June 24, 2026

The Engineering Reality Behind India's Coal Substitution Challenge

Every power system carries embedded assumptions. The turbines, boilers, and fuel handling infrastructure of a generation facility are not neutral machines capable of running on any combustible material fed into them. They are precision systems calibrated for specific fuel properties, and when those properties change, the consequences ripple through efficiency curves, maintenance schedules, and economic models in ways that are rarely visible from the outside.

This engineering reality sits at the heart of one of the most consequential shifts currently underway in global thermal coal markets: India's accelerating effort to substitute domestic coal into power plants that were purpose-built to run on imported fuel. Understanding why this transition is technically difficult, why it is happening now, and what it means for seaborne coal trade requires moving past the headline figures and into the operational mechanics of the fuel switch itself. Furthermore, these coal supply challenges extend well beyond India's borders, reshaping global trade flows in ways that few anticipated just a few years ago.

When big ASX news breaks, our subscribers know first

Why Imported Coal-Based Plants Represent a Unique Engineering Category

The Fuel Quality Gap That Defines the Problem

The fundamental distinction between imported thermal coal and Indian domestic coal comes down to two interrelated parameters: Gross Calorific Value (GCV) and ash content. These two metrics move in opposite directions in the two fuel streams, and that divergence is the source of virtually every operational complication in the India domestic coal use in import-based power plants transition.

Imported thermal coal, primarily sourced from Indonesia, South Africa, and Russia, typically carries a GCV in the range of 5,000 to 6,500 kilocalories per kilogram (kcal/kg), with ash content often below 15%. Indian domestic coal, predominantly sourced from eastern coalfields operated by Coal India and its subsidiaries such as Mahanadi Coalfields and South Eastern Coalfields Limited (SECL), typically carries a GCV in the range of 3,500 to 4,500 kcal/kg, with ash content frequently exceeding 35% and in some grades reaching 45%.

This is not a marginal difference. A boiler designed to process low-ash, high-energy imported coal will face several compounding problems when fed high-ash domestic material:

- Combustion inefficiency: Higher ash loads reduce flame temperature and burn efficiency, increasing unburnt carbon in fly ash.

- Slagging and fouling risk: High-ash coal with certain mineral compositions deposits slag on boiler tubes at rates that can accelerate maintenance cycles and reduce plant availability.

- Handling system stress: Pulverising mills, conveyors, and ash handling systems calibrated for low-ash fuel face significantly higher throughput volumes of inert material.

- Emissions profile changes: Higher ash content alters particulate and sulphur dioxide emissions profiles, creating potential compliance complications.

