June 17, 2026

When Political Agreements Outpace Physical Reality: The Energy Recovery Illusion

Global commodity markets have a well-documented tendency to discount future outcomes long before the underlying physical conditions actually change. In the hours following a ceasefire announcement, algorithmic trading systems, futures desks, and risk managers all move in the same direction simultaneously, repricing geopolitical risk out of oil contracts with a speed that bears little relationship to how long it actually takes to restart a damaged refinery, redirect a tanker fleet, or restore shipping insurance coverage to a war-affected maritime corridor.

This divergence between financial market speed and physical supply reality sits at the heart of the International Monetary Fund's post-ceasefire warning about IMF energy recovery after the US-Iran ceasefire. The Fund's position is straightforward but easily misread: a ceasefire is a necessary first step, not a finish line.

When big ASX news breaks, our subscribers know first

The Structural Gap Between Diplomacy and Supply Chain Restoration

Understanding why energy markets cannot simply "snap back" after a conflict requires separating two fundamentally different systems that operate on incompatible timescales.

Financial markets process new information in milliseconds. The risk premium embedded in crude oil futures in response to conflict can be unwound in a single trading session. Physical supply chains work on entirely different logic. Wells that have been shut in, processing facilities that have been damaged or idled, and tanker routes that have been abandoned due to security concerns do not restart overnight regardless of what a peace agreement says.

The four-month duration of the US-Iran conflict is particularly significant from an infrastructure standpoint. Extended conflict periods cause cumulative degradation that differs qualitatively from brief disruptions. Furthermore, this damage extends across multiple interconnected systems simultaneously:

- Reservoir pressure management becomes problematic when wells are shut in for extended periods, potentially reducing recoverable output upon restart

- Processing and separation equipment may require safety inspections and maintenance cycles before returning to full capacity

- Skilled operational personnel may have evacuated the region, creating staffing constraints on restart timelines

- Marine insurance underwriters typically require reassessment periods before reinstating coverage for tanker transit through previously hazardous corridors

- Port logistics systems, including scheduling, pilotage services, and cargo documentation, require time to rebuild operational cadence

Each of these factors compounds the others, meaning the actual timeline for restoring full supply is not a simple linear function of political will.

The Strait of Hormuz: More Than a Shipping Lane

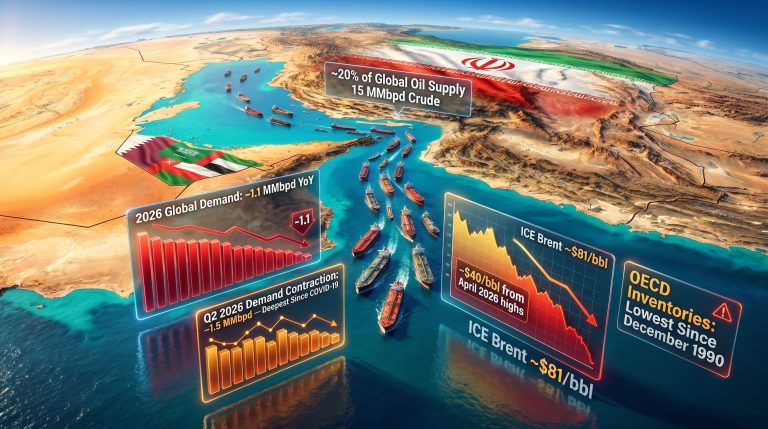

The Strait of Hormuz carries approximately 20% of the world's daily oil consumption under normal operating conditions, making it the single most consequential maritime chokepoint in the global energy system. Unlike many strategic waterways, Hormuz has no viable large-scale alternative for the volumes it handles. Pipeline capacity across the Arabian Peninsula can divert some Gulf crude, but nothing approaching the full throughput of seaborne trade through the strait.

What makes Hormuz disruptions particularly severe from a supply chain perspective is the compounding effect of production shutdowns and transit disruptions occurring simultaneously. A disruption that affects only shipping can be partially offset by drawing down inventories. A disruption that affects both production and shipping simultaneously creates a supply deficit that cannot be bridged through inventory releases alone, particularly when the disruption extends across multiple quarters.

