May 13, 2026

Mexico's evolving energy landscape presents compelling opportunities for addressing long-standing import dependencies through innovative extraction technologies. Hydraulic fracturing in Mexico represents a paradigmatic shift from ideological opposition to pragmatic energy security considerations, driven by economic pressures and technological advances that promise reduced environmental impacts.

The complex geology underlying Mexico's energy landscape represents a paradigm shift from conventional resource extraction methodologies. Unlike traditional drilling operations that target naturally permeable rock formations, hydraulic fracturing in Mexico requires sophisticated engineering approaches to unlock hydrocarbons trapped within tight shale formations. Furthermore, understanding these energy transition strategies becomes crucial for long-term planning.

Table: Hydraulic Fracturing vs Conventional Drilling Comparison

| Aspect | Conventional Drilling | Hydraulic Fracturing |

|---|---|---|

| Rock Permeability | High (naturally porous) | Low (requires artificial fracturing) |

| Well Depth | 1,000-3,000 meters | 2,000-5,000+ meters |

| Water Usage | 100,000-500,000 gallons | 2-8 million gallons per well |

| Production Timeline | 20-40 years | 5-15 years |

| Environmental Footprint | Smaller surface area | Larger surface operations |

Mexican shale formations, particularly those resembling Texas Eagle Ford and Louisiana Haynesville equivalents, present unique geological challenges. The Burgos Basin's Cretaceous-age organic-rich shales require pressure differentials significantly higher than conventional wells, with formation pressures exceeding 8,000 pounds per square inch (PSI) at target depths.

The Science Behind Shale Gas Liberation

Modern hydraulic fracturing operations deploy precisely engineered fluid systems to create micro-fracture networks extending hundreds of feet from wellbores. The process involves injecting 90-95% water, 4-9% proppants, and 0.5-2% chemical additives under extreme pressure to overcome the natural tensile strength of shale rock formations.

Mexico's geological formations present specific technical considerations absent from North American analogues. The Sabinas Basin's Haynesville-equivalent formations contain higher clay content, requiring modified fluid chemistry to prevent formation damage. Advanced ceramic proppants, rather than conventional sand, become essential for maintaining fracture conductivity in these clay-rich environments.

Moreover, AI drilling innovations are revolutionising operational efficiency and safety standards. These technological advances help optimise drilling parameters and reduce environmental impacts.

Contemporary fracturing operations increasingly utilise closed-loop water systems and advanced filtration technologies, achieving water recycling rates exceeding 80% whilst reducing freshwater consumption through brackish water sourcing and produced water treatment.

Real-time monitoring technologies now enable operators to track induced seismicity during fracturing operations, with seismic arrays detecting micro-earthquakes as small as magnitude -2.0. These monitoring systems become particularly critical in Mexico's tectonically active regions, where natural seismic activity requires careful distinction from induced events.

