July 18, 2026

The Refining Chokepoint Nobody Talks About: Inside the IEA Critical Minerals Supply Risk Report for 2026

Every sophisticated economy runs on a hidden layer of industrial inputs that most people never consider until they disappear. Rare earth elements inside a wind turbine generator. Cobalt locked inside an EV battery pack. Gallium etched into semiconductor wafers. These materials flow invisibly through global supply chains until a trade restriction, an armed conflict, or a policy shift forces them into headlines. The IEA critical minerals supply risk report published for 2026 is the most authoritative attempt yet to measure exactly how fragile these flows have become, and its findings mark a departure from earlier editions: supply disruption is no longer a modelled future scenario. It is already happening, and the economic consequences are already being counted.

When big ASX news breaks, our subscribers know first

Why Mineral Security Has Moved From Policy Paper to Production Floor

For years, critical mineral vulnerability was discussed almost exclusively in the language of strategy and national security planning. Governments commissioned reports, academics modelled worst-case scenarios, and industry bodies issued warnings. What the 2026 IEA Global Critical Minerals Outlook confirms is that this period of theoretical concern is now over.

The shift is visible at the factory gate. In 2025, China's rare earth export restrictions on seven heavy rare earth elements forced certain automakers to reduce or temporarily suspend production lines. This was not a simulation. Vehicles were not built. Revenue was not earned. The minerals in question, despite representing a tiny fraction of a finished vehicle's weight, proved irreplaceable in the short term because no alternative supply infrastructure existed at the required scale or purity.

This is the structural reality the IEA report forces into focus. Critical minerals are not like bulk commodities where a shortfall in one region can be offset by drawing on global inventories or switching to a different grade. Many have no practical substitutes at industrial scale. A neodymium-iron-boron permanent magnet cannot simply be replaced by a different magnet architecture without fundamentally redesigning the motor it powers.

Cobalt-bearing cathode chemistries cannot be instantly swapped for cobalt-free alternatives without retooling entire battery production lines.

Structural Insight: The irreplaceability of critical minerals at the point of manufacturing, not at the geological level, is the core vulnerability. Substitutes often exist in theory but require years of process re-engineering to implement at scale.

Refining Dominance: Where the Real Concentration Risk Lives

A common misconception in public discussion of critical mineral risk is that the problem is primarily geological. The assumption is that if Western nations can find and develop their own deposits, supply security follows. The IEA's 2026 data dismantles this view with clarity.

Over the past two years, China and Indonesia together accounted for more than three-quarters of all growth in global refined mineral supply. For manganese, nickel, and graphite specifically, these two countries captured virtually 100% of new supply gains. At the refining stage, China processes between 60% and 90% of lithium, cobalt, and rare earth elements before they enter global manufacturing supply chains.

This means that a Western nation could successfully mine lithium from its own territory and still depend entirely on Chinese processing infrastructure to convert that spodumene concentrate into battery-grade lithium hydroxide. The ore is sovereign. The product is not.

| Mineral | Dominant Refining Nation | Estimated Processing Share | Key Vulnerability |

|---|---|---|---|

| Lithium | China | 60–90% | Refining concentration |

| Cobalt | China (from DRC ore) | ~70% of refined output | Export controls + geopolitics |

| Graphite | China | Supply outside China covers only ~10% of 2030 demand | Near-total dependency |

| Rare Earths | China | Dominant across mining and processing stages | Export restriction risk |

| Nickel | Indonesia (mining) + China (refining) | Indonesia ~40% of mine supply | Dual-country concentration |

| Copper | Geographically distributed | ~10% of production faces water stress | Climate-related disruption |

The pipeline imbalance compounds this problem significantly. Planned rare earth magnet capacity and battery cathode manufacturing currently sit at approximately one-third of the upstream mineral supply expected to be available by 2035. More ore is being produced than the downstream industrial chain can process into finished materials. This is a structural mismatch that expands vulnerability rather than resolving it.

Furthermore, the critical minerals demand surge across energy transition sectors means this mismatch is likely to widen before any meaningful correction occurs.

