May 10, 2026

Global energy markets are experiencing unprecedented turbulence as supply chain vulnerabilities expose the interconnected nature of modern commodity trading. When geopolitical tensions disrupt established trade routes and pricing mechanisms, the ripple effects cascade through regional markets in ways that reshape procurement strategies across entire industries. This dynamic is particularly evident in how international coal price volatility influences domestic auction mechanisms, where india coal auction prices rise on seaborne volatility, creating new paradigms for energy security planning.

The phenomenon extends beyond simple supply and demand fundamentals to encompass complex risk management frameworks that industrial buyers must navigate in an increasingly uncertain global environment. As traditional procurement models face stress testing under volatile conditions, the emergence of alternative sourcing strategies reveals the adaptability of market participants operating under constrained choices.

Understanding India's Coal Auction Mechanism and Market Dynamics

The Structure of India's Domestic Coal Distribution System

India's coal distribution operates through a sophisticated dual-track system that balances administrative price controls with market-driven price discovery. Coal India Limited commands approximately 75% of the nation's coal supply, establishing it as the dominant force in domestic fuel procurement. This quasi-monopolistic position creates unique market dynamics where administrative pricing coexists with competitive auction mechanisms.

The electronic auction framework represents a critical price discovery tool within this controlled environment. During March 2026, average auction premiums reached 45% above administratively notified prices, demonstrating significant market stress compared to February's 35% premium levels. Furthermore, the financial year 2025-2026 recorded an overall average premium of 38%, indicating sustained pressure on domestic coal procurement.

Coal India's Auction Performance Metrics:

- Single window mode agnostic e-auctions: 14% of total CIL sales

- Long-term contracted sales: Priced at government-notified rates

- March 2026 premium range: 25-171% above notified prices

- Highest premium achieved: 171% for G10 grade coal at Rs 3,682/tonne

The auction mechanism serves multiple functions beyond price discovery, acting as a release valve for market pressures while maintaining government oversight of strategic energy resources. This hybrid approach allows market forces to operate within controlled parameters, ensuring domestic supply security while providing flexibility for industrial procurement.

Key Players in India's Coal Value Chain

Regional coalfield subsidiaries exhibit distinct performance characteristics that reflect their strategic positioning and operational capabilities. Northern Coalfields achieved the highest March 2026 auction premium at 80%, followed by South Eastern Coalfields at 70% and Eastern Coalfields at 48%. These variations highlight competitive advantages related to coal quality, transportation infrastructure, and proximity to industrial demand centers.

Industrial buyer segments demonstrate differentiated procurement strategies based on technical specifications and operational requirements:

Sponge Iron Manufacturers:

- Increased domestic coal blend from 30-40% to 80% during recent volatility

- Preference for high fixed-carbon content coal from specific regional sources

- Cost optimization through reduced import dependency

Cement Industry:

- Strategic switching between petroleum coke and coal based on relative pricing

- Energy content calculations driving procurement decisions

- Infrastructure investments for fuel handling flexibility

Power Generation Utilities:

- Reliance on long-term Coal India contracts for baseload requirements

- Limited participation in spot auctions for marginal volume needs

- Strategic inventory management for seasonal demand patterns

The transportation infrastructure creates additional competitive advantages for certain coalfields. Proximity to major industrial hubs, rail connectivity, and coastal access for export potential all influence auction dynamics and premium levels across different regions.

When big ASX news breaks, our subscribers know first

What Factors Drive Premium Fluctuations in Indian Coal Auctions?

International Market Spillover Effects on Domestic Pricing

Global coal price movements create powerful transmission mechanisms that influence domestic auction behaviour through competitive dynamics and import parity calculations. Indonesian GAR 4,200 kcal/kg coal prices increased approximately 10% between late February and early April 2026, rising from $54.31/tonne to $59.51/tonne. This represents a 33% increase from the beginning of 2026, when prices stood at $44.91/tonne.

