June 8, 2026

The Processing Gap That Defines the Modern Battery Race

For decades, the global mining industry operated under a comfortable assumption: secure the ore, and the supply chain takes care of itself. That logic held reasonably well for bulk commodities like iron ore and copper. For battery-critical minerals in the era of electrification, it has proven dangerously incomplete.

Graphite is the clearest illustration of this miscalculation. While Western nations debated policies, commissioned feasibility studies, and celebrated new mine discoveries, China quietly built something far more valuable than a mining industry. It built a processing empire. Today, that empire controls not just where graphite comes from, but what graphite becomes — specifically the battery-grade Active Anode Material (AAM) that sits at the heart of every lithium-ion cell powering the electric vehicle revolution.

Understanding the Tesla Syrah graphite supply deal requires starting from this structural reality, because without it, the deal looks like a routine procurement contract. In context, it looks like something else entirely.

When big ASX news breaks, our subscribers know first

China's Processing Dominance: The Number Behind the Vulnerability

The 70/90 Problem Explained

The figures cited by Benchmark Mineral Intelligence are striking on their own terms. China produces approximately 70% of the world's naturally mined graphite and controls more than 90% of global anode manufacturing capacity. But the more important number is the gap between those two figures.

That 20-percentage-point spread between mining share and processing share is where the real competitive moat lies. It means that even graphite mined outside China frequently travels to Chinese facilities for the processing steps that transform raw flake into battery-ready anode material. The dependency is not simply on Chinese mines. It is on Chinese chemistry, Chinese industrial infrastructure, and Chinese process expertise accumulated over roughly two decades of deliberate industrial policy. The global graphite shortage is, in large part, a processing shortage rather than a mining one.

Why Export Controls Changed Everything

When Beijing introduced targeted graphite export restrictions aimed specifically at the United States in December 2024, the effect was immediate and structural. American battery manufacturers held no significant buffer inventory. There had been no domestic alternative at commercial scale. The assumption that Chinese supply would remain accessible, even in a deteriorating geopolitical environment, was exposed as precisely that: an assumption.

Furthermore, the controls did not merely create a commercial problem. They demonstrated that a foreign government could, at a moment of its choosing, switch off access to a material required for domestic energy security and automotive production. China's export controls have proven to be a powerful instrument of geopolitical leverage, and that is the context in which the Tesla Syrah graphite supply deal must be evaluated.

What the Tesla Syrah Graphite Supply Deal Actually Involves

From Contract to Crisis: A Timeline

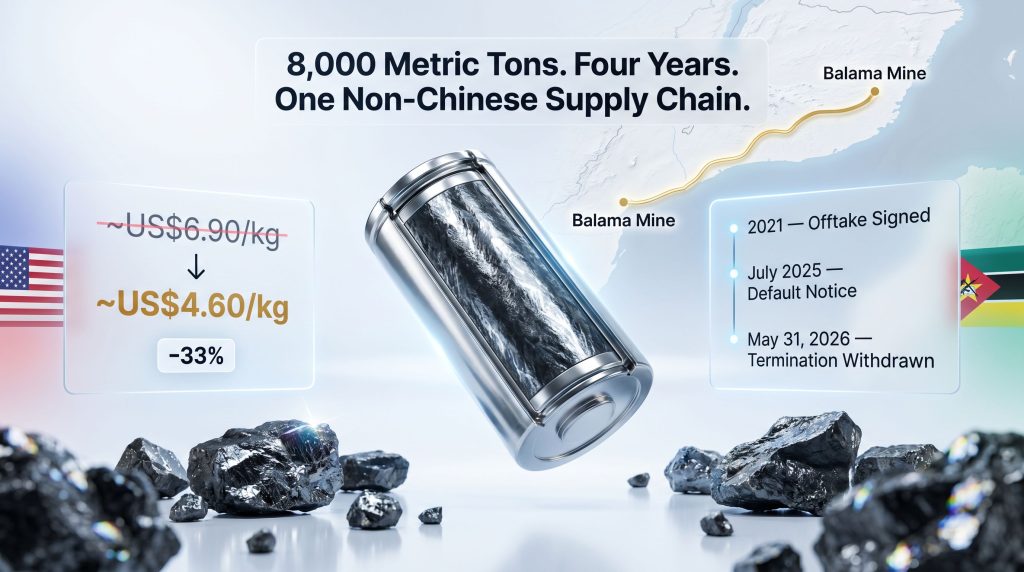

The agreement between Tesla and Syrah Resources was signed in 2021, committing Syrah to supply 8,000 metric tons of Active Anode Material over four years from its Vidalia facility in Louisiana, using raw graphite sourced from the Balama mine in Mozambique.

