June 4, 2026

The Mechanics Behind a $10 Billion Mine Valuation: What Investors Rarely Ask

Most investors encounter a headline NPV figure and treat it as a price tag. They rarely interrogate the architecture underneath it: the discount rate chosen, the commodity price assumptions embedded, the processing recoveries modelled, or the resources deliberately excluded from the calculation. When a single development-stage project publishes a $10 billion post-tax net present value, the instinct is to compare it against the company's market capitalisation and call the gap an opportunity. The more rigorous instinct is to understand exactly what conditions must hold for that number to remain valid, and what has been left out entirely.

The Hycroft Mining technical report $10 billion NPV, filed with the SEC in June 2026, offers one of the most instructive case studies in this discipline currently available in the North American precious metals sector. The numbers are large enough to attract attention, but the structure of those numbers tells a more nuanced story about commodity leverage, resource classification, processing complexity, and the long road between a preliminary assessment and a mine that is actually built.

When big ASX news breaks, our subscribers know first

Understanding the Regulatory Weight of an SEC S-K 1300 Technical Report Summary

Before engaging with any economic figure from the Hycroft Mining technical report, investors need to understand the regulatory category it occupies. The Technical Report Summary filed by Hycroft Mining Holding Corporation (NASDAQ: HYMC) on June 2, 2026, was prepared in compliance with SEC Regulation S-K 1300, the framework governing mineral resource and reserve disclosures for US-listed mining companies.

This matters because S-K 1300 mandates that all estimates be prepared and certified by a Qualified Person, providing a layer of regulatory accountability absent from purely company-generated marketing materials. However, the classification of the study itself carries equal importance.

A Technical Report Summary at the initial assessment stage is explicitly not a pre-feasibility or feasibility study. It does not demonstrate economic viability under recognised industry standards, and it does not constitute or support a formal development decision. These are not disclaimers buried in footnotes; they are structural definitions that define what this document legally represents.

The practical implication for investors is significant. Initial assessments use wider engineering tolerances, less precise cost estimates, and broader metallurgical assumptions than the bankable feasibility studies that lenders and equity partners require before committing capital to construction. The economic outputs are directional indicators with genuine analytical value, but they are separated from a construction-ready project by multiple additional study stages, each carrying its own capital cost and timeline. A definitive feasibility study represents a considerably higher standard of certainty than what is presented here.

Dissecting the Two NPV Scenarios and the Commodity Leverage Engine

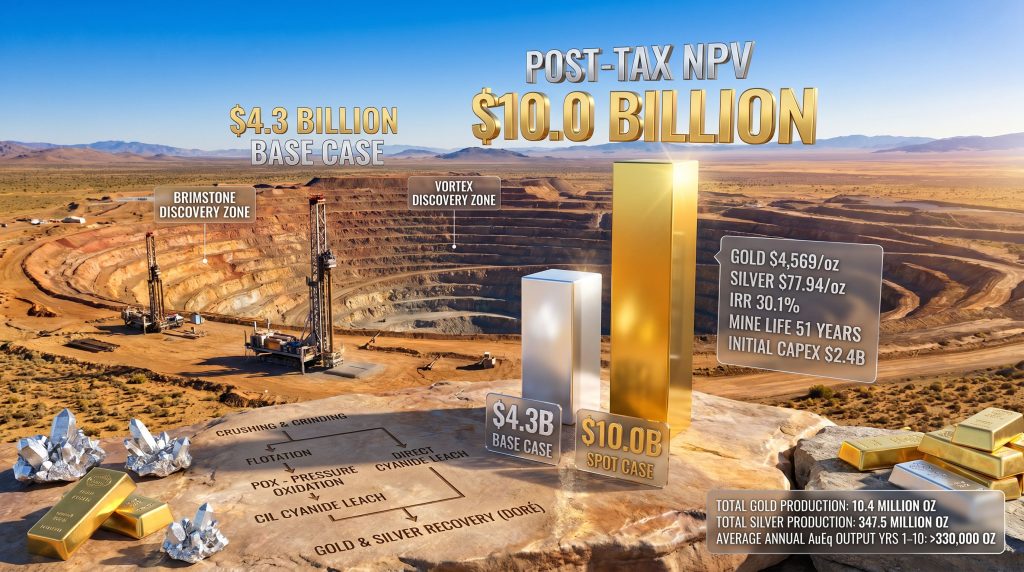

The Hycroft Mining technical report presents economics under two distinct commodity price scenarios, and the gap between them is arguably the most revealing feature of the entire document.

