June 12, 2026

When Supply Buffers Run Dry: Decoding the IEA Warning on Global Oil Inventories and Summer Supply Shortage

Energy markets have a long history of oscillating between excess and scarcity, but the structural conditions defining mid-2026 are genuinely without modern precedent. A geopolitical shock of historic proportions has collided with the seasonal calendar at precisely the worst moment, stripping away the inventory cushions that markets rely on during periods of disruption. The IEA warning on global oil inventories and summer supply shortage is not simply a cautionary note from an intergovernmental body. It reflects a deteriorating physical reality that is already being priced into benchmark crude contracts and reverberating across equity markets from Mexico City to Singapore.

Understanding what is actually happening requires separating two distinct market dynamics that are unfolding simultaneously and pointing in opposite directions. Furthermore, the intersection of oil trade and geopolitics in 2026 has made traditional analytical frameworks considerably harder to apply.

When big ASX news breaks, our subscribers know first

The Structural Paradox Defining Oil Markets in 2026

Near-Term Tightness Versus Medium-Term Oversupply

Rarely does the same commodity market face credible warnings of both imminent shortage and eventual surplus within the same twelve-month window. Yet that is precisely the situation confronting global oil markets today. In the near term, shrinking inventories and rising summer consumption are converging to create genuine supply stress. Over a longer horizon, projections from both the IEA and the U.S. Energy Information Administration suggest that global supply growth could substantially outpace demand growth by late 2026, potentially generating inventory builds of close to 3 million barrels per day if current production trajectories continue.

This bifurcation matters enormously for how market participants interpret price signals. A trader focused on the next 60 days sees a market that looks tight, with Brent crude above US$100 per barrel and inventories at critical pricing hubs falling below historical seasonal averages. A strategist with a 12-month view sees a market that could be oversupplied by the fourth quarter. Both readings can be correct simultaneously, which is part of what makes current conditions so analytically complex.

What Inventory Depletion Actually Means at the Point of Delivery

It is worth distinguishing between two types of inventory data that often get conflated in market commentary. Reported aggregate inventory reflects total global stockpiles including strategic reserves, pipeline fill, and floating storage. Observable inventory at pricing hubs, such as Cushing, Oklahoma for WTI or ARA (Amsterdam-Rotterdam-Antwerp) for European crude grades, reflects the barrels that are actually available for near-term commercial delivery.

When observable stocks at these hubs fall below their five-year seasonal averages, physical buyers face genuine competition for available supply. This dynamic creates what traders call backwardation, where near-month contracts trade at a premium to forward contracts. Backwardation is itself a signal that the physical market is experiencing real tightness regardless of what aggregate inventory statistics might suggest. The practical consequence is that refiners who cannot secure adequate forward coverage face margin compression and potential throughput reductions, which ultimately feeds through to product prices at the pump.

According to the IEA's oil market report, global oil markets can simultaneously register a medium-term surplus on paper while experiencing real-world tightness at critical distribution nodes. This dynamic confuses price signals, complicates policy responses, and creates mismatches between what financial models project and what physical operators actually experience.

The Strait of Hormuz Disruption: Scale, Timeline, and Market Consequences

How the Largest Supply Shock in IEA History Unfolded

On February 28, 2026, U.S. and Israeli-led military operations against Iran triggered the effective closure of Strait of Hormuz shipping lanes to commercial crude tanker traffic. The Strait of Hormuz is the world's most critical oil transit chokepoint, through which approximately 20% of global seaborne crude oil and liquefied natural gas passes on any given day. Its sudden inaccessibility to commercial traffic represented an immediate and severe disruption to global supply chains.

The IEA subsequently classified the event as the largest supply disruption in the organisation's recorded history, with lost production volumes exceeding 1 million barrels per day. To place that figure in context, even partial disruptions of this chokepoint have historically triggered significant price responses. The scale of the current event is categorically different from anything the IEA's emergency response mechanisms were originally designed to address.

The global market entered the crisis with a surplus inventory position that initially absorbed some of the shock. However, IEA Executive Director Fatih Birol has made clear that this buffer has now been substantially consumed, with the agency issuing the IEA warning on global oil inventories and summer supply shortage to signal that markets could face severe pressure by July or August 2026 if Middle Eastern oil flows do not resume.