Export Controls: The Policy Tool That Became a Market Force

Between 2018 and 2024, more than 200 export restrictions on critical minerals were imposed globally. Approximately 40% of those restrictions were concentrated in 2023 alone, signalling an acceleration in the use of mineral access as a geopolitical instrument rather than a conventional trade policy measure.

The price consequences of these controls have been dramatic and in some cases unprecedented. The table below captures the scale of market movement between January 2025 and April 2026:

| Mineral | Price Movement | Primary Driver |

|---|---|---|

| Aluminum | +approximately 33% | Trade disruption, Middle East conflict |

| Copper | +approximately 33% | Demand growth, constrained supply |

| Tin | +approximately 33% | Industrial demand, supply tightness |

| Lithium | More than doubled | Energy storage demand surge |

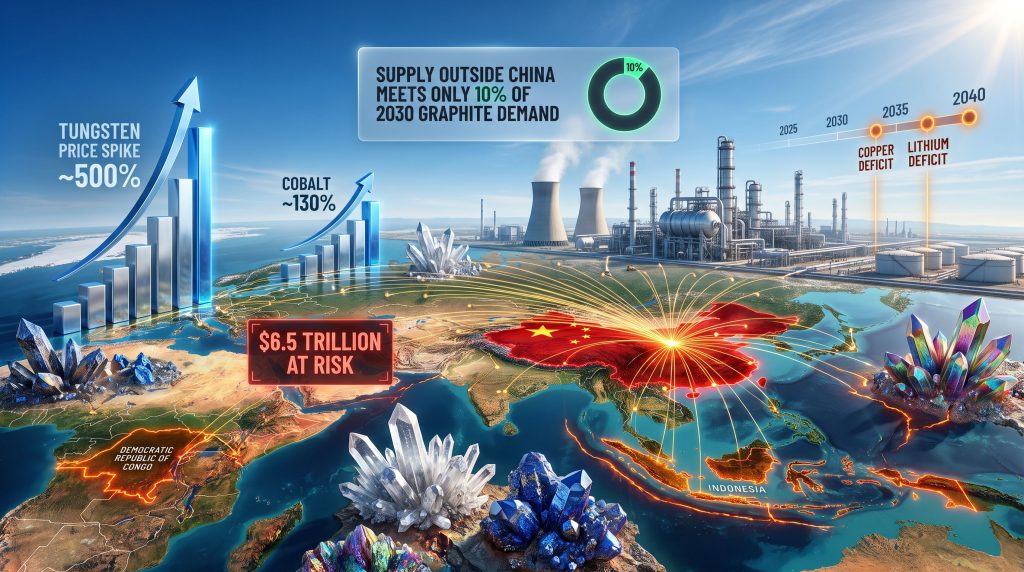

| Cobalt | +approximately 130% | DRC export quota restrictions |

| Tungsten | +approximately 500% (sixfold) | Export controls, tightened availability |

| Gallium (Europe vs. China) | Approximately 5x price differential | Chinese export controls |

| Germanium (Europe vs. China) | Approximately 3x price differential | Chinese export controls |

The gallium and germanium price divergence deserves particular attention because it illustrates a phenomenon that is becoming more common: price bifurcation by geography. When export controls partition a global commodity into domestic and export markets, buyers outside the controlling nation pay a structurally elevated price regardless of underlying supply fundamentals.

European buyers of gallium were not paying a premium because gallium was physically scarce. They were paying it because the trade architecture had been deliberately reshaped.

Critical Warning: The $6.5 trillion figure the IEA attaches to fully implemented export measures represents downstream manufacturing at risk outside China, not direct mineral market value. This distinction matters enormously for understanding the leverage that mineral processing concentration creates.

A complete disruption of battery-grade graphite trade flows alone could threaten more than $300 billion in annual downstream production outside China. Graphite is not a glamorous mineral. It rarely features in mainstream financial media. Yet its role as an anode material in virtually every lithium-ion battery makes it a foundational input for the entire electrification economy.

Investment Withdrawal: The Hidden Crisis Compounding Supply Risk

Even as demand projections for critical minerals have strengthened, private investment in the sector contracted sharply in 2025. Overall critical mineral investment fell by 9%, ending a multi-year growth trend. Exploration spending declined by more than 10%. Battery metal companies reduced capital expenditure by more than 20%, with lithium producers cutting spending by approximately 40%.

