June 22, 2026

The Chemistry of Geopolitics: Why Platinum Group Metals Are at the Heart of the Global Hydrogen Race

The global energy transition has a materials problem that rarely makes front-page news. Hydrogen fuel cells, widely celebrated as a cornerstone technology for decarbonising transport and industry, depend on a group of precious metals so rare and geographically concentrated that their supply chains are inherently geopolitical. Platinum group metals (PGMs) sit at the intersection of electrochemistry, clean energy infrastructure, and national economic strategy in ways that most investors and policymakers are only beginning to fully appreciate.

Understanding this dynamic helps explain why a working visit by South Africa's Deputy President Paul Mashatile to China in June 2026, focused specifically on hydrogen fuel cell technologies, carries implications that extend well beyond diplomatic formality. The South Africa Deputy President hydrogen fuel cell visit to China touches on one of the most structurally significant commodity relationships of the next decade.

When big ASX news breaks, our subscribers know first

PGMs and the Electrochemistry That Connects Two Nations

South Africa holds the world's most concentrated reserves of platinum group metals, producing the substantial majority of global platinum and significant shares of palladium, rhodium, ruthenium, and iridium. China, meanwhile, represents the single largest consuming nation for these metals across multiple end-use categories. That pairing creates a structural interdependency that underpins the entire hydrogen fuel cell value chain. For more on platinum and palladium dynamics, these shifts are reshaping investment strategies globally.

The connection is rooted in chemistry. Green hydrogen is produced through a process called proton exchange membrane (PEM) electrolysis, which splits water molecules into hydrogen and oxygen using electricity generated from renewable sources. The membranes within PEM electrolysers require platinum and iridium as catalysts to function efficiently. Without PGM catalysts, the electrochemical reaction either cannot proceed or operates at unacceptable efficiency losses.

The relationship continues on the other side of the hydrogen economy. When stored hydrogen is converted back into electricity inside a fuel cell, the proton exchange membrane again requires platinum-group catalysts, particularly platinum, to facilitate the reaction between hydrogen and oxygen. This dual role — enabling both the production of green hydrogen through electrolysis and the generation of electricity through fuel cells — means that PGMs are embedded twice in the hydrogen value chain. PEM technology expansion is, furthermore, accelerating the pace at which these catalysts will be required at scale.

A less widely appreciated fact is that iridium, one of the rarest elements on Earth, is arguably more critical than platinum in PEM electrolysis. Global iridium supply is measured in just a few tonnes per year, almost all of it recovered as a byproduct of platinum mining in South Africa. Any large-scale PEM electrolyser buildout confronts an iridium supply ceiling that the industry has not yet resolved at commercial scale.

No commercially viable substitute for PGM catalysts currently exists in proton exchange membrane systems. Alternative catalyst research, including work on non-precious metal and single-atom catalysts, remains at laboratory or early pilot stages and has not demonstrated the durability required for commercial deployment in transport or industrial applications.

The International Hydrogen Fuel Cell Association and Its Significance

Deputy President Mashatile's delegation met with the International Hydrogen Fuel Cell Association (IHFCA), the leading institutional body in China responsible for coordinating hydrogen policy, setting technical standards, and facilitating commercial deployment of fuel cell technologies. Secretary-General Wang Ju leads the organisation, which functions as a bridge between government policy priorities and the commercial hydrogen sector across China.

The IHFCA's influence extends into vehicle certification, infrastructure standards for hydrogen refuelling, and the technical frameworks that govern fuel cell system procurement. For South Africa, engaging directly with this institution signals an intent to position itself not merely as a raw material supplier, but as a participant in the broader value architecture that China is constructing around hydrogen energy.

The delegation also included Deputy Minister of Trade, Industry and Competition Zuko Godlimpi, whose portfolio directly relates to supply chain integration, industrial investment attraction, and trade policy alignment — all of which are relevant to South Africa's ambition to deepen its hydrogen economy engagement with Chinese counterparts.