| Contract Parameter | Detail |

|---|---|

| Agreement Signed | 2021 |

| Material Type | Active Anode Material (AAM) |

| Volume Committed | 8,000 metric tons |

| Duration | Four years |

| Processing Location | Vidalia, Louisiana, USA |

| Raw Graphite Source | Balama Mine, Mozambique |

For three years, the deal sat largely unexamined by public attention. Then, in July 2025, Tesla issued a formal default notice after receiving non-conforming material samples from the Vidalia facility, triggering a dispute resolution process that would unfold over the better part of a year. According to reporting by Mining Weekly, Tesla ultimately dropped its threat to scrap the arrangement entirely after Syrah demonstrated meaningful progress at Vidalia.

Key milestones in the dispute resolution:

- 2021 – Offtake agreement signed between Tesla and Syrah Resources

- July 2025 – Tesla issues a formal default notice citing non-conforming AAM samples

- Late 2025 to early 2026 – Tesla extends the cure deadline four consecutive times with involvement from the US Department of Energy in approving extensions

- 31 May 2026 – Tesla withdraws its termination notice after Syrah demonstrates conforming AAM production at Vidalia

- Pending – Final product qualification and full commercial approval at scale still required

Understanding Active Anode Material

AAM is not simply mined graphite. It is the result of a multi-stage industrial process in which natural graphite flake undergoes purification, micronisation, spheroidisation, and surface coating to achieve the particle morphology and electrochemical properties required for lithium-ion battery anodes.

This transformation is technically demanding and capital intensive. It requires precision manufacturing tolerances, rigorous quality controls, and significant process chemistry expertise. The fact that this capability remains concentrated in China is not accidental. It reflects two decades of targeted industrial development that Western nations, focused on upstream mining, largely failed to replicate.

"The overwhelming majority of Western efforts to reduce Chinese graphite dependency have focused exclusively on the mining stage. The conversion of raw graphite into battery-grade anode material, the step that actually enables EV battery production, has remained almost entirely within Chinese industrial infrastructure."

What Makes Vidalia Structurally Different

Vertical Integration as the Competitive Differentiator

The Vidalia facility represents a departure from the typical Western critical minerals playbook in one critical respect: it does not stop at extraction. Raw graphite from the Balama mine in Mozambique travels to Louisiana where it is processed into finished AAM on American soil. This mine-to-anode integration is what makes the facility strategically significant beyond its individual output volume, and it is central to the broader critical minerals energy security debate unfolding across Western policy circles.

Most competing Western initiatives have sought to reduce Chinese graphite dependency by developing new mines. This addresses only the first stage of the supply problem. An anode manufacturer in the United States that sources raw graphite from a non-Chinese mine but sends it to a Chinese processor for conversion into AAM has not materially reduced its exposure to the same geopolitical risks that December 2024's export controls made tangible.

The Processing Barrier as the Real Competitive Moat

Battery qualification requirements add another layer of complexity that is frequently underestimated. Automotive-grade AAM must meet precise specifications for particle size distribution, carbon purity, surface area, and electrochemical cycling performance. Meeting those specifications once is necessary but not sufficient. Meeting them consistently at commercial volume, with batch-to-batch reproducibility, is what actually qualifies a supplier.

This is precisely the challenge that the Tesla default notice exposed. Syrah was capable of producing AAM. The question the dispute forced into the open was whether Vidalia could produce AAM that consistently met Tesla's automotive-grade specifications. Four deadline extensions later, the answer appears to be yes, though full qualification at scale remains the final hurdle.

Federal Involvement and Financial Stake

The US Department of Energy participated in approving extensions to Tesla's cure deadlines, and the federal government has provided direct financial support to the Vidalia facility as part of Washington's broader effort to develop domestic battery material supply chains. This institutional involvement is relevant not only as a signal of policy priority but as a practical commercial factor. It reduced the likelihood of Tesla walking away from the deal, knowing that doing so would also effectively abandon a federally supported infrastructure project.