Understanding why requires recognising that mining investment decisions operate on very different timescales to commodity price cycles. A mine takes between 10 and 20 years from initial discovery through permitting, feasibility study, construction, and first production. An investor committing capital today is essentially making a bet on market conditions in the mid-2030s, filtered through geopolitical scenarios that nobody can reliably forecast.

Five structural deterrents are driving the pullback:

- Price volatility creates uncertainty around the revenue assumptions underpinning project economics, particularly for lithium and nickel where rapid price swings have eroded confidence.

- Geopolitical exposure makes long-term capital allocation difficult when export control regimes can shift abruptly and without warning.

- Policy uncertainty across multiple jurisdictions delays final investment decisions as regulatory timelines shift with changing government priorities.

- Battery chemistry evolution introduces demand uncertainty. As cathode formulations continue evolving, for example toward higher-nickel and lower-cobalt chemistries, the long-term demand forecasts for specific minerals become less predictable.

- Oversupply in select markets has suppressed prices in lithium and nickel, reducing the returns available to new entrants and making project financing harder to secure.

The IEA estimates that approximately $800 billion in cumulative mining investment is required between now and 2040 to support a 1.5 degree Celsius climate pathway. The current trajectory falls well short of that figure.

Government financing is attempting to fill the gap. Public commitments across advanced economies reached approximately $65 billion in 2025, representing more than four times the 2023 commitment level. However, the IEA flags a critical distinction: a substantial portion of these commitments remain announced rather than actively deployed. Announced capital and deployed capital are very different things for a project developer trying to finalise construction finance.

The Supply-Demand Trajectory Through 2035: Where the Deficits Are Building

Robust production growth kept most key energy mineral markets in surplus during 2025. This fact is sometimes misread as evidence that supply risk is overstated. The IEA's analysis is more nuanced: the concern is not primarily about whether enough mineral exists in the ground or even whether enough is currently being produced. It is about whether concentrated and geopolitically exposed supply chains can reliably deliver that material to the industries that need it.

With that framing in mind, the projected deficit picture through 2035 looks as follows:

- Copper: Faces a projected supply deficit through 2035, with the gap narrowing as new projects advance but not closing entirely. Approximately 10% of global copper production also faces climate-related water stress, adding a physical disruption dimension that sits outside normal market analysis.

- Lithium: Also faces a projected deficit through 2035 despite new production coming online. Advances in direct lithium extraction technology offer some promise for accelerating output, however the deficit narrowing remains gradual and demand from energy storage applications is expected to push requirements significantly higher.

- Cobalt: The Democratic Republic of the Congo's export quota has introduced a supply constraint that is entirely policy-driven rather than resource-limited. The DRC holds the world's largest cobalt reserves. The deficit emerging by 2035 exists not because the ore has run out but because access to it has been administratively restricted.

- Graphite: Perhaps the most exposed mineral in the entire critical minerals landscape. Supply outside China is currently projected to meet only approximately 10% of 2030 demand. No other major industrial mineral has this level of near-total external dependency.

The lone encouraging signal in the IEA's 2026 findings involves rare earths. New production projects in the United States, combined with expanded output from Malaysian processing facilities, have modestly reduced China's share of refined rare earth output. The IEA identifies this as the only meaningful diversification progress across major critical mineral categories in the current edition.

The next major ASX story will hit our subscribers first

Short-Term Buffers and Long-Term Structural Solutions

Strategic Stockpiling: Undervalued Insurance

The cost of maintaining strategic reserves covering 11 high-risk materials is estimated by the IEA at less than $900 million annually for nations outside the dominant supplier countries. Measured against the trillions in downstream manufacturing value that those materials support, this represents an extraordinarily cost-effective insurance mechanism.

Strategic stockpiles are not a substitute for supply chain diversification. They are a time-buying mechanism: a buffer that allows governments and industries to respond to disruptions without immediate production losses while longer-term structural solutions are developed. The IEA's framing of stockpiles as a near-term tool reflects a realistic assessment that refining and manufacturing capacity cannot be built overnight regardless of how much capital is committed.

