July 20, 2026

When Chokepoints Become Crisis Points: India's Oil Vulnerability Laid Bare

Every major oil importing nation carries a version of the same quiet anxiety: that the thin network of maritime corridors threading crude from producer to consumer could, one day, be severed. For decades, this anxiety remained largely theoretical. The Strait of Hormuz, a passage barely 33 kilometres wide at its narrowest navigable point, was treated as an inviolable artery of global commerce, too important to close, too costly to threaten. The escalation of the Iran conflict in early 2026 has shattered that assumption, transforming a theoretical vulnerability into a live operational crisis, with India sitting directly in the firing line.

Understanding why India crude oil stocks drop amid Iran conflict conditions has become one of the most consequential energy market questions of the year. The answer reveals a structural fragility that extends well beyond oil logistics and into the heart of India's macroeconomic stability. Furthermore, crude oil price trends suggest that the pressure on import-dependent economies will intensify before it eases.

When big ASX news breaks, our subscribers know first

India's Import Dependency: A Structural Exposure, Not a Policy Failure

India's position as one of the world's largest petroleum consumers, processing approximately 5 million barrels of oil per day, did not emerge from poor planning. It reflects decades of rapid industrialisation, population growth, and rising middle-class consumption that outpaced the country's domestic production capacity by orders of magnitude.

Unlike nations with deep pipeline connectivity to nearby producers, India relies almost exclusively on seaborne crude deliveries. Tankers carrying Gulf crude must navigate through the Strait of Hormuz, across the Arabian Sea, and into Indian port terminals along the western coastline. This configuration creates a supply chain that functions efficiently in stable geopolitical conditions but becomes acutely fragile when maritime corridors face disruption.

The strategic geography matters enormously here. The Strait of Hormuz serves as the exclusive maritime exit point for crude exports from Iran, Iraq, Kuwait, Qatar, and Bahrain, while Saudi Arabia and the UAE retain partial alternative routing capacity through overland pipelines and Red Sea terminals. When the Strait becomes inaccessible, the countries entirely dependent on it cannot ship a single barrel regardless of how much production capacity remains intact.

This is precisely the scenario that unfolded following the escalation of the Iran conflict in late February 2026. The trade war impact on oil has compounded these existing vulnerabilities, adding layers of complexity to an already stressed global supply environment.

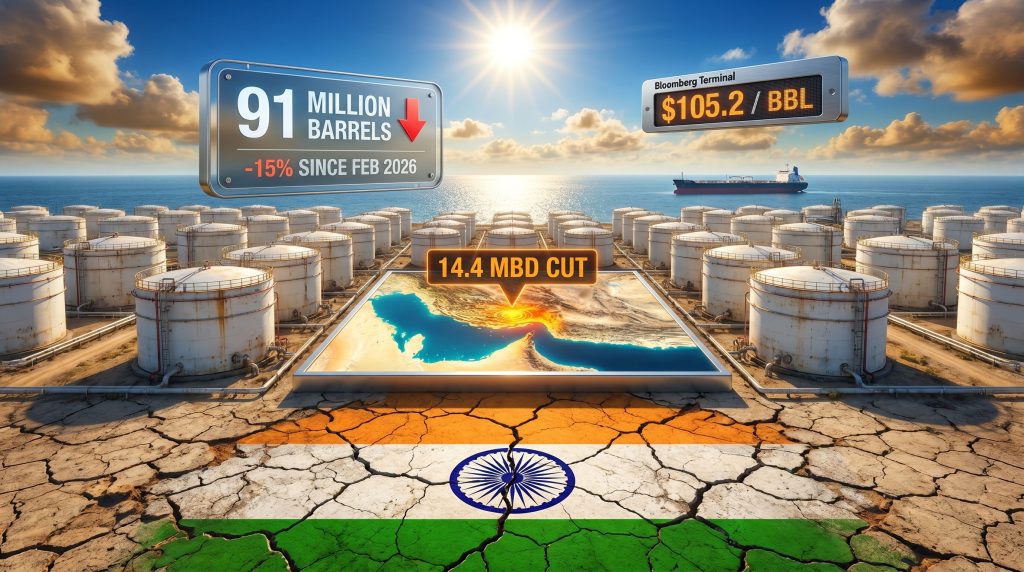

The near-closure of the Strait is estimated to have pulled approximately 14.4 million barrels per day of Gulf oil output below pre-conflict levels, a supply shock of extraordinary magnitude given that global production at this point sits at roughly 95.1 mbd. Saudi Arabia and the UAE have continued exporting through alternative routes, but their combined capacity falls far short of compensating for the volumes eliminated from Iraq and Kuwait.