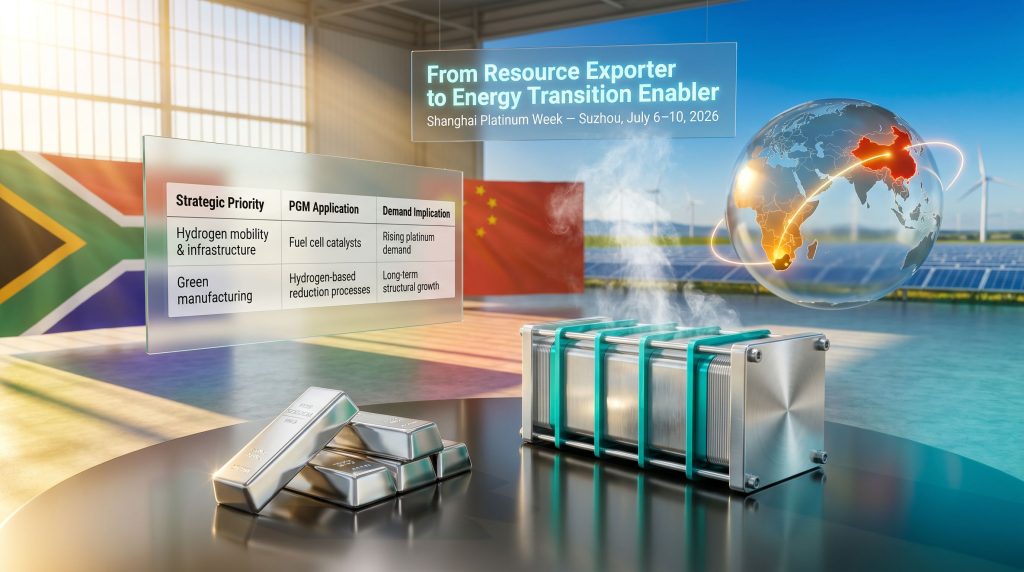

China's 15th Five-Year Plan: A Structural Demand Signal for PGMs

China's 15th Five-Year Plan, covering the period to 2030, embeds hydrogen and artificial intelligence as twin national priorities alongside carbon reduction and environmental protection. For the PGM market, this is a materially significant policy signal because all four priority areas create demand for platinum group metals through different mechanisms.

| Strategic Priority | PGM Application | Demand Implication |

|---|---|---|

| Hydrogen mobility and infrastructure | Fuel cell catalysts (platinum) | Rising structural demand |

| AI data centre expansion | Semiconductors, PCBs, sensors, optical interconnects | Emerging new end-use market |

| Carbon reduction and environmental compliance | Catalytic converters and industrial catalysis | Sustained baseline demand |

| Green manufacturing (steel, cement, chemicals) | Hydrogen-based industrial reduction processes | Long-term structural growth |

The AI dimension is particularly underappreciated by commodity markets. PGMs possess distinctive catalytic, thermal, and electrical properties that make them useful across the hardware stack that supports AI infrastructure, including data storage components, advanced sensor systems, and high-reliability circuit boards. As the World Platinum Investment Council has noted through its 60 Seconds In Platinum publication, AI is rapidly emerging as a new and growing end-use category for PGMs, with demand spanning multiple hardware and energy supply applications within data centres.

This multi-vector demand picture distinguishes the current demand environment from prior cycles where automotive catalytic converters dominated the PGM demand narrative. In addition, critical minerals demand continues to intensify as clean energy policy commitments deepen across major economies.

BYD, Commercial Vehicles, and the Validation of Near-Term Fuel Cell Demand

On the commercial deployment front, China's largest electric vehicle manufacturer BYD has moved into the hydrogen fuel cell space in ways that indicate genuine near-term market development rather than speculative positioning. Filings with China's Ministry of Industry and Information Technology have confirmed that BYD is supplying its own proprietary hydrogen fuel cell systems to power two new commercial vehicle platforms: a fuel cell refrigerated truck and a heavy-duty fuel cell cargo vehicle.

