June 24, 2026

The Hidden Architecture of Global Energy Vulnerability

Every barrel of crude oil carries with it an invisible geography — a map of chokepoints, corridors, and dependencies that most consumers never consider when filling a tank or paying an electricity bill. For India, the world's third-largest oil importer and consumer, that invisible geography has spent decades converging on a single maritime passage roughly 33 kilometres wide at its narrowest point. The Strait of Hormuz is not merely a shipping lane. It is the structural backbone of India's energy supply chain, and when that backbone came under acute stress in early 2026, the consequences reverberated from refinery procurement desks in Mumbai to fertiliser production schedules in rural agricultural belts.

Understanding why India turns to African and Latin American oil after Strait of Hormuz disruption requires more than tracking cargo manifests. It demands an examination of how supply chain concentration risk becomes visible only when a crisis forces it into the open.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Controls So Much of India's Energy Destiny

The Mathematics of a Single Chokepoint

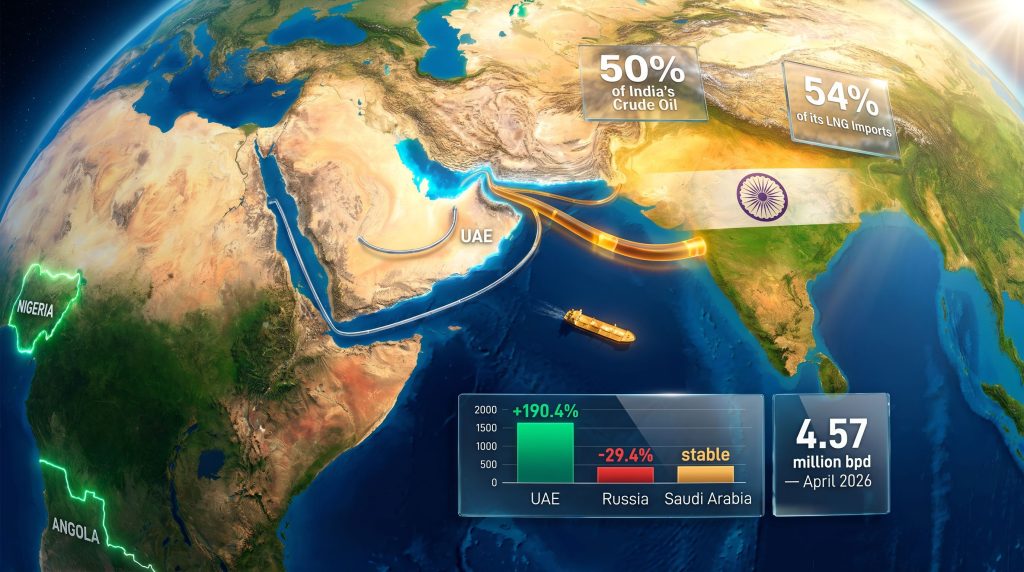

The Strait of Hormuz connects the Persian Gulf to the Gulf of Oman and, from there, to the broader global oil market. Approximately 21 million barrels of crude oil and petroleum products transit this passage every day, representing roughly 20% of global oil trade according to the U.S. Energy Information Administration. For context, no other maritime chokepoint carries a comparable volume of energy cargo.

India's exposure to this single corridor is particularly acute. Shipping data tracked by Kpler and reported through Reuters indicates that approximately 50% of India's crude oil imports and 54% of its LNG imports passed through the Strait of Hormuz during the 2024–25 financial year. Despite sourcing crude from roughly 40 different countries, the geographic concentration of those sources within the Persian Gulf means the supplier diversification India has cultivated provides limited protection against a corridor-level disruption.

The downstream consequences of a sustained Hormuz disruption extend well beyond elevated petrol prices at Indian forecourts:

- LPG supply compression, affecting domestic cooking fuel availability for hundreds of millions of households

- Natural gas shortfalls, constraining power generation during peak demand periods

- Fertiliser feedstock disruption, as ammonia and urea production depends heavily on natural gas inputs

- Agricultural cost inflation, transmitted through fertiliser price increases to food production costs across one of the world's most populous nations

A Hormuz disruption of sufficient duration would not register primarily as an energy market event in India. It would manifest as a food security and rural economy crisis — a dimension of the risk that rarely features in headline analysis of crude oil shipping lanes.

Furthermore, the LNG supply outlook for Asian markets adds yet another layer of complexity to this picture, given India's significant dependence on Hormuz-transiting LNG cargoes.

