June 18, 2026

The Upstream Blind Spot in India's Electric Vehicle Revolution

Every ambitious industrial transformation has a hidden chokepoint. For India's electric vehicle and clean energy ambitions, that chokepoint sits not in assembly lines or charging infrastructure, but in the chemistry of the battery itself. Specifically, it sits in the raw material inputs that determine whether a battery cell is made in India or merely assembled there. Until those upstream materials are produced domestically, every gigawatt-hour target and every PLI-backed cell factory rests on a foundation of imported dependency.

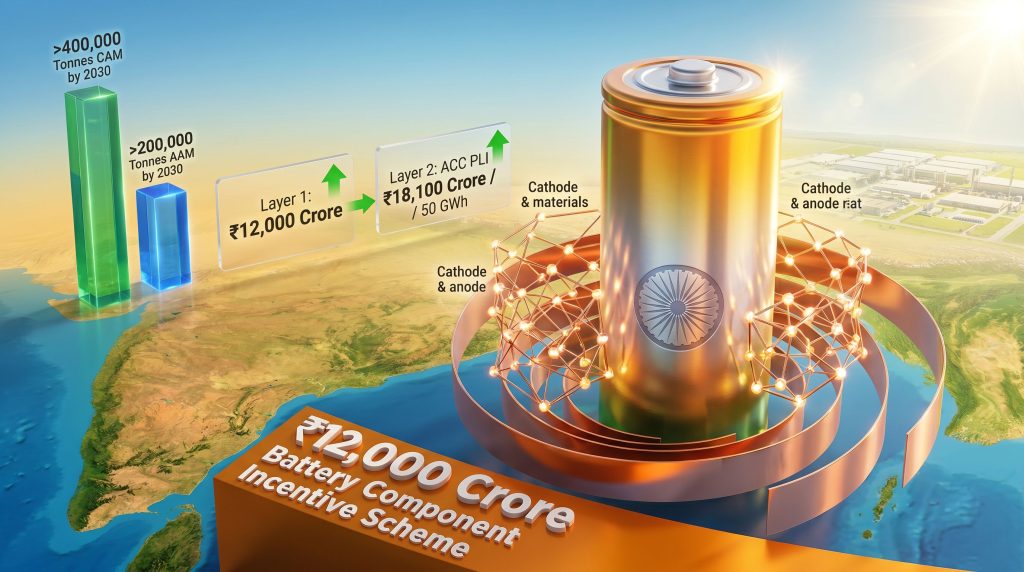

The India battery component incentive scheme, carrying a proposed financial allocation of approximately ₹12,000 crore, is the policy response to precisely this vulnerability. However, understanding why this scheme matters requires looking beyond the headline figure and into the structural mechanics of how battery supply chains actually work.

When big ASX news breaks, our subscribers know first

Why Full Import Dependency Is an Industrial Policy Problem

India's battery manufacturing ambitions are well documented. The Ministry of Heavy Industries has already committed ₹18,100 crore under the Advanced Chemistry Cell (ACC) Production-Linked Incentive scheme, targeting 50 GWh of domestic cell manufacturing capacity. On paper, that is a credible industrial commitment. In practice, however, those cell factories cannot manufacture competitively if every critical input material arrives from overseas.

The four material categories at the centre of this import dependency problem are:

- Cathode Active Materials (CAM): The electrochemically active compounds that determine a battery's voltage, energy density, and thermal characteristics. Examples include lithium iron phosphate (LFP), nickel manganese cobalt oxide (NMC), and nickel cobalt aluminium oxide (NCA).

- Anode Active Materials (AAM): Typically graphite-based compounds that store lithium ions during charging. Natural and synthetic graphite dominate this category, with silicon-blended variants increasingly used in high-performance applications.

- Copper Foil Separators: Ultra-thin copper current collectors that form the structural backbone of the anode layer. Producing foil at the thickness required for battery-grade applications (typically 6 to 10 microns) demands highly specialised rolling and deposition technology.

- Electrolysers: Devices that split water into hydrogen and oxygen using electrical current, relevant to green hydrogen production and certain battery-adjacent manufacturing processes.

India currently imports 100% of its requirements across all four categories. This is not simply a cost problem. It is a sovereignty problem. When downstream cell manufacturers depend entirely on foreign-sourced inputs, they are exposed to supply disruptions, currency fluctuations, and the geopolitical decisions of exporting nations — none of which are within India's control. Furthermore, the battery raw materials market dynamics globally are shifting rapidly, adding further urgency to domestic capability building.

The Incentive Arbitrage Risk That Policymakers Are Actively Trying to Close

There is a well-documented failure mode in industrial incentive programmes globally: companies perform minimal processing on imported near-finished goods and claim subsidies designed for genuine manufacturers. India's policymakers have explicitly acknowledged this risk in the context of the proposed battery component scheme.