The Emergency Reserve Response: Parsing the 400 Million Barrel Deployment

On March 20, 2026, the IEA coordinated the largest emergency strategic petroleum reserve release in its 50-year operational history, deploying 400 million barrels from member nations' collective stockpiles. To contextualise this intervention, the table below compares it against every previous major IEA emergency release on record.

| Release Event | Year | Volume Released | Market Context |

|---|---|---|---|

| Gulf War I Response | 1991 | ~33.75 MMb | Iraqi invasion of Kuwait |

| Hurricane Katrina Response | 2005 | ~30 MMb | U.S. Gulf Coast production loss |

| Libya Disruption Response | 2011 | 60 MMb | Libyan civil war supply halt |

| COVID Recovery Coordination | 2021 | 60 MMb | Post-pandemic demand surge |

| Strait of Hormuz Crisis | 2026 | 400 MMb | Largest in IEA history |

The sheer magnitude of the March 2026 deployment relative to all prior interventions illustrates the scale of the crisis. Every previous emergency release addressed disruptions measured in the tens of millions of barrels over defined geographic areas. The current intervention dwarfs the cumulative volume of the four preceding releases combined.

Birol has confirmed that the IEA retains the capacity and institutional readiness to coordinate additional reserve drawdowns if conditions deteriorate further. However, strategic petroleum reserves are a finite resource. A second release of comparable scale would push member nation reserves to levels not seen since the SPR programmes were established, raising serious questions about residual emergency buffer capacity.

Emergency petroleum reserve drawdowns are a finite tool. With the March 2026 deployment already representing the largest in IEA history at 400 million barrels, the capacity for a second intervention of comparable scale is materially constrained. Markets should not assume unlimited buffer availability.

Why Infrastructure Damage Extends the Recovery Timeline

One of the least-discussed but most consequential dimensions of the current disruption is the damage sustained by Middle Eastern oil production and refining infrastructure during military operations. Lydia Rainforth, Head of European Equity Strategy at Barclays, has noted that the scale of the outage means market normalisation will require considerable time even in a scenario where maritime transit through the Strait resumes immediately.

This is a critical nuance. Market commentary often frames the Hormuz disruption as though it were a gate that could simply be reopened when hostilities cease. The physical reality is more complex. Upstream wellheads, gathering systems, processing facilities, and export terminals that have sustained damage require months to years of repair and recommissioning work before they can return to pre-conflict production capacity.

The July-August Risk Window: Summer Demand Meets Depleted Buffers

Seasonal Demand Amplification and the Compounding Effect

The IEA's specific concern about the July-August 2026 timeframe is not arbitrary. Summer months consistently represent the peak of global refined product consumption, driven by aviation fuel demand during the Northern Hemisphere travel season, elevated road transport fuel consumption, and air conditioning-linked power generation demand in hot climates. In an environment where inventories are already declining from crisis-related supply losses, the additional demand load of peak summer consumption creates a compounding pressure dynamic.

IEA data indicates that while observed global inventories actually registered some growth during Q2 2026, this was primarily attributable to Chinese crude stock builds and U.S. natural gas liquids accumulation rather than genuine market easing. These are specific inventory categories with limited interchangeability with the crude grades required by international refiners. The underlying tightness in commercial crude availability has continued despite these headline inventory movements. In addition, natural gas price trends add further complexity to energy cost forecasting in this environment.

The Short-Term to Medium-Term Price Trajectory

The table below summarises the competing market forces across different timeframes and their implications for price direction.

| Timeframe | Market Condition | Price Direction | Key Driver |

|---|---|---|---|

| Near-Term (Q2-Q3 2026) | Tight supply, low visible stocks | Upward pressure | Hormuz disruption + summer demand |

| Medium-Term (Q4 2026) | Potential surplus build | Downward pressure | OPEC+ output + demand moderation |