What the 18.7 GW ICB Fleet Actually Represents

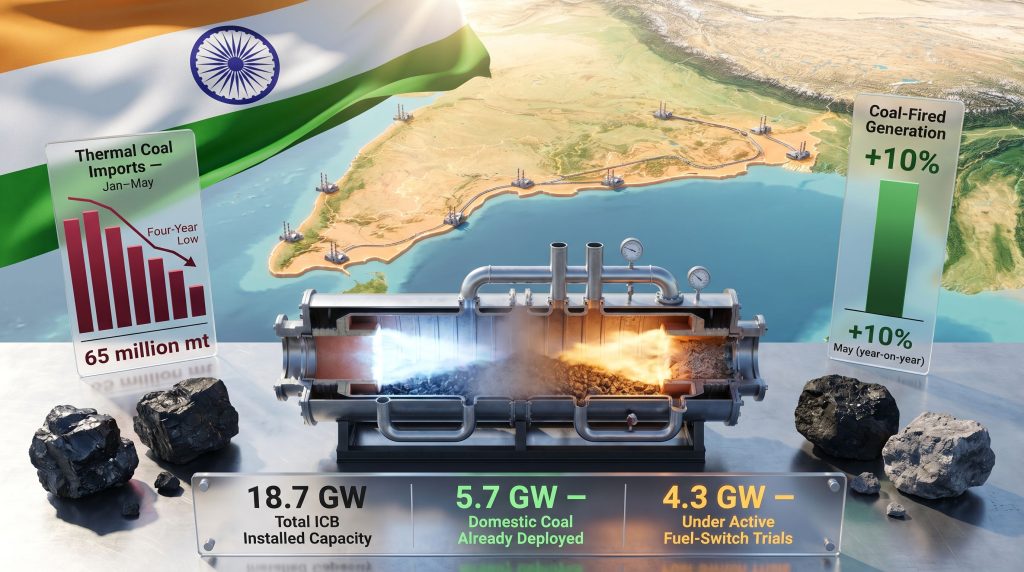

India's imported coal-based (ICB) power plants are concentrated in coastal states, particularly Gujarat, Maharashtra, and Andhra Pradesh, where proximity to port infrastructure minimised the landed cost of seaborne coal. The total installed capacity of this fleet stands at approximately 18.7 GW, representing roughly 9% of India's total coal-fired generation capacity.

These plants were constructed during a period when international coal prices were competitive relative to the logistics cost of transporting domestic coal from inland coalfields to coastal locations. That economic calculus has shifted materially, driven by the sustained elevation of international coal prices since 2021 and the parallel improvement in domestic supply reliability. In addition, the India coal trading exchange proposal reflects how fundamentally these market dynamics are being reconsidered at a policy level.

India's Coal Import Dependency: Key Metrics and What Is Changing

A Statistical Snapshot of the Transition

The scale of India's domestic coal integration into ICB plants, and the corresponding reduction in thermal coal imports, can be understood through the following data:

| Metric | Data Point |

|---|---|

| Total thermal coal imported (FY 2022-23) | ~238 million metric tons (mt) |

| Coal procured by ICB plants (FY 2022-23) | ~20 million mt |

| ICB plants' share of total imports | ~8.4% |

| Total ICB installed capacity | 18.7 GW |

| Domestic coal deployed to ICB plants (2026 YTD) | 5.7 GW equivalent capacity |

| ICB capacity under active fuel-switch trials | 4.3 GW |

| Domestic coal booked by ICB plants (forward) | 16 million mt |

| Thermal coal imports (January-May, current year) | 65 million mt (four-year low) |

The forward booking of 16 million mt of domestic coal by ICB plants is particularly significant. This represents a structural commitment, not an opportunistic spot purchase, and signals that plant operators are internalising the expectation of sustained domestic fuel availability at viable delivered cost.

Supplier Nations Absorbing the Demand Decline

The reduction in Indian ICB plant imports has created measurable disruption in trade flows from the two most affected exporting nations:

- Indonesia: Indian imports fell approximately 21% in January through April compared to the same period of the prior year. Indonesia has historically been India's dominant thermal coal supplier, making this decline commercially significant for Indonesian miners operating in the sub-bituminous and bituminous segments.

- South Africa: Indian imports from South Africa fell by approximately 68% over the same period, a substantially larger proportional decline that reflects both the fuel switch dynamics and competitive pressure from other seaborne sources.

- Russia: Remains a supplier to the ICB fleet, though the magnitude of volume changes in Russian coal flows to India has not been separately reported with the same granularity.

"The scale of South Africa's 68% import decline into India warrants careful interpretation. It likely reflects a combination of the ICB fuel switch, price competitiveness dynamics, and logistical factors rather than exclusively fuel substitution effects. Analysts should be cautious about attributing the full decline to a single cause."

The Renewable Energy Feedback Mechanism

A less-discussed factor enabling faster ICB fuel substitution is the indirect effect of India's renewable energy expansion on inland coal allocation. As solar and wind generation capacity expands, inland coal-fired plants are being partially displaced during peak renewable output hours. This frees domestic coal allocations that would otherwise be fully committed to inland generation facilities, creating a surplus that can be redirected toward coastal ICB plants without reducing inland plant output.

India's coal-fired generation still rose 10% in May year-on-year, the strongest monthly growth since May 2024, reflecting peak summer demand conditions running in parallel with the fuel substitution programme. This confirms that the domestic coal redeployment is not occurring in a slack demand environment but rather alongside genuine growth in power consumption.

The Three Structural Barriers That Cannot Be Solved Overnight

Barrier One: Boiler Modification Timelines

The most technically complex constraint is the requirement for staged boiler modification before ICB plants can safely process high-ash domestic coal at scale. According to research on power generation efficiency, operators cannot simply change fuel inputs without first upgrading:

- Pulverising mill capacity to handle the higher volume of material required to achieve equivalent heat input.

