June 21, 2026

Geopolitical Fault Lines and the Economies Built to Withstand Them

Not every economy buckles when its region catches fire. History shows that nations with diversified revenue streams, disciplined fiscal management, and intact export infrastructure can not only survive regional conflict but sometimes emerge from it with strengthened relative positioning. The Gulf has demonstrated this pattern before, and the IMF's June 2026 assessment of Oman's economic trajectory suggests the sultanate is doing so again.

Understanding IMF Oman economy resilience amidst Middle East war requires moving beyond headline growth figures. The more instructive analysis lies in examining the transmission mechanisms through which conflict stress enters an economy, which buffers absorb it, and where genuine vulnerability remains. Oman's current macroeconomic profile offers a compelling case study across all three dimensions.

When big ASX news breaks, our subscribers know first

What the IMF's 2026 Growth Revision Actually Signals

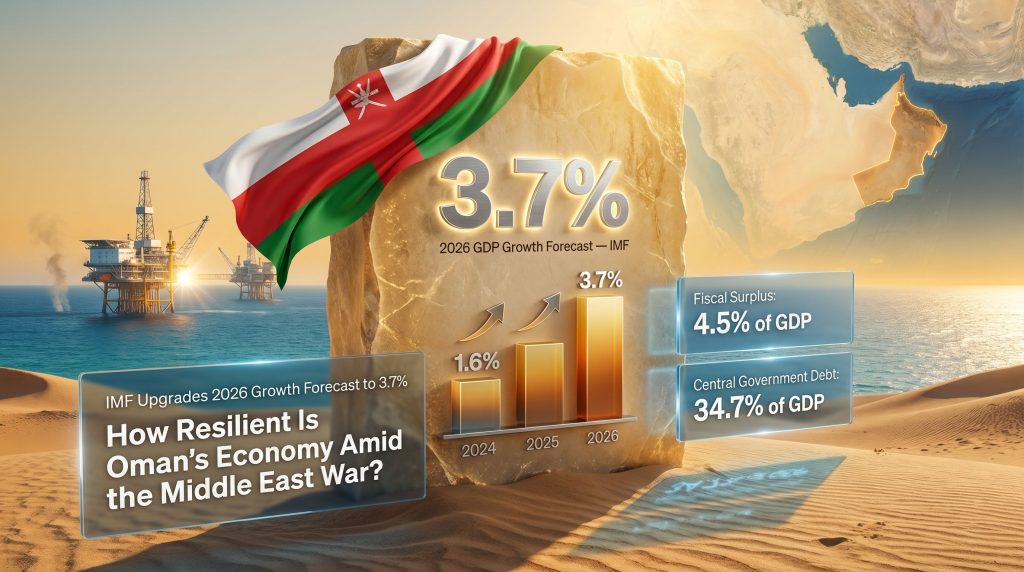

When the IMF revises a growth forecast upward mid-cycle during active regional conflict, that adjustment carries more informational weight than a routine update. The June 2026 upgrade, lifting Oman's projected real GDP expansion from 3.5% to 3.7% for the year, is notable precisely because it moves against the directional pressure that most analysts would expect conflict-adjacent economies to face.

The broader growth arc tells an equally instructive story:

| Year | Real GDP Growth | Primary Driver |

|---|---|---|

| 2024 | 1.6% | Moderate hydrocarbon recovery |

| 2025 | 2.4% | Balanced hydrocarbon and non-hydrocarbon growth |

| 2026 (projected) | 3.7% | Increased oil production and export volumes |

| 2027 (projected) | 3.0% | Sustained structural reform momentum |

This trajectory represents a near-doubling of growth pace from 2024 to 2026, a performance profile that sits in sharp contrast to what regional conflict economics would typically predict.

The Dual-Engine Expansion and Why It Matters

A critical but underappreciated aspect of Oman's growth story is that 2025 expansion was not exclusively hydrocarbon-driven. The IMF confirmed that real GDP growth in 2025 drew from both hydrocarbon and non-hydrocarbon activities, which matters enormously for assessing the durability of the recovery. Single-engine hydrocarbon growth is inherently volatile and oil-price dependent.

Balanced growth signals that Oman Vision 2040's diversification agenda is beginning to produce measurable real-economy outcomes, not just policy announcements. Furthermore, this dual-engine dynamic has important implications for how the country's performance is assessed within oil futures markets, where supply continuity and export volume projections carry significant weight.