This is industrially significant for several reasons:

- Heavy-duty transport applications place higher demands on fuel cell durability than passenger vehicles, validating the technology at a more rigorous operational level

- Refrigerated logistics is a sector where battery electric alternatives face genuine range and payload constraints, making hydrogen a technically competitive option

- BYD's involvement brings manufacturing scale and supply chain integration capabilities that smaller fuel cell specialists cannot match

- Ministry of Industry and Information Technology filings represent formal commercial readiness documentation, not prototype announcements

The broader pattern in China is that heavy-duty commercial vehicles, rather than passenger cars, are proving to be the leading edge of hydrogen fuel cell commercialisation. This aligns with the physics: hydrogen's gravimetric energy density advantage over battery technology is most valuable in high-payload, long-range applications where battery weight becomes a significant operational constraint.

South Africa's Green Hydrogen Competitive Position

The working visit also advanced discussion around South Africa's potential as a green hydrogen production hub, a proposition grounded in several intersecting resource and infrastructure factors.

South Africa's renewable energy endowment is frequently cited, but the specific combination of attributes that matter for green hydrogen economics is less often examined. The cost of green hydrogen is dominated by the cost of renewable electricity input, meaning that regions with the highest solar irradiance, strongest wind resources, and lowest land costs hold a structural cost advantage at scale.

South Africa's northern Cape region in particular offers solar irradiance levels among the highest globally, while its coastal and interior zones offer strong and consistent wind resources. Critically, the country also possesses large tracts of available land where gigawatt-scale hydrogen production facilities can be co-located with solar photovoltaic plants and wind turbines, enabling integrated project development at a scale that more densely populated or topographically constrained nations cannot easily replicate.

Liquid Organic Hydrogen Carriers (LOHC) represent another dimension of South Africa's potential advantage. LOHC technology enables hydrogen to be stored and transported using existing liquid fuel infrastructure, including pipelines, tankers, and storage terminals, by chemically bonding hydrogen to a carrier liquid such as dibenzyltoluene. This significantly reduces the capital cost of hydrogen export logistics compared to cryogenic liquid hydrogen or compressed gas alternatives, and South Africa's existing port infrastructure at Durban, Richards Bay, and Saldanha Bay could potentially be repurposed for LOHC export operations.

Green hydrogen also connects to industrial decarbonisation pathways that are directly relevant to South Africa's existing heavy industry base. Consequently, energy transition mining strategies are increasingly shaped by these industrial hydrogen applications:

- Green steel: Replacing coking coal with hydrogen in direct reduction iron processes

- Green cement: Hydrogen combustion as a thermal replacement for fossil fuels in kiln operations

- Green chemicals: Hydrogen as a feedstock for ammonia, methanol, and other industrial chemicals

Furthermore, the green steel market dynamics are evolving rapidly as South Africa positions itself within the global hydrogen-to-steel value chain.

The next major ASX story will hit our subscribers first

The Four Pillars of South Africa's Engagement Agenda

The objectives pursued through the Mashatile delegation's China engagements can be understood through four distinct but interconnected priorities:

- Technology transfer: Acquiring access to hydrogen fuel cell manufacturing knowledge and electrolyser technology to build domestic industrial capability rather than remaining a pure raw material exporter

- Skills development: Closing the human capital gap that would constrain South Africa's ability to operate and maintain hydrogen infrastructure at commercial scale

- Industrial investment attraction: Positioning South Africa as a destination for Chinese capital investment in green hydrogen production and processing facilities

- Trade facilitation: Aligning PGM supply chain relationships with China's clean energy procurement requirements, moving from spot commodity trading toward longer-term strategic supply arrangements

The timing of the South Africa Deputy President hydrogen fuel cell visit to China, relative to Shanghai Platinum Week scheduled in Suzhou from July 6 to 10, 2026, is unlikely to be coincidental. Since 2021, this gathering has progressively become the most significant annual forum connecting PGM supply chain stakeholders with end-use market participants across Asia. Diplomatic groundwork laid in June creates the conditions for more substantive commercial conversations at the July event.

Energy Resilience and the Long-Duration Storage Advantage

Beyond export economics, hydrogen carries specific strategic value for South Africa's domestic energy security calculus. The country's experience with electricity supply instability over the preceding decade has reinforced the case for energy storage solutions that can buffer supply disruptions across extended periods.