When big ASX news breaks, our subscribers know first

Quantifying Mexico's Shale Gas Potential

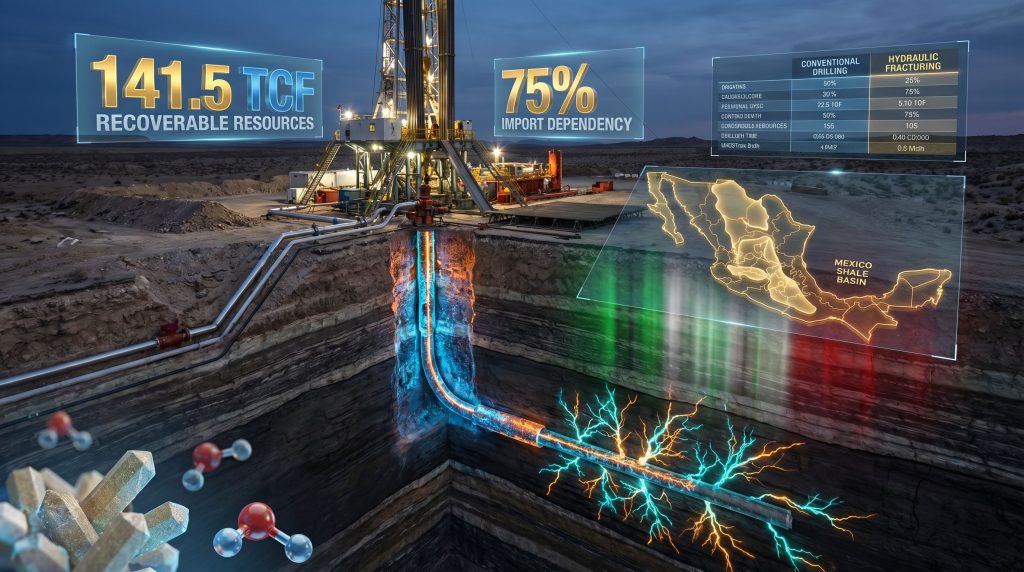

Mexico's unconventional gas endowment represents one of the world's most significant undeveloped shale resources, with 141.5 trillion cubic feet (TCF) of technically recoverable reserves distributed across four major sedimentary basins. This resource base positions Mexico as a potential game-changer in North American energy markets.

Table: Mexico's Major Shale Gas Basins

| Basin | Estimated Reserves (TCF) | Primary States | Geological Formation |

|---|---|---|---|

| Burgos | 45.2 | Tamaulipas, Nuevo León | Eagle Ford equivalent |

| Sabinas | 38.7 | Coahuila | Haynesville equivalent |

| Tampico-Misantla | 31.4 | Veracruz, Puebla | Jurassic shales |

| Veracruz | 26.2 | Veracruz | Cretaceous formations |

The Burgos Basin's 45.2 TCF represents the crown jewel of Mexico's shale potential, with geological characteristics closely resembling the prolific Eagle Ford formation that transformed Texas energy production. However, critical distinctions emerge in thermal maturity and kerogen composition, with Mexican formations exhibiting higher gas-to-oil ratios due to deeper burial depths and elevated geothermal gradients.

Fernando Cruz, Director of Energy at Kannbal Consulting, emphasised the urgency of policy decisions, stating that industry consensus recognises the inevitability of Mexico's shift toward unconventional resources development, despite previous ideological opposition.

Comparing Mexico's Position in Global Shale Gas Rankings

Mexico ranks sixth globally in technically recoverable shale gas resources, trailing China (1,115 TCF), Argentina (802 TCF), Algeria (707 TCF), the United States (665 TCF), and Canada (573 TCF). This positioning understates Mexico's strategic advantages, including proximity to established North American energy infrastructure and regulatory frameworks.

Table: Global Shale Gas Resource Rankings

| Rank | Country | Technically Recoverable Resources (TCF) | Development Status |

|---|---|---|---|

| 1 | China | 1,115 | Early development |

| 2 | Argentina | 802 | Active (Vaca Muerta) |

| 3 | Algeria | 707 | Exploration phase |

| 4 | United States | 665 | Mature production |

| 5 | Canada | 573 | Active development |

| 6 | Mexico | 141.5 | Pre-development |

Mexico's resource base could theoretically supply domestic natural gas consumption for approximately 50-60 years at current demand levels, assuming static consumption patterns. However, accelerated industrial development and LNG export potential could significantly alter this timeline, particularly if Mexico develops integration strategies with Texas refining and petrochemical complexes.

Energy Security Vulnerabilities Driving Policy Change

Mexico's 75% natural gas import dependency has created strategic vulnerabilities exposed during recent geopolitical crises. The US-Iran conflict that pushed Brent crude above $97 per barrel demonstrated how single-supplier dependencies can trigger energy inflation across entire economic sectors. These global trade dynamics significantly impact national energy security.

Key Energy Security Risks:

• Price volatility exposure to North American spot markets

• Infrastructure bottlenecks at cross-border pipeline capacity

• Geopolitical leverage concerns in bilateral trade negotiations

• Foreign exchange pressure from energy import costs

• Limited supply diversification options

The structural pressure behind Mexico's policy shift reflects harsh economic realities. Natural gas price increases of 340% between 2020-2024 added approximately $8.2 billion annually to the country's energy import bill, creating inflationary pressures across electricity generation and industrial manufacturing sectors.