| Economic Parameter | Base Case | Spot Price Case |

|---|---|---|

| Gold Price Assumption | $3,600/oz | $4,569/oz (25 May 2026) |

| Silver Price Assumption | $48.00/oz | $77.94/oz (25 May 2026) |

| Post-Tax NPV (5% discount) | $4.3 billion | $10.0 billion |

| Post-Tax IRR | 16.9% | 30.1% |

| Payback Period | 4.7 years | 2.9 years |

The $5.7 billion difference between the two scenarios is not primarily a function of gold. It is driven to a disproportionate degree by silver. The project's sensitivity analysis reveals that every $100 per ounce increase in the gold price adds approximately $300 million to the post-tax NPV at a 5% discount rate. By contrast, every $5.00 per ounce increase in the silver price adds approximately $460 million to the same metric.

This asymmetry is rarely discussed in coverage of the project but is central to understanding why the spot-price NPV is so dramatically higher. Silver moved from $48.00 per ounce in the base case to $77.94 per ounce at spot, a difference of roughly $30. Applying the $460 million sensitivity per $5 increment across that $30 range implies silver alone contributed approximately $2.76 billion of additional NPV before any gold price contribution is factored in. Furthermore, a broader gold-silver ratio analysis helps contextualise why silver's relative movement can so dramatically outpace gold in these scenarios.

The explanation lies in the scale of the silver inventory. The project hosts 562.6 million ounces of silver in Measured and Indicated categories, a figure that dwarfs most gold-primary development projects globally. When a project carries that volume of silver, even modest silver price movements generate outsized economic responses. This characteristic functions as a structural amplifier in the economic model, magnifying both upside and downside depending on market conditions.

Lifetime Financial Architecture

| Financial Metric | Value |

|---|---|

| Gross Revenue (Life of Mine, Base Case) | $54.2 billion |

| Initial Capital Cost | $2.4 billion |

| Life-of-Mine Sustaining Capital | $3.1 billion |

| Total Capital Commitment | $5.5 billion |

| AISC (per gold equivalent ounce) | $2,147 |

| Cash Cost (per gold equivalent ounce) | $1,924 |

The all-in sustaining cost of $2,147 per gold equivalent ounce sits above the historical industry average for open pit gold operations, reflecting the capital intensity of the pressure oxidation circuit required to process sulphide material. However, evaluating this figure in isolation from current gold price and mining equities creates a misleading impression. At spot gold prices exceeding $4,500 per ounce, the margin between revenue and AISC remains substantial. The relevant question for investors is not whether the AISC is high in absolute terms, but whether it remains well below the realised commodity price across the mine life, accounting for price volatility over a 51-year operating period.

The Resource Base: What the Mine Plan Includes and What It Does Not

The 2026 Mineral Resource Estimate underpinning the Hycroft Mining technical report $10 billion NPV is built around 16.4 million ounces of gold and 562.6 million ounces of silver in the Measured and Indicated categories. These figures place Hycroft among the largest combined precious metals resource inventories held by any single development-stage project within the United States.

What is less frequently emphasised is what the current TRS economics deliberately exclude:

- 5.0 million ounces of gold and 132.8 million ounces of silver in the Inferred resource category were excluded from the mine plan in accordance with S-K 1300 requirements

- All drilling results from the active 2025-2026 drill programme are absent from the current economic model

- Neither the Brimstone nor the Vortex high-grade silver systems are incorporated into any aspect of the TRS mine plan

- The known mineralised system covers less than 15% of a land package exceeding 64,000 acres, and the deposit remains geologically open in all directions and at depth

The arithmetic implication is that the TRS economics represent a conservative baseline derived from a subset of a larger and still-growing resource system. Every future resource update that successfully converts inferred ounces to Measured and Indicated status has the potential to directly expand the mine plan, extend mine life, and improve economic outcomes.