International Coal Price Movements (2026):

| Coal Type | Early 2026 | Late Feb | Early April | YTD Change |

|---|---|---|---|---|

| Indonesian GAR 4,200 | $44.91/t | $54.31/t | $59.51/t | +33% |

| Newcastle NAR 5,500 | – | – | $87.59/t | +24% |

| South African NAR 5,500 | – | – | $96.11/t | +31% |

The price transmission mechanism operates through industrial buyers' import parity calculations, where international delivered costs establish reference benchmarks for domestic auction bidding strategies. When seaborne coal prices increase, domestic coal becomes relatively more attractive, intensifying competition in auction markets and driving premium escalation.

Currency volatility compounds these effects by altering landed cost calculations for imported alternatives. The Indian rupee averaged Rs 92.90 per dollar in March 2026, compared to Rs 90.76 in February, before weakening further to Rs 93.46 in April. This depreciation increases import costs in rupee terms, making domestic coal auctions more competitive despite premium increases.

However, freight rate volatility represents another critical transmission vector, as shipping costs directly impact delivered pricing for imported coal. Supramax vessel rates for Indonesian routes and larger vessel rates for Atlantic coal affect the competitiveness threshold that domestic auctions must exceed to trigger increased import substitution.

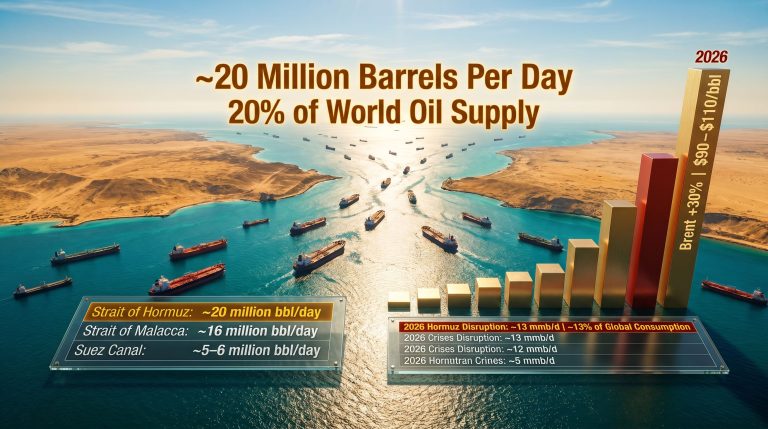

Geopolitical Risk Assessment and Energy Security Concerns

Middle Eastern tensions create multifaceted impacts on global energy markets that extend far beyond direct regional supply disruptions. The recent escalation involving US-Iran conflicts demonstrates how geopolitical risk premiums propagate through interconnected commodity markets, affecting coal, petroleum products, and freight rates simultaneously. In addition, these trade war strategies reveal how quickly market dynamics can shift during periods of international uncertainty.

Risk Transmission Pathways:

- Energy supply constraints: Potential LNG and oil production disruptions affecting global energy balances

- Maritime route security: Strait of Hormuz vulnerability impacting shipping costs and delivery reliability

- Financial market contagion: Risk-off sentiment increasing commodity volatility and hedging premiums

- Strategic stockpiling behaviour: Industrial buyers accelerating inventory accumulation during uncertainty periods

Government responses indicate systematic preparation for potential supply disruptions. Delhi's directive for thermal power utilities to prepare for harsh summer conditions reflects strategic inventory building, while the restart order for Tata Power's 4GW imported coal facility in Gujarat demonstrates emergency capacity activation protocols.

The Philippines' implementation of energy conservation measures, including increased reliance on coal-fired generation, illustrates regional responses to similar geopolitical pressures. Their establishment of a $33.2 million emergency fund for fuel security and stockpiling up to 2 million barrels demonstrates the scale of contingency planning across Asia-Pacific energy markets.

Seasonal Demand Patterns and Industrial Requirements

Pre-summer power generation preparation creates predictable demand surges that amplify auction premium volatility during critical periods. The March 2026 premium spike from 35% to 45% correlates directly with utilities' inventory building ahead of peak cooling demand seasons.

