June 23, 2026

The Structural Trap: Why India Exports Raw Metal While China Exports Wealth

There is a well-documented pattern in economic history where resource-rich nations fail to capture the full value of their natural endowments. They extract, refine to a basic level, and export. Downstream processing, employment multiplication, and technological upgrading happen elsewhere. For decades, this pattern defined commodity exporters across Africa, Latin America, and Southeast Asia.

The uncomfortable question now facing India's aluminium sector is whether the country is falling into the same structural trap, and whether its current trade policy architecture is actively reinforcing it.

The India aluminium export duty proposal, advanced by the Global Trade Research Initiative (GTRI), is best understood not as a narrow tax measure but as a diagnostic response to a deeper industrial policy failure. Two parallel conversations are happening simultaneously: one about fixing domestic tariff distortions, and one about how India responds to escalating U.S. aluminium tariffs on metal imports. Together, they define a critical inflection point for India's aluminium sector through 2025 and beyond.

When big ASX news breaks, our subscribers know first

Understanding the Inverted Duty Problem at the Heart of India's Aluminium Supply Chain

Before evaluating any reform proposal, it is essential to understand what an inverted duty structure actually means in practice. In a well-designed tariff architecture, duties on raw materials are lower than duties on intermediate goods, which are in turn lower than duties on finished products. This gradient protects domestic manufacturers at each stage of processing, giving them a cost advantage over importers of more sophisticated goods.

India's current aluminium tariff framework inverts this logic in several damaging ways. The 7.5% basic customs duty on unwrought aluminium raises input costs for domestic manufacturers who need primary metal as a raw material. Meanwhile, finished aluminium products can enter India through free trade agreement (FTA) routes at zero or near-zero duty rates, allowing foreign producers to undercut local manufacturers on price.

The result is a system that simultaneously taxes domestic processors on their inputs while offering no protection against finished product competition. Furthermore, as global bauxite production dynamics shift, India's policy misalignment becomes increasingly costly.

India's Existing Aluminium Tariff Architecture

| Tariff Category | Current Rate | Policy Problem Identified |

|---|---|---|

| Basic Customs Duty on Unwrought Aluminium | 7.5% | Raises input costs for domestic manufacturers |

| Finished Aluminium Products via FTA routes | 0% or near-zero | Allows cheaper imports to undercut local producers |

| Export Duty on Primary Aluminium | None (proposed: 20%) | Incentivises raw metal exports over domestic supply |

| Industry Demand for Import Duty Protection | ~15% (proposed) | Not yet confirmed as government policy |

The absence of an export duty on primary aluminium compounds the problem. With no financial disincentive to exporting raw metal, Indian primary producers face stronger economic signals to sell internationally than to supply domestic manufacturers. This is not a market failure in the traditional sense; it is a policy-induced distortion operating exactly as its architecture dictates.

A Four-Pillar Reform Framework: What the GTRI Proposals Actually Involve

The GTRI reform agenda rests on four interconnected proposals that collectively aim to realign India's tariff architecture with its industrial objectives. Each pillar addresses a distinct dimension of the problem.

- Remove the 7.5% customs duty on unwrought aluminium imports to give domestic manufacturers access to primary metal at globally competitive prices, eliminating a structural cost disadvantage

- Introduce a 20% export levy on primary aluminium to redirect metal supply toward domestic industrial users and create a financial disincentive for exporting raw, low-value metal

- Enforce a progressive tariff ladder where duties on raw materials are consistently lower than those applied to intermediate and finished goods, restoring logical tariff graduation

- Conduct a targeted FTA audit to close provisions that currently allow finished aluminium products to enter India at preferential or zero-duty rates, removing the competitive asymmetry faced by domestic processors

What is notable about this framework is its internal coherence. Each measure reinforces the others. Removing input duties lowers costs for manufacturers. Introducing an export duty redirects raw metal supply toward those same manufacturers. Fixing the tariff ladder ensures the gradient incentivises processing rather than raw exports. Closing FTA loopholes ensures that the resulting cost advantages for domestic producers are not immediately eroded by cheaper finished imports.

