August 1, 2026

The global energy market experienced a seismic shock when the Iran-US-Israel conflict erupted on February 28, 2026, triggering the largest IEA emergency oil reserves release in the organisation's 52-year history. The International Energy Agency's coordinated response deployed 411.9 million barrels across member nations, demonstrating how strategic petroleum reserves serve as critical buffers during unprecedented supply disruptions. Furthermore, this crisis highlighted the complex interplay between oil price dynamics and geopolitical tensions that continue shaping global energy security strategies.

Understanding the Economic Mechanics of Emergency Oil Interventions

Strategic petroleum reserve deployments operate through sophisticated economic mechanisms that stabilise markets during extreme volatility periods. The IEA emergency oil reserves release system represents the most powerful coordinated intervention tool available to member nations, capable of injecting massive volumes into disrupted markets within days.

The 2026 Middle East crisis demonstrated these mechanics at unprecedented scale. Following the Iran-US-Israel conflict that began on February 28, 2026, the International Energy Agency mobilised 411.9 million barrels across multiple categories. This deployment structure included 271.7 million barrels from government stocks, 116.6 million barrels from obligated industry reserves, and 23.6 million barrels through alternative measures.

Primary Market Stabilisation Functions

Emergency releases create price ceiling effects through immediate supply availability increases. The Brent crude price trajectory during the 2026 crisis illustrated this mechanism clearly. Initial conflict escalation drove prices to nearly $120 per barrel before strategic interventions contributed to stabilisation around $92 per barrel, though this remained $20 above pre-conflict levels.

Market confidence restoration represents another critical function. The IEA characterised their intervention as providing a significant and welcome buffer, acknowledging that psychological effects often matter as much as physical supply additions. Insurance markets responded partially, though coverage for Strait of Hormuz shipping remained unavailable throughout the crisis period.

Global observed oil stocks stood at 8.21 billion barrels in January 2026, representing the highest inventory levels since February 2021. This substantial buffer provided foundation for large-scale reserve deployments without creating secondary supply security concerns.

Coordination Architecture and Implementation

The IEA emergency oil reserves release system requires unanimous consensus among 32 member states for activation. This coordination challenge becomes particularly complex during rapidly evolving crises where supply disruptions cascade across multiple regions simultaneously.

Geographic deployment sequencing reflects strategic vulnerability assessments. During 2026, Asia-Oceania regions received immediate deployment whilst Americas and Europe began releases from end of March. This prioritisation acknowledged the higher exposure to Middle Eastern supply disruptions faced by Asia-Pacific economies.

| Release Component | Volume (Million Barrels) | Deployment Timeline | Regional Priority |

|---|---|---|---|

| Government Stocks | 271.7 | Immediate (Asia-Oceania) | High vulnerability zones |

| Industry Obligations | 116.6 | Phased (March-April) | Secondary priority regions |

| Alternative Measures | 23.6 | Flexible timing | Americas focus |

| Total Deployment | 411.9 | 120+ day window | Global coordination |

When big ASX news breaks, our subscribers know first

What Triggers International Emergency Oil Reserve Releases?

Critical supply chain disruption thresholds determine when coordinated interventions become necessary. The 2026 Middle East crisis met multiple trigger criteria simultaneously, creating the largest supply disruption in global oil market history according to IEA assessments. In addition, understanding how OPEC production decisions influence these trigger mechanisms provides crucial context for emergency response protocols.