According to reporting by ET Bureau's Twesh Mishra in ET EnergyWorld (June 2026), government officials confirmed that funding support will carry conditions specifically designed to mandate authentic domestic manufacturing. The scheme framework is intended to disqualify any applicant that imports finished or near-finished components and performs only superficial final-stage processing before claiming incentives.

Policy Design Insight: The anti-gaming provisions embedded in the India battery component incentive scheme reflect lessons drawn from earlier PLI implementations globally, where the line between genuine domestic manufacturing and sophisticated import processing proved difficult to police without explicit conditionality frameworks.

The Scale of India's Battery Material Requirements by 2030

Perhaps the most striking aspect of this policy development is the sheer scale of the manufacturing challenge it is attempting to address. Industry estimates, cited in the ET EnergyWorld report, quantify the upstream material requirements needed to support India's 223 GWh domestic battery manufacturing capacity target:

| Material | Projected Annual Requirement by 2030 | Current Domestic Production |

|---|---|---|

| Cathode Active Materials (CAM) | >400,000 tonnes | Effectively zero |

| Anode Active Materials (AAM) | >200,000 tonnes | Effectively zero |

Building from a near-zero production base to these volumes within a five-year window represents one of the most compressed industrial scaling challenges in India's manufacturing history. For context, a single large-scale CAM facility might produce 20,000 to 50,000 tonnes per year at full capacity, meaning India would need to commission multiple facilities operating simultaneously and at scale before the end of the decade.

The technical barriers are also significant. CAM production requires precise control of particle morphology, elemental ratios, and surface coatings. Defects at the precursor stage propagate through the entire cell and appear as capacity fade, thermal instability, or cycle life degradation in the finished battery. These are not problems that can be resolved through investment alone; they require deep process chemistry expertise and substantial technology transfer.

The Copper Foil Concentration Problem: A Vulnerability Few Analysts Discuss

While CAM and AAM attract most of the policy attention in battery supply chain discussions, copper foil represents a less visible but equally critical vulnerability. According to a report by the International Copper Association of India on battery supply chain indigenisation, Chinese producers control approximately 80% of global copper foil manufacturing capacity, with Korean manufacturers accounting for the remaining 20%.

This near-total duopoly is the result of decades of capital concentration and incremental process refinement. Battery-grade copper foil production is technically demanding in ways that are not immediately apparent. The foil must be produced at extremely uniform thickness, typically between 6 and 10 microns, with surface roughness and tensile strength properties that are difficult to achieve consistently at scale.

Chinese manufacturers have invested heavily in the precision electrodeposition and rolling technologies required, creating a competitive moat that new entrants cannot easily replicate. For India, localising copper foil production is therefore not simply an economic efficiency measure — it is a strategic industrial capability question. Consequently, a nation that cannot produce its own copper foil remains structurally dependent on two foreign supply bases for a component that goes into every single battery cell manufactured domestically.

How the Two Schemes Work Together: A Two-Layer Policy Architecture

The India battery component incentive scheme is most accurately understood not as a standalone initiative but as the upstream layer of a two-part industrial policy structure:

| Scheme | Focus | Financial Allocation | Capacity Target |

|---|---|---|---|

| Battery Component Incentive Scheme | CAM, AAM, copper foil, electrolysers | ~₹12,000 crore (proposed) | Upstream input localisation |

| ACC Battery PLI | Finished cell manufacturing | ₹18,100 crore | 50 GWh |

| Combined | Full supply chain coverage | ~₹30,100 crore | Cell + components |

Under the ACC PLI framework, selected manufacturers are required to establish cell production within two years of selection, with incentive disbursements structured across a five-year performance window tied to domestically sold batteries. The component scheme is designed to ensure those cell manufacturers are not simply converting imported inputs into locally assembled cells, but are drawing from a genuinely localised upstream supply base.

The combined ₹30,100 crore committed across both layers places India among the more serious emerging market investors in integrated battery industrial policy. However, it remains modest compared to the scale of support deployed in the United States under the Inflation Reduction Act's 45X advanced manufacturing tax credit provisions, or the European Battery Alliance's multi-billion euro programme. In addition, the broader question of critical minerals security underpins the long-term viability of both schemes.

The Unresolved Duty Question: A Material Uncertainty for Investors

One of the most consequential unresolved issues surrounding the India battery component incentive scheme is the question of import duty relief on raw material inputs.

Industry participants have formally requested duty waivers to make domestic CAM and AAM production economically viable. The logic is straightforward: if raw material inputs such as lithium carbonate, precursor chemicals, and refined graphite are subject to standard import tariffs, the cost structure of domestic component manufacturing becomes difficult to justify against simply purchasing finished components from established Chinese or South Korean suppliers.

