June 26, 2026

The Global Steel Glut That Pushed India Toward a Multi-Front Trade Defence

When a commodity market develops chronic oversupply, the pressure does not disappear — it migrates. Excess steel production from capital-intensive mills in China, Japan, and Russia does not simply sit idle; it searches for markets where it can be sold at marginal cost, often below what domestic producers in destination countries can competitively match. India, as one of the world's fastest-growing steel consumers and an increasingly ambitious domestic producer, has become a prime destination for this displaced volume. The resulting collision between low-cost imported material and domestically produced steel has pushed Indian trade policy into a new phase — one defined by layered, systematic, and escalating protection measures.

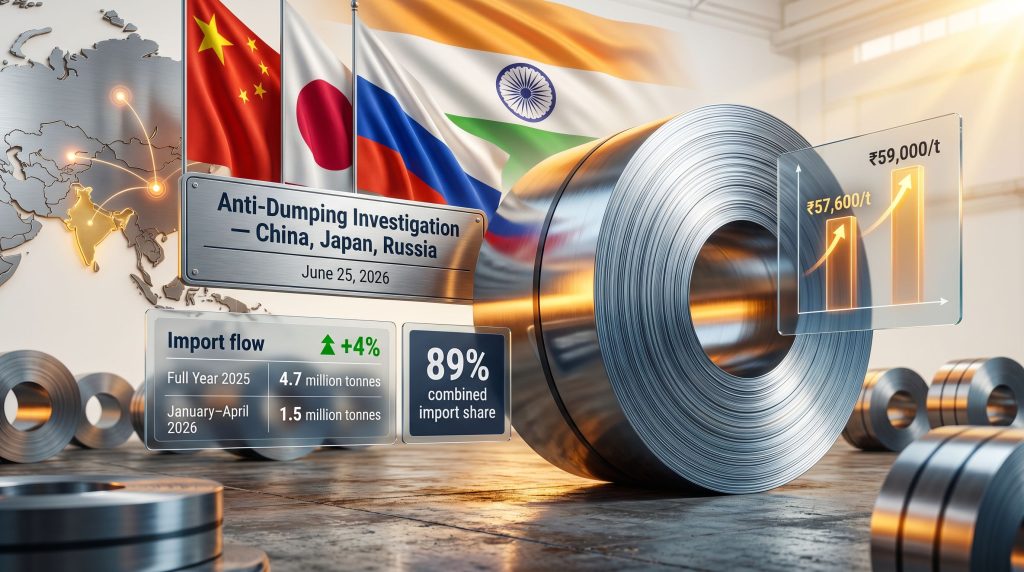

The India anti-dumping probe into hot-rolled steel imports launched on June 25, 2026, targeting exports from China, Japan, and Russia, is the latest and arguably most consequential action in this ongoing policy evolution. To understand what it means for Asian exporters, Indian consumers, and flat steel pricing, it is necessary to trace the structural forces that made this investigation inevitable.

When big ASX news breaks, our subscribers know first

How India's Flat Steel Market Became a Contested Battleground

The Mechanics of Global Oversupply and Import Displacement

Steel is a capital-intensive industry with high fixed costs and significant political sensitivity in most producing nations. When domestic demand in a major steel economy weakens, mills face a binary choice: reduce output at significant financial cost or redirect production toward export markets. China, the world's largest steel producer by an enormous margin — responsible for roughly 57% of global steel output — faced precisely this situation as its property sector decelerated sharply after 2021.

The consequence was a surge in Chinese flat steel exports to emerging market economies with fewer trade barriers. India, with its large infrastructure pipeline, growing manufacturing base, and historically open import environment, absorbed a disproportionate share of this redirected volume. Japanese and Russian mills, facing their own demand headwinds and market access constraints in Western economies, followed a similar export redirection logic.

India's domestic steel industry — led by privately owned integrated mills and a growing number of secondary producers — found itself competing against material priced at or near marginal production cost, a structurally unfair comparison given that Indian producers must recover their full capital and operating cost base from domestic sales.