The Price Collapse That Complicates Everything

A 33% Decline and Its Consequences

Since the Tesla Syrah graphite supply deal was signed in 2021, graphite prices have fallen by approximately one third, from roughly US$6.90 per kilogram to approximately US$4.60 per kilogram. This price trajectory has fundamentally altered the commercial calculus for the Vidalia facility, and it sits at the centre of the evolving battery raw materials market challenge facing non-Chinese producers.

| Metric | 2021 (Contract Signing) | 2026 (Current) |

|---|---|---|

| Graphite Price (approx.) | ~US$6.90/kg | ~US$4.60/kg |

| Price Movement | Baseline | ~-33% |

| Chinese Supplier Competitive Advantage | Moderate | Significantly Elevated |

| Syrah Operating Conditions | Viable | Materially Tightened |

Lower graphite prices benefit Chinese producers disproportionately. Chinese anode manufacturers operate at larger scale, with lower average costs, and with infrastructure investment already largely amortised. For Syrah, which is still in the process of building out Vidalia's production capabilities, the cost base relative to Chinese competitors has widened precisely as the price environment has deteriorated.

The Commercial Tension That Defines the Deal

This price decline creates a fundamental tension that sits at the centre of the Tesla Syrah graphite supply deal. At current market prices, a Chinese anode supplier would almost certainly offer a materially cheaper alternative. Tesla's continued commitment to the Vidalia contract in this price environment is therefore not a commercially neutral decision.

It is an active choice to pay a premium — whether explicit in contractual terms or implicit in the cost of managing a complex multi-year dispute — for a supply chain that operates outside Chinese jurisdiction. That premium represents what might be called the strategic surcharge of supply chain sovereignty.

What Tesla's Four Extensions Actually Reveal

Reading Between the Deadlines

A company that extends a cure deadline once might be showing patience. A company that extends it four consecutive times is revealing something about its underlying priorities. Tesla had multiple commercial off-ramps available throughout the eighteen-month dispute period. Chinese suppliers capable of meeting anode specifications exist. Lower-cost options were available.

Tesla did not take them. This behavioural evidence is arguably more informative about the direction of EV supply chain strategy than any policy statement, because it reflects revealed preference under real commercial pressure rather than aspirational positioning. Indeed, Reuters reported that Syrah bought itself more time on the deal rather than facing an abrupt termination, underscoring how carefully both parties navigated each extension.

The Geopolitical Premium in Practice

What Tesla's decision illuminates is the emergence of a quantifiable but rarely disclosed geopolitical premium in critical mineral procurement. Large original equipment manufacturers are increasingly willing to pay above-market rates, tolerate operational complications, and absorb extended dispute processes to maintain access to supply chains that do not pass through Chinese processing infrastructure.

This premium is not purely altruistic or driven solely by regulatory incentives. It reflects a rational assessment that the risk of supply disruption via Chinese export controls — now demonstrated rather than theoretical following December 2024 — represents a material business risk that justifies a structural cost to mitigate. In addition, understanding this shift is essential for anyone navigating the battery metals investment landscape in the years ahead.

The next major ASX story will hit our subscribers first

Risks That Remain Unresolved

Final Qualification Is Not a Formality

The withdrawal of Tesla's termination notice removes the most immediate commercial threat to the agreement, but it does not mean the deal is complete. Final product qualification at scale represents a technically distinct challenge from demonstrating conforming material in development quantities.

Key remaining risk factors:

- Tesla retains termination rights if final specifications are not met at production volume

- Consistent batch-to-batch reproducibility must be demonstrated across full commercial supply quantities

- Syrah's financial position faces ongoing pressure from low graphite prices that compress operating margins

- The gap between successfully producing conforming material and reliably supplying 8,000 metric tons over four years involves significant operational scaling

"While Tesla's withdrawal of the termination notice removes the most immediate commercial threat, the agreement contains provisions allowing Tesla to exit if final product specifications are not satisfied at scale. Demonstrating conforming material is the first step. Delivering it consistently at volume is the test that actually matters."

Syrah's Financial Position Under Prolonged Price Pressure

The combination of a challenged graphite price environment, capital requirements for scaling Vidalia, and the operational costs associated with a prolonged commercial dispute creates meaningful financial pressure for Syrah Resources. This is worth noting not as a prediction but as a structural variable. The viability of the Vidalia supply chain ultimately depends not just on technical performance but on the financial durability of the company operating it.

Broader Implications for Critical Mineral Strategy

The Vidalia Model as Industrial Blueprint

The Tesla Syrah graphite supply deal, in its totality — including the dispute, the extensions, the federal involvement, and the eventual resolution — provides a more complete template for critical mineral supply chain development than any project that has progressed smoothly. Its difficulties are as instructive as its achievements.

