June 4, 2026

India's Energy Security Landscape in an Era of Supply Chain Volatility

Global energy markets operate within an intricate web of geopolitical dependencies, where single-nation supply concentration creates systemic vulnerabilities for major importers. The recent surge in liquefied natural gas demand across Asian economies has intensified these dependencies, particularly as nations pursue ambitious energy transition challenges while maintaining industrial competitiveness. India's experience navigating supply disruptions illuminates the broader challenges facing energy-importing nations in an increasingly fragmented geopolitical environment.

The intersection of diplomatic relations, infrastructure resilience, and market dynamics reveals how energy security transcends simple supply-demand equations. When examining the mechanisms through which nations adapt to supply shocks, the role of ministerial diplomacy, alternative sourcing strategies, and domestic allocation priorities becomes critical to understanding modern energy statecraft.

When big ASX news breaks, our subscribers know first

Strategic Dependencies That Define India's Natural Gas Vulnerability Profile

Quantifying India's LNG Import Dependencies

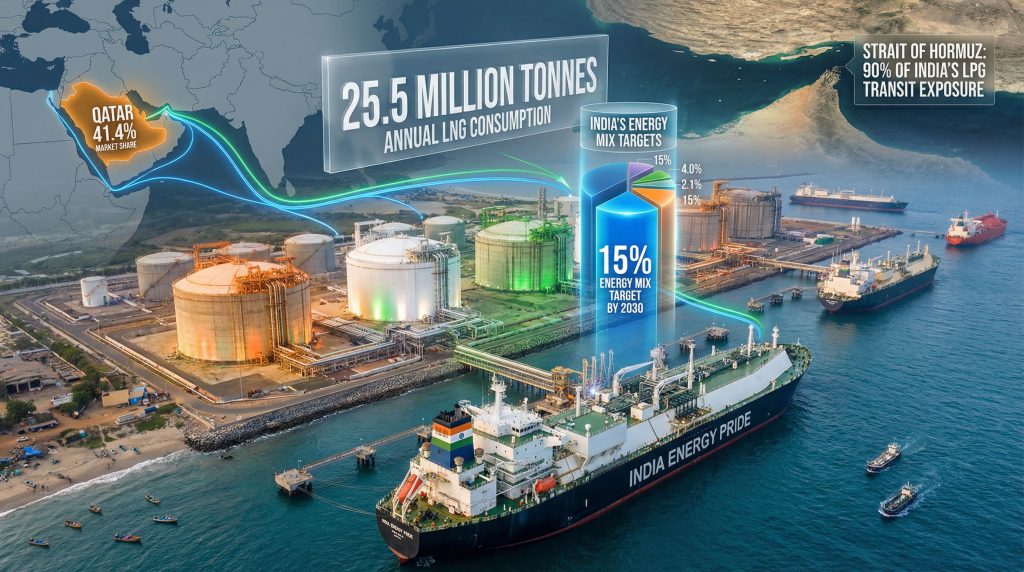

India's natural gas consumption patterns reveal a concerning level of supply concentration that mirrors broader global trends toward single-source dependencies. The nation's annual LNG consumption of 25.5 million tonnes places it among the world's largest importers, with Qatar commanding a dominant 41.4% market share of India's total LNG requirements.

This level of supplier concentration exceeds industry risk management benchmarks, where energy security experts typically recommend maintaining single-source dependencies below 25% to ensure supply chain resilience. The magnitude of this dependency becomes particularly stark when analyzed against India's broader energy mix transformation goals.

India's LNG Supply Concentration Analysis:

| Supplier | Market Share | Estimated Annual Volume (MTPA) | Contract Type |

|---|---|---|---|

| Qatar | 41.4% | ~10.6 | Long-term contracts |

| United States | Data unavailable* | Variable | Mixed spot/contract |

| Australia | Data unavailable* | Variable | Long-term contracts |

| Russia | Data unavailable* | Variable | Emerging partnerships |

| Others | Balance | Balance | Mixed portfolio |

*Specific market share data for non-Qatar suppliers requires verification through official Ministry of Petroleum & Natural Gas reports.