The Inventory Numbers Telling a Concerning Story

Commodity analytics firm Kpler, which tracks crude storage across strategic petroleum reserves, commercial inventories, and refinery storage tanks, has recorded a striking deterioration in India's crude oil position since the conflict began.

| Metric | Late February 2026 | May 2026 |

|---|---|---|

| Crude Oil Stocks | ~107 million barrels | ~91 million barrels |

| Absolute Decline | – | 16 million barrels |

| Percentage Decline | – | 15% |

| Implied Days of Demand Coverage | ~21 days | ~18 days |

| Government Coverage Estimate | – | ~60 days |

| Import Rate | ~5.0 mbd | ~4.5 mbd |

The divergence between Kpler's 18-day coverage figure and the Indian government's 60-day claim is not a contradiction — it reflects different measurement scopes. Kpler's methodology explicitly excludes pipeline stocks, whereas the government's figure, as clarified by Sujata Sharma, Joint Secretary in the petroleum ministry, incorporates both pipeline inventories and cargoes already loaded onto India-bound vessels at origin ports. Both figures carry analytical validity; they simply measure different things.

What the data consistently shows is that Indian refiners have been drawing down inventories rather than cutting throughput. Crude imports fell from 5.0 mbd to approximately 4.5 mbd, a 10% reduction, but refinery run rates have not declined proportionally. The gap between what is arriving and what is being processed has been bridged through active stock drawdowns, most likely from refinery-level storage tanks rather than the strategic petroleum reserve layer.

According to analysis from Kpler's lead refining analyst, this pattern indicates that operators are prioritising short-term output continuity over long-term buffer preservation. The characterisation of the current drawdown as moderate carries an important conditional: it only holds if Strait of Hormuz access is restored within the near term. The same analysis warns explicitly that India cannot rely on inventory drawdowns indefinitely, and that refineries may eventually need to reduce run rates in line with the reduced oil supply reaching Indian shores.

The Nayara Energy Variable

One factor that has inadvertently softened the inventory decline is the planned maintenance shutdown at Nayara Energy's 400,000 barrels-per-day refinery in Gujarat during April 2026. With this major facility offline for scheduled works, demand on crude stocks was temporarily reduced. Had it remained fully operational through April, the inventory depletion figure would have been materially larger than the 16 million barrel decline recorded.

This maintenance window has now closed. Full capacity returning at this facility will apply fresh pressure to stocks already running well below their February baseline.

A Global Supply Picture Without Recent Precedent

India's inventory stress does not exist in isolation. The broader global oil market is experiencing inventory drawdowns that the International Energy Agency has described as historically record-setting. Oil market volatility at this scale has not been observed in recent memory, and the ripple effects are spreading rapidly across import-dependent economies.

| Period | Global Inventory Change |

|---|---|

| March 2026 | -129 million barrels |

| April 2026 | -117 million barrels |

| Cumulative Loss (Feb-Apr 2026) | -12.8 mbd equivalent |

Global oil output fell by a further 1.8 mbd in April 2026 alone, bringing total worldwide supply to approximately 95.1 mbd. The IEA has explicitly warned that further price volatility is probable as the peak summer demand season approaches, a period when consumption typically rises across both developed and emerging economies simultaneously.

Brent crude has responded predictably. After crossing the psychologically significant $100 per barrel threshold, prices reached approximately $105.2 per barrel by mid-May 2026. For context, this pricing environment represents a structural stress test for any crude import-dependent economy, but the impact is particularly acute for India given the rupee's sensitivity to dollar-denominated commodity costs.

A price level above $100 per barrel does not merely affect the energy sector. It transmits through every layer of the Indian economy via import costs, currency dynamics, inflation, and fiscal pressure simultaneously.

Four Transmission Channels From Oil Shock to Economic Pain

The macroeconomic consequences of elevated crude prices are not abstract. They operate through four distinct and reinforcing channels:

1. Import Bill Expansion

At $105 per barrel, India's annual crude import expenditure increases by tens of billions of dollars compared to a sub-$80 pricing environment. India processes roughly 5 mbd, equating to approximately 1.825 billion barrels annually. Each $10 per barrel price increase therefore adds approximately $18 billion to the annual import bill, directly widening the current account deficit.