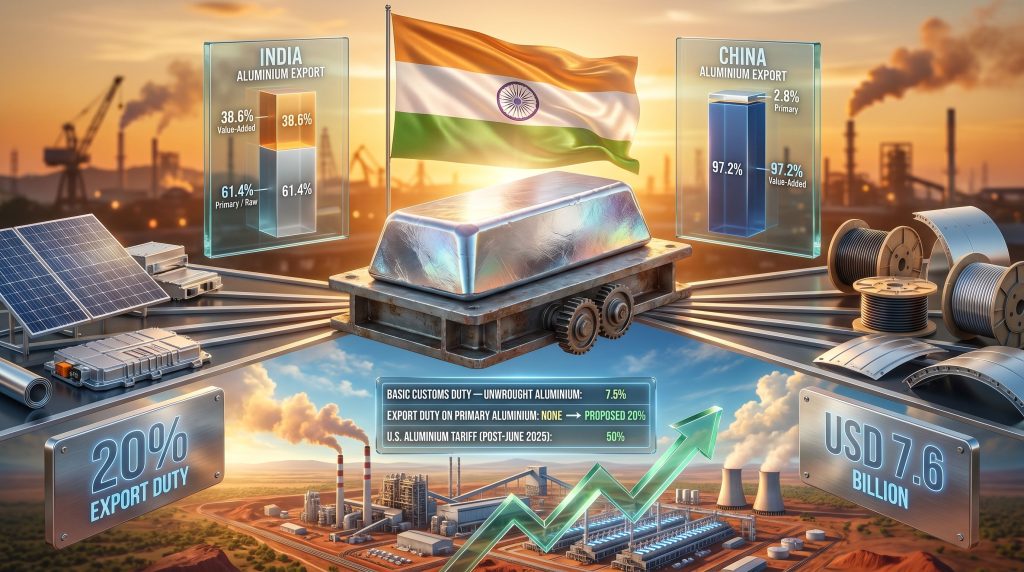

India vs. China: A Structural Comparison That Reveals the Stakes

The contrast between India's aluminium export profile and China's is not simply a difference in scale. It reflects fundamentally different industrial policy philosophies that have compounded over decades into dramatically different economic outcomes. In addition, the global tariff impact of recent U.S. trade measures has accelerated the urgency of India's own structural reform debate.

India vs. China Aluminium Export Composition (2025-26)

| Metric | India (2025-26) | China (2025-26) |

|---|---|---|

| Total Aluminium Export Value | ~USD 7 billion | ~USD 42.5 billion |

| Primary/Raw Aluminium Share | ~61.4% | ~2.8% |

| Value-Added Products Share | ~38.6% | ~97.2% |

| Export Duty on Aluminium Ingots | None (proposed: 20%) | 30% |

These figures reveal a structural divergence that goes well beyond production capacity. China's 97.2% value-added export share is the cumulative result of deliberate policy choices sustained over many years, including a 30% export duty on aluminium ingots that creates powerful financial incentives to process metal domestically rather than ship it raw. India's 61.4% raw metal export share represents the inverse outcome: a policy environment that has consistently under-incentivised downstream processing.

"The economic cost of exporting raw aluminium rather than finished products is not simply the difference in unit price. It includes foregone manufacturing employment, reduced investment in processing technology, weaker development of supplier ecosystems, and diminished export earnings growth potential over time."

It is worth noting that China's model is not without complexity. Its dominance in value-added aluminium exports has generated significant trade friction globally, and the strategic use of export taxes to direct resource allocation raises questions under WTO frameworks. India would need to design its own approach carefully, drawing on the underlying logic without replicating the specific mechanisms that have drawn international scrutiny.