The concentration risk extends beyond simple volume calculations. Qatar's 14 LNG trains represent critical infrastructure whose operational capacity directly impacts India's energy security calculus. When examining the technical specifications of LNG infrastructure, each train typically processes 5-8 million tonnes per annum, meaning that damage to even two facilities can eliminate 10-16% of a supplier's total export capacity.

Critical Infrastructure Risk Assessment Through Geographic Chokepoints

The vulnerability of India's LNG supply chains extends significantly beyond supplier concentration to encompass critical maritime transit routes. The Strait of Hormuz represents a singular chokepoint through which approximately 20% of global petroleum liquids transit, creating cascading risk exposure for energy-importing nations.

Infrastructure Vulnerability Matrix:

• Upstream Production Risks: Natural gas field disruption, production facility damage

• Liquefaction Facility Risks: Compression train shutdowns, utilities infrastructure damage

• Storage & Export Risks: LNG tank damage, loading terminal disruption

• Transportation Risks: Maritime chokepoint exposure, piracy considerations

• Regasification Infrastructure: Terminal capacity constraints, pipeline connectivity limitations

The technical complexity of LNG infrastructure creates extended vulnerability windows during disruption scenarios. Unlike crude oil facilities, which can often resume operations within months, LNG compression trains require specialised engineering components with lengthy procurement and installation cycles. The sophisticated nature of these facilities means that repair timelines can extend 3-5 years for major infrastructure damage.

Economic Impact Modelling for Supply Disruption Scenarios:

• 30-day disruption: Estimated industrial capacity reduction of 15-20%

• 90-day disruption: Power generation sector impact with potential rolling blackouts

• 1-year disruption: Fundamental restructuring of India's natural gas allocation priorities

• Multi-year disruption: Acceleration of renewable energy deployment and coal utilisation

Geopolitical Conflict Mechanisms Reshaping Global LNG Trade Architecture

West Asia Conflict Impact on Global Market Dynamics

Regional conflicts create immediate and measurable impacts on global LNG markets through several distinct mechanisms. The ongoing tensions in West Asia have demonstrated how geopolitical events can rapidly transform supply chain assumptions and force major importers to activate alternative sourcing strategies.

Recent infrastructure damage in Qatar has reportedly affected approximately 12.8 million tonnes per annum of LNG production capacity, representing roughly 17% of the nation's total export capability. This capacity reduction occurred through damage to two of Qatar's 14 LNG trains plus one gas-to-liquids facility, highlighting the concentrated nature of global LNG infrastructure.

Global LNG Market Disruption Impact Analysis:

The scale of disruption becomes clearer when examined against global production capacity. Furthermore, with worldwide LNG production at approximately 413 MTPA in 2025, the offline capacity represents about 3.1% of global supply availability. While this percentage may appear modest, the regional concentration of demand in Asia creates amplified price volatility and supply competition effects.

Force Majeure Declaration Strategic Implications:

QatarEnergy's declaration of force majeure on long-term LNG contracts for up to five years represents a significant contractual mechanism that shifts supply risk from the supplier to purchasing nations. This action demonstrates several critical market dynamics:

• Contractual Risk Reallocation: Force majeure invocation transfers supply uncertainty to buyers

• Duration Mismatch Analysis: Five-year contract suspension versus 3-5 year repair timelines

• Supply Chain Flexibility Requirements: Buyers must activate alternative sourcing mechanisms

• Price Discovery Impact: Increased spot market activity during contract suspensions

Alternative Supply Chain Development During Crisis Periods

The shift toward alternative LNG suppliers during supply disruptions reveals both the flexibility and constraints within global gas markets. Indian companies have reportedly redirected procurement toward United States, Australian, and Russian LNG suppliers, primarily serving industrial consumption requirements.