The oil market trade war impact on supply chain fragility provides important context here, as pre-existing vulnerabilities were amplified by the conflict's effects on regional infrastructure. Traders appear to be pricing in a relatively swift restoration of supply through Hormuz, while the IMF is explicitly flagging that physical recovery operates on a materially longer timeline. The gap between those two readings is itself a market risk.

IMF Energy Recovery After US-Iran Ceasefire: What the Fund Actually Said

IMF Managing Director Kristalina Georgieva's formal response to the ceasefire was notably calibrated. She welcomed the agreement while simultaneously cautioning that supply recovery would be constrained by the extent of infrastructure damage sustained during the conflict. The Fund's assessment explicitly distinguished between the global economy demonstrating resilience and declaring the energy crisis resolved, two conditions that are very different in practice.

Georgieva's core analytical point was that supply will require extended time to recover given the significant infrastructure damage incurred, and that the duration and intensity of the energy supply shock remain the critical variable determining global economic outcomes. The ceasefire addresses duration but does not immediately resolve intensity, because physical infrastructure does not repair itself at the pace of diplomatic negotiations. The IMF chief's warning underscores that energy recovery timelines must be assessed independently from diplomatic progress.

The July 8 World Economic Outlook Update: Key Metrics to Watch

The IMF's April World Economic Outlook established a range of scenarios against which the July 8 revision will be benchmarked. The following comparison illustrates what analysts will be assessing:

| IMF Scenario Framework | Growth Projection | Inflation Projection | Status |

|---|---|---|---|

| April Base Case | Above 2.0% | Moderate | Benchmark reference |

| April Severe Scenario | Approximately 2.0% | Above 6.0% | Worst-case contingency |

| Post-Ceasefire Trajectory | TBD | TBD | July 8 WEO update |

The July 8 revision will constitute the first comprehensive post-conflict assessment, revealing how closely the global economy tracked against the Fund's severe scenario and providing updated projections that incorporate the ceasefire's partial resolution of geopolitical uncertainty.

Notably, Georgieva indicated that both the United States and China, the two primary engines of global economic momentum, showed continued resilience through the disruption period. This anchoring effect from the world's two largest economies may explain why the IMF's language emphasises caution rather than alarm.

Oil Price Reaction: Optimism Running Ahead of Fundamentals

The immediate market reaction to the ceasefire announcement was sharp and instructive. WTI crude fell more than 5% to approximately US$80 per barrel, while Brent crude declined around 4.5% to approximately US$83 per barrel, with both benchmarks reaching their lowest levels since early March 2026, shortly after the conflict commenced.

This single-session repricing illustrates a well-understood but persistently underappreciated dynamic in commodity markets: geopolitical risk premiums are priced into futures almost instantly when conflict escalates, and they are unwound almost as instantly when conflict de-escalates. Understanding crude oil price trends in the months preceding the conflict reveals how sensitive these markets are to even partial resolutions of geopolitical uncertainty.

The risk embedded in this disconnect can be framed as a secondary correction scenario: if tanker traffic through Hormuz and Gulf production capacity take longer to restore than the market's one-day repricing implies, futures prices will need to be revised upward again to reflect the persistent supply deficit. This second-wave correction would carry its own inflationary consequences for oil-importing economies, compounding the damage already absorbed.

Three Scenarios for the Post-Ceasefire Oil Market

| Scenario | Hormuz Reopening Speed | OPEC+ Output Effect | Likely Price Direction |

|---|---|---|---|

| A: Gradual Recovery | Months | Partial deficit offset | Elevated and persistent |

| B: Rapid Recovery | Weeks | Potential oversupply | Sharp downward correction |

| C: Extended Disruption | Delayed | Absorbed by supply gap | Prolonged price elevation |

Gulf Economies: Production Collapse Behind Higher Prices

One of the less-examined aspects of the conflict's impact involves the paradox facing Gulf oil-exporting nations. While elevated crude prices might theoretically benefit producers, the actual production collapse caused by conflict-related infrastructure damage created a situation where higher prices only partially offset collapsed output volumes. The net revenue effect was strongly negative for most regional producers.