India's Trade Defence Escalation: A Chronological Framework

What makes the current situation analytically significant is the speed and breadth of India's trade defence escalation over a compressed period. Furthermore, the China steel market dynamics have played a central role in driving this escalation:

- 2023–2024: Finished steel imports climbed consistently, driven by global surplus and weak demand across key producing economies

- April 2025: India imposed provisional safeguard duties across a broad range of steel import categories

- December 2025: A three-year extension of safeguard measures was confirmed, signalling a structural rather than temporary policy commitment

- August 2024: Anti-dumping investigation initiated into Vietnamese hot-rolled flat steel (Case No. AD OI – 13/2024)

- 2025: Anti-dumping duties applied to Chinese cold-rolled non-oriented steel

- June 2026: New investigation opened into cold-rolled grain-oriented electrical steel from multiple origins

- June 25, 2026: Anti-dumping investigation launched into hot-rolled coil imports from China, Japan, and Russia

India's trade defence posture has shifted from reactive, product-specific responses to a proactive and systematic framework that now touches virtually every major flat steel product category and import origin simultaneously.

This layering of measures — safeguard duties on top of anti-dumping duties, across multiple product types and origins — represents a qualitatively different approach from the single-measure interventions that characterised earlier Indian trade policy on steel.

Anatomy of the June 2026 Hot-Rolled Steel Investigation

Product Scope and HS Code Coverage

The current investigation covers a well-defined but broad product range under four harmonised system codes:

| HS Code | Product Description |

|---|---|

| 7208 | Flat-rolled iron or non-alloy steel, hot-rolled, not clad, width ≥600mm |

| 7211 | Flat-rolled iron or non-alloy steel, hot-rolled, width <600mm |

| 7225 | Flat-rolled alloy steel (excluding stainless), hot-rolled, width ≥600mm |

| 7226 | Flat-rolled alloy steel (excluding stainless), hot-rolled, width <600mm |

The specifications cover alloy and non-alloy material up to 25mm thick and 2,100mm wide. Hot-rolled stainless steel coils are explicitly excluded. Notably, these are the identical HS codes used in the 2024 anti-dumping case against Vietnamese HRC, confirming a consistent and replicable definitional framework across India's flat steel trade cases — a detail that signals institutional learning within the Directorate General of Trade Remedies (DGTR).

The Complainants and Their Market Position

Three domestic producers filed the application that triggered the investigation:

- JSW Steel — India's largest private-sector integrated steel producer

- JSW Vijayanagar Metallics — a subsidiary within the JSW Group's production network

- Jindal Steel Odisha — part of the broader Jindal Group steelmaking portfolio

The DGTR accepted the prima facie evidence of dumping and material injury as sufficient to warrant a full formal investigation. Under WTO Anti-Dumping Agreement rules and Indian trade remedy law, this threshold requires complainant producers to demonstrate that imports are priced below their normal value in the country of origin and that this pricing has caused or threatens to cause measurable harm to the domestic industry.

Import Volume Data: What the Numbers Actually Show

Flows in 2025 Versus Early 2026

The trade data underpinning this investigation reveals a nuanced picture — one of a market that responded sharply to safeguard duties in 2025 before partially rebounding in early 2026:

| Period | Import Volume (HS 7208, 7211, 7225, 7226) | Year-on-Year Change | Dominant Origins |

|---|---|---|---|

| Full Year 2025 | 4.7 million tonnes | -23% | South Korea, China, Japan, Russia (89% combined) |

| January–April 2026 | 1.5 million tonnes | +4% | China and Japan (volumes doubled in this period) |

The 2025 decline directly reflects the competitive impact of safeguard duties imposed from April of that year. However, the early 2026 rebound is driven by two separate but reinforcing mechanisms. First, domestic HRC prices climbed to a peak of ₹59,000 per tonne in early April 2026, widening the landed cost advantage for imported material and creating genuine arbitrage for buyers.

Second, pipe and tube manufacturers began booking Chinese and Japanese coils under re-export frameworks, exploiting the advance authorisation scheme to bypass Bureau of Indian Standards certification requirements.

The South Korea Anomaly: Why the Largest Supplier Was Left Out

One of the most strategically significant details in this investigation is what it does not include. South Korea was the largest single-origin supplier of HRC to India under the relevant HS codes in 2025, yet it is absent from the current anti-dumping probe.

Under Indian and WTO trade remedy procedures, anti-dumping investigations cover only the origins named in the complainant's petition, provided the DGTR accepts the supporting evidence. Several possibilities explain South Korea's exclusion:

- Korean HRC pricing may not have met the evidentiary threshold required to demonstrate dumping relative to its domestic market normal value

- Existing bilateral trade frameworks between India and South Korea may have created diplomatic or procedural complications

- Complainant producers may have made a tactical decision to concentrate the case on origins where dumping evidence is stronger

Whatever the reason, South Korean exporters are positioned to benefit from trade diversion if anti-dumping duties ultimately restrict Chinese, Japanese, and Russian volumes. This is a non-obvious but potentially material outcome for Korean mills.