Economic Pressures Reshaping Political Calculations

President Claudia Sheinbaum's trajectory on hydraulic fracturing in Mexico demonstrates remarkable policy evolution. During her presidential campaign, she explicitly committed to prohibiting fracking operations. Within months of taking office, her administration embraced "sustainable technology" frameworks for unconventional gas extraction, establishing a scientific committee led by UNAM rector Leonardo Lomelí.

The transition from ideological opposition to pragmatic acceptance occurred within an 18-month window, demonstrating how energy security crises can rapidly reshape long-standing political positions on controversial extraction technologies.

Canada's Energy Minister Tim Hodgson described this phenomenon as "value-based pragmatism," emphasising that governments must engage the world as it exists rather than as they wish it existed. This perspective reflects broader centre-left political recalculations on fossil fuel policies across North America.

Water Resource Management Challenges

Mexico's semi-arid climate conditions create significant constraints for hydraulic fracturing in Mexico. Each horizontal well requires 2-8 million gallons of water, with peak drilling scenarios potentially consuming water equivalent to supplying 50,000-200,000 people annually. This scale demands innovative water management strategies.

Table: Water Stress Analysis by Proposed Fracking Region

| State | Water Stress Level | Annual Precipitation (mm) | Competing Water Uses |

|---|---|---|---|

| Coahuila | Extremely High | 250-400 | Agriculture, Mining, Municipal |

| Tamaulipas | High | 400-800 | Agriculture, Industry |

| Veracruz | Moderate | 1,200-2,000 | Agriculture, Tourism |

| Puebla | High | 600-1,000 | Agriculture, Municipal |

Advanced water recycling technologies offer potential solutions to scarcity constraints. Modern fracturing operations achieve 80-90% water recycling rates through multi-stage treatment systems that process flowback water for reuse in subsequent fracturing operations. Brackish groundwater sources and produced water treatment can further reduce freshwater consumption.

Coahuila, identified as the probable pilot programme location, presents the greatest water challenges with extremely high stress levels and annual precipitation below 400mm. This necessitates mandatory water recycling requirements and potential sourcing from non-potable aquifers to avoid competing with agricultural and municipal uses.

Community Health and Environmental Justice Concerns

Indigenous and rural communities in proposed fracking zones have documented concerns about air quality degradation, groundwater contamination risks, and increased industrial traffic impacts. Historical drilling activities in the Burgos Basin provide relevant precedent for potential environmental impacts.

Documented Environmental Concerns:

• Methane emissions affecting local air quality standards

• Potential groundwater contamination from wellbore integrity failures

• Noise pollution from continuous drilling operations

• Road damage and safety concerns from heavy truck traffic

• Induced seismicity risks in tectonically active regions

The scientific committee's mandate includes developing comprehensive environmental monitoring protocols that exceed current international standards. Real-time air quality monitoring, groundwater protection measures, and seismic activity tracking represent minimum requirements for social acceptance of hydraulic fracturing in Mexico.

Cost Structure Analysis for Unconventional Gas Development

Mexican shale gas development faces higher breakeven costs compared to conventional production, with estimated development costs ranging from $4-8 per thousand cubic feet (MCF) versus $1-3 per MCF for conventional wells. These economics require sustained natural gas prices above $4-5 per MCF for commercial viability.

Table: Energy Source Cost Comparison (Mexico Context)

| Energy Source | Development Cost ($/MCF equivalent) | Infrastructure Requirements | Timeline to Production |

|---|---|---|---|

| Conventional Natural Gas | $1-3 | Moderate | 6-18 months |

| Shale Gas (Fracking) | $4-8 | High | 12-36 months |

| LNG Imports | $6-12 | Port infrastructure | 24-60 months |

| Renewable + Storage | $8-15 | Grid integration | 18-48 months |

Higher drilling costs in Mexico reflect several factors: deeper target formations, more complex geology, limited service sector infrastructure, and stricter environmental compliance requirements. However, proximity to Texas markets and established pipeline infrastructure provide cost advantages absent in other emerging shale regions.

Additionally, the US natural gas forecast indicates favourable market conditions for Mexican development initiatives.

Investment Requirements and Financial Feasibility

Developing Mexico's shale gas resources requires estimated capital investments of $150-200 billion over 15-20 years, including drilling operations, pipeline infrastructure, processing facilities, and environmental compliance systems. This investment scale necessitates significant private sector participation and favourable regulatory frameworks.

