June 27, 2026

The Geopolitics of Cooking Fuel: How a Maritime Chokepoint Brought India's Energy System to Its Knees

When geopolitical analysts discuss the Strait of Hormuz, the conversation typically gravitates toward crude oil tankers, petrochemical giants, and sovereign wealth funds. Rarely does it begin with the humble gas cylinder sitting in a household kitchen. Yet the escalation of US-Iran hostilities in early 2026 forced precisely that reframe onto policymakers in New Delhi, exposing a structural fragility in India's energy architecture that extends far beyond barrel prices and into the daily lives of hundreds of millions of people.

India ends restrictions on commercial gas after the Strait of Hormuz situation eased in late June 2026, marking a pivotal moment not just for LPG supply chains, but for how emerging economies must now think about energy security in an era of recurring geopolitical disruption. Furthermore, understanding India's LNG import tax framework provides essential context for why supply disruptions carry such outsized consequences for the broader Indian energy market.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is Unlike Any Other Shipping Lane

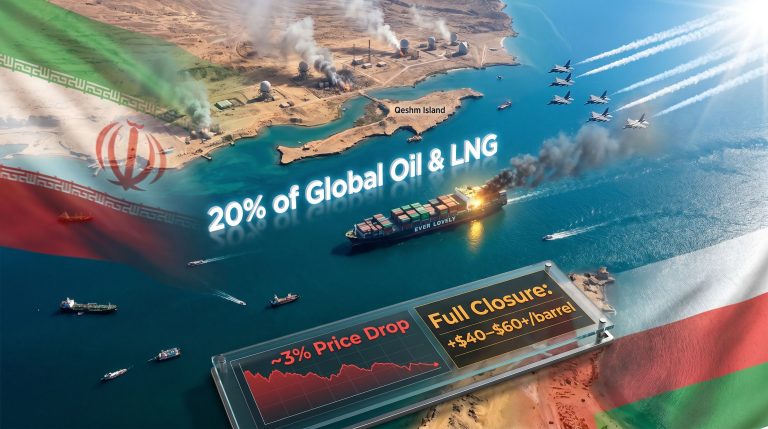

No other maritime passage on earth concentrates so much of the world's energy flow through such a narrow geographic point. Approximately one-fifth of all global oil and natural gas volumes transit the Strait of Hormuz under normal operating conditions, according to the US Energy Information Administration. The waterway, which measures roughly 33 kilometres at its narrowest navigable point between Iran and Oman, functions as the circulatory valve of the global energy system.

For most commodity-importing nations, a disruption to this corridor creates a pricing problem. For India, it creates an existential supply problem.

As the world's second-largest LPG importer, India sources the overwhelming majority of its cooking gas volumes from West Asian producers, almost all of which route their exports through the strait. This is not merely a concentration-of-supplier issue. It is a concentration-of-corridor issue, meaning that even supplier diversification within the Gulf region offers limited protection when the single exit route is compromised.

The Cooking Fuel Variable That Complicates Everything

Unlike crude oil, which feeds industrial processes and transport systems where substitution options exist over medium-term horizons, LPG occupies a different position in India's energy stack. It is the primary cooking fuel for hundreds of millions of Indian households, many of which have no viable short-term alternative.

This creates an asymmetric vulnerability that policymakers must manage differently from industrial fuel shortages. A crude oil disruption can theoretically be absorbed through strategic reserves, demand reduction, or fuel switching over weeks and months. An LPG disruption translates almost immediately into retail shortages, price spikes, and social tension. The political sensitivity of cooking fuel costs in India has historically been acute, which explains the speed and decisiveness with which the government intervened when the crisis began.

From Escalation to Emergency: The Timeline of India's LPG Crisis

The sequence of events that culminated in India's commercial LPG restrictions unfolded rapidly once US and Israeli military strikes escalated tensions with Iran beginning in late February 2026. Indeed, the oil market disruption risks associated with such geopolitical flashpoints had long been flagged by analysts, yet the speed of this crisis still caught supply chains off-guard.

| Event | Approximate Timing |

|---|---|

| US and Israel strikes escalate tensions with Iran | Late February 2026 |

| Strait of Hormuz closure disrupts maritime traffic | Following escalation |

| India imposes restrictions on non-domestic packed LPG | Crisis onset |

| Bulk LPG supplies suspended entirely | Crisis onset |

| Indian tanker Shivalik navigates strait post-diplomatic talks | Pre-resolution phase |

| Two Indian LPG tankers deliver approximately 92,000 tonnes of cooking gas | Short-term relief phase |

| Iran-US deal signed, waterway reopened | June 2026 |

| India lifts commercial LPG restrictions | June 25-27, 2026 |

The government's response followed a recognisable triage logic: protect household consumers first, ration commercial and industrial users, and manage demand through pricing signals. LPG prices were raised during the crisis period as a deliberate demand-management mechanism, a move that carries significant political cost in a country where cooking fuel affordability is treated as a social policy priority.