| 2026 Full Year | Contested | Volatile | Geopolitical risk premium |

Oil Price Benchmarks and the Geopolitical Risk Premium

Brent and WTI: Reading the 45% Rally

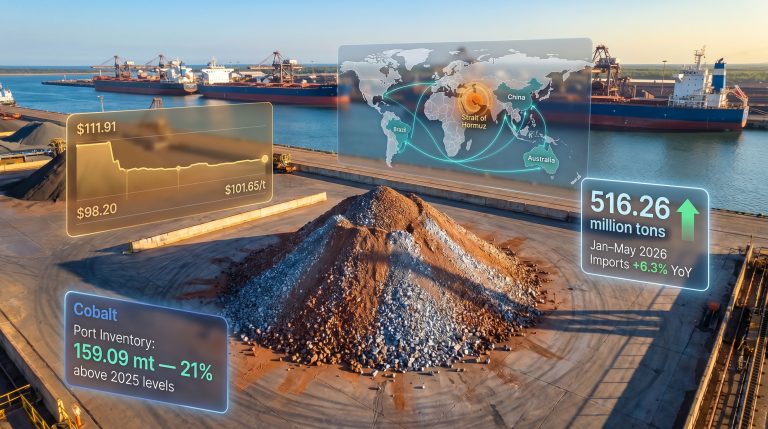

As of afternoon trading in London in May 2026, Brent crude futures had risen 1.9% to US$106.92 per barrel whilst WTI futures gained 2.4% to reach US$100.59 per barrel. Both benchmarks have appreciated approximately 45% since military operations commenced on February 28, 2026.

A gain of this magnitude in roughly 80 trading days raises a legitimate analytical question: how much of the current price level reflects genuine physical scarcity versus a geopolitical risk premium that could deflate rapidly on positive diplomatic news? The answer matters because these two components of the price respond to very different catalysts.

- Physical scarcity premium dissipates only when supply is physically restored and inventories rebuild, a process measured in months to years.

- Geopolitical risk premium can evaporate within hours on credible peace deal signals, as demonstrated by the temporary market stabilisation on May 18, 2026, when diplomatic commentary from Washington briefly reduced selling pressure.

The implication is that even a partial diplomatic resolution could produce sharp near-term price corrections without actually resolving the underlying supply deficit. This oil price impact has been particularly pronounced in import-dependent emerging economies, where currency depreciation compounds the effect of higher dollar-denominated crude costs.

Scenario Analysis: Three Pathways Through Year-End 2026

Scenario 1: Hormuz Reopens, Surplus Returns

If a diplomatic resolution allows maritime traffic to resume within 60-90 days and infrastructure rehabilitation proceeds without further disruption, the market would likely transition toward surplus in Q4 2026. Brent would be expected to retreat toward the US$75-85 per barrel range as inventories rebuild and the geopolitical premium unwinds.

Scenario 2: Prolonged Disruption, Strategic Reserves Further Depleted

If the conflict extends through Q3 2026, forcing a second coordinated SPR release, Brent could remain sustained above US$100 per barrel well into the fourth quarter. Demand destruction would begin to emerge in price-sensitive markets, particularly import-dependent developing economies. Central banks in emerging markets would face the unwelcome choice between defending currencies and containing inflation.

Scenario 3: Partial Resumption With Persistent Risk Premium

The scenario most consistent with current market positioning involves partial reopening of Strait traffic, with residual military and geopolitical risk keeping a sustained premium embedded in prices. Under this scenario, Brent would likely trade in a volatile range between US$90-105 per barrel, with significant intraday volatility driven by diplomatic news flow.

Developing Economies and the Disproportionate Impact of Supply Shocks

Asia, Africa, and the Intersection of Energy and Food Security

The IEA's assessment of economic consequences draws a direct line between oil price inflation and food security outcomes in developing nations. This connection is more direct than is commonly understood. Oil price increases transmit into food costs through multiple channels simultaneously:

- Fertiliser costs, as nitrogen-based fertilisers are produced from natural gas, whose price correlates with crude oil.

- Agricultural machinery fuel costs, which raise the direct cost of cultivation and harvest.

- Freight and logistics costs, which inflate food prices at every point along the distribution chain.

- Irrigation energy costs in countries reliant on pump-based water systems for agriculture.

For nations already experiencing fiscal stress, currency depreciation, or inadequate foreign exchange reserves to manage elevated import costs, the compounding effect of simultaneously higher energy and food prices can produce serious social and macroeconomic consequences.

Mexico's Market Response and Structural Energy Vulnerabilities

Mexico's financial markets have not been immune to the transmission effects of the global oil supply shock. The S&P/BMV IPC benchmark index declined 0.40% to close at 68,128.22 units on May 19, 2026, whilst the FTSE BIVA index fell 0.42% to settle at 1,365.18 units during the same session.