Pipeline Asymmetry: The Infrastructure Factor Most Analysis Misses

One of the less widely understood dynamics within Gulf crude supply is that not all producers face equal Hormuz exposure. Saudi Arabia and the United Arab Emirates are the only two Gulf producers possessing pipeline infrastructure capable of moving crude to export terminals that bypass the strait entirely.

The East-West Pipeline in Saudi Arabia can carry up to 5 million barrels per day to the Red Sea port of Yanbu, while the UAE's Abu Dhabi Crude Oil Pipeline connects production fields to Fujairah on the Gulf of Oman. Bahrain, Kuwait, Iraq, and Qatar, by contrast, have no viable alternative to Hormuz transit for their crude exports. This infrastructure asymmetry transforms a geopolitical crisis into a supplier selection mechanism, automatically elevating the strategic value of Saudi and UAE barrels when tensions in the strait escalate.

From Iran Conflict to Refinery Procurement: How India's Response Unfolded

The February 2026 Trigger and Its Immediate Market Consequences

The US-Iran conflict that escalated from February 2026 onward forced Indian Oil Marketing Companies (OMCs) to move from contingency planning to active procurement restructuring almost simultaneously. The standard playbook for Indian refiners, which had long prioritised Middle Eastern crude for its cost efficiency and proximity advantages, was suddenly inadequate against a backdrop of genuine supply route uncertainty. The oil price shock that followed rippled well beyond the Gulf, reshaping procurement decisions across Asia.

The response unfolded in several distinct phases:

- Inventory assessment across major Indian refiners to quantify buffer capacity and near-term procurement requirements

- Alternative supplier identification, accelerating existing exploration of West African and Latin American crude grades

- Procurement round execution, with the Indian Oil Corporation (IOC) securing approximately 6 million barrels of crude from West African and Middle Eastern producers for April delivery as early as February

- Ongoing monitoring and adjustment, with Kpler shipping data informing real-time recalibration of the import portfolio

The IOC's February procurement round offers a revealing window into exactly which grades Indian refiners prioritised. The purchases included Angolan Pazflor and Nigerian Agbami grades secured through trading house Totsa, alongside Nigerian Akpo and Bonny Light grades acquired through Shell. The deliberate sourcing across multiple Nigerian grade types signals a structured assessment of West African crude quality rather than an opportunistic panic buy.

The Iranian Waiver: Stability Measure With Inherent Fragility

One of the less anticipated developments of the crisis period was a temporary trade waiver granted by Washington that permitted India to resume purchases of Iranian crude after a seven-year absence from that supply relationship. The waiver's stated purpose was to provide stabilisation support for global oil price benchmarks during a period of acute market stress.

However, waiver-dependent supply relationships carry structural fragility that Indian energy planners cannot ignore. A trade arrangement contingent on political discretion in Washington offers none of the contractual certainty that long-term supply agreements with African producers can provide. The Iranian waiver may have eased near-term price pressure, but it simultaneously reinforced the logic of building durable alternative supply corridors.

Iraq's Suspension and the May Recovery Signal

India's temporary suspension of Iraqi crude procurement in April 2026 added further complexity to an already shifting import landscape. Kpler's forward estimates for May 2026 projected approximately 41,000 bpd of Iraqi crude flowing to India, suggesting a partial resumption rather than a structural severance of that relationship. The Iraq disruption, however brief, accelerated the urgency of securing non-Hormuz supply relationships. The broader trade war oil impacts from ongoing geopolitical tensions further complicated India's procurement calculus during this period.

India's New Oil Geography: African and Latin American Producers Step Forward

April 2026 Import Data Across Key Suppliers

| Supplier | March 2026 (bpd) | April 2026 (bpd) | Change |

|---|---|---|---|

| United Arab Emirates | ~230,600 | ~669,700 | +190.4% |

| Saudi Arabia | ~619,500 | ~619,500 | Stable |

| Russia | ~2.27 million (est.) | ~1.6 million | -29.4% |

| Iraq | Active | Suspended | ~41,000 projected (May) |

| Nigeria | Minimal | Inaugural cargo | 950,000 barrels (Cawthorne) |

Nigeria's Cawthorne Crude: More Than a Single Cargo

The shipment that arguably captured the most symbolic significance in India's supply pivot was Nigeria's first-ever export of Cawthorne crude to Indian shores. As reported by the Economic Times, the cargo totalling 950,000 barrels was exported from the FSO Cawthorne and delivered to India's Sikka port in April 2026. The NNPC confirmed the milestone, describing the weekend export of the new Cawthorne crude grade from the vessel, with the full volume verified at 950,000 barrels, as reported by S&P Global's Platts service.

