June 4, 2026

The Quiet Industrial Revolution Reshaping Asia-Pacific Chemical Supply Chains

Across global commodity markets, the chemicals most critical to industrial civilisation rarely attract headlines. Yet the foundational inputs that enable aluminium smelting, petroleum refining, textile processing, and clean water delivery quietly determine the competitive architecture of entire manufacturing economies. Caustic soda, or sodium hydroxide, sits precisely at this intersection: invisible to consumers, indispensable to industry. Understanding where its production capacity is being built, and at what pace, reveals something far more significant than a sectoral footnote. It reveals which economies are positioning themselves to anchor the next generation of industrial supply chains.

India caustic soda capacity growth is now one of the defining stories in global chlor-alkali markets. The scale, speed, and geographic breadth of the country's capacity build-out through 2030 suggests a structural transformation rather than a cyclical upswing. This analysis examines what is driving that transformation, which projects are delivering it, and what the implications are for producers, industrial buyers, and supply chain strategists across Asia-Pacific and beyond.

When big ASX news breaks, our subscribers know first

Caustic Soda's Industrial Centrality: Why This Chemical Matters More Than Most Realise

To appreciate the significance of India's capacity expansion, it helps to understand just how deeply embedded caustic soda is within modern industrial activity. Few chemicals touch as many sectors simultaneously.

In the aluminium industry, sodium hydroxide is the essential reagent in the Bayer process, where it dissolves aluminium-bearing minerals from bauxite ore to produce alumina before smelting. In pulp and paper manufacturing, it functions as both a pulping agent and a bleaching input. Textile producers use it for mercerisation and scouring, processes that improve fibre strength and dye uptake. Water treatment facilities rely on it for pH adjustment and purification.

Soap and detergent production depends on saponification reactions driven by caustic soda. In petrochemical and refinery settings, it serves as a process control chemical and neutralising agent across multiple unit operations.

The oil and gas sector's relationship with caustic soda is particularly multifaceted and often underappreciated:

- Upstream drilling operations use caustic soda to condition drilling fluids, maintain wellbore stability, and scavenge hydrogen sulphide (H₂S), a toxic and corrosive gas encountered during hydrocarbon extraction

- Midstream pipeline infrastructure relies on caustic soda for cleaning, corrosion inhibition, and the neutralisation of acidic contaminants in transported fluids

- Downstream refinery operations incorporate caustic soda in crude distillation processes, mercaptan removal, and effluent treatment systems

This cross-sector demand profile means that growth in India's industrial base, whether driven by aluminium capacity expansion, refinery upgrades, textile export growth, or urban water infrastructure investment, translates directly into rising caustic soda consumption. Domestic demand is projected to reach approximately 5,400 KT by FY2027-28, expanding at roughly a 5.5% CAGR, according to industry estimates.