Per-well development costs in Mexican formations are projected at $8-12 million, compared to $6-8 million for comparable wells in Texas Eagle Ford operations. Higher costs reflect Mexico's nascent service sector, environmental compliance requirements, and initial learning curve effects as operators adapt to local geological conditions.

The financial feasibility depends critically on sustained natural gas price differentials between Mexican domestic markets and North American export prices. Current price spreads of $2-4 per MCF provide adequate margins for profitable operations, assuming successful technology transfer and regulatory clarity.

Trade Agreement Implications for Energy Policy

The USMCA review process has highlighted Mexico's energy import dependency as a bilateral trade issue. Outstanding Pemex payments to US suppliers exceeding $2.5 billion create diplomatic tensions whilst demonstrating the fiscal burden of import dependency during price volatility periods.

Domestic production could address trade balance concerns whilst reducing bilateral energy dependencies that complicate diplomatic relationships. Energy independence through unconventional gas development offers Mexico greater negotiating flexibility in future USMCA reviews and reduces vulnerability to US energy policy changes.

Strategic Autonomy Considerations

Energy security considerations extend beyond economic factors to encompass geopolitical strategy. Mexico's current dependency on Texas pipeline imports creates leverage imbalances that affect broader bilateral negotiations on trade, immigration, and security cooperation.

Successful shale gas development could fundamentally alter North American energy dynamics, potentially positioning Mexico as an LNG exporter rather than importer by 2035. This transformation would require coordinated development of export infrastructure and international marketing strategies targeting Asian and European markets.

The next major ASX story will hit our subscribers first

International Case Studies in Shale Gas Policy Evolution

Argentina's Vaca Muerta Experience

Argentina's Vaca Muerta shale formation development demonstrates both opportunities and challenges for Latin American unconventional gas development. Since 2013, Argentina has attracted over $20 billion in foreign investment whilst implementing environmental regulations and community consultation requirements that provide relevant precedents for Mexico.

Vaca Muerta's production history reveals critical lessons for Mexican development strategies. Initial development phases achieved significant production growth, but recent years have shown vulnerability to commodity price volatility and regulatory uncertainty. Investment momentum decreased substantially during 2022-2024 due to inflation concerns and currency instability.

Key Vaca Muerta Lessons for Mexico:

• Environmental compliance costs represent 15-20% of total development expenditures

• Community engagement programmes require 12-18 months of advance consultation

• Regulatory consistency proves more important than initial permissive frameworks

• Infrastructure development timelines often exceed drilling operation schedules

Canada's Regulatory Framework Evolution

Canada's experience provides relevant precedents for environmental regulation and Indigenous consultation protocols. Alberta and British Columbia have implemented comprehensive frameworks balancing development objectives with environmental protection.

Canadian regulatory innovations include mandatory water recycling requirements, real-time emissions monitoring systems, and Indigenous consultation protocols that ensure community participation in development decisions. These frameworks achieve social acceptance whilst maintaining commercial viability for operators.

Technology Transfer and Best Practices

International cooperation on environmental technologies enables newer shale gas operations to achieve significantly reduced environmental footprints through advanced water recycling systems, real-time emissions monitoring, and reduced-impact drilling techniques. Furthermore, understanding decarbonisation benefits helps inform sustainable development approaches.

Modern Environmental Technologies:

• Advanced water recycling systems reducing freshwater consumption by 80-90%

• Real-time emissions monitoring and leak detection technologies

• Reduced-impact drilling techniques minimising surface disturbance

• Closed-loop drilling systems eliminating waste pit requirements

Scenario Modelling for 2030-2040 Energy Transition

Successful shale gas development could fundamentally alter Mexico's energy landscape, potentially reducing natural gas imports from 75% to 25-30% by 2035 whilst providing transitional fuel for renewable energy integration. Multiple development scenarios present different risk-reward profiles for policymakers.

