing. The domestic cathode nature of the Cactus product makes it a natural candidate for this type of arrangement.

The Copper Demand Architecture Driving This Investment

Understanding why the Hudbay Arizona Sonoran acquisition carries long-term strategic weight requires examining the demand side of the copper equation with some precision. Indeed, the global copper supply gap is widening, which adds urgency to developing new domestic production capacity in North America.

Electric vehicles consume significantly more copper than their internal combustion counterparts. A conventional vehicle uses roughly 18 to 22 kg of copper, while a battery electric vehicle requires approximately 83 kg, nearly four times as much. When that differential is multiplied across projected EV adoption curves through 2030 and beyond, the incremental copper demand figure becomes substantial.

Grid infrastructure expansion adds another layer of demand pressure. Transmission and distribution network upgrades required to support electrification, renewable energy integration, and data centre growth are copper-intensive by nature. Industry estimates suggest the U.S. alone will require hundreds of thousands of additional tonnes of copper annually to meet its grid modernisation targets through 2035.

The timing of Arizona's production ramp matters here. Both Copper World and Cactus are targeting production timelines that align with the demand inflection point projected for the late 2020s, a period when EV penetration rates are expected to accelerate and grid investment programs move from planning to active construction.

The next major ASX story will hit our subscribers first

Operational Synergies: What Proximity Unlocks

The geographic co-location of Cactus and Copper World within southern Arizona's copper corridor is not merely a narrative convenience. It creates tangible engineering and cost opportunities:

- Shared power infrastructure and water management systems across adjacent operations reduce per-tonne capital costs

- Workforce and contractor pooling during concurrent construction and ramp-up phases reduces labour overhead

- Shared tailings and waste management infrastructure lowers environmental liability and regulatory complexity

- Logistics corridors and transport infrastructure for cathode dispatch can be consolidated

- Exploration and resource definition drilling across the combined land package can be scheduled and contracted more efficiently under unified management

Hudbay brings relevant track record to this integration challenge. Its development of the Constancia operation in Peru and the Lalor underground mine in Manitoba demonstrated the company's capacity to execute complex mining projects through permitting, construction, and ramp-up phases in challenging environments. Applying those operational lessons to Arizona's development sequence is an underappreciated element of the acquisition's value proposition.

ESG Dimensions: Water, Community, and Arid Climate Mining

Mining in the Sonoran Desert environment introduces specific ESG considerations that will shape both the operational profile and the social licence trajectory of the combined Arizona platform.

Water availability is among the most scrutinised aspects of mining in the American Southwest. SX-EW processing is generally more water-efficient than conventional concentrator circuits, but the scale of operations projected for the combined Cactus and Copper World platform means water sourcing, recycling rates, and aquifer impact monitoring will remain under close regulatory and community attention.

Indigenous land consultation frameworks in Arizona require early, ongoing engagement with tribal nations whose cultural and territorial interests intersect with southern Arizona's mining corridor. This is not a peripheral compliance matter; it is a material factor in permitting timelines and community licence to operate.

Tailings management under Arizona's regulatory framework, combined with heightened ESG scrutiny from institutional investors following high-profile tailings failures elsewhere in the Americas, means the design and oversight of storage facilities will be an area of ongoing disclosure and investor attention.

Competitive Context: Where Hudbay Sits in the North American Copper Hierarchy

Prior to this acquisition, Hudbay occupied a defined but limited position in the North American copper producer landscape, operating well below the scale of majors such as Freeport-McMoRan, which produces over 800,000 tonnes per year from its Americas operations, or the copper divisions of diversified majors like BHP and Rio Tinto.

The trajectory toward 350,000 tonnes per year does not close that gap entirely, but it meaningfully repositions Hudbay within the tier below the super-majors, a cohort that attracts dedicated copper fund flows, commodity-specific index weighting, and the analyst coverage that comes with scale-relevant production profiles.

Hudbay's differentiated strategic identity as an Americas-focused producer, rather than a globally diversified mining conglomerate, also carries appeal in an investment environment where portfolio managers seek pure-play or near-pure-play copper exposure. Those exploring copper investment strategies for 2025 and beyond will note that without the gold, iron ore, or potash complexity that characterises the majors, Hudbay presents a more focused proposition.

Frequently Asked Questions: Hudbay Arizona Sonoran Acquisition

What did Hudbay acquire from Arizona Sonoran Copper Company?

Hudbay acquired full ownership of Arizona Sonoran Copper Company through an all-stock transaction completed in Q2 2026, adding the Cactus copper development project in southern Arizona to its existing Copper World asset in the same region.

How was the Hudbay Arizona Sonoran acquisition valued?

The transaction was valued at approximately US$1.48 billion, structured as an exchange of 0.242 Hudbay shares for each Arizona Sonoran share, implying a price of approximately C$9.35 per ASCU share and representing a premium of between 29.5% and 36% over recent trading prices.

What is the Cactus project's production profile?

The Cactus project is designed as an open-pit SX-EW operation targeting approximately 103,000 tonnes of copper cathode per year at full capacity, located south of Phoenix, Arizona.

Why does Hudbay's pre-existing stake in Arizona Sonoran matter?

Hudbay acquired approximately a 10% stake in Arizona Sonoran through a private placement in 2025, establishing a financial interest and strategic familiarity with the asset before pursuing the full acquisition. This approach allowed Hudbay to validate the asset at lower cost before committing to the larger transaction.

What does the combined Arizona platform mean for Hudbay's production outlook?

The combined Cactus and Copper World assets position Hudbay to potentially exceed 350,000 tonnes of annual copper production by 2030, compared to a pre-acquisition baseline of approximately 125,000 tonnes per year.

What ownership split resulted from the transaction?

Following completion, legacy Hudbay shareholders retained approximately 89% of the combined entity, with former Arizona Sonoran shareholders holding approximately 11%.

Key Strategic Takeaways

The Hudbay Arizona Sonoran acquisition signals several broader dynamics worth tracking across the copper sector. Consequently, understanding these themes is essential for anyone monitoring the future of copper mining as the energy transition accelerates:

- Consolidation within development corridors is accelerating as mid-tier producers seek the scale necessary to justify large project capital expenditures and attract institutional mandates

- Domestic copper cathode production carries a structural premium over concentrate in the current policy environment, and SX-EW operations like Cactus are positioned to benefit from that dynamic

- All-stock deal structures are the preferred mechanism for copper M&A at this point in the cycle, preserving balance sheet flexibility for the capital-intensive development phases that follow acquisition

- Production scale thresholds have real consequences for index inclusion, analyst coverage, and fund mandate eligibility, making the path toward 350,000 tonnes strategically significant beyond the revenue arithmetic alone

- Southern Arizona's copper corridor has now been consolidated under a single operator, reducing the probability of competing development timelines fragmenting the region's infrastructure investment and creating a more coherent long-term production hub

Disclaimer: This article contains forward-looking statements, production projections, and scenario modelling based on publicly available information as of the date of publication. Production estimates, deal valuations, and strategic scenarios are subject to material risks, uncertainties, and assumptions. This content does not constitute financial or investment advice. Readers should conduct their own due diligence and consult qualified advisers before making investment decisions.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex geological data into actionable investment insights — explore the historic returns major mineral discoveries have generated to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.