2. Currency Depreciation Pressure

Rising dollar-denominated energy imports increase demand for US dollars while simultaneously weakening the rupee. A weaker rupee raises the domestic cost of all imported goods, not just oil, creating a secondary inflationary loop that extends well beyond the energy sector.

3. Fiscal Deficit Widening

If the government opts to absorb fuel price increases through subsidies rather than passing them to end consumers, the fiscal deficit expands correspondingly. This constrains public investment capacity and crowds out other spending priorities at precisely the moment economic pressures are intensifying.

4. Inflationary Pass-Through

Transport fuel costs underpin pricing across virtually every supply chain in India's economy. Higher diesel prices elevate food transport costs, manufacturing logistics, and consumer goods delivery simultaneously, compressing household purchasing power across income brackets.

Prominent Indian banker Uday Kotak publicly advised citizens to prepare for a potential economic shock if tensions across West Asia continue to escalate — a signal that the financial sector views this situation as systemic rather than merely a commodity market event.

How Indian Equity Markets Are Absorbing the Shock

Financial markets have responded to the oil crisis with broad-based selling pressure across major indices. According to Reuters, Indian shares have faced steep declines as the widening Middle East conflict drives oil prices higher, reinforcing the vulnerability of equity markets to energy supply shocks.

| Index | Level (Mid-May 2026) | Movement |

|---|---|---|

| NSE Nifty 50 | 24,176.15 | -0.62% |

| BSE Sensex | 77,328.19 | -0.66% |

| BSE Sensex (May 12) | 75,489.84 | -525.44 points |

| NSE Nifty (May 12) | 23,651.35 | -164.5 points |

Sector-specific pressure has been uneven. State Bank of India declined approximately 6.4% as earnings disappointments combined with macro headwinds to amplify selling. ONGC and Oil India both fell in the 2-3% range as upstream economics came under pressure. Technology, financial services, and energy names bore the heaviest brunt of the selling.

Foreign Institutional Investor outflows have compounded domestic selling pressure, accelerating index declines beyond what fundamentals alone would produce. This is a familiar pattern during commodity shocks: international capital rotates away from high-oil-import-sensitivity economies toward commodity exporters or domestically insulated markets.

Not every sector has suffered equally, however. NTPC in power generation and Bharti Airtel in telecommunications demonstrated relative resilience, reflecting investor rotation toward businesses with limited direct exposure to oil input costs. This rotation behaviour offers a useful signal of how institutional capital is repositioning within India rather than simply exiting.

The next major ASX story will hit our subscribers first

Three Scenarios for What Comes Next

The trajectory from here depends almost entirely on one variable: the duration of Strait of Hormuz restrictions. Furthermore, the broader geopolitical risk landscape will play a defining role in determining how quickly diplomatic solutions can be reached.

Scenario A: Short-Term Resolution (0-60 Days)

Within the current inventory buffer window, Indian refiners can maintain processing rates without operational reductions. Both the Kpler 18-day figure and the government's broader 60-day estimate suggest meaningful near-term cushion exists. If diplomatic progress reopens shipping lanes within two months, the crisis remains manageable without structural economic damage.

Scenario B: Prolonged Disruption (60-120 Days)

As inventory buffers approach depletion, refiners face a binary choice: cut processing rates or source alternative crude at significant premium from suppliers outside the Gulf. US, Russian, and West African producers represent the most viable alternatives, but sourcing at sufficient volume in compressed timeframes carries both logistical and price challenges. Fuel conservation directives would likely intensify.

Scenario C: Extended Closure (120+ Days)

Structural refinery run-rate reductions become unavoidable. Domestic fuel availability tightens meaningfully. Inflationary pressures intensify, fiscal and monetary policy options narrow, and the strategic petroleum reserve framework faces intense operational scrutiny. This scenario represents the transition from a supply disruption to a supply crisis.

The point at which refinery run-rate reductions shift from precautionary to operationally necessary marks a critical threshold. Beyond that point, the economic impact of the Iran conflict becomes embedded in India's domestic economy rather than contained within the energy sector.

Reading Modi's Fuel Conservation Call as a Forward Signal

Prime Minister Narendra Modi's public call for fuel conservation is widely interpreted by energy analysts as a forward-looking policy signal rather than a declaration of immediate emergency. The timing and framing of the directive suggest the government is preparing the public for a trajectory in which current inventory drawdown rates cannot continue indefinitely.

