July 22, 2026

Understanding the Economic Forces Behind Hydrogen's Market Acceleration

The global energy landscape stands at an unprecedented crossroads where technological maturation, policy alignment, and market demand convergence are creating transformative conditions for hydrogen adoption. This pivotal hydrogen moment represents more than incremental progress; it signals a fundamental shift in how industrial economies approach energy security, carbon reduction, and long-term competitiveness.

Traditional energy paradigms that dominated industrial processes for decades are encountering mounting pressure from multiple directions. Carbon pricing mechanisms increasingly favor cleaner alternatives, while supply chain disruptions have highlighted the vulnerability of fossil fuel dependence. Simultaneously, technological breakthroughs in electrolysis efficiency and renewable energy integration are rapidly closing cost gaps that previously made hydrogen economically unviable for widespread adoption.

When big ASX news breaks, our subscribers know first

Quantifying the Investment Surge in Clean Hydrogen Infrastructure

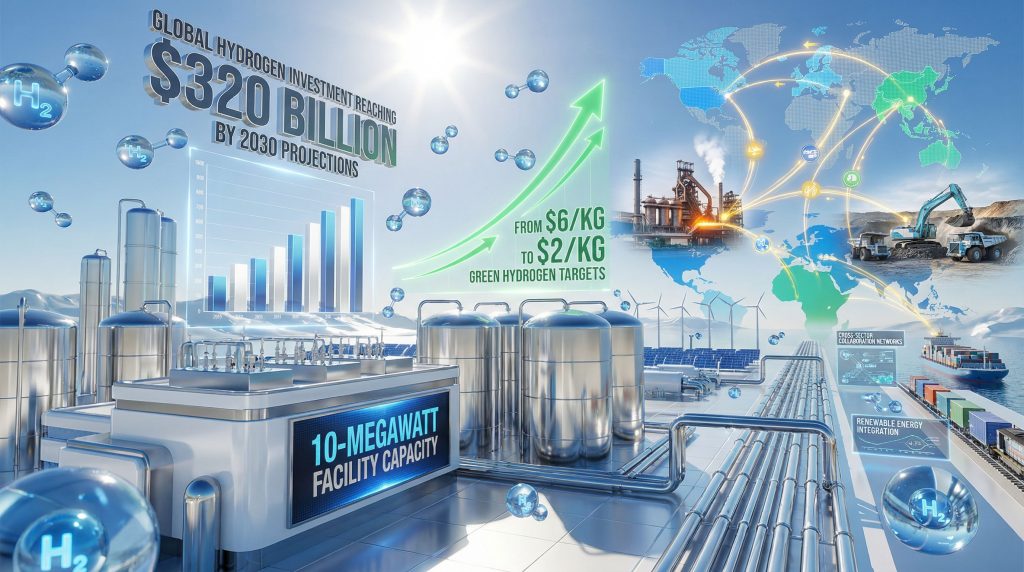

Global capital allocation toward hydrogen infrastructure has reached extraordinary momentum, with cumulative investments projected to approach $320 billion by 2030. This funding surge encompasses both public sector commitments and private capital deployment, creating a multi-layered financial ecosystem that reduces project risk while accelerating deployment timelines.

The investment landscape reveals sophisticated financing mechanisms that combine government incentives, green bonds, and venture capital to bridge the traditional gap between early-stage technology and commercial viability. Development finance institutions are providing patient capital for infrastructure projects, while pension funds and sovereign wealth funds are increasingly viewing hydrogen assets as essential portfolio diversification tools.

Cost reduction trajectories demonstrate remarkable progress, with green hydrogen production costs declining from approximately $6 per kilogram in recent years toward targeted levels of $2 per kilogram by 2030. This trajectory depends heavily on electrolyzer manufacturing scale-up, renewable energy cost declines, and operational efficiency improvements across the entire hydrogen value chain.