Seasonal Demand Drivers:

- Summer cooling load preparation: March-April inventory accumulation for May-June peak demand

- Monsoon logistics planning: June-September transportation constraint hedging

- Post-monsoon restocking: October-November inventory replenishment cycles

- Industrial production scheduling: Year-round operations with optimised inventory management

Regional variations in seasonal patterns reflect different supply chain dependencies and infrastructure constraints. Coastal regions with import access may exhibit different inventory cycles compared to inland areas reliant on domestic rail transport, creating arbitrage opportunities during peak demand periods.

Industrial buyers optimise working capital through sophisticated inventory management strategies that balance carrying costs against supply security risks. Just-in-time delivery works during stable periods, but geopolitical uncertainty drives strategic stockpiling behaviour that amplifies spot market demand.

Regional Analysis: Coal Quality Specifications and End-User Preferences

Northern Coalfields: Premium Grade Production Centres

Northern Coalfields' achievement of 80% auction premiums in March 2026 reflects superior coal quality characteristics and strategic positioning within India's industrial landscape. The region specialises in higher calorific value coal grades that command premium pricing due to their efficiency advantages in industrial applications.

Technical specifications for Northern Coalfields production emphasise:

- GAR content: 4,200-4,400 kcal/kg for G6 grades achieving 45% premiums

- Transportation advantages: Proximity to major industrial hubs reducing logistics costs

- Infrastructure capacity: Advanced rail connectivity supporting high-volume deliveries

- Quality consistency: Reliable specifications reducing procurement risk for industrial buyers

Buyer concentration patterns in northern regions reflect the presence of major sponge iron and cement manufacturing facilities that require consistent fuel specifications. The premium pricing reflects not only quality advantages but also supply chain reliability and reduced transportation costs compared to alternative sourcing regions.

South Eastern Coalfields: Volume Leadership and Market Access

South Eastern Coalfields recorded 70% average premiums while demonstrating the market's highest individual auction result of 171% for G10 grade coal from the Amadand mine. This extreme premium variation highlights the importance of specific quality characteristics and delivery terms in auction dynamics.

The G10 grade coal achieving 171% premium represents GAR 3,100-3,400 kcal/kg specifications that serve specialised industrial applications. Despite lower calorific content compared to premium grades, certain industrial processes require specific coal characteristics that command significant premiums during supply-constrained periods.

Volume leadership positions SECL as a critical supplier for industrial buyers seeking to diversify sourcing while maintaining quality standards. The region's production capacity and infrastructure development support both domestic consumption and potential export opportunities, creating additional market dynamics.

Eastern Coalfields: Traditional Mining Regions and Market Evolution

Eastern Coalfields achieved 48% average premiums, representing the most moderate pricing among major subsidiaries while maintaining significant market share in traditional industrial applications. This positioning reflects the region's role in supplying cost-sensitive applications where quality premiums are less justified.

Historical production trends in eastern regions demonstrate ongoing modernisation efforts aimed at improving operational efficiency and environmental compliance. These investments enhance long-term competitiveness while addressing regulatory requirements that affect operational permits and expansion potential.

Consequently, the region's strategic positioning within India's energy transition landscape involves balancing traditional coal supply roles with emerging requirements for cleaner production technologies and improved environmental performance standards.

Industry-Specific Impact Assessment

Sponge Iron Manufacturing: Raw Material Cost Optimisation

Sponge iron producers have fundamentally restructured their procurement strategies in response to international price volatility, increasing domestic coal utilisation from 30-40% to approximately 80% of their fuel requirements. This dramatic shift reflects the economic benefits of domestic sourcing during periods of elevated import prices.

Sponge Iron Cost Analysis:

| Cost Component | Domestic Coal Scenario | Import Coal Scenario | Economic Impact |

|---|---|---|---|

| Raw material cost per tonne | Rs 8,000-9,000 | Rs 12,000-14,000 | 30-35% savings |

| Energy content per unit | Rs 1.85/unit | Rs 2.40/unit | 23% efficiency advantage |

| Supply security benefit | 80% domestic blend | 30-40% domestic blend | Reduced volatility exposure |

Production cost pressures from rising auction premiums have pushed sponge iron prices higher by 5-7% in key manufacturing centres like Raipur. However, these increases remain economically justified compared to import alternatives, maintaining domestic sourcing advantages despite premium escalation.