India Caustic Soda Capacity Growth: The Three-Year Production Trajectory

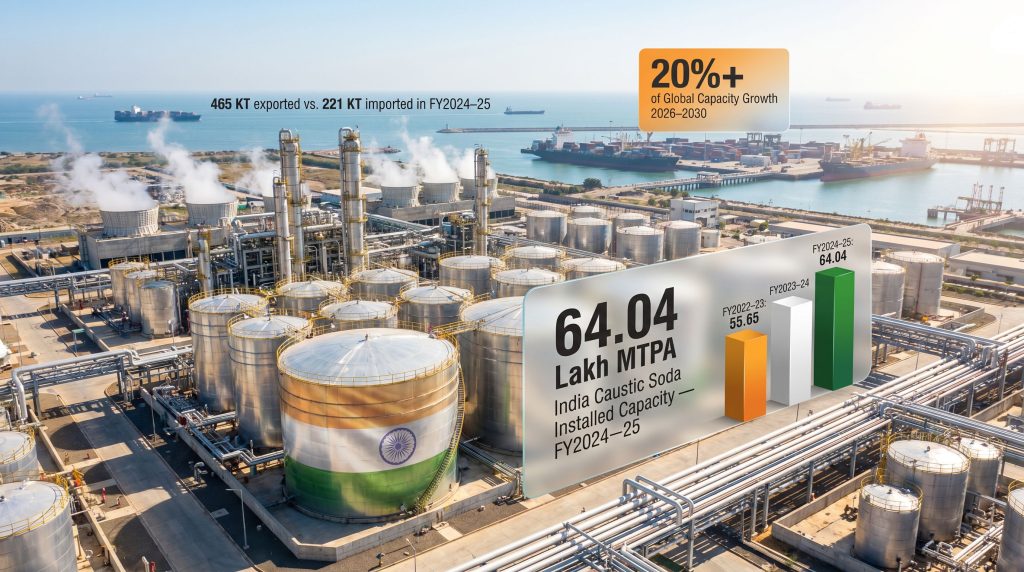

The numbers underpinning India caustic soda capacity growth tell a story of accelerating investment and resilient demand absorption. Data from the Alkali Manufacturers Association of India (AMAI) captures the trajectory clearly across a three-year window.

| Fiscal Year | Installed Capacity (Lakh MTPA) | Production (Lakh MT) | Utilisation Rate |

|---|---|---|---|

| FY2022-23 | 55.65 | 44.73 | ~80% |

| FY2023-24 | 57.85 | 46.13 | ~80% |

| FY2024-25 | 64.04 | 50.20 | ~78.4% |

Source: Alkali Manufacturers Association of India (AMAI)

Several dimensions of this data deserve careful attention beyond the headline figures:

- Installed capacity increased by approximately 15% between FY2023 and FY2025, rising from 55.65 to 64.04 lakh MTPA

- Production volumes grew from 44.73 lakh MT to 50.20 lakh MT over the same period, a gain of roughly 12.3%

- The utilisation rate held at 78.4% in FY2024-25, a figure that remains robust given the scale of new capacity coming online

The stability of the utilisation rate amid significant capacity additions is an important signal. It indicates that demand absorption has kept pace with supply growth rather than lagging behind it. However, the broader trajectory points toward a widening gap: production capacity is expanding at approximately 9% CAGR, while domestic demand growth tracks closer to 4-5.5% CAGR. The inevitable consequence of this divergence is a structural surplus, and that surplus is already reshaping India's trade position.

In FY2024-25, India exported 465 KT of caustic soda while importing just 221 KT, yielding a net export position of approximately 244 KT. This reversal from historic import dependency to net exporter status is not a temporary anomaly. It reflects the directional logic of the entire capacity build programme.

India's transition from a net importer to a net exporter of caustic soda is a structural realignment, not a short-term arbitrage play. The country is now on a trajectory to influence Asia-Pacific pricing benchmarks as export volumes scale through the remainder of the decade.

The Project Pipeline: Who Is Building What, and Where

The depth of India's capacity pipeline is perhaps its most compelling feature. Across multiple states, a mix of established industrial conglomerates, integrated refinery-chemical operators, and sector-focused manufacturers are committing capital to chlor-alkali expansion. Furthermore, India's resource security strategy is reinforcing this momentum, as the country increasingly prioritises self-sufficiency across critical industrial inputs.

| Project / Developer | Capacity (MTPD) | Location | Status |

|---|---|---|---|

| Adani Group | 4,360 (Phase 1) | TBC | Planned |

| Reliance Industries | 4,000 | TBC | Engineering completion stage |

| IOCL Vadodara | 1,000 | Gujarat | Planning/Engineering |

| IOCL Paradip | 1,000 | Odisha | Planning/Engineering |

| Valor Petrochemicals Mundra | TBC | Gujarat (Mundra) | Commissioning expected 2026-27 |

| Indian Peroxide Dahej | TBC | Gujarat (Dahej) | Commissioning expected within year |

| Grasim Industries (Project 1) | TBC | Andhra Pradesh | Targeted commissioning 2027 |

| Grasim Industries (Project 2) | TBC | Andhra Pradesh | Targeted commissioning 2029 |

| TGV SRAAC Kurnool | TBC | Andhra Pradesh (Kurnool) | Expected production start 2028 |

| DCM Shriram, Kutch Chemicals, Atul, Aurobindo Pharma | Various | Multiple states | Various stages |

Gujarat: The Established Chlor-Alkali Heartland

Gujarat's dominance in the capacity pipeline reflects structural advantages that are difficult for competing states to replicate quickly. The state benefits from an existing chlor-alkali manufacturing base, deep-water port infrastructure at Mundra and Dahej, and direct connectivity to one of Asia's densest petrochemical and refining corridors. These advantages compress logistics costs, enable feedstock integration, and simplify export access.