Lifetime Production Forecast

| Production Metric | Value |

|---|---|

| Total Gold Production (51-year LOM) | 10.4 million ounces |

| Total Silver Production (51-year LOM) | 347.5 million ounces |

| Average Annual Gold Equivalent Output (Years 1-10) | >330,000 oz/year |

| Total Gold Equivalent (M&I Resource Base) | 15.1 million oz |

A 51-year mine life is exceptional by global standards. The majority of large open pit operations are designed for 20 to 30 year operating periods, and many significant mines have mine lives considerably shorter than that. The extended duration at Hycroft reflects the sheer volume of material available for processing and creates a different investment thesis than a shorter-life, higher-grade operation: sustained production over multiple commodity price cycles rather than concentrated near-term cash flow.

Processing Technology: Why the Flowsheet Matters as Much as the Grade

One of the more technically significant aspects of the Hycroft Mining technical report is the dual-stream processing configuration, which addresses the geological reality that the deposit contains both oxide and sulphide material requiring fundamentally different treatment methods.

The primary processing route combines conventional flotation with pressure oxidation, followed by cyanide leaching for sulphide ore. This POX circuit is designed to break down the sulphide mineral matrix that traps gold and silver particles, making them accessible for cyanide extraction. It is a proven and widely used technology for refractory sulphide deposits, but it is also capital-intensive and operationally complex compared to simpler heap leach or direct cyanidation circuits.

A run-of-mine heap leach circuit operates in parallel for oxide and transition material, providing a lower-cost, lower-capital processing pathway for the portion of the resource that does not require oxidation.

Average metallurgical recoveries across the mine life are modelled at 82.8% for gold and 77.5% for silver. These are weighted averages across both processing streams and across different ore types encountered over 51 years of mining. Recovery rates for individual ore domains within the mine plan will vary, with oxide material through the heap leach typically achieving different recovery profiles than sulphide material through the POX mill.

Roasting as a Processing Optionality Play

A dimension of the project not yet reflected in the TRS economics is the ongoing evaluation of roasting as an alternative or supplementary sulphide processing technology. Unlike POX, roasting generates sulphur dioxide as a by-product, which can be captured and converted into sulphuric acid for commercial sale. If roasting test work confirms technical and economic viability, it could introduce a by-product revenue stream that partially offsets operating costs and improves the project's overall cost structure. This optionality is entirely absent from the current TRS model, representing a further potential source of economic improvement not yet quantified.

Brimstone and Vortex: The Value Catalysts Outside the Economic Model

The two high-grade silver systems known as Brimstone and Vortex occupy an unusual position in the Hycroft investment thesis: they are the subject of the most active current exploration work, yet they are completely absent from the document that generated the $10 billion NPV headline. According to Hycroft's official announcement, both systems were identified during the 2023 exploration campaign and represent mineralisation styles distinct from the bulk-tonnage character of the broader resource base.

Both systems represent mineralisation styles that are distinct from the bulk-tonnage, lower-grade character of the resource base incorporated into the TRS mine plan. High-grade silver systems, when encountered within or adjacent to a large-tonnage open pit deposit, carry disproportionate economic value because they can be incorporated into the processing schedule at preferential priority, effectively improving the head grade fed to the mill during periods when those zones are being mined.

The potential compounding effect is worth understanding clearly:

- Additional high-grade silver ounces successfully converted from Inferred or exploration-stage to Measured and Indicated status expand the total resource base available for mine planning

- If those ounces carry grades materially above the average resource grade, they improve the blended mill feed grade and enhance metallurgical recoveries on a per-tonne basis

- Given the project's demonstrated silver price sensitivity of $460 million per $5/oz silver price move, a larger silver inventory processed at higher average grades during an elevated silver price environment creates a multiplicative rather than additive improvement in project economics

As of the TRS filing date, two core drill rigs were operating across both targets, with plans to scale to four rigs within the following quarter. Both systems remain open in all directions and at depth, indicating that the current drill programme is still defining the boundaries of what may prove to be substantial silver endowments. Consequently, interpreting drill results from these emerging targets will be a critical skill for investors tracking the project's progress.

The next major ASX story will hit our subscribers first

The Permitting Pathway: Understanding the BLM Review Process

The most significant regulatory milestone standing between the current TRS status and any potential construction decision is the Bureau of Land Management review process for a revised Plan of Operations. This is the gateway through which the environmental impact of the proposed mining operation is formally assessed, and it represents the critical path item with the greatest timeline uncertainty.