How India's DGTR Anti-Dumping Process Works

Step-by-Step Investigation Methodology

Understanding the procedural mechanics is essential for assessing when and how any duties might actually take effect. In addition, the broader steel trade impacts from global protectionism provide important context for this domestic process:

- Petition submission: Domestic producers file a detailed application including pricing evidence, import data, and injury analysis

- Prima facie review: The DGTR determines whether the preliminary evidence clears the threshold for initiating a formal investigation

- Official initiation: A formal notification is published — in this case dated June 25, 2026

- Investigation period definition: The complainants proposed January–December 2025 as the primary dumping investigation period

- Injury period assessment: The DGTR will examine domestic industry conditions across the financial years ending March 2023, March 2024, March 2025, and the investigation period

- Interested party submissions: Exporters, importers, and downstream users have 30 days from notification to register and submit responses

- Dumping margin calculation: The DGTR calculates the extent to which export prices fall below normal value in the country of origin

- Injury causation analysis: The agency must establish a causal link between dumped imports and material injury to Indian producers

- Final recommendation: The DGTR recommends duty levels to the Ministry of Finance, which issues the formal notification for implementation

Under WTO Anti-Dumping Agreement rules, investigations must ordinarily conclude within 12 months and cannot exceed 18 months. Provisional duties can be applied before the final determination if injury is considered imminent, typically no earlier than 60 days after initiation.

A critical but under-appreciated point: the initiation of an investigation imposes no duties. Market participants who interpret the June 25 notification as an immediate trade barrier are misreading the procedural reality. The investigation creates legal uncertainty that may restrain some importers, but commercially motivated buyers — particularly those operating under the advance authorisation scheme — may continue sourcing offshore material throughout the investigation period.

Domestic HRC Market Conditions: Price Dynamics and Supply Realities

Where Prices Stand and What Is Moving Them

As of June 19, 2026, the Argus weekly Indian domestic HRC assessment for 2.5–4.0mm material was priced at ₹57,600 per tonne (approximately $610 per tonne) ex-Mumbai, excluding goods and services tax. This represents a retreat from the early April 2026 peak of ₹59,000 per tonne, driven by a combination of:

- Monsoon seasonality: Construction and manufacturing activity in India slows materially during the June–September monsoon period, compressing HRC demand

- Mill restart and capacity additions: JSW Steel restarted a blast furnace in June 2026 after a prolonged shutdown for capacity upgradation, adding to domestic HRC availability at a moment when seasonal demand is soft

- Re-export-driven import continuation: Chinese HRC entering India primarily through the advance authorisation re-export pathway has maintained supply competition even as formal import economics became less favourable

Market participants broadly assess the near-term pricing impact of the India anti-dumping probe into hot-rolled steel imports as limited to modest. The investigation could stimulate some restocking activity as buyers hedge against the possibility of future duty imposition, but this effect is likely to be temporary and offset by the seasonal demand trough.

The next major ASX story will hit our subscribers first

Country-by-Country Exposure: How Each Named Origin Is Affected

China: Highest Volume, Multiple Structural Constraints

China faces the greatest exposure from this investigation, but also has the most established workaround pathways. The China steel outlook suggests ongoing export pressure will persist regardless of individual market actions. Chinese HRC lacks the BIS certifications required for standard customs clearance into India, which means direct commercial sales have already been structurally constrained.

The primary channel for Chinese material entering India in 2026 has been the advance authorisation re-export scheme — a regulatory carve-out that an anti-dumping determination cannot automatically close without separate policy intervention. If anti-dumping duties are imposed, Chinese mills would face a second layer of trade barriers on top of existing safeguard duties, making direct commercial sales to Indian end-users essentially unviable outside the re-export framework.

Japan: Legitimate Supply Chains at Risk

Japanese HRC occupies a different market position. Japanese coils serve established downstream supply relationships in India, particularly with pipe and tube manufacturers that value Japanese material's consistent quality specifications. At least one major domestic Indian steel mill is identified as a regular buyer of Japanese coils — a supply chain that could be disrupted or restructured if provisional duties are applied during the investigation period.

Japanese producers may mount a defence based on product quality differentiation and non-substitutability relative to domestically produced Indian HRC, which is a legitimate argument in product differentiation cases but historically difficult to sustain across the full volume range under investigation.