Non-integrated sponge iron units demonstrate the most aggressive domestic substitution strategies, with some facilities switching entirely to domestic coal to protect profit margins. This behaviour illustrates the flexibility advantages of smaller-scale operations compared to integrated steel producers with more complex supply chain requirements.

Cement Industry: Energy Mix Rebalancing Strategies

Cement manufacturers face complex fuel choice decisions involving coal, petroleum coke, and alternative fuel integration based on relative pricing and operational flexibility requirements. The cost of NAR 4,000 kcal/kg auction coal increased 11% to approximately Rs 8,000 per tonne delivered to plant, raising per-unit energy costs from Rs 1.60 to Rs 1.85 per unit.

Despite auction premium increases, domestic coal remains economically attractive compared to imported alternatives priced at Rs 2.40 per unit based on $150/tonne cfr pricing for NAR 6,900 kcal/kg Northern Appalachian coal. This 23% cost advantage supports continued domestic procurement despite premium volatility.

Cement Industry Fuel Switching Analysis:

- Petroleum coke cfr India (6.5%): $160/tonne (+24% since conflict began, +36% year-to-date)

- Imported coal (NAR 6,900): $150/tonne cfr equivalent to Rs 2.40/unit energy cost

- Domestic auction coal (NAR 4,000): Rs 8,000/tonne equivalent to Rs 1.85/unit energy cost

Capital expenditure considerations for fuel handling infrastructure influence long-term procurement strategies. Facilities with petroleum coke handling capabilities maintain operational flexibility to optimise fuel mix based on relative pricing, while coal-only facilities rely more heavily on domestic auction markets.

Power Generation: Grid Stability and Fuel Security Priorities

Thermal power utilities operate under different constraints compared to industrial buyers, relying primarily on long-term Coal India contracts rather than spot auction markets. Their limited auction participation focuses on small spot volumes for operational flexibility rather than baseload fuel requirements.

Government directives for summer preparation demonstrate systematic energy security planning that extends beyond market-driven procurement. The restart order for Tata Power's 4GW facility indicates emergency capacity activation protocols designed to maintain grid stability during peak demand periods.

Power Sector Strategic Responses:

- Emergency capacity activation: Government-directed restart of 4GW imported coal facility

- Summer preparation protocols: Delhi directive for enhanced thermal utility readiness

- Inventory management: Strategic stockpiling ahead of peak cooling demand seasons

- Fuel diversification: Coastal plants utilising Indonesian imports while inland facilities rely on domestic supplies

Independent Power Producers demonstrate more market-responsive behaviour in auction participation, reflecting their commercial operating models compared to state-controlled utilities with regulated pricing structures and supply obligations.

Comparative International Context: Global Coal Market Interconnectedness

Indonesian Coal Export Dynamics and Regional Pricing Influence

Indonesia's position as the dominant supplier to Asia-Pacific coal markets creates powerful price transmission mechanisms that influence regional auction dynamics. The GAR 4,200 kcal/kg benchmark serves as a critical reference point for Indian industrial buyers evaluating domestic versus import alternatives.

Indonesian Coal Market Characteristics:

- Primary demand sources: China, India, Japan, South Korea, and Southeast Asian power markets

- Quality specifications: Range from GAR 3,400 to GAR 6,300 kcal/kg serving diverse applications

- Shipping infrastructure: Dedicated export terminals in Kalimantan and Sumatra with Supramax/Panamax capabilities

- Supply chain efficiency: Integrated mining-to-port operations reducing logistical complexity

Indonesian coal price volatility reflects both domestic policy decisions and international demand fluctuations. Export quotas, royalty adjustments, and environmental regulations create supply-side constraints that amplify price movements during demand surge periods.