Table: Energy Mix Scenarios for Mexico (2030-2040)

| Scenario | Natural Gas (Domestic %) | Renewable % | Oil % | Coal % |

|---|---|---|---|---|

| Status Quo | 25% | 35% | 30% | 10% |

| Moderate Shale Development | 45% | 40% | 12% | 3% |

| Accelerated Shale Development | 60% | 35% | 4% | 1% |

Moderate development scenarios assume 500-1,000 wells annually across all basins, requiring $15-20 billion in annual capital investment. This pace could achieve energy independence by 2032 whilst maintaining social acceptance through gradual ramp-up periods and comprehensive environmental monitoring.

Accelerated development scenarios involve 1,500-2,500 wells annually, potentially achieving LNG export capability by 2030. However, this timeline assumes resolution of water scarcity concerns, community acceptance, and successful technology transfer from North American operators.

Integration with Renewable Energy Strategy

Natural gas from domestic shale formations serves as optimal backup power for renewable energy systems, enabling higher renewable penetration whilst maintaining grid stability. This integration strategy aligns with Mexico's climate commitments whilst ensuring energy security during renewable energy transitions.

Domestic production provides transitional fuel supporting renewable energy deployment through:

• Grid balancing services during solar and wind intermittency periods

• Industrial process heat for manufacturing and petrochemical sectors

• Feedstock for hydrogen production supporting long-term decarbonisation goals

• Backup power generation capacity during extreme weather events

The integration timeline requires coordinated planning between unconventional gas development and renewable energy deployment. Optimal scenarios achieve peak gas production during the 2030-2035 period, followed by gradual decline as renewable capacity and storage technologies mature.

Frequently Asked Questions About Hydraulic Fracturing in Mexico

Is fracking banned in Mexico?

No, fracking is not currently banned. Whilst former President López Obrador imposed restrictions on new fracking permits between 2018-2024, President Sheinbaum's administration has announced plans to resume unconventional gas development using "sustainable technologies" starting in 2026.

The scientific committee led by UNAM rector Leonardo Lomelí has a two-month mandate to deliver feasibility assessments for pilot programmes, with Coahuila identified as the likely initial development zone. This represents a complete reversal from previous administrative positions opposing unconventional extraction techniques.

How much water does fracking use compared to other industries?

Operations typically require 2-8 million gallons of water per well, equivalent to the annual water consumption of 15-60 average Mexican households. However, this represents less than 1% of total water consumption in proposed fracking regions, where agriculture accounts for 70-80% of water use.

Advanced recycling technologies can reduce freshwater consumption by 80-90% through flowback water treatment and reuse systems. Brackish groundwater sources and produced water recycling further minimise competition with agricultural and municipal water supplies in water-stressed regions like Coahuila.

What environmental protections are planned for Mexico's fracking operations?

The scientific committee is developing environmental protocols including mandatory water recycling, air quality monitoring, seismic activity tracking, and community consultation requirements. These standards are expected to exceed current international best practices based on lessons learned from North American and Argentine operations.

Planned Environmental Protections:

• Real-time air quality monitoring with public data access

• Comprehensive groundwater protection and monitoring systems

• Seismic monitoring networks detecting induced earthquake activity

• Mandatory community consultation periods before permit approvals

• Water recycling requirements exceeding 80% flowback recovery rates

The regulatory framework emphasises "sustainable technology" approaches that minimise environmental impacts whilst achieving energy security objectives. Implementation timelines allow 18-24 months for comprehensive environmental baseline studies before commercial operations begin.

Furthermore, Mexico's evolving energy security policies reflect broader trends toward strategic resource development that balance environmental concerns with economic necessities. Additionally, environmental advocacy groups continue raising important questions about long-term sustainability impacts.

Disclaimer: This article contains analysis and projections based on current policy announcements and industry trends. Actual development timelines, environmental impacts, and economic outcomes may differ significantly from projections. Energy investment decisions involve substantial risks and should be evaluated with professional advice. Regulatory frameworks and environmental requirements are subject to change based on scientific committee recommendations and public consultation processes.

Ready to Capitalise on Mexico's Energy Revolution?

Discovery Alert's proprietary Discovery IQ model provides real-time alerts on significant ASX mineral discoveries, including critical energy transition minerals essential for Mexico's evolving resource landscape. Explore how historic discoveries can generate substantial returns and begin your 14-day free trial today to position yourself ahead of the market in the rapidly changing energy sector.