Conservation appeals serve a strategic dual purpose. On the demand side, they reduce the pace at which inventories deplete, extending the runway before run-rate reductions become unavoidable. On the communications side, they begin conditioning public expectations for potential supply adjustments if the Hormuz situation does not resolve promptly.

The analysis from commodity market experts reinforces this reading directly. The assessment that the Prime Minister's conservation call may reflect awareness that refineries could eventually need to reduce processing in line with lower oil supplies arriving from the Gulf represents an unusual degree of convergence between market analytics and policy signalling. Consequently, India crude oil stocks drop amid Iran conflict dynamics are now embedded in the government's own forward planning assumptions.

Importantly, India's strategic petroleum reserves are designed as last-resort buffers rather than operational supply sources. Drawing them down to sustain refinery throughput during a prolonged disruption accelerates the timeline toward a point where no further buffer exists. The government's inclusion of in-transit cargoes and pipeline stocks in its 60-day coverage estimate suggests an awareness of this constraint and a desire to present the most complete picture of available supply rather than relying solely on tank-level inventories.

In addition, global trade disruptions of this magnitude historically produce secondary effects that extend well beyond energy markets, affecting shipping routes, insurance costs, and supply chain reliability across multiple sectors simultaneously.

Frequently Asked Questions

How much have India's crude oil stocks fallen since the Iran conflict began?

India's crude oil inventories have declined by approximately 15%, from around 107 million barrels in late February 2026 to approximately 91 million barrels in May 2026, according to Kpler commodity analytics data.

Why do the government and Kpler give different coverage figures?

Kpler's methodology covers strategic reserves, commercial inventories, and refinery storage tanks but excludes pipeline volumes. The government's broader 60-day estimate incorporates pipeline stocks and cargoes already loaded onto India-bound vessels at origin ports. Both are valid; they measure different components of the total supply picture.

Why haven't Indian refineries cut production yet?

Refiners have been drawing down stored inventory to bridge the gap between reduced imports and maintained processing rates. This is a finite strategy, sustainable only as long as adequate stocks remain.

What does the Nayara Energy maintenance mean for future inventory levels?

The April 2026 maintenance shutdown at Nayara's 400,000 bpd Gujarat facility temporarily reduced crude demand, softening the drawdown rate. With that facility returning to full capacity, inventory depletion pressure is expected to increase.

How is the crisis affecting Indian financial markets?

Both the Sensex and Nifty have recorded significant declines, with energy, financial, and technology sector stocks among the most affected. As reported by the Economic Times, however, certain stocks stand to benefit if a ceasefire were to materialise, highlighting the bifurcated nature of the market response. Foreign Institutional Investor outflows have amplified domestic selling pressure across asset classes.

Key Risk Summary for Investors and Analysts

For those tracking India's energy situation and its market implications, the following factors represent the most critical variables to monitor:

- The duration of Strait of Hormuz restrictions is the single most important variable determining whether this crisis remains manageable or escalates structurally

- India's inventory buffer, measured at 18 days by Kpler methodology or approximately 60 days by government methodology, provides near-term operational stability but not indefinite runway

- Brent crude above $105 per barrel applies simultaneous pressure on the current account, rupee valuation, fiscal position, and consumer inflation

- The return of Nayara Energy's 400,000 bpd Gujarat refinery to full operation removes a temporary demand reduction that had been softening the inventory drawdown rate

- FII outflows from Indian equity markets reflect international capital's assessment of oil-import-sensitivity risk and are unlikely to reverse until supply disruption concerns ease

- The government's conservation directive and the Kpler analyst's assessment that run-rate reductions may eventually become necessary represent converging signals that the current trajectory is not indefinitely sustainable

Disclaimer: This article contains analysis of market conditions, economic projections, and geopolitical scenarios. All figures, projections, and scenario analyses are based on data available as of mid-May 2026 and are subject to significant revision as conditions evolve. Nothing in this article constitutes financial or investment advice. Commodity markets, geopolitical developments, and macroeconomic conditions involve inherent uncertainty, and past patterns do not guarantee future outcomes.

Want to Identify ASX Mineral Discoveries Before the Broader Market Does?

While geopolitical shocks like the Iran conflict expose the fragility of global energy supply chains, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly transforming complex commodity data into actionable investment insights for both short-term traders and long-term investors. Explore Discovery Alert's dedicated discoveries page to understand how major mineral discoveries have historically generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.