The IMF's assessment found that five out of eight Gulf oil-exporting countries face outright economic contractions in 2026, with steep downward growth revisions across the region. This is a striking figure given that the Gulf's fiscal models are structured around hydrocarbon revenue as the primary source of government income. When production volumes collapse, even elevated prices cannot compensate for the volume deficit in fiscal arithmetic.

This regional damage assessment forms the bedrock of Georgieva's broader caution: if the producing economies themselves are contracting, the assumption that supply will quickly normalise after a ceasefire lacks a credible physical foundation.

The next major ASX story will hit our subscribers first

OPEC+ Production Strategy and the Convergence Risk

A factor that adds significant complexity to post-ceasefire price dynamics is the concurrent OPEC+ production strategy. The group approved four consecutive monthly output quota increases during the conflict period as part of a previously scheduled unwinding of voluntary production cuts. Consequently, OPEC+ supply additions were already entering the market before the ceasefire was announced. OPEC's market influence during this period has therefore created a dual dynamic that complicates straightforward price forecasting.

The convergence of these two supply-side forces, Hormuz reopening and OPEC+ additions, creates materially different outcomes depending on the speed of physical restoration:

-

If Hormuz reopens gradually over several months, OPEC+ additions will be absorbed by the ongoing supply deficit, and prices may stabilise at elevated levels without a sharp correction.

-

If Hormuz reopens faster than physical infrastructure conditions actually support, the combined effect of OPEC+ additions and restored Gulf production could create a temporary oversupply condition, driving a price correction beyond what current market expectations anticipate.

-

If infrastructure damage proves more severe than initial assessments suggest, even the combined effect of OPEC+ additions and a nominal ceasefire will be insufficient to fill the production gap, sustaining prices at elevated levels for an extended period.

The critical variable that no market participant can currently price with confidence is the actual severity of damage to Gulf production infrastructure, which will only become clear as technical teams conduct on-the-ground assessments over the coming weeks. OPEC demand revisions will further shape how these scenarios ultimately play out across the second half of 2026.

Mexico's Fiscal Exposure: A Compounded Planning Challenge

The Budget Reference Price and Its Current Alignment

Mexico's Pre-Criterios 2027 document revised the country's 2026 budget reference oil price upward to US$77.3 per barrel in response to the conflict's impact on global crude markets. With post-ceasefire WTI prices trading near US$80 per barrel, the current market level sits broadly consistent with this revised planning assumption, at least in the immediate term.

However, the keyword is "immediate term." Mexico's fiscal planning must account for price trajectories across the full budget year, not just the day following a ceasefire announcement. Both the upside and downside risks from this point remain material.

The IEPS Subsidy Mechanism: Fiscal Exposure in Both Directions

Mexico's Impuesto Especial sobre Producción y Servicios (IEPS) fuel subsidy creates a direct and automatic linkage between international oil prices and federal expenditure. This mechanism functions as an involuntary hedge in the fiscal accounts, but one that creates costs in both high-price and low-price environments:

- When prices remain elevated above budget assumptions: IEPS subsidy costs increase to protect domestic consumers from full pass-through of international prices, partially offsetting the hydrocarbon revenue benefit that elevated prices provide to Pemex and federal accounts.

- When prices fall sharply below budget assumptions: IEPS subsidy costs decline, reducing expenditure pressure, but hydrocarbon revenues simultaneously compress, creating a different category of fiscal imbalance.

Mexico's SHCP faces a compounded uncertainty that few fiscal authorities globally must navigate: modelling federal revenues against an oil price that could move materially in either direction, with the determining variable being the pace of infrastructure restoration thousands of kilometres away in the Persian Gulf.

The April Ceasefire Precedent as a Risk Signal

A critical historical reference point for Mexico's planning context is the April 2026 ceasefire attempt that ultimately proved short-lived. That episode would have exposed the fiscal model to the same optimistic repricing followed by renewed disruption pattern that the current ceasefire risks repeating if physical restoration lags diplomatic resolution.

If OPEC+ supply additions combine with a faster-than-expected Hormuz reopening, prices could fall below the revised US$77.3 per barrel planning assumption, creating the same fiscal stress dynamic that the April episode demonstrated. This is precisely the scenario that the SHCP must model as a credible downside case. The broader oil geopolitics analysis for 2025 and 2026 highlights how rapidly these fiscal planning assumptions can become obsolete when geopolitical conditions shift.