Depending on the scale and complexity of the proposed operation, the BLM can conduct either an Environmental Assessment or a full Environmental Impact Statement. For large-scale open pit mines in Nevada, the EIS pathway is more common, and historically these processes have required multiple years to complete. The timeline is influenced by the scope of the proposed operation, the quality and completeness of the applicant's environmental baseline data, the level of public and agency interest, and the workload and resourcing of the relevant BLM field office.

Permitting Risk Framework: Investors assessing probability-weighted development timelines should consider permitting risks as the binding constraint in the critical path, not the completion of the next study stage. An EIS process that takes three to five years adds directly to the timeline before any construction capital can be committed, regardless of how quickly a pre-feasibility or feasibility study might be completed.

The full development pathway from current TRS status to a potential construction decision involves the following sequence:

- Complete the active Brimstone and Vortex drill programme and scale to four rigs

- Update the Mineral Resource Estimate to incorporate 2025-2026 drill results

- Advance the project to a Pre-Feasibility Study level

- Complete roasting technology test work and evaluate oxide targets for early heap leach potential

- Complete a full Feasibility Study

- File a revised Plan of Operations with the BLM and navigate the EA or EIS review process

Each of these stages carries its own capital requirement, technical execution risk, and timeline uncertainty. The $10 billion NPV from the Hycroft Mining technical report $10 billion NPV valuation is the starting point of this journey, not its conclusion.

Contextualising the TRS Against Large-Scale Precious Metals Development Projects

| Benchmark Metric | Hycroft TRS (Spot Case) |

|---|---|

| Post-Tax NPV | $10.0 billion |

| IRR | 30.1% |

| Mine Life | 51 years |

| Initial Capex | $2.4 billion |

| AISC | $2,147/oz AuEq |

| Land Package | >64,000 acres |

| Resource Coverage of Land | <15% |

An IRR of 30.1% at spot prices is considered robust for a capital project requiring $2.4 billion in initial expenditure. The payback period of 2.9 years at spot prices reflects the project's front-loaded production profile, with the first decade averaging more than 330,000 gold equivalent ounces annually before the mine plan transitions to lower-intensity processing of the broader resource base.

What distinguishes Hycroft from many comparable development-stage projects is the combination of scale, jurisdiction, and exploration upside. Nevada's legal and regulatory framework for mining is well-established, infrastructure access in the region is relatively developed by global standards, and the depth of resource knowledge accumulated over decades of historical work provides a geological foundation for the current technical study. In addition, independent coverage from financial analysts tracking the project has highlighted the fact that less than 15% of a 64,000-acre land package has been incorporated into the resource model, suggesting that the geological system extends well beyond the boundaries of the current mine plan.

Key Investor Takeaways: Reading the $10 Billion NPV Correctly

Investors approaching the Hycroft Mining technical report and its $10 billion NPV figure should hold the following framework clearly in mind:

- The $10 billion figure is a spot-price scenario calculated at $4,569/oz gold and $77.94/oz silver as of May 25, 2026, not the base case. The base case NPV at $3,600/oz gold and $48/oz silver is $4.3 billion

- Both figures are derived from an initial assessment, a preliminary study category that carries wider engineering tolerances and less definitive cost estimates than a bankable feasibility study

- The project's silver sensitivity exceeds its gold sensitivity on a per-dollar-of-price-movement basis, making silver market dynamics a primary driver of economic outcomes

- 5.0 million ounces of gold and 132.8 million ounces of silver in Inferred resources, plus all results from the current drill programme, are entirely excluded from the economic model, representing unquantified upside

- The Brimstone and Vortex high-grade silver systems are the primary near-term exploration catalysts and are completely absent from the TRS economics

- BLM permitting, whether through an Environmental Assessment or a full Environmental Impact Statement, is the critical path regulatory constraint before any development decision can be reached

- A 51-year mine life creates a fundamentally different risk and return profile than a shorter-life operation, with economics exposed to multiple commodity price cycles over the operating period

Disclaimer: This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. All economic figures referenced are drawn from the Hycroft Mining TRS filed with the SEC on June 2, 2026, and are subject to the assumptions, limitations, and qualifications described in that document. Commodity price sensitivity figures and NPV estimates are model-derived and highly sensitive to changes in input assumptions. Investors should conduct their own due diligence and consult a licensed financial adviser before making any investment decision.

Want To Be First When the Next Major Precious Metals Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, transforming complex resource data into clear, actionable insights for both short-term traders and long-term investors — explore historic discoveries and the substantial returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.