Furthermore, the recent 33% year-to-date price increase demonstrates how quickly regional supply-demand imbalances can develop, particularly when geopolitical events disrupt alternative supply chains and increase demand for "safe" sourcing regions.

Australian Premium Coal Markets and Price Discovery Mechanisms

Newcastle NAR 5,500 kcal/kg coal serves as the international reference standard for higher-quality thermal coal markets, with 24% year-to-date price increases reflecting global energy market stress. Australian coal quality consistency and established infrastructure support premium pricing compared to alternative origins.

Australian Coal Market Structure:

- Quality advantage: Higher calorific content and lower impurities commanding premium pricing

- Infrastructure capacity: Port capacity constraints creating supply bottlenecks during peak demand

- Contract mechanisms: Mix of long-term agreements and spot market exposure

- Geographic advantages: Proximity to Asian demand centres reducing shipping costs and time

Long-term contract structures in Australian markets provide price stability for major buyers while spot market exposure creates volatility during supply disruption periods. This dual-market approach influences price discovery mechanisms that cascade through regional markets.

South African Coal Trade Flows and Specialised Applications

South African coal markets demonstrate the highest price volatility with 31% year-to-date increases, reaching $96.11 per tonne fob Richards Bay. This performance reflects both supply chain constraints and specialised quality characteristics demanded by specific industrial applications.

Richards Bay terminal operations face capacity constraints that limit export flexibility during high-demand periods, contributing to price volatility. The terminal's role as the primary export gateway creates bottleneck effects when shipping demand exceeds handling capacity.

South African Coal Specifications:

- High fixed carbon content: Preferred for sponge iron and specialty metallurgical applications

- Quality consistency: Established mining operations with reliable specifications

- Shipping distance: Longer routes to Asian markets increasing freight sensitivity

- Infrastructure limitations: Port capacity constraints affecting export flexibility

Risk Management and Strategic Procurement Frameworks

Currency Hedging Strategies for Import-Dependent Industries

Rupee volatility creates additional complexity for import-dependent industries, with the currency weakening from Rs 90.76 per dollar in February to Rs 93.46 in early April 2026. This depreciation increases landed costs for imported coal while making domestic auction participation relatively more attractive despite premium increases.

Currency Risk Management Approaches:

- Natural hedging: Increased domestic sourcing reducing foreign exchange exposure

- Forward contracts: Fixed exchange rate agreements for planned import volumes

- Option strategies: Protective mechanisms against adverse currency movements

- Operational flexibility: Ability to switch between domestic and import sources based on delivered cost calculations

Industrial buyers with significant import exposure maintain sophisticated treasury functions to manage currency risk, while smaller operations rely more heavily on natural hedging through domestic procurement strategies.

Supply Chain Resilience Building and Contingency Planning

Multi-source procurement strategies become essential during volatile periods, requiring industrial buyers to maintain qualified supplier relationships across multiple geographic regions and quality specifications. This diversification approach reduces concentration risk while maintaining operational flexibility.

Resilience Framework Components:

- Vendor diversification: Qualified suppliers across multiple coalfields and international sources

- Inventory optimisation: Strategic stockpiling during stable periods to hedge disruption risk

- Transportation redundancy: Multiple delivery modes and route options reducing logistics vulnerability

- Quality flexibility: Operational capability to utilise various coal grades based on availability and pricing

Emergency stockpiling protocols require sophisticated working capital management as inventory carrying costs must be balanced against supply security benefits. Industries with seasonal demand patterns optimise these trade-offs through predictive procurement planning.

Long-term Energy Security Planning and Investment Priorities

Infrastructure development requirements for efficient coal distribution include rail capacity expansion, port facility upgrades, and regional distribution networks capable of handling increased domestic production volumes. These investments require coordinated planning between government and private sector stakeholders.

Technology adoption opportunities include automated coal handling systems, quality testing infrastructure, and logistics optimisation platforms that reduce operational costs while improving supply chain visibility and reliability.