This sourcing pivot illustrates several critical aspects of global LNG market structure:

Regional Supply Redistribution Dynamics:

• Atlantic Basin Suppliers: US LNG export capacity offers flexibility but at premium pricing

• Pacific Basin Suppliers: Australian suppliers provide reliable supply but limited swing capacity

• Russian LNG Options: Geopolitically complex but potentially cost-effective alternative

• Spot Market Liquidity: Increased reliance on short-term contracts during long-term disruptions

The technical characteristics of different LNG suppliers create varying risk profiles for importing nations. For instance, US natural gas forecast indicates that US LNG facilities, designed with modular capacity, can adjust output levels more readily than traditional integrated facilities. Australian suppliers offer geographic proximity benefits for Asian importers but operate with high capacity utilisation rates that limit surplus availability.

Ministerial Diplomacy as Energy Security Crisis Management

High-Level Diplomatic Engagement During Supply Disruptions

The Hardeep Singh Puri visit to Qatar amid LNG crisis exemplifies how energy security challenges require immediate diplomatic intervention at the highest government levels. Such ministerial engagements serve multiple strategic functions beyond simple commercial negotiations.

Energy diplomacy during crisis periods operates through several distinct channels:

• Bilateral Security Dialogue Frameworks: Direct government-to-government supply guarantee discussions

• Infrastructure Protection Agreements: Diplomatic protocols for energy facility security

• Contract Renegotiation Facilitation: Government backing for commercial entity negotiations

• Regional Coordination Mechanisms: Multi-party diplomatic frameworks for supply chain stability

The timing of ministerial visits during active conflicts demonstrates the critical importance of maintaining energy partnerships despite broader geopolitical tensions. Consequently, these engagements often occur simultaneously with ceasefire negotiations and broader diplomatic initiatives, as India's petroleum minister engages in crucial energy security discussions.

Contract Restructuring Through Diplomatic Channels

High-level diplomatic engagement facilitates contract restructuring mechanisms that extend beyond standard commercial frameworks. The potential for extending 10-year LNG contracts to 20-year agreements represents strategic partnership deepening that transcends immediate crisis management.

Diplomatic Contract Enhancement Mechanisms:

• Force Majeure Clause Modifications: Diplomatic agreements can influence contractual interpretations

• Investment Commitment Negotiations: Government backing for infrastructure development financing

• Multi-Sector Trade Integration: Energy partnerships expanded to include technology transfer

• Regional Stability Frameworks: Energy security linked to broader diplomatic cooperation

Prime Minister Modi's engagement with Qatar's Emir Sheikh Tamim bin Hamad Al Thani demonstrates how energy security concerns receive attention at the highest diplomatic levels. These interactions often result in strategic frameworks that extend beyond immediate supply concerns to encompass long-term partnership development.

Priority Sector Allocation Systems During Energy Supply Constraints

Government Intervention in Natural Gas Distribution Networks

Energy supply disruptions activate government intervention mechanisms that prioritise critical sectors over market-driven allocation systems. India's approach to natural gas distribution during supply constraints reveals sophisticated priority frameworks designed to maintain essential economic functions.

Government Priority Sector Classification:

• Power Generation Sector: Maintaining grid stability and essential electricity supply

• Fertiliser Production: Food security implications through agricultural input availability

• Industrial Manufacturing: Critical export industries and employment-intensive sectors

• Transportation Sector: CNG supply for public transportation systems

• Residential Cooking Gas: LPG cylinder distribution for household energy security

The technical implementation of priority sector allocation requires sophisticated distribution network management. Natural gas pipeline systems must redirect flows from lower-priority industrial users to critical sectors, often requiring real-time coordination between multiple distribution companies.

LPG Supply Chain Resilience During Import Disruptions

Cooking gas supply chains represent a critical component of household energy security that requires specialised crisis management protocols. Daily LPG cylinder distribution patterns must maintain consistent delivery schedules despite upstream supply volatility.