It demonstrates that building processing capability outside China requires:

- Sustained commitment from anchor customers willing to absorb commercial friction

- Federal financial support to de-risk capital-intensive processing infrastructure

- Technical iteration time to bring facilities from initial production to automotive-grade consistency

- Willingness from all parties to prioritise strategic outcomes over short-term procurement economics

December 2024 as an Inflection Point

China's targeted graphite export restrictions represent a shift in the nature of supply chain risk for battery materials. Before December 2024, the dependency on Chinese graphite processing was primarily a theoretical vulnerability discussed in policy papers and industry reports. After December 2024, it became a demonstrated operational reality.

That shift changes the calculus for every battery material in which China holds comparable processing dominance, which extends well beyond graphite to include precursor cathode materials, lithium hydroxide, manganese, and cobalt refining. The Vidalia experience provides both a cautionary illustration of how difficult supply chain diversification actually is and a proof of concept that it can be accomplished under sustained pressure.

Frequently Asked Questions

What is the Tesla Syrah graphite supply deal?

It is a four-year offtake agreement signed in 2021 in which Syrah Resources commits to supply Tesla with 8,000 metric tons of Active Anode Material from its Vidalia facility in Louisiana, using raw graphite from Syrah's Balama mine in Mozambique.

Why did Tesla threaten to terminate the contract?

Tesla issued a formal default notice in July 2025 after receiving non-conforming material samples from the Vidalia facility that did not meet its automotive-grade specifications for battery anode material.

What is Active Anode Material and why does it matter for EV batteries?

AAM is processed graphite that has undergone purification, shaping, and surface treatment to meet the electrochemical requirements of lithium-ion battery anodes. It is the form of graphite that actually functions inside a battery cell, and its production has been almost entirely concentrated within Chinese industrial infrastructure.

Where is the Syrah Vidalia facility and what makes it significant?

The facility is located in Vidalia, Louisiana, and is considered the only large-scale, vertically integrated producer of natural graphite anode material outside China, processing raw graphite from Mozambique into battery-grade AAM on American soil.

What role did the US government play in the dispute?

The US Department of Energy was involved in approving the extensions to Tesla's cure deadlines, and Washington has provided direct financial support to the Vidalia facility as part of its domestic battery supply chain development strategy.

Is the deal now finalised?

Tesla has withdrawn its termination notice following Syrah's demonstration of conforming AAM production, but final product qualification and full commercial approval at scale remain pending as of mid-2026.

What happens next for the Tesla Syrah agreement?

Syrah must demonstrate consistent, large-volume delivery of conforming AAM to complete Tesla's final qualification process. Successfully achieving this at production scale represents the next critical milestone for the Vidalia facility and the broader non-Chinese graphite supply chain it anchors.

A Supply Chain Stress-Tested and Still Standing

The Tesla Syrah graphite supply deal has survived a sequence of challenges that would have ended most commercial agreements: a formal default notice, four consecutive deadline extensions, a 33% commodity price collapse, targeted export controls from a dominant competing supplier, and the ongoing difficulty of scaling a technically complex manufacturing process to automotive-grade consistency.

That it has survived all of these simultaneously — and that Tesla chose to extend rather than exit at each decision point — says something significant about where the EV industry's supply chain priorities have moved. The cheapest option was available throughout. It was not taken.

What remains is the harder work: not surviving a dispute, but delivering a supply chain. Conforming material produced at Vidalia is a meaningful achievement. Conforming material delivered reliably at 8,000 metric tons over four years, with the financial durability to sustain operations through a depressed price environment, is the actual test of whether this supply chain can function as a genuine alternative to Chinese anode manufacturing rather than a strategically significant prototype.

"The Tesla Syrah graphite supply deal is no longer simply a procurement contract. It has become a live case study in the difficulty, cost, and strategic necessity of building battery material supply chains outside China. The fact that it survived a near-terminal dispute, four deadline extensions, a 33% commodity price decline, and direct Chinese export pressure makes its resolution as instructive as any policy paper on critical mineral sovereignty."

The gap between proof-of-concept and proof-of-supply-chain is where the real work of industrial decoupling occurs. Vidalia has cleared the first hurdle. The race is still running.

This article contains forward-looking assessments regarding supply chain development, commercial agreements, and commodity markets. These involve inherent uncertainties and should not be interpreted as financial advice. Past commercial outcomes do not guarantee future performance. Readers should conduct independent research before making investment decisions related to any companies or sectors discussed.

Want to Stay Ahead of the Next Major Battery Minerals Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries — including graphite and other battery-critical commodities — are announced on the ASX, turning complex data into actionable investment insights before the broader market reacts. Explore why major mineral discoveries have historically generated substantial returns, and begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the critical minerals supply chain opportunity.