Key Insight: The IMF's upward revision from 3.5% to 3.7% for 2026 signals more than positive short-term momentum. It reflects an institutional judgment that Oman's structural buffers are holding under active conflict pressure, a materially different assessment than simply benefiting from elevated oil prices.

Oil and Gas Infrastructure: The Competitive Moat That War Hasn't Breached

At the core of Oman's economic resilience sits a fact that receives insufficient analytical attention: its hydrocarbon infrastructure has remained largely unaffected by the regional conflict. This is not a passive outcome. It reflects Oman's geographic position, diplomatic posture, and the sultanate's longstanding practice of maintaining working relationships across otherwise adversarial regional blocs.

The practical economic consequences of intact infrastructure are substantial:

- Oman has been able to increase oil production at precisely the moment when regional supply disruptions have created export opportunity gaps.

- Uninterrupted export logistics have allowed the country to capture premium pricing in markets where alternative supply sources have been constrained.

- The continuity of gas processing and LNG export operations has sustained government revenue streams that fund both fiscal surpluses and Vision 2040 investment programs. In addition, the broader LNG supply outlook for the region suggests that Oman's operational continuity positions it advantageously as competing suppliers face disruption.

- Infrastructure integrity preserves Oman's credit relationships with international energy majors and project finance lenders, which would otherwise face force majeure risk assessments.

This dynamic illustrates a broader principle in resource-economy geopolitics: when a producer can maintain operational continuity during a period of regional supply disruption, it captures not just its own normal market share but incremental demand displaced from disrupted competitors. Oman appears to be benefiting from exactly this mechanism in 2026.

How War Pressure Is Transmitting Into the Omani Economy

Despite the headline resilience narrative, it would be analytically incomplete to ignore the channels through which conflict stress is reaching the Omani economy. The IMF's assessment identifies inflation as the most visible and near-term transmission mechanism.

Inflation: From Subdued to Accelerating

Inflation averaged just 1.0% across 2025, a figure that reflects both the Gulf's historically moderate consumer price environment and the relative insulation Oman enjoyed during the earlier phase of the conflict. However, the first five months of 2026 have seen that figure climb to 2.8%, driven by higher food costs and transportation expenses.

Watch Point: A move from 1.0% to 2.8% represents a near-tripling of inflation pressure within a single fiscal year. While 2.8% remains manageable by global standards, the velocity of the acceleration matters as much as the absolute level. Sustained conflict-driven supply chain friction could push this trajectory further.

The mechanics of this inflationary transmission are worth understanding in detail:

- Regional logistics disruption raises freight and insurance costs for imported goods, with food staples being particularly exposed given Oman's import dependency for certain agricultural products.

- Transportation cost pass-through affects domestic distribution economics across retail, hospitality, and manufacturing supply chains.

- Food price escalation hits lower-income household budgets disproportionately, creating social pressure that can feed into wage demands and broader cost structures over time.

- Energy-adjacent input costs for construction and manufacturing can rise even when headline oil prices remain stable, given the friction in regional procurement logistics.

Sectoral Vulnerability: Where Conflict Risk Concentrates

Not all sectors of Oman's economy face equivalent exposure. The IMF's assessment implies an asymmetric impact profile:

| Sector | Conflict Exposure | Key Risk Mechanism |

|---|---|---|

| Hydrocarbon production | Low | Infrastructure intact, export volumes rising |

| Tourism | High | Regional conflict perception suppresses visitor flows |

| Non-hydrocarbon exports | Moderate-High | Trade route disruption and logistics cost escalation |

| Foreign direct investment | Moderate | Geopolitical uncertainty extends investor decision cycles |

| Banking system | Low-Moderate | Well-capitalised but monitoring inflation and FDI flows |

| Real estate | Low-Moderate | Domestic demand supported; Q1 price index rose 15.9% year-on-year |

The tourism sector deserves particular attention. Oman has invested significantly in developing its tourism infrastructure as a core non-hydrocarbon revenue pillar under Vision 2040. Regional conflict, regardless of its proximity to Omani territory, creates perception-based risk aversion among international leisure travellers that can suppress inbound visitor numbers well beyond the physical reach of any hostilities.

Fiscal Strength: The Quantitative Case for Resilience

Perhaps the most compelling evidence for IMF Oman economy resilience amidst Middle East war is visible not in growth forecasts but in fiscal metrics. The combination of a dramatically widening surplus, declining government debt, and a current account reversal creates a policy buffer that most regional peers cannot match.