Within the benchmark index, mining and industrial equities registered the sharpest losses:

- Industrias Peñoles fell 3.48% to close at MX$918.51 (approximately US$53)

- Grupo México declined 1.86% to MX$196.88

- Orbia dropped 1.44% to MX$21.85

Technical analysts at CopKapital noted that the S&P/BMV IPC continues to trade below its one-month moving average, with weak technical signals persisting across the benchmark. This is a pattern consistent with markets experiencing externally-driven macroeconomic uncertainty rather than company-specific or domestically-generated selling pressure.

Mexico's exposure to Hormuz-related disruptions is structural rather than incidental. As a net importer of refined petroleum products and an economy with significant industrial and manufacturing sectors, sustained above-US$100 crude pricing creates pass-through inflation pressure that directly affects the Bank of Mexico's policy calculus.

The next major ASX story will hit our subscribers first

OPEC+ Output Decisions and the Medium-Term Supply Equation

Record Supply Growth on the Horizon

Beyond the near-term crisis, IEA projections paint a picture of global oil supply growing faster than demand over the medium term. If current production trends from non-OPEC+ producers continue and OPEC+ production decisions lead to output increases in response to elevated prices, the global market could face inventory accumulation of nearly 3 million barrels per day by late 2026. This would represent one of the most rapid inventory build cycles in modern petroleum history.

The strategic dilemma for OPEC+ is acute. Higher prices incentivise production increases, but those increases risk accelerating the transition from shortage to surplus and ultimately undermining the price levels that make higher production financially attractive. Furthermore, OPEC's market influence remains a central variable in how quickly any medium-term surplus materialises.

Sanctions as Partial Supply Offsets

Ongoing sanctions on both Iranian and Russian crude exports represent a constraining factor on the anticipated global supply surge. However, the IEA's assessment is that even accounting for sanctions-related production caps, the year-end 2026 supply balance remains skewed toward oversupply if the Hormuz disruption resolves. The EIA's global oil outlook reflects similar expectations, with lower Brent price forecasts for late 2026 contingent on supply outpacing demand as the conflict-related premium unwinds.

What Market Participants Should Monitor

Key Data Releases and Decision Points

For commodity market participants navigating this environment, the following data points and decision nodes represent the highest-priority monitoring priorities:

- Weekly EIA Petroleum Status Reports: The primary source for real-time observable inventory data at U.S. pricing hubs, particularly Cushing.

- IEA Monthly Oil Market Reports: The definitive source for global supply-demand balance revisions and inventory trajectory updates.

- OPEC+ meeting outcomes: Any production quota decisions will directly affect the medium-term supply-demand balance.

- U.S.-Iran diplomatic communications: Given the demonstrated sensitivity of intraday price movements to diplomatic signals, monitoring official statements from both governments is essential.

- Strait of Hormuz transit data: Vessel tracking services that monitor tanker movements through the Strait provide the earliest observable signal of any partial or full resumption of traffic.

Managing Energy Cost Exposure for Industrial Operators

For energy-intensive businesses operating in import-dependent economies, the sustained above-US$100 crude environment creates specific operational challenges. Forward energy contract coverage during periods of geopolitical uncertainty can provide cost predictability that raw exposure to spot prices cannot. Supply chain diversification, particularly the identification of alternative feedstock sources and logistics routes that reduce dependence on Middle Eastern crude, represents a medium-term resilience investment with relevance well beyond the current crisis. The IEA warning on global oil inventories and summer supply shortage should therefore serve as a catalyst for strategic operational review rather than simply a market headline.

Disclaimer: This article contains forward-looking statements, scenario projections, and market analysis that are inherently speculative. Price forecasts, scenario outcomes, and supply-demand projections are subject to material change based on geopolitical developments, policy decisions, and market forces that cannot be reliably predicted. Nothing in this article constitutes investment advice. Readers should conduct independent due diligence and consult qualified financial advisors before making any investment or business decisions based on information contained herein.

Want To Stay Ahead of Market-Moving Resource Discoveries Amid Energy Market Volatility?

While geopolitical shocks reshape global commodity markets, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and delivering actionable insights to subscribers before the broader market reacts — explore historic discovery returns on the Discovery Alert discoveries page and begin your 14-day free trial today.