The government's approach to LPG supply chain management during disruptions involves several key mechanisms:

• Strategic Reserve Utilisation: Drawing down petroleum reserves to maintain supply continuity

• Alternative Sourcing Agreements: Emergency procurement from non-traditional suppliers

• Distribution Network Optimisation: Prioritising high-density population centres

• Subsidy Reallocation: Government financial support for maintaining affordable access

In addition, as detailed in financial media reports, the government has prioritised LPG supply security through immediate diplomatic intervention.

Long-Term Implications for India's Energy Transition Strategy

Natural Gas Share Target Adjustments in Supply Disruption Context

India's goal of increasing natural gas share to 15% of the energy mix by 2030 faces significant challenges when viewed through supply security considerations. The target requires substantial infrastructure investment combined with reliable long-term supply agreements that recent disruptions have called into question.

Energy Mix Transition Risk Assessment:

Current natural gas share in India's energy mix remains below 10%, requiring sustained growth to achieve the 15% target within the decade. This expansion must occur while simultaneously reducing single-supplier dependencies and building supply chain resilience.

• Infrastructure Investment Requirements: LNG terminal expansion, pipeline network development

• Supply Diversification Mandates: Reducing Qatar dependency below 30% market share

• Renewable Energy Acceleration: Natural gas as bridge fuel versus renewable priority

• Energy Security Balancing: Climate goals versus supply chain reliability

Strategic Partnership Evolution Beyond Crisis Management

Long-term energy partnerships must evolve beyond traditional buyer-seller relationships to encompass broader strategic cooperation frameworks. The Qatar-India energy relationship demonstrates how crisis management can catalyse deeper partnership structures.

Partnership Evolution Framework:

• Technology Transfer Agreements: LNG infrastructure development capabilities

• Joint Investment Vehicles: Shared ownership of upstream and midstream facilities

• Regional Energy Cooperation: South Asian energy integration initiatives

• Innovation Partnerships: Clean energy technology development collaboration

The next major ASX story will hit our subscribers first

Regional Conflicts and Global Energy Security Architecture

Chokepoint Vulnerability Assessment Across Major Economies

The Strait of Hormuz represents one of several critical maritime chokepoints that create systemic vulnerabilities for global energy trade. Understanding these geographic constraints becomes essential for energy security insights across major importing economies.

Global Energy Chokepoint Analysis:

• Strait of Hormuz: 20% of global petroleum liquids, 18% of global LNG transit

• Strait of Malacca: Critical route for Asian LNG imports from Atlantic Basin suppliers

• Suez Canal: Alternative routing for Middle Eastern energy exports to European markets

• Danish Straits: Russian pipeline gas alternative routing considerations

Chokepoint closure scenarios create immediate price impacts and supply redistribution requirements across global energy markets. Historical analysis of temporary chokepoint disruptions suggests price premiums of 10-40% depending on closure duration and alternative routing availability.

Market Adaptation Strategies During Prolonged Disruptions

Extended supply disruptions force fundamental adaptations in energy market structure and pricing mechanisms. The development of alternative supply chains, storage capacity expansion, and risk management instruments becomes essential for maintaining market functionality.

Market Structure Adaptation Mechanisms:

• Spot Market Liquidity Enhancement: Increased short-term trading activity during contract disruptions

• Price Discovery Evolution: New benchmarking mechanisms for disrupted supply environments

• Risk Premium Integration: Higher baseline prices reflecting geopolitical uncertainty

• Insurance Market Development: Enhanced coverage for energy supply chain disruptions

However, these adaptation strategies must account for broader oil price movements that influence overall energy market dynamics during crisis periods.

Investment Opportunities Emerging from Supply Diversification Requirements

Infrastructure Development Priorities for Supply Chain Resilience

Energy supply disruptions create investment opportunities in infrastructure projects designed to enhance supply chain resilience and reduce single-source dependencies. The scale of required investment spans multiple sectors and geographic regions.