As of mid-2026, a decision on broader duty waivers has not been finalised. Budget 2026-27 did extend basic customs duty exemptions on capital goods used in lithium-ion cell manufacturing for battery energy storage systems, which signals a degree of policy receptivity, but raw material input duties remain unresolved.

Investor Consideration: The duty structure outcome represents a binary variable for the investment economics of domestic CAM and AAM manufacturing. Companies evaluating capital commitments in this space ahead of formal duty decisions are carrying meaningful regulatory uncertainty on their cost assumptions.

The next major ASX story will hit our subscribers first

India's Approach in a Global Policy Context

How does India's battery component policy compare to the approaches taken by leading battery manufacturing nations?

| Country/Region | Primary Instrument | Scale | Key Characteristics |

|---|---|---|---|

| India | ACC PLI + Component Scheme | ~₹30,100 crore combined | Conditionality-driven, anti-gaming provisions |

| United States | IRA 45X Manufacturing Credits | USD billions over decade | Production tax credits per unit output |

| European Union | European Battery Alliance + IPCEI | €6+ billion | Full chain from mining to recycling |

| China | State-directed industrial policy | Effectively uncapped | Decades of integrated value chain investment |

India's approach is notably more conditionality-driven than any of these comparators. The explicit anti-gaming provisions, the requirement for verifiable domestic supply chains, and the deliberate separation of cell-level and component-level incentives into distinct schemes reflect a sophisticated understanding of where earlier industrial subsidy programmes have failed.

What India cannot replicate quickly is the technology depth that underpins Chinese battery material production. China's dominance in CAM, AAM, and copper foil is not purely the product of state support; it reflects two decades of process chemistry refinement, workforce development, and supply chain integration. Furthermore, India's lithium supply strategy will play a pivotal role in determining how effectively the country can close that gap through international partnerships and joint ventures.

Who Is Positioned to Participate?

The companies best positioned to benefit from the India battery component incentive scheme share several characteristics:

- Existing chemical manufacturing infrastructure that can be adapted for precursor and active material production, reducing greenfield capital requirements.

- Access to critical mineral inputs, particularly lithium, manganese, cobalt, and graphite, either through domestic mining positions or long-term offtake agreements with international suppliers.

- Technology partnerships with established international battery material producers willing to transfer process know-how in exchange for access to India's market and incentive framework.

- Balance sheet capacity to fund multi-year ramp-up periods before incentive disbursements and commercial revenues reach meaningful scale.

Foreign battery material producers considering India as a manufacturing hub represent another important participant category. India's global lithium push has already demonstrated the country's intent to secure upstream supply chains at an international level. The combination of a large and growing domestic EV market, the incentive framework, and India's improving industrial infrastructure creates a potentially attractive case for localised production — provided the duty question is resolved favourably. For investors evaluating exposure to this space, the broader battery metals investment landscape offers important context on where capital is flowing globally.

It is also worth noting that independent assessments of India's incentive schemes suggest delivery against targets has historically been uneven, with only a fraction of target capacity delivered under previous battery manufacturing programmes — underscoring the importance of the stricter conditionality provisions built into the current framework.

Key Takeaways

- The India battery component incentive scheme proposes ₹12,000 crore in financial support for domestic production of CAM, AAM, copper foil separators, and electrolysers

- All four categories are currently 100% import-dependent, creating structural exposure across India's EV, defence, and aerospace sectors

- Industry estimates require >400,000 tonnes of CAM and >200,000 tonnes of AAM annually by 2030 to support India's 223 GWh manufacturing target

- Chinese producers control ~80% of global copper foil capacity, with Korean manufacturers holding the remaining ~20%, making localisation a strategic priority

- The component scheme complements the existing ₹18,100 crore ACC Battery PLI, bringing total committed battery industrial policy support to approximately ₹30,100 crore

- Anti-gaming conditions require verifiable domestic manufacturing; import processing operations will not qualify

- The duty waiver question remains unresolved, representing the most significant financial uncertainty for prospective investors

- The scheme was described as being in final stages of approval as of June 2026, with formal gazette notification pending

This article contains forward-looking analysis based on publicly available policy information and industry estimates as of June 2026. Readers should note that the scheme described has not yet received formal gazette notification, and financial and policy details remain subject to change. Nothing in this article constitutes investment advice.

Want to Track the Next Major Battery Metals Discovery Before the Broader Market Does?

India's race to secure upstream battery materials — from cathode actives to copper foil — underscores just how critical early identification of significant mineral discoveries has become for investors. Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts on significant battery and critical minerals discoveries, turning complex geological data into actionable insights the moment they hit the exchange — explore historic discovery returns on Discovery Alert's discoveries page and begin your 14-day free trial to position yourself ahead of the market.