Fiscal Surplus: From Narrow to Substantial

The projected expansion of Oman's fiscal surplus from 0.6% of GDP in 2025 to 4.5% of GDP in 2026 is a dramatic shift driven by a convergence of factors: higher oil export revenues from increased production volumes, disciplined expenditure management, and the compounding benefits of earlier structural reforms feeding through into revenue efficiency.

A fiscal surplus of this scale matters for several reasons beyond the headline number:

- It creates counter-cyclical spending capacity if the conflict escalates and demands emergency economic support measures.

- It reduces the government's need to access external debt markets, lowering refinancing risk and preserving borrowing capacity for strategic purposes.

- It signals to credit rating agencies and sovereign bond investors that fiscal consolidation is durable rather than oil-price dependent.

- It provides the government with resources to accelerate Vision 2040 infrastructure investments even if private FDI inflows slow due to geopolitical hesitancy.

Debt Trajectory and Current Account Reversal

Central government debt has been following a disciplined downward path, reaching 34.7% of GDP at end-2025. For an oil-exporting sovereign, this level represents a manageable debt burden, particularly when combined with a widening fiscal surplus that accelerates the deleveraging trajectory.

The current account story is equally significant. A swing from a deficit of 1.9% of GDP in 2025 to a projected surplus of approximately 3.0% in both 2026 and 2027 reflects the combined effect of higher export revenues and moderated import demand. This reversal reduces Oman's external financing requirement and supports riyal stability under the country's dollar-pegged exchange rate regime.

| Fiscal Metric | 2025 (Actual) | 2026 (Projected) | 2027 (Projected) |

|---|---|---|---|

| Fiscal Surplus (% of GDP) | 0.6% | 4.5% | Positive |

| Central Govt Debt (% of GDP) | 34.7% | Declining | Declining |

| Current Account Balance (% of GDP) | -1.9% | ~+3.0% | ~+3.0% |

Banking Sector Resilience: The Institutional Foundation

A frequently overlooked dimension of sovereign economic resilience is the condition of the domestic banking system. Fiscal surpluses mean little if the financial transmission mechanism that converts government revenue into private sector credit growth is impaired.

The IMF's June 2026 assessment characterises Oman's banking sector as operating with comfortable capital adequacy ratios, strong liquidity buffers, and sustained profitability. Non-performing loan levels and provisioning adequacy have remained within acceptable parameters despite the inflationary pressure building in the first half of 2026.

Credibility Marker: An IMF assessment endorsing banking sector health provides tangible institutional credibility for Oman's correspondent banking relationships and access to international capital markets, particularly important when regional risk premiums are generally elevated.

The banking system's resilience also matters for Vision 2040 implementation. Private sector diversification initiatives, whether in tourism infrastructure, logistics, or digital economy development, depend heavily on domestic credit availability and the willingness of both local and international banks to extend project finance against an uncertain regional backdrop.

The next major ASX story will hit our subscribers first

Downside Risks: What Could Derail the Resilience Narrative?

The IMF is explicit that risks to Oman's near-term outlook are tilted to the downside, a judgment that warrants careful scenario analysis rather than dismissal. Consequently, understanding the full geopolitical risk landscape is essential for any investor or policymaker assessing the durability of Oman's current trajectory.

Conflict Escalation Scenarios

A sustained or deepening regional conflict could generate several compounding pressures:

- Tourism revenue collapse: Even a modest deterioration in regional security perceptions could significantly reduce inbound visitor numbers, undermining a critical non-hydrocarbon growth pillar.

- Non-oil export disruption: Construction materials, manufactured goods, and re-export logistics all depend on regional trade route functionality that cannot be guaranteed under escalating conflict conditions. Indeed, global trade disruptions of this nature have historically proven difficult to reverse quickly once established.

- FDI withdrawal acceleration: Foreign investors making long-duration capital commitments face elevated uncertainty costs that can push decision timelines outward by years, not months.

- Oil price volatility: Paradoxically, sustained high oil prices benefit Omani fiscal revenues, but severe regional conflict escalation could trigger global demand destruction that reverses the oil price environment underpinning the current surplus projection.

Upside Scenarios That Could Accelerate Growth

- A negotiated conflict resolution, even partial, could rapidly unlock suppressed tourism demand and release FDI decisions that have been deferred during the period of uncertainty.

- Extended regional supply disruptions elsewhere could maintain elevated oil prices for longer, compressing Oman's breakeven fiscal oil price requirement.

- Accelerated Vision 2040 reform implementation could attract a new cohort of strategic investors seeking stable, reform-oriented Gulf exposure.