The navigation of the Indian tanker Shivalik through the strait during diplomatic negotiations provided an early signal that a resolution pathway existed. Together with a second vessel, the Shivalik delivered approximately 92,000 tonnes of cooking gas, offering short-term supply relief before the broader diplomatic agreement was finalised.

The Backlog That Signals Incomplete Normalisation

Despite the diplomatic breakthrough that enabled India to lift commercial LPG restrictions, approximately 22 Indian-registered vessels remained awaiting clearance to transit the Strait of Hormuz at the time the announcement was made. This vessel backlog is a tangible indicator that operational normalisation continues to lag behind diplomatic normalisation, and that full supply chain recovery will require additional weeks to complete.

This distinction matters for market interpretation. A diplomatic agreement reopening a waterway and the physical restoration of pre-crisis shipping flows are two separate events separated by real-world logistics, vessel positioning, port scheduling, and cargo confirmation processes. As reported by OilPrice.com, the Hormuz shutdown threw India's LPG market into considerable chaos, underlining just how exposed the country's import architecture truly was.

Dissecting the Government's Two-Part Restoration Decision

India's petroleum ministry announcement in late June 2026 contained two distinct components, and understanding the difference between them is critical for assessing how confident the government actually is in sustained supply normalisation.

Component 1: Full restoration of non-domestic packed LPG

Commercial and industrial packed LPG supplies were returned to pre-crisis consumption levels with no volume cap applied.

Component 2: Partial relaxation of bulk LPG suspension

Bulk LPG, which had been suspended entirely at the crisis onset, was restored to only 50% of pre-crisis consumption levels.

The asymmetry between these two decisions is revealing. A government that was fully confident in supply chain stability would have restored both categories to 100% simultaneously. The decision to hold bulk LPG at a 50% threshold communicates ongoing caution, a deliberate hedge against the possibility that the Iran-US diplomatic agreement remains fragile and that supply disruption could re-emerge.

Analysts tracking India's energy policy posture should treat the progressive lifting of bulk LPG restrictions as a leading indicator of the government's real-time confidence assessment in Strait of Hormuz stability.

Which Nations Share India's Exposure?

India is not alone in its vulnerability to Strait of Hormuz disruptions, though its LPG dependency makes its exposure particularly acute in the cooking fuel dimension.

| Country | Primary Exposure | Dependency Level |

|---|---|---|

| India | LPG, crude oil imports | Very High |

| Japan | LNG, crude oil | Very High |

| South Korea | Crude oil, LNG | High |

| China | Crude oil | High |

| European importers | LNG spot market | Moderate |

Japan and South Korea also faced significant exposure during the 2026 crisis, given their near-total dependence on Gulf crude and LNG. However, both countries maintain more developed strategic reserve infrastructure than India, providing a longer buffer window before domestic supply impacts become acute. This difference in reserve capacity is one of the less-discussed dimensions of comparative energy security vulnerability among Asia-Pacific importers.

India's Structural Response: Coal Gasification and the Long-Term Pivot

In the month preceding the LPG restriction lift, the Indian government approved a nearly USD $4 billion coal gasification expansion plan. This initiative aims to convert coal into synthetic gas through a process that involves partial oxidation at high temperatures, producing a combustible gas mixture that can substitute for imported natural gas and LPG in certain industrial and power generation applications.

Coal gasification is not a new technology. It has been employed commercially for decades in China, South Africa, and parts of Europe. What is notable about India's move is the scale of the investment commitment and the explicit framing of it as an energy security mechanism rather than purely a commercial or environmental decision.

Short-Term Relief vs. Long-Term Structural Hedge

| Response Category | Measure | Timeframe |

|---|---|---|

| Short-term demand management | LPG price increases | Immediate |

| Short-term supply relief | Diplomatic tanker negotiations | Weeks |

| Medium-term supply restoration | Strait deal, restriction lift | Months |

| Long-term structural hedge | $4 billion coal gasification expansion | Multi-year |

The critical limitation of the coal gasification pivot is temporal. Even accelerated project timelines for large-scale gasification infrastructure operate on multi-year development, construction, and commissioning horizons. This means the $4 billion program, while strategically sound as a long-term hedge, would have offered zero near-term relief had the Strait of Hormuz remained closed for an extended period.

This temporal gap between long-term structural solutions and short-term supply crises is a fundamental challenge in energy security planning that is frequently underappreciated in policy discussions. The speed at which the 2026 crisis moved from diplomatic tension to domestic cooking fuel shortages illustrates why strategic reserve capacity and genuine supplier diversification cannot be deferred to multi-year infrastructure timelines.

What a Six-Month Closure Would Have Meant

If the Strait of Hormuz had remained closed for a full six months rather than the period actually experienced, India would have confronted a compounding cascade: LPG retail shortages escalating into household energy insecurity across hundreds of millions of homes, industrial gas rationing disrupting manufacturing and chemical production, significant GDP growth compression, and the prospect of social unrest linked directly to cooking fuel unavailability. The coal gasification program, however strategically valuable over a five-to-ten-year horizon, would have been operationally irrelevant to that scenario.