Infrastructure Investment Priority Matrix:

• LNG Terminal Expansion: Additional regasification capacity to accommodate diverse suppliers

• Pipeline Connectivity Enhancement: Network redundancy for alternative supply routing

• Storage Capacity Optimisation: Strategic reserves for supply shock absorption

• Technology Integration: Digital monitoring systems for supply chain transparency

LNG terminal expansion projects typically require 3-5 years for planning and construction, representing significant capital deployment opportunities. Each new terminal adds 2-5 MTPA of regasification capacity, contributing to national supply chain flexibility.

Market Entry Opportunities for Alternative Suppliers

Supply disruptions create market entry opportunities for non-traditional suppliers seeking to establish long-term partnerships with major importing nations. The competitive dynamics shift during crisis periods, allowing new suppliers to compete against established market participants.

Alternative Supplier Market Entry Strategies:

• US LNG Export Expansion: Modular capacity additions targeting Asian markets

• Australian Contract Availability: Long-term agreements during Middle East disruptions

• African LNG Development: Accelerated project development for Indian market access

• Technology Partnership Integration: Supplier relationships beyond simple commodity sales

The emergence of new LNG suppliers creates portfolio diversification opportunities for importing nations while generating revenue streams for exporting countries. These relationships often develop into broader strategic partnerships encompassing technology transfer and joint investment initiatives.

Strategic Lessons for Global Energy Security Management

Crisis Response Effectiveness and Diplomatic Engagement

The effectiveness of diplomatic engagement during energy supply crises provides valuable insights for other nations facing similar challenges. The speed and level of government intervention significantly influences supply chain restoration and alternative sourcing success.

Diplomatic Crisis Management Best Practices:

• Immediate High-Level Engagement: Ministerial visits within weeks of supply disruption onset

• Multi-Channel Communication: Government, commercial, and technical dialogue streams

• Regional Coordination Integration: Broader diplomatic initiatives linked to energy security

• Long-Term Partnership Reinforcement: Crisis management as foundation for deeper cooperation

Future-Proofing Energy Import Strategies Against Geopolitical Volatility

Modern energy security requires anticipating and preparing for supply chain disruptions rather than simply responding to them. The development of resilient energy import strategies must balance cost optimisation with supply chain security considerations.

Strategic Energy Security Framework:

• Supplier Portfolio Optimisation: Maximum 25% single-source dependency targets

• Infrastructure Redundancy Investment: Multiple supply chain pathway development

• Diplomatic Relationship Maintenance: Sustained engagement across geopolitical divisions

• Technology Adoption Acceleration: Supply chain monitoring and risk management systems

The integration of renewable energy development with natural gas import strategies provides additional resilience through fuel diversification. Nations that successfully balance energy transition goals with supply security requirements demonstrate superior long-term energy planning capabilities.

Furthermore, understanding the broader implications of the US-China trade impact on energy markets becomes essential for comprehensive risk assessment and strategic planning.

The Hardeep Singh Puri visit to Qatar amid LNG crisis represents a critical moment in India's energy diplomacy, demonstrating how ministerial-level engagement becomes essential during supply chain disruptions. This diplomatic intervention exemplifies the strategic importance of maintaining energy partnerships despite regional conflicts and geopolitical uncertainties.

The evolution of global energy security architecture requires continuous adaptation to changing geopolitical conditions, technological developments, and market dynamics. Nations that develop comprehensive crisis response capabilities while maintaining strategic flexibility demonstrate superior resilience in an interconnected but increasingly fragmented global energy system.

Investment Disclaimer: This analysis discusses hypothetical geopolitical scenarios and their potential energy market impacts. Readers should conduct independent research and consult qualified financial advisors before making investment decisions based on geopolitical risk assessments. Energy market predictions involve significant uncertainty and past performance does not guarantee future results.

Ready to Capitalise on Energy Market Disruptions and Commodity Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral and energy discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market during periods of supply chain volatility. Begin your 14-day free trial today and secure your market-leading advantage whilst major energy transitions create new investment opportunities across critical mineral sectors.