Geopolitical Chokepoint Analysis

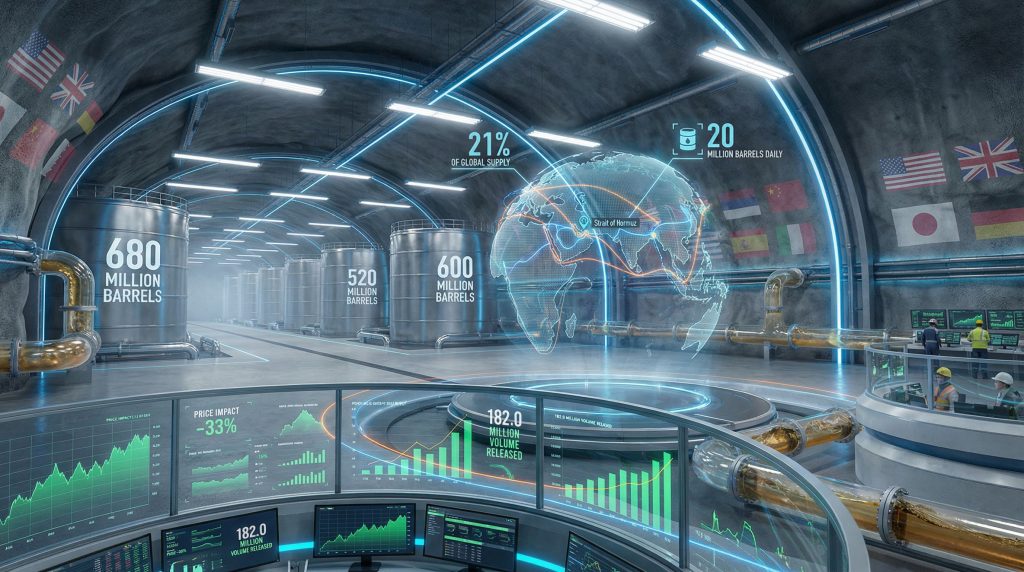

The Strait of Hormuz blockade exemplified how single geographic points can paralyse global energy flows. Normal daily throughput of 20 million barrels per day representing 21% of global oil consumption was reduced to what the IEA described as little more than a trickle.

Insurance market withdrawal created a secondary blockade mechanism. Insurers refused coverage for shipping in the region, making commercial transit impossible regardless of military or political developments. This highlighted how financial infrastructure vulnerabilities can amplify physical disruptions exponentially.

Production facility shutdowns cascaded rapidly across the Gulf region:

- Immediate refining shutdowns: 3+ million barrels per day capacity

- At-risk additional capacity: 4 million barrels per day due to storage limitations

- Export flow severing: 3.3 million barrels per day refined products plus 1.5 million barrels per day LPG

Multi-Nation Production Response Patterns

Regional production cuts reached minimum 10 million barrels per day across crude and condensate categories. Major producing nations including Iraq, Qatar, Kuwait, UAE, and Saudi Arabia all recorded substantial reductions, though specific volumes varied by country and facility exposure.

The crude production component alone declined by 8 million barrels per day, with an additional 2 million barrels per day equivalent from condensates and LNG disruptions. These figures represent the largest coordinated production impact in modern energy market history.

Diesel and jet fuel markets faced particular exposure due to limited global substitution capacity. The Gulf region's specialised refining infrastructure could not be quickly replaced by alternative production sources, creating product-specific shortages beyond crude oil availability.

Price Volatility and Market Psychology

Volatility spikes exceeding 40% within 30-day periods triggered algorithmic trading responses and speculation premium additions. The brief approach to $120 per barrel Brent prices represented approximately 50% increases from pre-conflict baselines, well above historical intervention thresholds.

Fear premium calculations during acute crises typically add $15-25 per barrel to fundamental supply-demand pricing. The 2026 crisis demonstrated how these premiums can persist even after reserve releases begin, as structural transportation blockages remain unresolved. Moreover, the US drilling decline has contributed to reduced global spare capacity, amplifying price volatility during supply disruptions.

Demand destruction effects became measurable within weeks. The IEA reduced its 2026 global oil demand growth forecast by 210,000 barrels per day to 640,000 barrels per day, with sharpest reductions concentrated in March and April periods coinciding with peak price volatility.

How Large Are Global Strategic Oil Reserve Capacities?