Key Investment Drivers:

- Electrolyzer manufacturing capacity expansion

- Renewable energy generation dedicated to hydrogen production

- Storage and distribution infrastructure development

- End-use application technology advancement

- Workforce training and development programs

Supply Chain Integration Patterns Across Industrial Sectors

Industrial hydrogen adoption is following distinct integration patterns that reflect sector-specific requirements, risk tolerance, and capital availability. Mining operations are emerging as early adopters, with hydrogen-powered trucks leading the way in transforming mining transportation while capitalising on their existing industrial infrastructure and technical expertise.

Furthermore, refinery partnerships represent another significant adoption pathway, where facilities are incorporating hydrogen into existing processing workflows to reduce carbon intensity while maintaining operational continuity. These partnerships demonstrate how incumbent industries can transition gradually without requiring complete operational overhauls.

Cross-sector collaboration models are developing between traditional fossil fuel companies and renewable energy developers, creating integrated value chains that optimise both supply reliability and cost efficiency. These partnerships often involve shared infrastructure investments, risk distribution mechanisms, and technology transfer agreements that accelerate learning curves across participating organisations.

Integration Success Factors:

- Existing industrial infrastructure compatibility

- Technical workforce capabilities

- Capital availability and financing access

- Regulatory framework certainty

- Market demand visibility

How Are Regional Hydrogen Hubs Reshaping Global Energy Geography?

Regional hydrogen development patterns are creating new energy trade relationships that could fundamentally alter global energy geography. These emerging hubs combine natural resource advantages, policy support, and industrial demand to create competitive advantages that extend beyond traditional energy exporting regions.

North American Green Hydrogen Corridor Development

Canadian hydrogen initiatives are demonstrating industrial scalability through integrated projects that combine renewable energy generation, hydrogen production, and end-use applications within single geographic regions. Pulp mill integration projects serve as proving grounds for broader industrial adoption, showing how hydrogen can replace natural gas in heat-intensive processes while maintaining production efficiency.

10-megawatt facility capacity benchmarks are emerging as minimum viable scale for industrial hydrogen applications, providing reference points for project developers and investors evaluating deployment opportunities. These benchmarks reflect the balance between capital efficiency, operational reliability, and economies of scale necessary for commercial viability.

Natural gas displacement economics in heavy industry applications reveal increasingly favourable conditions for hydrogen adoption. As carbon pricing mechanisms expand and natural gas price volatility continues, hydrogen's value proposition strengthens particularly in regions with abundant renewable energy resources and supportive policy frameworks.

European Hydrogen Valley Network Expansion

European hydrogen development follows a coordinated approach that emphasises cross-border integration and standardisation to create continent-wide hydrogen markets. Policy framework alignment supports long-term investment planning by reducing regulatory uncertainty and enabling economies of scale across multiple national jurisdictions.

Infrastructure investment priorities for 2026-2030 focus on backbone pipeline development that connects production hubs with demand centres, creating the foundation for liquid hydrogen trading markets. These investments require unprecedented coordination between national governments, European Union institutions, and private sector participants.

Energy security implications have gained prominence amid geopolitical supply chain diversification efforts, positioning hydrogen as both a domestic energy source and a tool for reducing dependence on volatile international energy markets. This aligns with broader resource energy exports considerations that countries are making to secure their energy future.

Asia-Pacific Hydrogen Market Dynamics

Industrial conglomerate participation in hydrogen development signals long-term strategic commitment beyond short-term profit optimisation. Board-level engagement from major industrial groups provides project stability and access to integrated supply chains that accelerate deployment timelines.

Technology transfer partnerships between established industrial companies and emerging hydrogen specialists are creating knowledge-sharing mechanisms that accelerate technical development while distributing risks across multiple participants.

Export-import balance shifts are becoming apparent as traditional energy importers develop domestic hydrogen production capabilities, potentially reducing their reliance on international energy markets while creating new export opportunities. The critical minerals transition plays a crucial role in supporting these hydrogen infrastructure developments.

What Economic Barriers Are Preventing Faster Hydrogen Scale-Up?

Despite impressive investment momentum and technological progress, several economic barriers continue constraining hydrogen market development. Understanding these limitations provides insight into timeline expectations and strategic priorities for market participants.

