June 8, 2026

The Uncomfortable Truth Behind the IEA Coal Investment 14-Year High

Energy markets have never moved in straight lines. History shows that every era of accelerating clean technology adoption has coexisted, at least temporarily, with continued investment in the very systems it is meant to replace. The industrial revolution did not end wood burning overnight. Natural gas did not displace oil in a decade. And the current renewable energy expansion, despite its unprecedented scale and speed, is not eliminating coal investment. If anything, the IEA coal investment hits 14-year high finding from the agency's 2026 World Energy Investment report suggests the opposite is occurring in key parts of the world, demanding a more sophisticated analytical framework than simple transition narratives allow.

Understanding why requires moving beyond headlines and examining the structural forces, geographic divergences, and geopolitical pressures that are simultaneously accelerating both renewable capacity additions and fossil fuel spending in parallel energy systems operating on entirely different timelines.

When big ASX news breaks, our subscribers know first

Two Energy Worlds Running Simultaneously

The global energy system in 2026 is not a single market undergoing a linear transformation. It is more accurately described as two overlapping systems: one predominantly found in Europe and North America, where coal is in structural decline and renewable energy dominates new investment; and another concentrated in Asia, where energy security imperatives, industrial growth requirements, and development priorities are producing an entirely different set of capital allocation decisions.

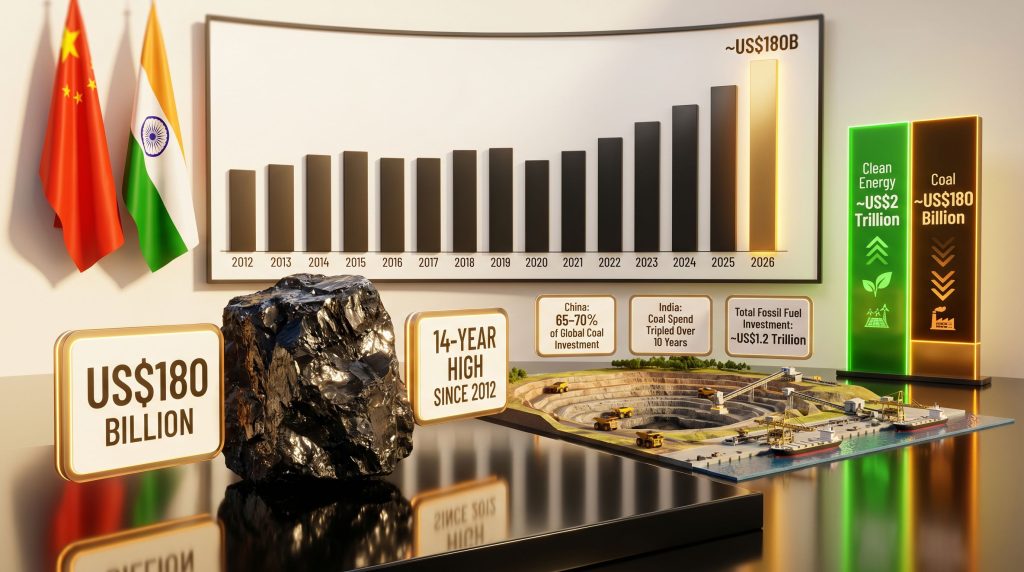

The International Energy Agency's 2026 World Energy Investment report captures this duality with unusual clarity. Total annual clean energy investment now exceeds US$2 trillion globally, a figure that represents remarkable momentum for decarbonisation. Yet sitting alongside that number is a coal investment total projected to reach approximately US$180 billion by the end of 2026, the highest recorded level since 2012 and a 4% increase from 2025 levels. Furthermore, coal supply challenges in preceding years have paradoxically reinforced the case for expanded capital deployment in production capacity.

These figures are not contradictory. They are reflective of a world where some economies are decarbonising rapidly while others are prioritising energy access, industrial output, and supply security above all else.

"The global investment data does not signal a reversal of the energy transition. It signals that the transition is proceeding unevenly, with Asian economies operating on fundamentally different planning horizons than their European counterparts."

Dissecting the US$180 Billion: Where the Capital Is Actually Going

The aggregate figure of US$180 billion encompasses several distinct categories of spending, each driven by different demand signals and policy environments.

| Coal Segment | Projected 2026 Investment Direction | Primary Driver |

|---|---|---|

| Steam Coal (Thermal Power) | Rising, ~5% year-on-year | Grid stability and power security in Asia |

| Coking Coal (Metallurgical) | Rising, ~3% year-on-year | Steel production in emerging markets |

| Rail and Port Infrastructure | Rising, led by India | Domestic supply chain buildout |

| Coal Gasification | Emerging spend | Chemical feedstock diversification |

| Total 2026 Projection | ~US$180 billion | 4% above 2025 levels |

Steam coal investment in China alone is on track to exceed US$100 billion in 2026, a figure the IEA notes is approximately double what it was a decade ago. This single national segment accounts for the majority of the global total and represents the clearest illustration of how concentrated the current investment surge actually is.