Diversification Pathways India Must Now Accelerate

The 2026 crisis has functioned as a stress test of India's energy import architecture. Three structural gaps were exposed:

- Supplier concentration within a single maritime corridor: Even if India were sourcing LPG from multiple Gulf states, all volumes still exit through the same chokepoint, making multi-supplier strategies within the Gulf region an inadequate diversification response.

- Absence of meaningful alternative supply corridors: India currently lacks developed procurement relationships with non-Gulf LPG exporters of sufficient scale to substitute during a Gulf disruption. The US, Australia, and certain African producers represent potential alternative sources, but building the trading relationships, shipping contracts, and terminal infrastructure to activate them at volume takes years, not weeks.

- Insufficient strategic reserve buffer: India's LPG storage infrastructure, while expanding, does not currently provide the buffer duration required to absorb a multi-month supply disruption without triggering retail shortages. Comparable Asian economies with greater strategic reserve capacity demonstrated meaningfully more resilience during the same crisis period.

The Hidden Cost of Commodity Concentration Risk

One dimension of this crisis that receives insufficient analytical attention is the correlation between geopolitical risk and commodity concentration risk. Energy security frameworks often treat supplier diversification as the primary risk mitigation tool. The 2026 Strait of Hormuz closure demonstrated that corridor concentration can render supplier diversification largely irrelevant during a physical closure event.

This insight has implications for how India, and other heavily Gulf-dependent importers, should structure their energy security frameworks. The relevant unit of analysis for diversification is not the supplier but the supply corridor. In addition, the global LNG supply outlook for 2025 and beyond makes clear that corridor constraints will remain a defining vulnerability for Asian importers well into the decade ahead.

Furthermore, the broader energy transition demand pressures reshaping global commodity markets mean that India's energy export challenges are likely to intensify, particularly as the country attempts to balance domestic energy security with its longer-term decarbonisation commitments. Indeed, India's energy export challenges mirror those faced by other resource-dependent economies navigating an increasingly volatile geopolitical environment.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

Why was commercial LPG restricted before household LPG?

The priority logic was straightforward: household cooking fuel represents a social and political necessity that the government determined must be protected even at the cost of commercial and industrial supply disruption. By rationing the non-domestic segment first, policymakers preserved retail availability for the hundreds of millions of Indian households dependent on LPG cylinders for daily cooking.

What is the significance of the 50% bulk LPG restoration threshold?

The 50% figure reflects deliberate policy caution rather than full supply confidence. It signals that the government is hedging against potential re-escalation of geopolitical tensions near the Strait of Hormuz, and that full normalisation will be phased based on ongoing supply chain assessment rather than declared in a single announcement.

How does coal gasification reduce import dependency?

Coal gasification converts solid coal into a combustible synthetic gas through high-temperature partial oxidation. The resulting gas can replace imported natural gas in industrial and power generation applications. Since India holds substantial domestic coal reserves, scaling gasification capacity converts an import dependency into a domestically sourced energy stream, reducing exposure to Gulf supply disruptions over a multi-year horizon.

What is the Shivalik tanker's place in the crisis narrative?

The Shivalik was among the first Indian LPG vessels to successfully transit the Strait of Hormuz following diplomatic negotiations during the crisis. Its passage, alongside a second tanker, delivered approximately 92,000 tonnes of cooking gas to India. As confirmed by The Statesman, the government subsequently lifted all sectoral restrictions on commercial LPG supply in the days following the reopening of the strait, confirming the practical effectiveness of the tanker operation as a supply restoration template.

Key Takeaways for Energy Policy and Market Watchers

- India ends restrictions on commercial gas following the Strait of Hormuz easing, representing a functional but incomplete normalisation, not a full declaration of supply security.

- The 50% bulk LPG restoration is the most important signal in the government's announcement, communicating continued caution about supply chain stability.

- The 22 Indian vessels still awaiting transit clearance at the time of the announcement confirm that diplomatic resolution and operational normalisation are not the same event.

- The $4 billion coal gasification program is a strategically rational long-term hedge but offers no protection against short-duration supply shocks of the kind experienced in 2026.

- The structural lesson from this crisis is that India must reframe its energy diversification strategy around corridor diversification, not merely supplier diversification, since the former is the binding constraint that the latter cannot resolve.

- The durability of the Iran-US agreement will remain the single most consequential variable determining whether the current supply normalisation holds or reverses over the months ahead.

This article contains forward-looking analysis and scenario assessments that involve assumptions about geopolitical developments, diplomatic agreements, and energy supply chains. Such projections carry inherent uncertainty and should not be interpreted as investment advice or definitive forecasts. Readers are encouraged to consult independent energy market analysts and primary sources for investment decisions.

For ongoing coverage of India's oil and gas sector and Strait of Hormuz developments, ET EnergyWorld at energy.economictimes.indiatimes.com provides continuous reporting from the region.

Want to Stay Ahead of the Next Major Energy Commodity Disruption?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity data into actionable insights for both short-term traders and long-term investors — explore historic examples of exceptional discovery returns to understand the scale of opportunity these moments can create, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.