Valor Petrochemicals Mundra stands out as the single largest incremental capacity addition in the current development cycle. Developed by Valor Petrochemicals Ltd and anticipated to commence operations during 2026-27, the facility is positioned to strengthen regional chemical supply chains and provide a competitive domestic alternative to imported product for oil and gas and petrochemical buyers across western India.

Indian Peroxide Dahej, led by Indian Peroxide Ltd, is expected to come online within the current year. Its commissioning will further consolidate Gujarat's position as the country's premier chlor-alkali hub and deepen the integration between caustic soda production and the downstream petrochemical manufacturing ecosystem clustered around Dahej's special economic zone.

Andhra Pradesh: An Emerging Eastern Production Corridor

The geographic concentration of three separate projects within Andhra Pradesh signals something strategically important: India's caustic soda capacity growth is actively diversifying away from western dominance. This matters for supply chain resilience and for the eastern coastal energy corridor that is increasingly central to India's oil and gas infrastructure development.

Grasim Industries is advancing two separate chlor-alkali developments within the state, with commissioning targets of 2027 and 2029 respectively. These timelines align with Grasim's broader chemicals strategy, which emphasises downstream integration and the expansion of speciality and commodity chemical portfolios in tandem.

TGV SRAAC Kurnool, developed and fully owned by TGV SRAAC Ltd, is targeting production commencement in 2028. The project reflects rising institutional confidence in eastern India's industrial demand profile and signals that the investment case for the region extends well beyond existing clusters.

Energy Economics: The Variable That Determines Long-Term Competitiveness

One technical dimension of caustic soda production that rarely receives adequate attention in market commentary is its extraordinary energy intensity. The chlor-alkali process, which involves the electrolysis of brine solution to produce caustic soda, chlorine, and hydrogen simultaneously, is among the most electricity-intensive operations in the chemical manufacturing sector. Electricity costs typically account for 35-50% of total production costs depending on the technology deployed and the local power tariff environment.

This energy intensity creates a critical competitive variable that will significantly influence which Indian producers achieve sustainable economics through the 2030 horizon:

- Technology selection: Modern membrane cell technology offers substantially better energy efficiency than older diaphragm or mercury cell processes, reducing power consumption per tonne of caustic soda produced. India's newer capacity additions are predominantly adopting membrane cell technology, which positions them favourably relative to older installed base.

- Renewable energy integration: Producers with access to captive renewable power, whether solar, wind, or hybrid systems, can meaningfully reduce their exposure to grid electricity tariff volatility. This mirrors broader trends seen in green iron production, where energy sourcing has become a defining competitive factor.

- State-level power cost differentials: Electricity tariff structures vary significantly between Gujarat and Andhra Pradesh, a factor that may increasingly influence investment allocation decisions as the pipeline progresses toward commissioning.

The economics of chlor-alkali manufacturing are fundamentally tied to the cost of electrons. Producers who secure long-term competitive power arrangements, whether through renewable integration or favourable industrial tariffs, will hold a structural advantage over those exposed to volatile grid pricing.

End-Use Demand Matrix: Mapping the Growth Drivers

India's caustic soda demand growth is not driven by a single sector but by the simultaneous expansion of multiple industrial verticals. This breadth provides demand resilience that single-sector dependent markets lack.

| Sector | Role of Caustic Soda | Primary Growth Driver |

|---|---|---|

| Alumina Refining | Bayer process feedstock | Bauxite-to-aluminium expansion |

| Oil and Gas (Upstream) | Drilling fluid treatment, H₂S scavenging | Rising domestic exploration and production activity |

| Oil and Gas (Downstream) | Refinery process control, pipeline cleaning | Refinery capacity expansion |

| Paper and Pulp | Pulping and bleaching agent | Packaging and e-commerce demand growth |

| Textiles | Mercerisation, scouring | Export-oriented manufacturing growth |

| Water Treatment | pH adjustment, purification | Urban infrastructure investment |

| Soaps and Detergents | Saponification feedstock | FMCG sector expansion |

| Petrochemicals | Process chemical input | Downstream complex expansion |

The oil and gas sector's demand contribution deserves particular emphasis because it operates across multiple nodes of the value chain simultaneously. A single integrated refinery-petrochemical complex may consume caustic soda in refinery desulphurisation units, in effluent neutralisation systems, and in feedstock pre-treatment operations. As India's refinery capacity expands and domestic exploration activity intensifies, this institutional demand for domestically sourced caustic soda will grow materially.