Russia: Geopolitical Rerouting and Structural Limits

Russian steel exports to India have expanded significantly as Western sanctions forced a fundamental rerouting of Russian trade flows. Russia formed part of the four-origin bloc — alongside South Korea, China, and Japan — that collectively accounted for 89% of HRC imports under the relevant HS codes in 2025. Anti-dumping duties would place a formal trade remedy barrier on top of already complex logistical and financial arrangements for Russian exporters serving the Indian market.

Downstream Consequences for Indian Steel Consumers

Industries Most Exposed to Potential Import Restrictions

The downstream impact of any duty imposition would not fall uniformly across the Indian economy. Consequently, understanding which sectors face the greatest exposure is essential:

- Pipe and tube manufacturers: The most immediately exposed segment, given their reliance on imported coils for both domestic processing and re-export manufacturing

- Automotive components: Indian vehicle body panel and structural component producers rely on consistent flat steel supply and could face cost pressure if domestic HRC prices rise in response to reduced import competition

- Construction and infrastructure: India's extensive public infrastructure build-out requires large volumes of flat steel; any price increase would flow through to project economics

- White goods and appliance manufacturing: Domestic appliance producers consume processed flat steel and would face margin compression if input costs rise

The Advance Authorisation Scheme: Trade Remedy's Persistent Blind Spot

One of the least-discussed but most consequential dynamics in India's steel import market is the advance authorisation scheme's interaction with trade remedy measures. Under this regulatory mechanism, importers can bring steel into India without paying safeguard or anti-dumping duties — and without obtaining BIS certification — provided the finished processed goods are subsequently re-exported.

This creates a structural bypass that sits largely outside the reach of anti-dumping determinations. Even if the DGTR recommends and the Ministry of Finance imposes duties on Chinese, Japanese, and Russian HRC, pipe manufacturers and other re-export processors can continue accessing offshore material through this channel. Indeed, tariffs on iron ore and broader flat steel categories face similar evasion challenges, demonstrating this is not an isolated regulatory gap.

Industry participants note that a meaningful volume of imported steel — particularly Chinese HRC — will continue flowing through this pathway regardless of the investigation's outcome.

Scenario Analysis: HRC Price Outlook Through 2026

| Scenario | Key Drivers | Expected HRC Price Direction |

|---|---|---|

| Investigation proceeds, no provisional duties | Seasonal weakness, rising domestic supply | Sideways to lower; ₹56,000–₹58,000/t range |

| Provisional duties imposed within 60–90 days | Import curtailment, restocking demand | Recovery toward ₹59,000–₹61,000/t |

| Full duties confirmed after 12-month process | Structural import reduction, capacity expansion | Sustained support above ₹60,000/t medium-term |

| Re-export loophole remains open throughout | Continued offshore inflows via advance authorisation | Price upside capped; domestic producer margins constrained |

Frequently Asked Questions

What is the difference between safeguard duties and anti-dumping duties?

Safeguard duties are broad, non-discriminatory import restrictions applied to all origins when an import surge threatens serious injury to a domestic industry. Anti-dumping duties are origin-specific and product-specific, targeting imports priced below their normal value in the exporting country. India currently operates both mechanisms simultaneously on flat steel, creating a compounding effect on import economics for named origins.

Will the investigation immediately restrict imports from China, Japan, and Russia?

No. The formal initiation of an investigation does not impose any duties. Provisional anti-dumping measures require a preliminary determination of dumping and injury, which cannot occur earlier than 60 days after initiation. Final duties require a completed investigation and a separate Ministry of Finance notification.

How long will the investigation take to conclude?

Under WTO commitments and Indian trade remedy law, investigations are expected to conclude within 12 months of initiation, with a permissible extension to 18 months for complex cases. The proposed investigation period covers January through December 2025, with injury assessment extending back to the financial year ending March 2023.

Why was South Korea excluded despite being the largest import source in 2025?

Anti-dumping investigations cover only the origins named in the complainant's petition, provided the DGTR accepts the supporting evidence. The DGTR's anti-dumping investigation framework confirms that South Korea's pricing, trade frameworks, or evidentiary record may not have met the threshold required for inclusion. The exclusion leaves South Korean producers in a potentially advantaged position if duties curtail competing origins.

Disclaimer: This article contains forward-looking assessments, price scenario analysis, and regulatory interpretations for informational purposes only. It does not constitute financial, legal, or investment advice. Trade remedy outcomes are subject to independent regulatory determinations and may differ materially from the scenarios presented. Readers should consult qualified professionals before making any commercial or investment decisions based on the information contained herein.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

While India's steel trade defence measures reshape global commodity flows and redirect capital across the mining sector, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across 30+ commodities — explore historic discovery returns that demonstrate why being early matters, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.