Production Cost Analysis and Competitive Positioning

Electrolysis efficiency improvements remain central to hydrogen cost competitiveness, with current technology requiring continued advancement to achieve parity with conventional alternatives. While learning curves demonstrate consistent progress, the pace of improvement must accelerate to meet aggressive deployment targets.

Capital expenditure requirements for gigawatt-scale facilities present financing challenges that extend beyond traditional project finance structures. These projects require patient capital, long-term off-take agreements, and sophisticated risk management approaches that are still developing within financial markets.

Operating expense optimisation through automation and process integration offers significant cost reduction potential, but requires operational experience that can only be gained through commercial deployment. This creates a circular challenge where cost reduction depends on scale, while scale depends on cost competitiveness.

Cost Structure Components:

| Element | Current Impact | Improvement Potential |

|---|---|---|

| Electrolyzer CAPEX | 40-50% of total cost | High – manufacturing scale |

| Electricity Input | 30-40% of operating cost | Medium – renewable energy costs |

| Balance of System | 15-20% of total cost | Medium – standardisation |

| Operations & Maintenance | 5-10% annually | High – automation potential |

Demand Creation Challenges in Key Industrial Sectors

Steel production hydrogen adoption faces complex technical and economic hurdles that extend beyond simple fuel switching. Existing infrastructure, workforce capabilities, and product quality considerations require careful management during transition periods.

Transportation sector fleet conversion presents coordination challenges between vehicle manufacturers, refuelling infrastructure developers, and fleet operators. The interdependencies between these stakeholders create deployment barriers that require coordinated approaches and risk-sharing mechanisms.

Power generation backup system applications offer promising near-term opportunities, but require demonstration of reliability and cost-effectiveness compared to established alternatives like natural gas peaking plants and battery storage systems.

Which Market Signals Indicate Hydrogen's Tipping Point Arrival?

Several converging market signals suggest hydrogen may be approaching a critical inflection point where adoption accelerates beyond current linear growth patterns. These indicators provide insight into timing and probability of widespread commercial deployment.

Corporate Strategic Alliance Formation Patterns

Multi-industry board appointments reflect strategic integration thinking that extends beyond single-sector optimisation. When executives from diverse industrial backgrounds join hydrogen company boards, it signals expectation of cross-industry value chain development and market expansion.

Technology licensing agreements are accelerating deployment speed by enabling rapid technology transfer between organisations with complementary capabilities. These agreements reduce development timelines while distributing risks across multiple participants.

Joint venture structures optimising risk distribution and capital efficiency demonstrate sophisticated approaches to managing hydrogen project uncertainties. These structures often combine technical expertise, financial resources, and market access in ways that individual organisations cannot achieve independently.

Policy Convergence Creating Market Certainty

Carbon pricing mechanisms increasingly favour hydrogen over traditional alternatives, creating economic incentives that supplement technological improvements. As carbon prices rise and coverage expands, hydrogen's value proposition strengthens across multiple applications.

Regulatory standardisation efforts reduce compliance complexity and enable economies of scale across multiple jurisdictions. Harmonised technical standards, safety protocols, and certification requirements lower barriers to market entry and technology transfer.

International trade agreement provisions supporting hydrogen commerce signal governmental commitment to developing global hydrogen markets. These provisions create legal frameworks for hydrogen trade while addressing technical barriers and quality standards.

Financial Market Recognition Through Investment Flows

Institutional investor portfolio allocation shifts toward hydrogen assets reflect changing risk-return expectations and long-term strategic positioning. When pension funds and sovereign wealth funds increase hydrogen investments, it signals confidence in long-term market viability.

Green bond issuance specifically targeting hydrogen infrastructure provides dedicated capital sources while meeting environmental, social, and governance investment criteria. This funding source offers lower cost capital compared to traditional project finance while extending investment horizons.

Venture capital deployment in hydrogen technology startups continues accelerating, focusing on breakthrough technologies that could eliminate remaining economic barriers. This investment pattern suggests continued technological advancement potential.

The next major ASX story will hit our subscribers first

How Will Hydrogen Economics Transform Traditional Energy Markets?