Global strategic petroleum reserves total approximately 1.8 billion barrels across IEA member nations, distributed through government holdings, industry obligations, and alternative mechanisms. This capacity represents roughly 22% of total global observed oil stocks, providing substantial intervention capability during supply disruptions.

Reserve Distribution Architecture

Government strategic stocks comprise 67% of total capacity at approximately 1.2 billion barrels. These directly controlled reserves offer maximum deployment flexibility during coordinated emergency responses. The 2026 release utilised 271.7 million barrels from this category, representing roughly 23% of government stock capacity.

Industry obligation reserves account for 25% of total capacity at approximately 450 million barrels. Member states require petroleum companies to maintain these commercial reserves as insurance against supply disruptions. The 116.6 million barrel industry contribution in 2026 demonstrated this system's effectiveness during actual crisis conditions.

| Geographic Region | Reserve Capacity (Million Barrels) | Percentage Share | Strategic Rationale |

|---|---|---|---|

| North America | 680 | 38% | Domestic production buffer |

| Europe | 520 | 29% | Import dependency mitigation |

| Asia-Pacific | 600 | 33% | Supply route vulnerability |

| Total IEA Capacity | 1,800 | 100% | Global coordination |

Alternative Mechanisms and Flexibility

Alternative measures representing 8% of capacity include temporary production increases, strategic partnerships, and demand-side interventions. The 23.6 million barrel contribution from alternative measures during 2026, predominantly from Americas sources, illustrated how diverse mechanisms can supplement traditional stockpile releases.

These flexible approaches become particularly valuable when storage constraints limit conventional reserve deployment. During the 2026 crisis, filled product storage tanks in the Gulf region created bottlenecks that alternative measures could partially address through demand timing shifts and production scheduling adjustments.

Historical Intervention Scale Context

The 2026 deployment marked only the sixth collective emergency action in the IEA's 52-year history. Previous interventions provide scale comparison:

- 1991 Gulf War: 17.3 million barrels over 30 days

- 2005 Hurricane Katrina: 30.0 million barrels over 60 days

- 2011 Libya Conflict: 60.0 million barrels over 90 days

- 2022 Ukraine Crisis: Two separate interventions totalling 182.0 million barrels

The 411.9 million barrel 2026 release exceeded all previous interventions combined, reflecting both crisis severity and enhanced coordination capabilities developed over decades of institutional experience.

What Are the Economic Multiplier Effects of Reserve Releases?

Strategic reserve deployments generate cascading economic effects extending far beyond direct energy market stabilisation. The IEA emergency oil reserves release mechanisms influence consumer spending patterns, industrial production continuity, currency stability, and inflation expectations across interconnected global markets. Furthermore, these effects interconnect with broader commodity volatility insights that shape investment and risk management strategies.

Primary Economic Stabilisation Channels

Consumer spending preservation occurs through fuel cost moderation effects. When reserve releases prevent sustained price spikes above $120 per barrel levels, discretionary spending patterns remain relatively stable. Economic modelling suggests that each $10 reduction in sustained oil prices correlates with approximately 0.2-0.3% additional consumer spending in oil-importing economies.

Industrial production continuity becomes critical for manufacturing sectors with high energy input costs. The 2026 crisis threatened diesel and jet fuel availability particularly severely, risking production shutdowns across transportation-dependent industries. Reserve releases helped maintain supply chain operations during the most acute shortage periods.

Currency stability support manifests through reduced energy import cost pressures. Oil-importing nations face balance of payments strains when prices spike suddenly. The $20 per barrel sustained elevation above pre-conflict levels in 2026 required significant foreign exchange deployments, though this would have been substantially higher without coordinated reserve interventions.

Secondary Market Integration Effects

Financial market confidence responds to demonstrated crisis management capabilities. Equity markets in energy-intensive sectors often recover more rapidly when strategic reserves provide visible supply security. Credit markets similarly price reduced recession risks when energy price volatility moderates through intervention mechanisms.