The production source matters for understanding this crude's characteristics. Cawthorne originates from Oil Mining Lease (OML) 18 in the eastern Niger Delta, operated by the Nigerian National Petroleum Company (NNPC) in partnership with Sahara Group and associated partners. OML 18 is a mature production block with historical output challenges related to pipeline sabotage and community relations in the Niger Delta, making the successful export of a new crude grade from this acreage a logistically significant achievement beyond the headline barrel count.

The strategic implication reaches further than a single shipment. When a new crude grade successfully completes its first delivery to a major Asian refiner, it establishes a commercial and logistical template. Refineries adapt their crude blending models to accommodate the grade's specific characteristics, including API gravity, sulphur content, and yield profile. Once that adaptation occurs, repeat procurement becomes progressively easier and the bilateral trade corridor gains structural durability.

The West African Crude Quality Dimension

West African crude grades, including those Nigeria and Angola export to Asian markets, generally fall into the light sweet category, characterised by low sulphur content and high yields of premium refined products such as gasoline and diesel. This quality profile holds appeal for Indian refiners whose refinery configurations are optimised for lighter crude slates.

In addition, the crude oil price analysis for West African grades relative to Middle Eastern benchmarks suggests these barrels carry competitive pricing alongside their quality advantages. Compare this to the heavier, more sour grades that have historically dominated Indian imports from certain Middle Eastern producers. The shift toward West African crude is not purely a geopolitical hedge — it carries refinery-economics logic, potentially improving product yield ratios for refiners equipped to process lighter grades efficiently.

Angola, Brazil, Venezuela: Completing the Diversification Basket

Angola contributes Pazflor grade crude to India's diversified import portfolio, sourced through trading intermediaries with established relationships in the West African market. Brazil and Venezuela round out the Latin American component of the diversification strategy, though Venezuelan procurement carries geopolitical complexity given existing US sanctions frameworks that constrain the commercial and financial mechanics of that trade relationship.

Russia's April Decline: Maintenance Cycle or Structural Shift?

The approximately 29.4% month-on-month decline in Russian crude flowing to India during April 2026 — falling to 1.6 million bpd from an estimated 2.27 million bpd in March — requires careful interpretation. Kpler's analysis attributes the drop primarily to the temporary closure of Nayara Energy's 400,000-bpd refinery for scheduled maintenance operations, a planned operational event rather than a policy-driven or geopolitically motivated reduction.

Forward estimates for May 2026 projected Russian volumes recovering to approximately 1.9 million bpd, broadly consistent with the maintenance-cycle explanation. However, the February 2026 context adds an additional layer. India's Africa pivot was partly framed around the desire to reduce Russian supply concentration, suggesting that even as Russian volumes recover, Indian OMCs are likely to maintain elevated African and Latin American procurement as a deliberate diversification overlay.

The UAE Surge: Pipeline Infrastructure as Crisis Alpha

The most striking single data point in India's April 2026 import profile is the 190.4% surge in UAE crude volumes, rising from approximately 230,600 bpd in March to 669,700 bpd in April. This is not a coincidence of market timing. It is a direct expression of the pipeline infrastructure advantage that makes UAE barrels uniquely attractive when Hormuz anxiety is elevated.

The broader OPEC consequence of this reorientation is significant. OPEC's collective share of Indian crude imports expanded from approximately 30% in March to 45.2% in April 2026, driven overwhelmingly by the UAE volume surge. Consequently, this represents a counterintuitive outcome: a Hormuz crisis that might have been expected to reduce Gulf supplier dominance actually increased OPEC's share because the crisis selectively elevated the two Gulf producers capable of bypassing the troubled corridor.

The next major ASX story will hit our subscribers first

Scenario Analysis: Three Pathways for India's Energy Supply Architecture

Scenario 1: Short Disruption, Managed Return

Hormuz tensions de-escalate within three to six months. Middle Eastern procurement normalises, African and Latin American suppliers retain an elevated but minority share of India's import basket, and the crisis is absorbed as an accelerant of diversification trends already underway rather than a structural rupture.

Scenario 2: Prolonged Instability and Formalised New Corridors

Hormuz tensions persist beyond twelve months, prompting Indian OMCs to formalise long-term supply agreements with Nigerian, Angolan, and Brazilian producers. Bilateral energy frameworks are negotiated at the governmental level, transforming what began as a crisis response into an institutionalised component of India's energy security architecture. Freight cost pressures intensify, creating incentives for investment in logistics optimisation and strategic petroleum reserve expansion.

Scenario 3: Escalation and Emergency Protocol Activation

A sustained or complete Hormuz closure triggers emergency responses across major Asian importers simultaneously. India draws down strategic petroleum reserves while accelerating renewable energy deployment timelines. Global crude prices spike, creating a demand surge for African and Latin American barrels that tests the export infrastructure capacity of those producers at scale.