- Ash handling and disposal systems to manage the substantially greater volumes of fly ash and bottom ash produced.

- Combustion management systems to optimise air-fuel ratios for lower-GCV fuel.

- Emissions control equipment to manage the altered particulate loading.

The blended fuel approach currently being used, where imported and domestic coal are combined to create a composite fuel specification within boiler tolerance limits, represents an interim operational strategy. Some facilities have already achieved domestic coal ratios of up to 70% of total fuel input through this blending methodology, demonstrating that meaningful substitution is achievable before full boiler conversion is complete.

Barrier Two: Rail Freight Economics and Coastal Geography

Even with boiler modifications complete, the economics of moving domestic coal from eastern India coalfields to coastal ICB plants in states like Gujarat present a structural challenge that engineering cannot resolve alone. Rail freight costs over distances of 1,500 to 2,000 kilometres can erode a significant portion of the price advantage of domestic coal relative to seaborne imported fuel delivered directly to port-adjacent plant coal yards.

This is the core reason the Coal Ministry's doorstep delivery initiative carries operational significance. By centralising the logistics coordination and supply commitment at the ministry level, the initiative attempts to reduce the cost and reliability risk premium that individual plant operators would otherwise factor into their domestic coal procurement decisions. However, the broader resource export pressures felt by competing supplier nations underscore just how consequential India's logistical choices have become for international markets.

Barrier Three: Power Purchase Agreement Misalignment

Many ICB plants operate under long-term power purchase agreements (PPAs) that were structured during a period of lower and more stable international coal prices. These agreements often contain fuel cost pass-through mechanisms calibrated for imported coal price dynamics, and may not adequately accommodate the variable cost structure of a blended domestic-imported fuel approach.

Plants operating at low capacity utilisation rates due to PPA pricing constraints face a paradox: switching to cheaper domestic coal could improve their operating economics, but only if utilisation rates increase to spread fixed costs. Resolving this requires renegotiation of PPA terms, which involves distribution companies and state electricity regulators, adding a regulatory layer to what is already a technically and logistically complex transition.

Comparing ICB and DCB Plants: An Operational Framework

| Dimension | Imported Coal-Based (ICB) Plants | Domestic Coal-Based (DCB) Plants |

|---|---|---|

| Primary fuel design | High-GCV imported coal | High-ash domestic coal |

| Typical GCV of design fuel | 5,000-6,500 kcal/kg | 3,500-4,500 kcal/kg |

| Boiler modification for fuel switch? | Yes, significant engineering work | Not applicable |

| Typical location | Coastal states (Gujarat, Maharashtra) | Central/eastern states near coalfields |

| Capacity utilisation | Often low due to PPA cost structures | High, backbone of national baseload |

| Government priority action | Boiler modification + doorstep domestic supply | Increase generation output |

| Logistics vulnerability | High, dependent on seaborne supply chains | Lower, direct rail access to mines |

| FY 2022-23 coal consumption | ~20 mt imported | ~35 mt domestic |

Three Scenarios for How the ICB Fuel Mix Evolves

The trajectory of India domestic coal use in import-based power plants over the next three to five years is not predetermined. Three plausible scenarios reflect different assumptions about the pace of infrastructure investment, boiler modification programmes, and renewable energy integration:

Scenario 1: Accelerated Domestic Transition

Full boiler modification across the ICB fleet is completed within a three-to-five-year window. Domestic coal achieves a 70% or greater share across most ICB facilities. Seaborne thermal coal imports for power generation fall below 40 million mt annually. This scenario requires sustained capital investment in boiler upgrades, material improvement in rail freight economics to coastal locations, and resolution of PPA structural misalignments.

Scenario 2: Partial Transition with a Structural Import Floor

Coastal logistics economics prevent full domestic coal substitution in the most geographically challenged locations. ICB plants stabilise at 50% to 60% domestic coal blending ratios. A residual import base of 25 to 35 million mt persists to supply high-GCV coal for blending requirements. This is arguably the most likely near-term outcome given the infrastructure investment timelines involved.