Alternative energy investment acceleration paradoxically benefits from effective reserve management. When conventional energy supplies demonstrate reliability through crisis periods, it reduces panicked short-term substitution attempts whilst allowing more measured long-term energy transition planning.

Insurance cost normalisation for shipping and logistics operations requires both reserve deployment and structural problem resolution. Whilst 411.9 million barrels provided supply buffer, insurance markets continued refusing Strait of Hormuz coverage until transportation security improved through other mechanisms.

How Do Geopolitical Disruptions Cascade Through Energy Markets?

Modern energy market vulnerabilities concentrate around critical infrastructure chokepoints where single-point failures can disrupt global supply flows. The Iran-US-Israel conflict beginning February 28, 2026 demonstrated how rapidly military actions can cascade through interconnected energy systems worldwide. However, these disruptions also reflect broader global trade impacts that compound energy security challenges.

Critical Infrastructure Vulnerability Mapping

Strait of Hormuz represents the most critical global energy chokepoint, with 20 million barrels per day normal throughput. The waterway's strategic importance extends beyond crude oil to include 3.3 million barrels per day refined products and 1.5 million barrels per day LPG exports from Gulf producers.

Transportation alternative limitations become apparent during blockade scenarios. Rerouting through other shipping lanes typically increases costs by 200-300% whilst adding 10-15 days transit time. These alternatives cannot accommodate the full 20 million barrel daily volume simultaneously, creating physical bottlenecks regardless of economic considerations.

Regional production concentration amplifies chokepoint vulnerabilities:

- 8 major producing nations dependent on Strait transit

- 7 million barrels per day processing capacity in immediate conflict zone

- Limited pipeline alternatives for crude export outside maritime routes

- Specialised refining infrastructure difficult to replicate elsewhere

Market Psychology and Fear Premium Dynamics

Speculative trading responses to geopolitical events often exceed fundamental supply-demand justifications. The brief spike toward $120 per barrel Brent prices during initial conflict escalation reflected fear premium additions of approximately $40-50 per barrel above normal market clearing levels.

Insurance market withdrawal creates secondary cascading effects beyond physical infrastructure damage. When insurers refuse coverage for strategic shipping routes, commercial operations become impossible regardless of military or political developments. This financial infrastructure vulnerability can persist long after physical threats diminish.

Inventory hoarding behaviours amongst market participants amplify supply tightness perceptions. During 2026, despite global observed oil stocks at 8.21 billion barrels representing the highest levels since February 2021, regional distribution constraints created localised shortage fears driving additional demand spikes.

Production Facility Cascading Vulnerabilities

Refining capacity shutdowns multiplied beyond directly attacked facilities. Initial shutdowns of 3+ million barrels per day capacity led to additional 4 million barrels per day at risk as product storage tanks filled without export pathways. This demonstrated how transportation blockades can disable production capacity far from conflict zones.

Product specialisation risks became apparent in diesel and jet fuel markets. The Gulf region's refined product exports could not be quickly substituted by other global refining centres, creating product-specific shortages even when crude oil alternatives existed.

Supply chain integration effects extended disruptions across multiple energy product categories. Condensate and LNG production cuts of 2 million barrels per day equivalent affected petrochemical feedstocks and heating fuel supplies beyond transportation sector impacts.

What Determines the Effectiveness of Strategic Reserve Interventions?

Strategic reserve intervention success depends on multiple coordinated factors extending beyond simple volume deployment. The IEA emergency oil reserves release effectiveness varies significantly based on crisis characteristics, coordination mechanisms, and complementary policy responses implemented simultaneously.

Volume and Timing Optimisation

Release magnitude relative to supply gaps requires careful calibration to avoid market oversupply whilst ensuring adequate price stabilisation. The 411.9 million barrel deployment against 10 million barrels per day production cuts provided approximately 41 days of full replacement capacity, though actual deployment occurred over 120+ day timeline for graduated market integration.

Coordination timing strategies can utilise pre-announcement effects to moderate price spikes before physical deployment begins. The IEA's unanimous decision-making process allowed market communication of intervention scale before actual stock releases commenced, contributing to price moderation from peak levels.