Hydrogen's key differentiator relative to battery storage is time-scale. Lithium-ion batteries are well suited to intraday energy balancing, managing hourly or sub-hourly fluctuations in renewable generation. Hydrogen, however, can be stored for weeks, months, or potentially longer without meaningful energy loss, making it a candidate for seasonal balancing where summer solar generation is stored and dispatched during winter demand peaks. No battery chemistry currently operates competitively in this multi-week to multi-month storage window.

Combined with LOHC storage technology, which allows hydrogen to be stored safely at ambient temperature and pressure using existing liquid infrastructure, South Africa's hydrogen economy could serve both domestic energy resilience objectives and international export ambitions simultaneously.

Frequently Asked Questions

What role do platinum group metals play in hydrogen fuel cells?

Platinum group metals, primarily platinum and iridium, serve as catalysts in proton exchange membrane fuel cells and electrolysers. They enable the electrochemical reactions that either produce hydrogen from water or generate electricity from hydrogen, and no commercially scalable alternatives currently exist.

Why is China the most important market for South African PGMs?

China is the world's largest single consumer of PGMs across automotive, industrial, electronics, and now hydrogen applications. Its 15th Five-Year Plan further embeds PGM-dependent technologies as national priorities, making demand growth structurally driven rather than cyclical.

What is the International Hydrogen Fuel Cell Association?

The IHFCA is China's primary institutional body for hydrogen and fuel cell technology policy, standards development, and commercial deployment coordination. It plays a central role in shaping how hydrogen technology is adopted and regulated across Chinese industry.

How does green hydrogen differ from grey or blue hydrogen?

Grey hydrogen is produced from natural gas via steam methane reforming without carbon capture, generating significant CO2 emissions. Blue hydrogen uses the same process but captures and stores the CO2. Green hydrogen is produced through electrolysis powered by renewable electricity, resulting in near-zero lifecycle emissions.

What is liquid organic hydrogen carrier technology?

LOHC technology chemically bonds hydrogen to a carrier liquid, enabling storage and transport at ambient conditions using conventional liquid fuel infrastructure. The hydrogen is later released through a dehydrogenation process at the point of use.

What was the outcome of Deputy President Mashatile's hydrogen-related meetings in China?

The meetings focused on advancing technology transfer, building South African manufacturing capabilities in the hydrogen and fuel cell sector, supporting skills development, and strengthening bilateral trade and investment relationships relevant to PGMs and green hydrogen. The South Africa Deputy President hydrogen fuel cell visit to China has, consequently, set the stage for deeper commercial and industrial collaboration in the years ahead.

Key Takeaways for Industry Stakeholders

- South Africa's diplomatic engagement with China's hydrogen institutions represents a deliberate effort to move up the PGM value chain from raw material extraction toward technology-integrated partnership

- China's 15th Five-Year Plan creates structural, policy-embedded demand for PGMs across hydrogen, AI infrastructure, environmental compliance, and green manufacturing simultaneously

- BYD's commercial fuel cell vehicle filings confirm that near-term fuel cell catalyst demand is real and advancing in heavy-duty transport applications

- Iridium supply constraints represent a less-discussed but potentially binding bottleneck in any large-scale PEM electrolyser buildout globally

- South Africa's solar irradiance, wind resources, land availability, and existing port infrastructure provide a credible cost and logistics foundation for green hydrogen production and export at gigawatt scale

- The convergence of the Mashatile China visit with Shanghai Platinum Week in Suzhou in July 2026 reflects deliberate diplomatic timing designed to support commercial outcomes

This article contains forward-looking statements and strategic assessments based on publicly available information. Projections regarding demand growth, technology deployment timelines, and investment outcomes are inherently uncertain and should not be construed as financial advice. Readers are encouraged to conduct independent research before making investment decisions.

Want to Track the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including those tied to platinum group metals and the critical commodities driving the global energy transition — and translating complex data into actionable investment insights. Explore historic discoveries and their exceptional market returns, then begin your 14-day free trial to position yourself ahead of the broader market.