Disclaimer: The scenarios described above represent analytical projections based on current market conditions and geopolitical trajectories. They do not constitute investment advice or price forecasts. Energy market outcomes depend on variables that are inherently unpredictable.

Africa's Structural Opportunity in Asia's Energy Rebalancing

The longer-term significance of India's supply pivot extends beyond bilateral trade statistics. Africa's oil producers, led by Nigeria and Angola, are increasingly positioned as credible swing suppliers capable of filling demand gaps created by geopolitical disruptions in other producing regions. The continent's crude exports carry a fundamental geographic advantage: they do not transit the Strait of Hormuz, making them inherently resilient supply options for any Asian importer seeking Hormuz-independent barrels.

The infrastructure challenge, however, is real and should not be underestimated. African export capacity, port logistics, floating storage systems, and upstream production reliability must scale meaningfully to absorb sustained demand increases from Asian importers. Nigeria's Niger Delta production environment, in particular, has historically been vulnerable to operational disruptions from pipeline vandalism, community disputes, and regulatory complexity.

The development of large-scale domestic refining infrastructure on the continent adds another dimension to this picture. As African refining capacity matures, the continent's producers face a strategic choice between maximising crude export volumes to Asian buyers and retaining more crude value domestically through refined product production. How Nigeria and Angola navigate this tension will shape the trajectory of their roles in India's long-term import portfolio.

Key Takeaways: What India's Supply Pivot Reveals About Global Energy Resilience

- The Strait of Hormuz crisis has accelerated a diversification strategy that Indian energy planners had been contemplating for years, compressing a gradual transition into a matter of months

- Africa, led by Nigeria and Angola, has demonstrated credibility as a structurally significant alternative crude source capable of delivering meaningful volumes to major Asian importers

- The UAE's pipeline bypass infrastructure made it the standout Gulf supplier during the crisis period, with volumes surging nearly 190% month on month

- Russia's reduced April share appears maintenance-driven, with May volumes projected to recover to approximately 1.9 million bpd, suggesting no structural severance of that relationship

- India's total oil imports of 4.57 million bpd in April 2026 held stable relative to March, demonstrating effective near-term supply continuity management

- The 15.5% year-on-year decline in total Indian crude imports warrants ongoing monitoring as a potential indicator of demand softness, inventory management, or refinery utilisation dynamics

- Longer shipping distances from Africa and Latin America introduce freight cost premiums and elevated insurance costs that carry direct implications for India's energy import bill and INR stability

Monitoring the current crude oil prices across these newly activated trade corridors will be essential for assessing whether India's diversification strategy is delivering genuine cost competitiveness alongside supply security.

Frequently Asked Questions

Why is the Strait of Hormuz so critical to India's energy security?

The strait serves as the primary maritime transit route for approximately 50% of India's crude oil imports and 54% of its LNG imports, meaning any sustained disruption immediately threatens national energy supply continuity and creates downstream pressure across LPG supply, gas generation, fertiliser production, and agricultural cost structures.

Which African countries are currently supplying oil to India?

Nigeria and Angola are the primary African contributors to India's diversified import basket. Nigeria shipped its first-ever Cawthorne crude cargo, totalling 950,000 barrels, to India's Sikka port in April 2026, while Angola's Pazflor grade has been secured through trading intermediaries including Totsa.

What drove the UAE's dramatic import volume increase in April 2026?

The UAE's pipeline infrastructure connecting its production fields to the Gulf of Oman port of Fujairah allows crude exports that bypass the Strait of Hormuz entirely. This structural advantage made UAE barrels uniquely attractive to Indian refiners during a period of elevated Hormuz risk, driving volumes from approximately 230,600 bpd in March to 669,700 bpd in April.

Could India's African and Latin American oil sourcing become a permanent feature?

While the immediate pivot was crisis-driven, the establishment of new bilateral trade corridors — particularly Nigeria's inaugural Cawthorne crude delivery to India — creates commercial and logistical templates that typically outlast their triggering events. The probability of these relationships persisting beyond the current disruption period is meaningfully higher than a purely opportunistic reading of the data would suggest. India turns to African and Latin American oil after Strait of Hormuz disruption not merely as a short-term fix, but as the foundation of a more resilient long-term energy architecture.

Want to Know Which ASX Resource Companies Are Positioned for Africa's Growing Energy Role?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities in the commodities reshaping global energy supply chains — including those tied to Africa's expanding role as a swing producer. Start your 14-day free trial today, or explore Discovery Alert's discoveries page to understand how major resource discoveries have historically generated substantial market returns.