Hydrogen market development will likely create cascading effects throughout traditional energy systems, altering competitive dynamics, investment priorities, and long-term strategic planning across multiple sectors.

Displacement Scenarios for Conventional Energy Sources

Natural gas market share erosion in industrial heating applications appears increasingly probable as hydrogen cost competitiveness improves and carbon pricing expands. This displacement could begin in regions with abundant renewable energy and supportive policy frameworks before expanding globally.

Coal replacement timelines in steel and cement production depend heavily on technology demonstration success and financial support mechanisms. While technical pathways exist, commercial deployment requires continued cost reduction and operational refinement.

Petroleum product substitution in heavy transport and shipping faces complex infrastructure requirements and international coordination challenges. Success in these applications could significantly impact global oil demand patterns, but deployment timelines remain uncertain.

Displacement Timeline Estimates:

- Industrial heating: 5-10 years in leading regions

- Steel production: 8-15 years for widespread adoption

- Heavy transport: 10-20 years depending on infrastructure

- Maritime fuel: 15-25 years for international adoption

Grid Integration and Energy Storage Market Implications

Seasonal energy storage economics position hydrogen favourably compared to battery alternatives for long-duration storage applications. While batteries excel in short-duration applications, hydrogen's energy density advantages become apparent for weekly or seasonal storage requirements.

Peak demand management through hydrogen power generation offers grid operators flexible capacity that complements renewable energy variability. This application could become economically attractive before broader industrial adoption, providing early market development opportunities.

Renewable energy curtailment reduction via hydrogen production addresses a growing challenge in renewable-heavy power systems. Converting excess renewable generation to hydrogen creates value from otherwise wasted energy while supporting renewable energy investment economics.

What Investment Opportunities Emerge from This Pivotal Moment?

The convergence of technological readiness, policy support, and market demand creates diverse investment opportunities across the hydrogen value chain. Understanding these opportunities requires analysis of risk-return profiles, timeline expectations, and competitive positioning.

Infrastructure Development Investment Themes

Pipeline and distribution network expansion represents foundational infrastructure investment with potentially attractive long-term returns. These assets offer regulated utility-like characteristics while supporting broader market development.

Port facility modifications for hydrogen import/export capabilities position investors to benefit from emerging global hydrogen trade. These investments combine traditional infrastructure characteristics with exposure to growing international hydrogen markets.

Industrial facility retrofitting for hydrogen compatibility offers opportunities to partner with established industrial companies during their transition processes. These investments often benefit from existing customer relationships and operational expertise.

Technology Innovation Investment Priorities

Electrolyzer manufacturing scale-up opportunities exist across the supply chain, from component manufacturing to system integration. Companies achieving cost reduction breakthroughs while maintaining quality and reliability could capture significant market share.

Fuel cell efficiency improvement research and development continues offering breakthrough potential that could accelerate market adoption. Investment in this area requires longer time horizons but offers potential for transformative returns.

However, recent research has highlighted concerns about overlooked hydrogen emissions that could impact environmental benefits, requiring careful consideration in investment decisions.

Carbon capture integration with blue hydrogen production creates opportunities to combine existing industrial processes with emerging carbon management requirements. This approach offers transition pathways for fossil fuel-dependent regions.

Resource Sector Integration Opportunities

Mining operation decarbonisation through hydrogen adoption offers investment opportunities that combine environmental benefits with operational efficiency improvements. Mining companies with abundant renewable energy resources may offer particularly attractive investment prospects.

Precious metals demand from fuel cell manufacturing growth creates secondary investment opportunities in materials markets. Platinum, iridium, and other catalyst materials could experience significant demand increases as fuel cell production scales.

Critical minerals supply chain development for hydrogen technologies mirrors broader energy transition investment themes while offering exposure to growing hydrogen markets. These investments often benefit from government support and strategic importance.

For investors seeking to navigate these complex opportunities, understanding comprehensive investment strategies 2025 becomes essential for successful portfolio allocation.

Frequently Asked Questions About Hydrogen's Economic Impact

When Will Hydrogen Achieve Cost Parity with Fossil Fuels?