India's trajectory is also striking from a rate-of-change perspective. The country's total coal spending has tripled over the past ten years, driven by a combination of domestic production expansion through commercial mine auctions and significant infrastructure investment. Rail and port spending specifically for coal transport has risen from approximately US$5 billion to US$7 billion, reflecting the logistical challenge of moving inland production volumes to coastal industrial and export centres.

Coal gasification deserves particular attention as a less-discussed dimension of India's strategy. Rather than positioning coal purely as a combustion fuel for power generation, India is investing in the conversion of coal into chemical feedstocks, including synthetic natural gas, methanol, and ammonia. This approach allows coal to remain economically relevant even as direct combustion faces increasing scrutiny, consequently extending the commercial lifespan of domestic coal reserves beyond what conventional analysis might suggest.

The Geographic Concentration Problem

One of the most analytically important aspects of the 2026 data is what happens to the global investment figure when China is removed from the calculation. The answer is stark: without China's contribution, global coal investment would be in decline for the second consecutive year.

China accounts for between 65% and 70% of all global coal supply investment in 2026. This level of concentration means that the headline figure is, in structural terms, almost entirely a story about one country's domestic energy policy decisions. The implications for interpreting the data are significant, and China steel demand further compounds the country's outsized role in shaping global commodity investment flows.

| Country or Region | 2026 Coal Investment Focus | Scale |

|---|---|---|

| China | Steam coal production and new-build power capacity | ~65-70% of global total |

| India | Production, transport infrastructure, gasification | Fastest growing by rate of change |

| Russia | Railway and seaport expansion for East Asian exports | ~US$6 billion |

| Australia | Coking coal processing capacity | ~US$4.5 billion |

| United States and Canada | Pipeline of approved projects | 15 projects; 34 million tonnes combined capacity |

| Europe | Structural phase-out continues | Declining; no major new programmes |

Russia's position in this table warrants closer examination. The approximately US$6 billion being directed toward coal supply infrastructure is notably weighted toward export logistics rather than domestic consumption growth. Significant railway capacity expansion and seaport development are oriented toward Asian markets, reflecting Moscow's strategic pivot toward Pacific trade routes following the effective closure of European energy markets.

This infrastructure investment has consequences beyond Russia's own production figures, as it increases the accessible supply of coal to Asian buyers, potentially keeping regional prices more competitive and reducing the relative cost advantage of alternatives.

Australia's US$4.5 billion in coking coal investment, including two newly announced processing facilities and a broader project pipeline, reflects the continued global demand for metallurgical coal in steel production. In addition, green steel pricing dynamics illustrate why coking coal investment remains commercially justified — unlike thermal coal, where alternatives are increasingly cost-competitive, coking coal lacks a commercially scalable substitute in conventional steelmaking processes.

The United States and Canada present a different dynamic again. The approval pipeline of 15 projects representing 34 million tonnes of new annual capacity reflects a policy environment that has become more permissive toward coal project development. Whether these approvals translate into actual capital expenditure and operational capacity depends on market conditions, financing availability, and the pace of demand signals from Asian export markets.

How Geopolitical Instability Is Reshaping Coal's Investment Logic

Energy security has historically been the variable that overrides economic efficiency calculations, and the current geopolitical environment is providing a clear demonstration of that principle. Ongoing conflict in the Middle East has introduced material oil market disruption to supply chains serving Asian markets, affecting both physical availability and pricing stability.

When liquefied natural gas and oil shipments face route disruption or spot price volatility, coal transitions from a fuel source under competitive pressure to a strategically indispensable fallback. This shift in perception accelerates investment decisions that might otherwise have been deferred pending clearer market signals.

The IEA's analysis specifically notes that the Iran conflict and associated maritime route uncertainties are contributing to increased Asian coal demand and, consequently, to supply-side investment decisions. Thailand's energy situation illustrated the acute nature of these pressures, with the government taking the unusual step of urging residents to work from home as a conservation measure while managing constrained energy reserves.

"When the security of alternative fuel supplies becomes uncertain, coal's key advantage is its domestic producibility or regional accessibility. That characteristic transforms it from an environmental liability into a strategic asset in the eyes of energy planners managing national security requirements."

Beyond new-build activity, geopolitical anxiety is accelerating a less visible but economically meaningful category of spending: the refurbishment and life-extension of existing coal facilities. Refurbishment projects carry lower political and financial risk than greenfield development, can be executed on shorter timelines, and provide immediate security benefits for governments managing constrained energy budgets. This category of investment tends to be underrepresented in headline figures but constitutes a meaningful portion of Asia's overall coal capital deployment in 2026.

Is Conflict Duration the Key Variable for Coal Investment Trajectories?

| Scenario | Probable Investment Impact |

|---|---|

| Conflict resolution within 12 months | Investment stabilises; incremental new projects deferred |

| Prolonged disruption over 2 to 3 years | Additional Asian economies accelerate domestic coal buildout |

| Escalation affecting Strait of Hormuz | Significant acceleration; coal positioned as strategic reserve fuel across Southeast Asia |

The Wholesale Price Transmission Mechanism

For energy professionals and procurement teams operating in markets that have substantially exited coal domestically, the IEA data carries a counterintuitive implication: what happens in Asian coal markets directly affects the price environment in economies like the United Kingdom, even when those economies consume no coal themselves.