The next major ASX story will hit our subscribers first

Global Positioning: India as a Second Force in Chlor-Alkali Capacity Additions

China has historically dominated global caustic soda production, commanding the largest installed base and setting export pricing benchmarks that have shaped procurement decisions across Asia-Pacific for decades. The China steel market offers a comparable illustration of how single-country dominance creates systemic risk for global buyers. India's emergence as the second largest contributor to global capacity additions through 2030, projected to account for more than 20% of total global capacity growth over the 2026-2030 period, represents a meaningful reconfiguration of this landscape.

For industrial buyers across Southeast Asia, East Africa, and South Asia, this creates a genuine sourcing alternative. Markets that have historically relied on Chinese export supply, accepting the price volatility and logistical dependencies that entails, will increasingly be able to draw on Indian production at competitive terms. India's geographic positioning, particularly for Gulf of Bengal and Indian Ocean basin markets, confers natural freight cost advantages that Chinese producers cannot easily replicate.

The implications extend beyond price. Supply chain security has become an explicit strategic priority for industrial operators following the disruptions of the early 2020s. A diversified supplier base, anchored by both Chinese and Indian production capacity, substantially reduces the systemic risk exposure for large industrial consumers of caustic soda.

Pricing Dynamics and the Surplus Scenario

With production capacity expanding at roughly 9% CAGR against domestic demand growth of 4-5.5% CAGR, the medium-term trajectory points clearly toward a structural surplus. How that surplus resolves will determine the pricing and margin environment for Indian producers through the back half of the decade.

Three plausible scenarios frame the range of outcomes:

Scenario 1: Balanced Export Absorption

Capacity additions commission broadly on schedule, and export market development absorbs the surplus efficiently. Asia-Pacific buyers diversify away from Chinese supply toward Indian product, sustaining Indian producers at viable utilisation rates above 75% and supporting acceptable margins.

Scenario 2: Oversupply and Domestic Price Compression

Commissioning timelines accelerate while regional demand disappoints. Domestic pricing falls as producers compete for available volume, compressing margins and potentially delaying the financial returns of newer entrants with higher capital costs.

Scenario 3: Integration Premium and Sector Consolidation

Large integrated operators such as Adani, Reliance, and Grasim leverage downstream chemical integration to insulate their margins from spot market pressure. Smaller standalone producers face competitive stress, accelerating consolidation and reshaping the competitive landscape of India's chlor-alkali sector.

For industrial procurement strategists, India's emerging surplus represents a structural opportunity: access to competitively priced caustic soda from a geographically proximate, cost-competitive production base. The timing and scale of that opportunity will depend on how quickly export logistics infrastructure can match the pace of upstream capacity additions.

Infrastructure and Logistics: The Binding Constraint

Capacity without export connectivity is an incomplete competitive proposition. India's ability to convert its emerging caustic soda surplus into sustainable export market share will depend critically on port infrastructure development, bulk liquid chemical terminal availability, and freight cost competitiveness.

Gujarat's port infrastructure at Mundra and Dahej already provides meaningful export capability for western India's production. However, as Andhra Pradesh's capacity comes online through 2027-2029, the adequacy of eastern coastal logistics infrastructure will come under increasing scrutiny. The development of dedicated chemical berths and bulk liquid handling capacity at eastern ports will be a critical enabling condition for the eastern corridor's export competitiveness.

Continued investment in industrial corridors, power infrastructure, and port connectivity will remain as essential to sustaining India caustic soda capacity growth as the upstream capital investment itself. Consequently, the green iron expansion model, where infrastructure investment runs in parallel with production build-out, offers instructive parallels for how India might structure its chemical export enablement programme.

Frequently Asked Questions: India Caustic Soda Capacity Growth

What is India's current caustic soda installed capacity?