Investment Priority Areas:

- Mining capacity expansion: Domestic production increases to reduce import dependency

- Transportation infrastructure: Rail and road capacity for efficient distribution

- Quality assurance systems: Testing and certification capabilities ensuring specification compliance

- Digital transformation: Supply chain visibility and optimisation technologies

Environmental compliance requirements increasingly influence investment priorities as regulatory frameworks evolve to address air quality and carbon emission concerns, requiring balanced approaches that maintain energy security while meeting environmental objectives.

The next major ASX story will hit our subscribers first

Market Outlook and Strategic Implications

Short-term Price Trajectory Projections

Geopolitical risk premiums embedded in current coal pricing reflect market expectations of prolonged Middle Eastern tensions and their cascading effects on global energy supply chains. Duration expectations for these premiums depend largely on conflict resolution timelines and alternative supply chain development.

Seasonal demand patterns suggest continued pressure on auction premiums through the summer cooling season, with potential moderation during monsoon periods if international prices stabilise. However, transportation constraints during monsoon season may offset international price benefits.

Price Trajectory Factors:

- Geopolitical resolution: Conflict de-escalation reducing risk premiums

- Seasonal patterns: Summer demand peaks followed by monsoon moderation

- International market recovery: Global supply chain normalisation timelines

- Domestic capacity utilisation: Coal India production and distribution efficiency

Industrial buyer behaviour demonstrates adaptive capacity through blend ratio adjustments and sourcing diversification, suggesting market mechanisms can accommodate moderate price volatility without fundamental supply disruptions.

Structural Changes in Global Energy Markets

Energy transition impacts on coal demand fundamentals create long-term uncertainty about investment priorities and capacity planning requirements. However, near-term energy security concerns may delay transition timelines as governments prioritise supply reliability over environmental objectives. This mirrors broader global trends in us tariffs & inflation where policy decisions increasingly influence energy market dynamics.

Carbon pricing mechanisms remain nascent in many Asian markets, limiting their immediate impact on fuel choice economics. However, evolving regulatory frameworks suggest increasing importance of emissions considerations in procurement decision-making.

Structural Evolution Trends:

- Technology disruption: Efficiency improvements in coal utilisation and alternative energy integration

- Regulatory development: Environmental compliance requirements affecting operational costs

- Infrastructure modernisation: Digital transformation in supply chain management

- Market concentration: Consolidation trends among suppliers and buyers

The emergence of hybrid energy systems combining traditional coal-fired generation with renewable sources creates new operational requirements that influence fuel procurement strategies and inventory management approaches.

Policy Framework Evolution and Regulatory Considerations

Government intervention mechanisms demonstrated during recent market stress include emergency capacity activation orders and strategic utility directives for summer preparation. These interventions establish precedents for future crisis response protocols.

International trade policy adjustments may include bilateral energy agreements designed to enhance supply security and reduce dependence on volatile spot markets. Regional cooperation frameworks could emerge to coordinate emergency response capabilities.

Regulatory Development Areas:

- Emergency response protocols: Government intervention authorities during supply crises

- Environmental compliance: Air quality and emission standards affecting operational permits

- International agreements: Bilateral and multilateral energy security cooperation

- Market structure reforms: Auction mechanism improvements and transparency enhancements

Energy security prioritisation may influence domestic mining development policies, including expedited permitting processes and infrastructure investment support for strategic capacity expansion projects.

Investment and Business Strategy Considerations

Capital Allocation Priorities for Energy-Intensive Industries

Fuel flexibility investments enable industrial operators to optimise procurement strategies based on relative pricing and availability conditions. These capabilities require significant capital commitments but provide long-term operational advantages during volatile periods.

Investment Framework Considerations:

- Operational flexibility: Multi-fuel capability reducing procurement constraints

- Supply chain optimisation: Inventory management and logistics efficiency improvements

- Technology upgrades: Efficiency enhancements reducing per-unit fuel requirements

- Geographic diversification: Production facility location strategies optimising access to multiple supply sources

Energy efficiency investments provide natural hedging against fuel cost volatility by reducing consumption requirements per unit of production output. These projects often justify investments through operational cost savings independent of procurement strategies.