The mechanism operates through interconnected commodity markets. Coal, liquefied natural gas, and oil are substitutable at the margin in Asian power generation, meaning that shifts in relative pricing across these fuels affect spot market dynamics globally. When coal investment surges in Asia and production expands, it affects the marginal cost of energy at regional hubs that in turn influence LNG pricing benchmarks. Disruptions to global LNG supply feed directly into European wholesale gas prices, which consequently affect UK power generation costs.

John Haw, CEO of UK energy procurement firm Fidelity Energy, has highlighted this precise dynamic. His assessment, made in the context of the IEA's findings, characterises the coal investment data as an uncomfortable data point within a report that otherwise tells a compelling story about clean energy acceleration. His position is that businesses would be mistaken to treat Asian commodity market developments as geographically irrelevant, since the price transmission effects reach UK procurement decisions regardless of domestic fuel mix.

This perspective has practical implications for energy procurement strategy. Models built on assumptions of a smooth, linear decline in coal's market influence may be systematically underestimating the commodity risk embedded in wholesale energy pricing, particularly over the medium-term horizon of three to seven years when Asian coal investment now being committed will translate into operational production capacity.

The next major ASX story will hit our subscribers first

Coal Within the Broader Fossil Fuel Investment Landscape

Coal's US$180 billion investment total exists within a larger fossil fuel investment picture that the IEA projects will reach approximately US$1.2 trillion across all hydrocarbon categories in 2026. This means coal represents roughly 15% of total fossil fuel capital expenditure, with oil and gas accounting for the remainder. According to IEA coal data, the agency continues to track these investment flows as a central indicator of whether real-world capital allocation is aligning with stated climate commitments.

| Investment Category | 2026 Projected Annual Flow |

|---|---|

| Clean Energy (global) | ~US$2 trillion |

| Total Fossil Fuels | ~US$1.2 trillion |

| Coal (subset of fossil fuels) | ~US$180 billion |

| Oil and Gas (remainder) | ~US$1.02 trillion |

The relationship between these figures reveals something important about the structure of the current energy transition. Clean energy investment is growing faster than fossil fuel investment, and the gap between the two is widening. However, the absolute scale of continued fossil fuel capital deployment means that the installed base of hydrocarbon infrastructure is still expanding in aggregate, even as its share of new investment declines proportionally.

The IEA's own climate modelling makes clear that current coal investment trajectories are not consistent with internationally agreed climate targets. Global coal demand reached an all-time high in 2024, providing the demand signal that continues to justify supply-side investment decisions. Without a structural reduction in consumption, particularly across China and India, investment will continue to follow demand regardless of international policy frameworks.

This is the central tension the IEA data exposes. The policy architecture for a low-carbon transition exists. The financial flows into clean energy are genuinely substantial. But demand-side behaviour, particularly in the world's two most populous nations, continues to support coal investment at a scale that makes near-term phase-out trajectories incompatible with observed market reality. Reporting from the Northern Miner underscores how geopolitical shocks are now routinely cited as catalysts accelerating this dynamic.

What the Data Means for Energy Strategy and Market Positioning

The structural implications of a 14-year high in coal investment extend beyond environmental analysis into practical questions of market positioning, commodity risk management, and long-term energy strategy.

Several critical indicators warrant ongoing monitoring:

-

China's domestic coal policy signals — any substantive shift in Beijing's approach to energy self-sufficiency would have an outsized and immediate impact on global investment figures, given the country's 65–70% share of global coal capital expenditure

-

India's commercial mine auction programme — the pace and scale of new capacity additions through private sector participation will determine whether India's investment trajectory continues to accelerate or plateaus as infrastructure bottlenecks emerge

-

Middle East conflict duration and escalation risk — the longer the current disruptions persist, the higher the probability that additional Asian economies commit to domestic coal expansion programmes as insurance against continued supply chain volatility

-

Global coal demand trajectory post-2024 — the all-time high recorded in 2024 is the foundational demand signal sustaining current investment; demand-side policy interventions in major consuming economies represent the most powerful available lever for altering the investment outlook

-

Coal gasification and non-combustion applications — India's emerging investment in coal-to-chemicals represents a structural shift in how coal is positioned economically, potentially creating new demand categories that are not captured in conventional coal phase-out modelling

The dual-track reality of the global energy system — in which clean energy investment and coal investment are growing simultaneously rather than in opposition — is not a temporary anomaly. It reflects the genuine divergence in national energy priorities, development trajectories, and security assessments between advanced economies and the industrialising world. Analytical frameworks, investment models, and corporate energy strategies that fail to account for this complexity risk being built on assumptions that the data increasingly does not support.

"The energy transition is real. The direction is clear. But the timeline is not uniform, and the path is significantly more complicated than aggregate investment figures or single-metric analyses are capable of capturing."

Want to Track the Commodity Opportunities Emerging From Global Energy Market Shifts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including coal, metals, and energy commodities — instantly translating complex market data into actionable investment opportunities for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself ahead of the broader market.