How Long Does Energy Infrastructure Recovery Actually Take?

A Four-Phase Framework for Post-Conflict Supply Restoration

Historical precedents from other conflict-affected producing regions provide a useful framework for understanding realistic recovery timelines. Physical restoration typically progresses through four distinct phases, each with its own minimum duration:

-

Safety and Security Assessment: Before any production restart can be attempted, facilities must be cleared, inspected, and confirmed safe. Depending on the scale of damage, this phase alone typically requires several weeks to several months.

-

Production Restart Sequencing: Wells and processing facilities cannot be brought back online simultaneously. They must be restarted in a carefully managed sequence to manage reservoir pressure and avoid equipment damage. This phase typically requires one to six months, with the outer range applying where significant equipment damage has occurred.

-

Logistics and Shipping Normalisation: Redirecting tanker fleets, clearing port backlogs, restoring marine insurance coverage, and rebuilding shipping schedules typically requires two to four months after a Hormuz-style disruption, even after the security environment is confirmed as stable.

-

Market Confidence Restoration: Buyers of Gulf crude require sustained evidence of supply reliability before returning to normal forward contracting patterns. This psychological recovery phase can extend from three months to a full year, representing the longest tail in the recovery process.

The IMF's explicit reference to significant infrastructure damage as the primary constraint on recovery speed is consistent with this framework. Furthermore, energy recovery warnings from the IMF chief reinforce the distinction between transit-only disruptions, which have historically resolved faster, and production-and-transit disruptions, which is the category the current conflict appears to represent.

Frequently Asked Questions: IMF Energy Recovery After the US-Iran Ceasefire

Why won't energy markets recover immediately after the US-Iran ceasefire?

A ceasefire removes the geopolitical risk premium from oil futures almost instantly, but it does not repair damaged production infrastructure, restore depleted inventories, or normalise tanker routing through the Strait of Hormuz. Physical supply chains recover on timelines measured in months, while financial markets reprice in hours. This fundamental asymmetry is the central risk the IMF is flagging.

What does the IMF project for global growth following the ceasefire?

The Fund's July 8 World Economic Outlook revision will provide the first comprehensive post-conflict projection. The April 2026 WEO severe scenario projected global growth falling to approximately 2% with inflation exceeding 6%. The July update will reveal how closely actual outcomes tracked that severe scenario versus the more optimistic base case.

How much did oil prices fall on the day of the ceasefire announcement?

WTI crude declined more than 5% to approximately US$80 per barrel and Brent crude fell around 4.5% to approximately US$83 per barrel, reaching the lowest levels for both benchmarks since the conflict's early days in March 2026.

How many Gulf economies are facing economic contraction?

The IMF assessed that five out of eight Gulf oil-exporting nations face outright economic contractions in 2026 as a direct result of the conflict's combined impact on production volumes and regional economic activity.

What is the secondary correction risk in oil markets?

If the physical restoration of Gulf production capacity and Hormuz tanker traffic proves slower than financial markets currently anticipate, a renewed upward price correction becomes plausible, as the market would need to reprice a supply deficit that was prematurely discounted in the initial post-ceasefire session.

How does the ceasefire affect Mexico's hydrocarbon revenue outlook?

Mexico revised its 2026 budget reference oil price to US$77.3 per barrel during the conflict. Post-ceasefire prices near US$80 per barrel are currently consistent with that assumption, but both upside and downside risks remain significant depending on the speed of Gulf infrastructure restoration and the net effect of concurrent OPEC+ production increases.

Disclaimer: This article contains forward-looking analysis, economic projections, and scenario-based assessments. The IMF's July 8 World Economic Outlook update may materially alter the projections referenced herein. Oil price forecasts and fiscal modelling outcomes involve significant uncertainty and should not be interpreted as investment advice. Readers should conduct their own analysis before making financial or investment decisions.

Want to Stay Ahead of the Next Major Resource Discovery Amid Global Energy Uncertainty?

While oil markets navigate the complex aftermath of geopolitical disruption, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries and turning complex data into actionable investment opportunities — explore the historic returns major discoveries have delivered and begin your 14-day free trial today to position yourself ahead of the broader market.