The IMF's Structural Reform Priorities for Long-Term Durability

Resilience in the short term is a function of buffers. Resilience over the long term is a function of structural transformation. The IMF has identified five reform priorities that collectively address Oman's structural dependency on hydrocarbon revenues:

- Tax Administration Modernisation: Improving collection efficiency and broadening the non-oil revenue base to reduce fiscal vulnerability to oil price cycles.

- Medium-Term Fiscal Frameworks: Building multi-year budget discipline that insulates public spending plans from year-to-year oil revenue volatility.

- State-Owned Enterprise Transparency: Enhancing governance, commercial accountability, and disclosure standards across the SOE sector to improve capital allocation efficiency.

- Female Labour Force Participation: Unlocking a significant underutilised human capital reservoir that could materially expand the non-hydrocarbon private sector workforce.

- Renewable Energy Investment: Accelerating the energy transition to diversify Oman's long-term economic base. This priority aligns closely with the broader shift towards renewable energy investment visible across Gulf and global resource economies, as nations seek to capture export opportunities in green hydrogen and clean energy.

Oman Vision 2040 provides the strategic architecture that connects these reform priorities into a coherent long-term programme. The pace at which Vision 2040's diversification pillars across tourism, logistics, manufacturing, digital economy, and green energy translate from planning documents into operational economic activity will ultimately determine whether Oman's current resilience converts into durable structural transformation.

Oman Within the Broader Regional Picture

Situating Oman within the IMF's broader regional assessment reveals important comparative insights. The organisation's analytical framework for the Middle East identifies conflict as transmitting economic shocks unevenly depending on three primary variables: export profile, fiscal buffer depth, and infrastructure integrity.

According to the IMF's own assessments, Oman scores favourably across all three dimensions relative to several regional peers:

| Economic Dimension | Oman's Position | Regional Pressure Points |

|---|---|---|

| Oil Infrastructure Integrity | Largely intact | Varied disruption across region |

| Fiscal Surplus | Widening to 4.5% GDP | Narrowing in some peer economies |

| Inflation (2026 YTD) | Rising but moderate at 2.8% | Higher in import-dependent economies |

| Banking Sector Health | Resilient, well-capitalised | Stress emerging in conflict-proximate markets |

| FDI Vulnerability | Moderate | Elevated in geographically proximate states |

Economies with thin fiscal buffers and high import dependency are experiencing compounded pressure from both the conflict-driven cost escalation that Oman is also navigating and the additional burden of deteriorating export revenues. Oman's relatively favourable positioning within this spectrum does not eliminate its exposure to regional risk, but it does meaningfully shape the severity and duration of economic headwinds the country faces.

Frequently Asked Questions

What is the IMF's current GDP growth forecast for Oman in 2026?

The IMF projects real GDP growth of approximately 3.7% in 2026, revised upward by 0.2 percentage points from the April 2026 projection of 3.5%.

How has regional conflict affected inflation in Oman?

Inflation averaged around 1.0% across 2025 but accelerated to 2.8% in the first five months of 2026, driven primarily by higher food and transportation costs linked to regional supply chain disruption.

Has Oman's oil and gas infrastructure been damaged?

According to the IMF's June 2026 assessment, Oman's oil and natural gas infrastructure has remained largely unaffected by the regional conflict, enabling increased production and export volumes.

What is Oman's projected fiscal surplus for 2026?

The IMF projects the fiscal surplus to widen to 4.5% of GDP in 2026, up from a narrow 0.6% surplus recorded in 2025. Furthermore, the IMF has commended Oman's reform momentum as a contributing factor to this strong fiscal outcome.

What are the primary downside risks identified by the IMF?

A prolonged escalation of regional conflict represents the primary downside risk, with potential knock-on effects across tourism revenues, non-oil exports, and foreign direct investment inflows. This dynamic reflects why IMF Oman economy resilience amidst Middle East war remains a closely monitored subject for regional analysts.

What structural reforms has the IMF prioritised for Oman?

The IMF has identified tax administration improvements, medium-term fiscal framework strengthening, state-owned enterprise transparency, female labour force participation, and renewable energy investment as the key structural priorities.

Disclaimer: This article contains forward-looking projections sourced from IMF assessments as of June 2026. Economic forecasts are inherently subject to revision based on evolving geopolitical conditions, oil price movements, and policy implementation outcomes. This content is informational in nature and does not constitute financial or investment advice.

Want to Identify the Next Major Resource Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across 30+ commodities into clear, actionable insights for investors at every level — explore Discovery Alert's discoveries page to understand how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.