Financial Performance Impact Assessment

Margin pressure analysis across industrial sectors reveals differential vulnerability to coal price volatility based on cost structure characteristics and pricing power with customers. Sponge iron and cement industries demonstrate significant exposure due to energy intensity and competitive pricing constraints.

Working capital requirements increase during volatile periods as strategic inventory management becomes more critical for supply security. This creates cash flow implications that must be balanced against operational benefits of increased stock levels.

Financial Impact Metrics:

- Cost structure sensitivity: Energy costs as percentage of total production costs

- Pricing power: Ability to pass through cost increases to customers

- Working capital intensity: Inventory investment requirements for supply security

- Credit risk exposure: Supplier payment terms and counterparty risk management

Credit risk evaluation becomes more complex as energy cost volatility affects customer payment patterns and supplier financial stability, requiring enhanced due diligence and monitoring capabilities.

Strategic Partnership Opportunities and Market Positioning

Vertical integration opportunities in coal value chains may provide supply security benefits while capturing margin improvements through direct sourcing arrangements. These strategies require significant capital commitments and operational expertise development.

Joint venture structures enable risk sharing and cost optimisation through pooled procurement volumes and shared infrastructure investments. Collaborative approaches become more attractive during high-volatility periods when individual risk management becomes costlier.

Partnership Strategy Options:

- Vertical integration: Direct mining investments or long-term supply agreements

- Horizontal collaboration: Industry consortiums for pooled procurement

- Technology partnerships: Efficiency improvement and alternative fuel development

- Infrastructure sharing: Transportation and handling facility joint investments

Technology collaboration opportunities include efficiency improvement initiatives, alternative fuel development programmes, and digital supply chain optimisation platforms that provide competitive advantages through operational excellence.

Market positioning strategies during volatile periods focus on maintaining operational flexibility while building competitive advantages through superior supply chain management and cost optimisation capabilities that enable market share gains when competitors face constraints. For instance, companies must consider how oil price movements can affect overall energy cost calculations and procurement strategies.

Adapting to Global Economic Policy Shifts

The intersection of international trade policies and energy procurement strategies requires careful consideration of tariff economic implications that extend beyond immediate coal market dynamics. Trade policy uncertainties create additional layers of complexity in long-term procurement planning.

Industrial operators must monitor evolving trade relationships between major economies, as policy changes can significantly impact coal import duties, freight costs, and alternative sourcing opportunities. This requires sophisticated scenario planning capabilities that incorporate geopolitical risk assessment alongside traditional market analysis.

The effectiveness of bilateral energy agreements and regional cooperation frameworks depends largely on stable international relationships. Consequently, companies with exposure to international coal markets must develop adaptive strategies that can function across various policy environments.

Conclusion

The intersection of geopolitical uncertainty, seasonal demand patterns, and structural market evolution creates a complex operating environment where traditional procurement strategies require fundamental reassessment. Organizations that successfully adapt to these changing conditions through strategic flexibility, operational efficiency improvements, and sophisticated risk management will emerge stronger as markets eventually stabilise.

Success in this environment demands recognition that coal markets operate within broader energy system dynamics where supply security often trumps cost optimisation during crisis periods. The ability to maintain operations whilst competitors face constraints provides strategic opportunities for market share expansion and competitive positioning improvement that extend beyond immediate procurement cost advantages.

When india coal auction prices rise on seaborne volatility, the resulting market dynamics reveal the interconnected nature of global energy supply chains and the importance of strategic procurement planning in maintaining operational resilience during periods of international uncertainty.

Looking to Navigate the Complex Coal Market Landscape?

Discovery Alert's proprietary Discovery IQ model provides real-time insights on Australian mining companies exposed to coal and energy sector developments, helping investors identify opportunities arising from global market volatility. When geopolitical events trigger commodity price shifts and supply chain disruptions, subscribers receive instant alerts about significant discoveries that could benefit from changing market dynamics. Begin your 14-day free trial today to stay ahead of market movements affecting resource investments.