India's installed caustic soda capacity reached 64.04 lakh MTPA (approximately 6.4 million MTPA) in FY2024-25, up from 55.65 lakh MTPA in FY2022-23, representing growth of approximately 15% over two years, according to the Alkali Manufacturers Association of India.

At what rate is India's caustic soda production capacity growing?

Production capacity is expanding at approximately 9% CAGR, meaningfully ahead of domestic demand growth estimated at 4-5.5% CAGR. This divergence is creating a structural surplus being directed toward export markets.

Which Indian states are leading caustic soda capacity expansion?

Gujarat leads the capacity pipeline, supported by established industrial infrastructure, deep-water port access at Mundra and Dahej, and proximity to a well-developed petrochemical and refining corridor. Andhra Pradesh is emerging as a secondary growth centre with three projects in planning stages targeting commissioning between 2027 and 2029.

How does caustic soda relate to India's oil and gas sector?

Caustic soda functions as a critical process chemical across upstream drilling operations (drilling fluid conditioning and H₂S scavenging), midstream pipeline maintenance, and downstream refinery process control and effluent treatment. India's expanding domestic production base supports supply chain security for oil and gas operators seeking competitively priced process chemicals.

Is India becoming a net exporter of caustic soda?

Yes. India exported 465 KT of caustic soda in FY2024-25 while importing just 221 KT, confirming a net export position of approximately 244 KT. This structural shift reflects capacity growth outpacing domestic demand absorption.

What is the demand outlook for caustic soda in India through 2028?

Domestic demand is projected to reach approximately 5,400 KT by FY2027-28, growing at a 5.5% CAGR. However, announced capacity additions are expected to grow at a faster rate, reinforcing the export-oriented dynamic that is reshaping India's trade position in the chlor-alkali market.

Strategic Outlook: Critical Success Factors Through 2030

India's caustic soda capacity growth narrative carries genuine strategic weight. For it to translate into durable competitive advantage rather than a temporary surplus overhang, several critical enablers must advance in parallel with upstream capacity investment. Furthermore, the global steel outlook demonstrates how rapidly commodity supply dynamics can shift when multiple large-scale capacity programmes converge simultaneously, offering a cautionary reference point for Indian chlor-alkali producers.

- Export logistics infrastructure at both western and eastern coastal ports must scale to handle rising bulk liquid chemical volumes

- Energy cost management, through renewable integration and efficient technology deployment, must protect production economics against tariff volatility

- Downstream demand development in alumina refining, petrochemicals, and oil and gas must absorb incremental domestic supply as new capacity comes online

- Policy consistency across industrial corridor development, chemical manufacturing incentives, and infrastructure investment must sustain the confidence of large capital allocators

- Sector consolidation dynamics must be managed in ways that maintain competitive tension without triggering destructive price competition that undermines the investment thesis for new entrants

For global industrial buyers, India's emergence as a significant caustic soda exporter is unambiguously positive. It introduces a credible alternative supply source, introduces competitive pressure on existing benchmark pricing, and reduces the systemic risk associated with single-country supply dependence. For India's producers, the challenge is converting installed capacity into sustainable export market share at economics that justify the capital invested. The 2026-2030 period will determine how effectively that conversion occurs.

Further analysis of global caustic soda capacity trends and capital expenditure outlooks across active and planned projects between 2026 and 2030 is available through the global caustic soda market report. Authoritative capacity and production data for the Indian domestic market is published by the Alkali Manufacturers Association of India (AMAI). For sector-specific coverage of India's chlor-alkali industry trends and regional market dynamics, specialist resources are available through industry analysts covering the Asia-Pacific chemicals sector. For broader coverage of India's oil and gas industry developments, readers can explore Petroleum Australia at petroleumaustralia.com.au.

Want to Track the ASX Mineral Discoveries Fuelling Asia-Pacific's Industrial Transformation?

As India's caustic soda capacity build-out accelerates demand for bauxite, industrial minerals, and energy commodities, the ASX companies supplying these critical inputs are increasingly in focus. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, turning complex geological data into actionable investment insights — explore historic discoveries and their returns to understand the opportunity, then begin a 14-day free trial at Discovery Alert to position yourself ahead of the broader market.