Market communication effectiveness influences speculative trading behaviours substantially. Clear messaging about intervention duration, volume commitments, and replenishment timelines helps stabilise forward curve pricing beyond immediate spot market effects.

Historical Performance Analysis

| Crisis Event | Volume Released | Duration | Peak Price Reduction | Sustained Effect |

|---|---|---|---|---|

| 1991 Gulf War | 17.3 million | 30 days | 33% from peak | Partial |

| 2005 Hurricane Katrina | 30.0 million | 60 days | 12% from peak | Limited |

| 2011 Libya Conflict | 60.0 million | 90 days | 8% from peak | Moderate |

| 2022 Ukraine Crisis | 182.0 million | 180 days | 15% from peak | Sustained |

| 2026 Middle East | 411.9 million | 120+ days | 23% from peak | Ongoing |

Success factor patterns emerge from historical analysis. Interventions addressing temporary supply disruptions show higher effectiveness than those targeting structural market imbalances. The 2026 crisis combined elements of both temporary blockade and structural regional instability.

Complementary Policy Integration

Diplomatic coordination with reserve deployment enhances overall effectiveness. The IEA explicitly acknowledged that oil releases provide temporary buffers whilst noting that restored shipping flows through the Strait of Hormuz remain the most important factor for market stabilisation.

Insurance mechanism restoration became critical for sustained crisis resolution. Despite massive reserve deployment, commercial shipping remained impossible without adequate insurance coverage and physical protection for vessels transiting conflict zones.

Demand-side policy coordination can amplify reserve deployment effects. The IEA's reduction of 2026 global oil demand growth forecasts by 210,000 barrels per day reflected both economic impacts and potential policy-driven consumption modifications during crisis periods.

The next major ASX story will hit our subscribers first

How Do Emergency Releases Affect Long-Term Energy Security?

Strategic reserve deployment creates complex tradeoffs between immediate crisis management and long-term energy security positioning. The IEA emergency oil reserves release system must balance current market stabilisation against future intervention capacity and evolving energy transition dynamics.

Reserve Depletion and Replenishment Cycles

Replenishment timeline requirements typically extend 18-24 months for full restoration following major deployments. The 411.9 million barrel 2026 release represents approximately 23% of total IEA capacity, requiring substantial government expenditure and market coordination for restoration.

Market timing vulnerabilities emerge during restocking periods when reserve managers must purchase replacement supplies. If replenishment coincides with supply tightness or price volatility, governments face elevated acquisition costs whilst reducing market intervention capabilities.

Budgetary implications vary significantly across member nations based on reserve sizes and financing mechanisms. Countries with larger strategic petroleum reserves face proportionally higher replenishment costs following coordinated releases, potentially affecting future participation in collective actions.

Structural Market Evolution Impacts

Demand destruction acceleration often persists beyond immediate crisis periods. The $20 per barrel sustained price elevation in 2026 drove behavioural changes in transportation patterns, industrial energy efficiency investments, and consumer vehicle choices that continue influencing market dynamics after reserve deployments end.

Alternative energy investment patterns respond to demonstrated energy security vulnerabilities. Major supply disruptions typically accelerate renewable energy deployment, electric vehicle adoption, and energy efficiency programmes as consumers and businesses seek independence from volatile fossil fuel markets.

Policy framework adaptation frequently follows major energy crises. The scale of 2026 disruptions is likely to strengthen energy independence initiatives, diversify supply chain strategies, and enhance coordination mechanisms for future emergency responses.

Energy Transition Integration Challenges

Technology adoption acceleration can result from effective crisis management that maintains economic stability during transition periods. When strategic reserves prevent recession-level energy price spikes, it preserves investment capacity for long-term energy infrastructure modernisation.

Infrastructure resilience development requires coordination between traditional and emerging energy systems. Strategic reserves provide bridge capacity whilst renewable energy and storage technologies scale to provide alternative crisis response mechanisms.