Recycling: Meaningful Contribution, Not a Complete Solution

Recycled mineral supply could nearly double its contribution to key mineral markets by 2040 under the IEA's projections. This is a significant potential offset, particularly for cobalt and rare earths where end-of-life recovery rates from consumer electronics and EV batteries are still relatively low. In addition, a recent battery recycling breakthrough has demonstrated that higher material recovery rates are technically achievable at industrial scale.

Realising this potential requires investment that goes well beyond collection bins. Hydrometallurgical processing facilities capable of recovering battery-grade lithium hydroxide from spent cells, separation plants for rare earth elements from decommissioned permanent magnets, and the technical workforce to operate them all represent substantial capital commitments that are currently undersupported relative to their strategic importance.

The Industrial Chain Imperative

Every pathway to genuine supply security that the IEA identifies runs through the same bottleneck: refining and downstream manufacturing capacity outside the currently dominant processing nations. Mining investment, however welcome, cannot resolve supply vulnerability if the ore it produces must travel to China or Indonesia for processing before it re-enters global supply chains.

The IEA's central structural recommendation is that governments and industry must direct resources toward the full industrial value chain. Consequently, the critical raw materials transition agenda must extend from refineries and chemical processing plants through to cathode active material production, magnet manufacturing, and the technical skills infrastructure needed to operate these facilities at scale. Technology transfer, equipment manufacturing localisation, and workforce development are identified as equally critical to mineral security as geological resource development.

The IEA's critical minerals policy tracker provides a useful framework for evaluating how individual nations are progressing against these structural benchmarks.

Long-Term Framework: The three-layer response the IEA outlines operates on sequential timescales: stockpiling provides near-term disruption buffering, government financing deployment builds medium-term refining capacity, and recycling infrastructure combined with genuine diversification achieves long-term structural resilience.

Frequently Asked Questions

What does the IEA Global Critical Minerals Outlook assess?

The IEA publishes this outlook annually to evaluate the market, investment, policy, and technology forces shaping mineral supply security. The 2026 edition reviews conditions through 2025 and early 2026, with supply and demand projections extending to 2040 across a broad mineral universe including aluminum, copper, nickel, manganese, uranium, cobalt, graphite, lithium, rare earths, and strategic minor minerals.

Which mineral currently carries the highest supply risk?

Graphite presents perhaps the most extreme exposure given that supply sources outside China are projected to cover only around 10% of 2030 demand. Lithium carries high overall risk due to refining concentration. Cobalt faces a policy-created deficit from DRC export restrictions. Rare earth heavy elements face severe regional price bifurcation due to export controls.

Why did investment fall in 2025 despite rising demand projections?

A combination of price volatility, geopolitical uncertainty, evolving battery chemistry forecasts, policy instability across multiple jurisdictions, and oversupply-driven price depression in lithium and nickel markets collectively eroded investor confidence. Mining capital allocation requires long time horizons, making it particularly sensitive to uncertainty rather than current price levels alone.

Is government financing enough to replace private capital?

The IEA's assessment is cautious. While public commitments reached approximately $65 billion in 2025, much of this remains announced rather than deployed. Government financing fills important gaps but cannot substitute for the full scale of private capital needed to meet the IEA's estimated $800 billion cumulative investment requirement through 2040. The IEA critical minerals supply risk report is explicit that public and private capital must work in tandem rather than sequentially.

What makes the 2026 report different from previous editions?

The qualitative shift in the 2026 findings is that disruption has moved from modelled risk to documented reality. Automakers have already lost production to rare earth export controls. Price differentials between markets have already widened to multiples of domestic levels. Investment has already contracted. The IEA critical minerals supply risk report is, consequently, no longer primarily predictive. It is now also diagnostic.

Readers seeking ongoing coverage of critical mineral market dynamics, technology metals, and supply chain policy developments can explore reporting from Metal Tech News at metaltechnews.com.

This article contains forward-looking projections drawn from IEA analysis. Mineral market conditions, investment flows, and geopolitical dynamics are subject to rapid change. Nothing in this article constitutes financial or investment advice.

Want to Know When the Next Major Mineral Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across critical commodities — including the lithium, cobalt, graphite, and rare earth sectors central to the supply chain vulnerabilities outlined above — and delivering actionable alerts directly to subscribers ahead of the broader market. Explore historic discoveries and their exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.