The WTO Dimension: India's Retaliation Position on U.S. Aluminium Tariffs

Running parallel to the domestic reform conversation is a trade diplomacy challenge of considerable magnitude. The United States escalated its aluminium import tariff to 50% effective June 4, 2025, building on earlier measures under Section 232 of the Trade Expansion Act. This escalation has placed significant pressure on Indian aluminium exporters with exposure to the U.S. market. Consequently, the broader implications of steel and aluminum tariffs introduced under the Trump administration continue to reverberate through global supply chains.

India's WTO Retaliation Framework: Key Metrics

| Parameter | Estimated Figure |

|---|---|

| Indian exports affected by U.S. steel and aluminium measures | ~USD 7.6 billion |

| Estimated duty collection impact on Indian exporters | ~USD 1.91 billion |

| U.S. aluminium tariff rate (post-June 2025 escalation) | 50% |

| India's WTO notification status | Filed, retaliation measures under consideration |

India has formally notified the WTO of its intention to consider retaliatory measures, identifying approximately USD 7.6 billion in affected exports and estimating a duty collection impact of around USD 1.91 billion on Indian exporters. According to Reuters reporting on small exporters, smaller Indian businesses are also seeking import duty reductions to help counter these U.S. measures. This notification establishes the legal basis for countermeasures under WTO dispute settlement rules, but converting a notification into actual retaliatory tariffs involves strategic calculations that go well beyond the legal framework.

India faces a genuine strategic dilemma here. Retaliatory escalation risks further damaging bilateral trade relations at a time when India and the United States are actively pursuing a broader trade agreement. Alternatively, Indian exporters are exploring whether lowering import tariffs on selected U.S. goods could serve as a negotiating concession to secure relief from the aluminium measures. Neither path is cost-free, and the outcome will likely depend on the trajectory of wider India-U.S. trade negotiations rather than the aluminium issue in isolation.

Aluminium's Strategic Position in India's Industrial Transition

One dimension of this debate that receives insufficient attention is the opportunity cost of the current policy framework measured against India's own stated industrial priorities. Aluminium is not a peripheral commodity. It is structurally embedded across virtually every major growth sector in India's economy.

Key sectors dependent on domestic aluminium supply include:

- Power transmission infrastructure, where aluminium conductors are the dominant technology for long-distance high-voltage lines

- Renewable energy installations, particularly solar mounting systems and wind turbine components

- Electric vehicles, where aluminium's weight-to-strength ratio is critical for battery housing, chassis components, and body panels

- Aerospace and defence manufacturing, where India's indigenisation ambitions require domestic supply chains for structural aluminium

- Rail and metro infrastructure, where lightweight aluminium carriages are increasingly specified

- Packaging and consumer goods, a large-volume application supporting both food security and export competitiveness

India holds significant natural advantages in aluminium production: substantial bauxite reserves, integrated refining and smelting capacity, and access to relatively low-cost power in key production regions. The gap between these endowments and the economic value actually captured represents a policy-induced underperformance that the reform agenda is designed to address. Furthermore, major aluminium industry leaders globally have demonstrated that integrated processing strategies consistently outperform raw export models over the long term.

The next major ASX story will hit our subscribers first

The Employment and Investment Case for Structural Reform

The economic argument for retaining more aluminium within India for domestic processing is not solely about export composition statistics. Manufacturing value-added products generates substantially more employment per tonne of aluminium processed than simply smelting and exporting primary metal. The multiplier effect through component manufacturing, fabrication, assembly, and associated supply chains is considerably larger for finished products than for raw metal exports.

Investment dynamics compound this effect over time. When downstream processors face structural cost disadvantages due to inverted duties and unreliable domestic supply, they reduce capital expenditure, delay capacity expansion, and in some cases source finished products from imports rather than investing in domestic production. This creates a self-reinforcing cycle where weak downstream investment reduces demand for domestic primary aluminium, which in turn reduces the incentive for primary producers to prioritise domestic supply.