Scenario 3: Renewable Bypass

Accelerating solar and wind capacity additions reduce ICB plant utilisation rates to the point where total fuel consumption declines regardless of fuel mix. Many ICB plants shift toward peaking or backup generation roles. Import volumes decline not through substitution but through reduced aggregate generation demand from the ICB fleet. This scenario is plausible over a longer time horizon but is unlikely to be the dominant dynamic within five years given current demand growth trajectories. Furthermore, the broader commodity demand challenges facing Asia's energy markets suggest that multiple forces will shape outcomes simultaneously.

The next major ASX story will hit our subscribers first

What the Four-Year Import Low Signals for Global Seaborne Coal Markets

India's thermal coal imports reaching 65 million mt in January through May, a four-year low, is the aggregate outcome of three converging forces: higher domestic coal output from Coal India and captive mining operations, growing renewable energy generation reducing pressure on inland coal plants, and the active ICB fuel substitution programme. The interaction of these three forces is more powerful than any single factor alone.

For global seaborne thermal coal markets, India's strategic importance as the world's second-largest thermal coal importer means that even partial sustained reductions in Indian import demand exert measurable downward pressure on benchmark pricing. The key analytical question is whether the January-May 2026 import low represents a cyclical trough that will partially reverse as demand and price dynamics shift, or whether it marks the beginning of a structural step-down in India's seaborne coal dependency.

The evidence from the ICB fuel switch programme — specifically the forward booking of 16 million mt of domestic coal and the active modification trials across 4.3 GW of capacity — suggests that at least a portion of the import reduction has structural rather than cyclical foundations. However, seasonal demand peaks, monsoon-related domestic supply disruptions, and the pace of renewable integration will all influence whether the downward import trend is sustained or interrupted in the near term.

Disclaimer: This article contains forward-looking analysis, scenario projections, and market assessments that involve assumptions and uncertainties. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research and consult qualified advisers before making investment decisions based on coal market or energy sector dynamics.

Frequently Asked Questions: India Domestic Coal Use in Import-Based Power Plants

What is an imported coal-based power plant in India?

An imported coal-based (ICB) power plant is a generation facility purpose-built to operate on high-calorific-value coal sourced from international markets. These plants are typically located in coastal states to minimise transport costs from seaborne delivery points. India has approximately 18.7 GW of this type of capacity installed.

Why can't ICB plants simply switch to domestic coal immediately?

ICB plant boilers are engineered for low-ash, high-energy imported coal. India's domestic coal carries significantly higher ash content and lower calorific value, creating combustion inefficiencies and potential equipment stress in unmodified boilers. Operators must undertake staged modification programmes before higher volumes of domestic coal can be safely processed.

How much domestic coal are ICB plants currently using?

As of mid-2026, ICB plants are using domestic coal to operate the equivalent of 5.7 GW of their 18.7 GW total capacity. A further 4.3 GW of capacity is undergoing active fuel-switch trials. Some individual facilities have already achieved domestic coal ratios of up to 70% of total fuel input through blending strategies.

What is the Coal Ministry's doorstep delivery initiative?

The Coal Ministry has offered to coordinate direct domestic coal supply to ICB plant gates, removing logistics planning and coordination burdens from individual plant operators. This is designed to address both coal quality assurance and quantity reliability concerns that have historically deterred ICB operators from committing to domestic fuel at scale.

How has India's thermal coal import volume changed recently?

India's thermal coal imports reached a four-year low of approximately 65 million mt in the January through May period of 2026, driven by higher domestic coal output, increased renewable energy generation, and the active transition of ICB plants toward domestic fuel sourcing.

Which countries are most affected by India's reduced coal imports?

Indonesia and South Africa are the most directly affected exporters, with Indian imports from these sources declining approximately 21% and 68% respectively in January through April compared to the prior year. Russia is also a supplier to India's ICB fleet, though specific volume change data for Russian-origin imports was not separately reported in available sources. Consequently, the commodity demand challenges facing major exporting nations are mounting from multiple directions simultaneously.

Want to Stay Ahead of the Commodity Shifts Reshaping Global Energy Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity data into actionable investment insights — explore historic discoveries and the exceptional returns they have generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major market move.