Cost parity timelines vary significantly by region, application, and fossil fuel price assumptions. Leading regions with abundant renewable energy and supportive policies may achieve parity within 5-7 years for specific applications, while broader global parity could require 8-12 years.

Subsidy phase-out scenarios and market sustainability depend on achieving sufficient cost reductions during supported development phases. Learning curve effects from manufacturing scale increases suggest continued cost improvement potential, but the rate of improvement remains uncertain.

Regional variation in cost competitiveness reflects differences in renewable energy resources, policy support, industrial demand, and existing infrastructure. Early parity achievement in advantaged regions could accelerate technology development and cost reduction for global markets.

Which Industries Will Drive Hydrogen Demand Growth?

Industrial heat applications appear most likely to drive near-term demand growth due to technical readiness and economic competitiveness compared to alternatives. Steel production represents the largest potential demand source, but requires longer development timelines.

Transportation sector demand growth depends heavily on infrastructure development coordination and vehicle availability. Heavy-duty transportation may precede light-duty adoption due to centralised refuelling requirements and fleet operator decision-making processes.

Power generation applications offer intermediate demand potential, particularly for backup systems and grid balancing services. This application could provide early market development while industrial demand scales.

How Will Hydrogen Trade Reshape Global Energy Markets?

Export-import relationship development between regions could create new energy interdependencies that differ from traditional oil and gas trade patterns. Hydrogen trade may favour regions with abundant renewable energy resources rather than traditional fossil fuel exporters.

Shipping and pipeline infrastructure investment requirements represent significant capital commitments that will influence trade pattern development. Early infrastructure investments may create competitive advantages and lock-in effects for specific trade routes.

Trade agreement implications for hydrogen commerce continue evolving as governments develop regulatory frameworks and international standards. These developments will significantly influence global hydrogen market structure and competitive dynamics.

Strategic Implications for Energy Market Participants

Traditional Energy Company Adaptation Strategies

Portfolio diversification into hydrogen value chains offers established energy companies opportunities to leverage existing capabilities while participating in energy transition trends. Successful adaptation requires balancing traditional business performance with long-term strategic positioning.

Existing infrastructure repurposing for hydrogen applications provides cost-effective entry strategies while extending asset life cycles. Natural gas pipelines, storage facilities, and industrial sites may offer conversion opportunities that reduce capital requirements.

Strategic partnership formation with renewable energy developers creates complementary capability combinations that neither party could achieve independently. These partnerships often focus on integrated project development that optimises both hydrogen production and end-use applications.

New Market Entrant Opportunities

Technology provider positioning in emerging hydrogen ecosystems requires understanding of customer needs, competitive dynamics, and technology integration requirements. Success often depends on developing solutions that address specific performance gaps or cost reduction opportunities.

Service company development for hydrogen facility operations creates opportunities to support growing operational requirements while building specialised expertise. These companies often benefit from recurring revenue models and close customer relationships.

Financial service innovation for hydrogen project financing addresses evolving capital requirements and risk management needs. Specialised financing approaches that understand hydrogen project characteristics could capture significant market share as the industry scales.

The current pivotal hydrogen moment presents unprecedented opportunities for stakeholders across the energy value chain. As refinery partnerships demonstrate increasing integration potential, organisations must position themselves strategically to capitalise on this transformational shift in global energy markets.

Investment Disclaimer: The hydrogen economy remains in early development stages with significant technological, market, and regulatory uncertainties. Investment decisions should consider these risks alongside potential opportunities, and investors should conduct thorough due diligence before making capital commitments. Past performance of early-stage energy technologies does not guarantee future results, and market development timelines may differ significantly from current projections.

Ready to Capitalise on the Next Energy Transition Breakthrough?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical materials essential for hydrogen infrastructure development and clean energy technologies. Stay ahead of the energy transition by identifying actionable investment opportunities in companies developing the minerals powering hydrogen's economic transformation through Discovery Alert's discoveries page, and begin your 30-day free trial today to secure your market-leading advantage.