The introduction of the India aluminium export duty proposal at a 20% rate would interrupt this cycle by making international sales of primary aluminium less financially attractive relative to domestic supply. Primary producers would face margin compression on export sales, creating an incentive to redirect metal toward domestic buyers at negotiated prices. Over time, this supply redirection would support lower input costs for downstream manufacturers, stimulate processing investment, and gradually shift India's export composition toward higher-value finished products. The Business Standard's analysis of India's raw aluminium exports similarly highlights how the current tariff structure actively hinders domestic manufacturing ambitions.

Frequently Asked Questions: India Aluminium Export Duty Proposal

What exactly is the proposed aluminium export duty in India?

The proposal, advanced by GTRI, calls for a 20% export duty on primary aluminium metal. The intention is to make exporting raw aluminium financially less attractive, thereby redirecting supply toward domestic manufacturers who need the metal as an input for value-added production.

Is the 20% export duty on aluminium a confirmed government policy?

No. As of the time of writing, this remains a policy recommendation from a research and trade policy organisation. It has not been formally adopted or announced as government policy by Indian authorities.

How does India's proposed export duty compare to China's approach?

China currently applies a 30% export duty on aluminium ingots, a longstanding measure that has been instrumental in directing primary aluminium supply toward domestic manufacturers. The proposed Indian rate of 20% is directionally similar but set at a lower level.

What is India's WTO position on U.S. aluminium tariffs?

India has filed a WTO notification identifying approximately USD 7.6 billion in exports affected by U.S. steel and aluminium tariff measures and estimating a duty impact of around USD 1.91 billion. Retaliatory countermeasures are under consideration but have not been formally implemented.

What is an inverted duty structure?

An inverted duty structure exists when tariffs on raw material inputs are higher than tariffs on finished goods. This penalises domestic manufacturers by raising their input costs while simultaneously allowing finished product imports to undercut their prices in the domestic market.

Policy Benchmarks and Implementation Considerations

Designing an effective export duty requires more than simply selecting a percentage rate. Several implementation variables will determine whether the measure achieves its industrial policy objectives or produces unintended consequences.

Key design considerations include:

- Exemption frameworks: Whether certain end-uses, such as exports of processed products or supply to designated manufacturing zones, qualify for duty exemptions or rebates

- Phase-in timelines: Primary producers will require adjustment periods to reorient commercial relationships and supply chain logistics away from established export customers

- Monitoring mechanisms: Ensuring that the duty achieves domestic supply redirection rather than simply being absorbed as a cost by producers with limited flexibility

- FTA compatibility: Careful legal review of existing FTA obligations to ensure the export duty does not conflict with treaty commitments in ways that could trigger dispute proceedings

Policy Proposals, Objectives, and Expected Outcomes

| Policy Proposal | Primary Objective | Expected Outcome |

|---|---|---|

| Remove 7.5% duty on unwrought aluminium | Lower input costs for manufacturers | Improved downstream competitiveness |

| Introduce 20% export duty on primary aluminium | Redirect raw metal to domestic users | Shift export mix toward value-added products |

| Enforce progressive tariff ladder | Correct inverted duty structure | Stronger domestic supply chain incentives |

| Review FTA zero-duty provisions | Protect domestic finished product manufacturers | Reduced import competition for local processors |

| WTO retaliation framework (U.S. tariffs) | Counter U.S. 50% aluminium import tariff | Negotiating leverage in bilateral trade talks |

Disclaimer: This article contains forward-looking analysis, policy projections, and scenario assessments. These represent analytical perspectives based on available information and do not constitute investment, financial, or legal advice. Policy proposals discussed herein have not been confirmed as enacted government measures. Readers should consult authoritative government and regulatory sources for the most current policy status.

The central question facing Indian policymakers is whether the country will continue exporting the raw material of its own industrial ambitions, or whether it will implement the structural corrections needed to retain and compound the value of its aluminium endowments domestically. The India aluminium export duty proposal provides a coherent analytical basis for that transition. However, what remains is the political economy of execution — and that may prove to be the most challenging variable of all.

Want to Track the Next Major ASX Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, converting complex mineral data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.