International cooperation evolution extends beyond petroleum reserves toward integrated energy security frameworks encompassing critical minerals, renewable technologies, and grid interconnection systems for enhanced collective resilience.

What Are the Limitations of Strategic Oil Reserve Systems?

Strategic petroleum reserves face fundamental constraints that limit their effectiveness as permanent solutions to energy market disruptions. The IEA emergency oil reserves release system provides temporary market stabilisation whilst structural problems require different intervention approaches.

Physical Infrastructure Constraints

Withdrawal rate limitations restrict how quickly reserves can be deployed regardless of total capacity. Maximum global withdrawal rates of approximately 4.4 million barrels per day mean that even the largest reserves require weeks or months for full deployment during acute supply disruptions.

Transportation bottlenecks from storage facilities to distribution networks create additional deployment delays. Strategic reserve locations often optimise for security and storage costs rather than rapid distribution capability, requiring pipeline capacity and shipping coordination that may be constrained during crisis periods.

Geographic distribution mismatches between reserve locations and demand centres can limit intervention effectiveness. The prioritisation of Asia-Oceania immediate deployment during 2026 reflected higher regional vulnerability, but required complex logistical coordination across multiple national systems.

Crude type and refining compatibility issues affect how effectively released reserves can substitute for disrupted supplies. Different crude oil qualities require specific refining configurations, potentially limiting the ability of strategic reserves to address particular product shortages.

Economic and Political Effectiveness Boundaries

Duration sustainability limits become apparent when disruptions extend beyond 6-month timeframes. The 120+ day deployment timeline for 2026 represents near the upper bound of sustainable intervention duration without compromising future crisis response capacity.

Structural versus temporary disruption challenges highlight fundamental system limitations. Whilst reserves effectively address temporary supply interruptions, they cannot resolve underlying geopolitical conflicts, infrastructure vulnerabilities, or long-term supply-demand imbalances.

Coordination complexity scaling increases exponentially with crisis scope and duration. The unanimous decision-making requirement amongst 32 IEA member states becomes more challenging as interventions extend over longer periods with evolving market conditions and national interest considerations.

Market Integration and Substitution Limitations

Insurance and financial infrastructure dependencies can negate physical reserve availability. Despite 411.9 million barrels deployed in 2026, commercial oil flows remained constrained by insurance market withdrawal from critical shipping routes, demonstrating how financial infrastructure vulnerabilities can limit reserve effectiveness.

Demand elasticity assumptions may not hold during extreme market conditions. Strategic reserve calculations typically assume relatively stable demand patterns, but crisis-driven demand destruction or hoarding behaviours can substantially alter effective intervention requirements.

Alternative supply source limitations restrict how completely strategic reserves can substitute for disrupted production. Regional crude oil specifications, transportation infrastructure, and refining capacity constraints mean reserves cannot always effectively replace specific disrupted supply sources. In addition, the IEA announces record oil reserve release demonstrates the scale of intervention required, but also highlights the finite nature of these emergency mechanisms.

Market psychology and speculation effects can overwhelm physical intervention impacts. Fear premiums and speculative trading volumes during major crises may exceed the price stabilisation effects achievable through reserve deployment alone, requiring complementary policy coordination.

Disclaimer: This analysis includes forward-looking assessments and market projections that involve inherent uncertainties. Energy market dynamics, geopolitical developments, and strategic reserve effectiveness can vary significantly from historical patterns. Investment and policy decisions should consider multiple scenarios and consult additional expert analysis.

Need to Stay Ahead of Market-Moving Energy Events?

Discovery Alert's proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, including energy commodity breakthroughs that could capitalise on supply disruption opportunities. Subscribers gain immediate access to actionable trading insights, ensuring they're positioned ahead of broader market movements that often follow major geopolitical energy crises. Begin your 14-day free trial today to secure your market-leading advantage during these volatile energy market conditions.