June 6, 2026

The Structural Economics Behind a Tenfold Battery Demand Surge

Every major industrial transformation has a moment where incremental progress gives way to exponential change. For India's energy storage sector, that inflection point is now visible on the horizon. The forces converging on India's electric vehicle ecosystem are not the product of any single policy lever or technology breakthrough but rather the compounding effect of cost compression, consumer behaviour shifts, infrastructure maturation, and supply chain reconfiguration happening simultaneously.

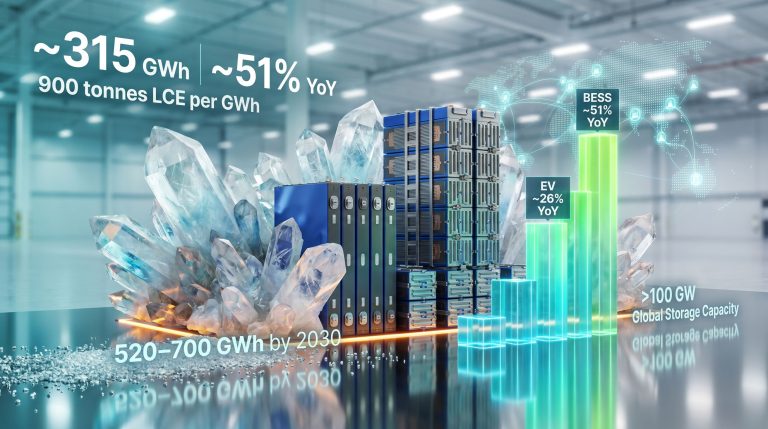

Understanding the scale of what is unfolding requires stepping back from the immediate news cycle and examining the structural mechanics driving India EV battery demand growth from a baseline of 20 gigawatt-hours (GWh) in 2025 toward a projected 200 GWh by 2032. This is not a forecast built on optimistic assumptions alone. It reflects a layered demand architecture spanning two-wheelers, three-wheelers, passenger vehicles, and commercial fleets, each segment adding successive layers of energy storage requirements as electrification deepens.

According to a report titled India EV and EV Component Market Outlook 2025-2034, released by the Indian Energy Storage Alliance (IESA) in association with Customized Energy Solutions (CES) at the 12th India Energy Storage Week, this trajectory represents one of the most consequential industrial scaling challenges in Asia's energy transition landscape. Furthermore, the global lithium market and Indian investment dynamics are playing a central role in shaping how this transformation unfolds. (ET EnergyWorld, May 15, 2026)

When big ASX news breaks, our subscribers know first

From 2.5 Million Units to a 200 GWh Ecosystem: Understanding the Demand Stack

India's EV sales crossed 2.5 million units in 2025, a figure that signals the market has moved well beyond its early-adopter phase. The breakdown is instructive: approximately 1.5 million electric two-wheelers and 0.7 million electric three-wheelers accounted for the dominant volume share. (IESA/CES, ET EnergyWorld, May 2026)

What makes this composition analytically significant is the relationship between unit volumes and aggregate GWh demand. A typical electric two-wheeler carries a battery pack of roughly 2 to 3 kWh, while a three-wheeler averages closer to 5 to 10 kWh. At 1.5 million two-wheeler units, the cumulative battery demand from this segment alone reaches multi-GWh scale before accounting for replacement cycles.

The demand architecture can be broken down into distinct layers:

- Layer 1 (Current): Electric two-wheelers and three-wheelers generating high unit volumes at small per-unit pack sizes, creating broad aggregate demand

- Layer 2 (Near-term): Passenger electric vehicles with significantly larger pack sizes (typically 30 to 60+ kWh per unit), amplifying GWh demand disproportionately to unit volume growth

- Layer 3 (Emerging): Light commercial vehicles and last-mile delivery fleets, where electrification is driven by total cost of ownership economics rather than consumer preference

- Layer 4 (Long-term): Stationary energy storage and grid applications absorbing surplus manufacturing capacity as the domestic cell industry scales

The IESA report notes that while two-wheelers continue to lead on volume, the next significant demand wave is expected from passenger electric cars and light commercial fleets. This transition will materially change the average kWh-per-unit calculation and accelerate GWh demand beyond what unit sales figures alone would suggest. According to industry projections on EV battery demand, India's EV battery demand is set to grow tenfold to 200 GWh by 2032.

The Chemistry Transition Reshaping India's Battery Procurement Landscape

Battery chemistry selection in India is not a static decision. It reflects a constantly shifting calculus between energy density requirements, thermal safety considerations, cost per kilowatt-hour, and supply chain security. The IESA/CES report identifies a clear hierarchy currently operating in the market.

NMC Dominance in Two-Wheelers and Its Structural Limitations

Nickel Manganese Cobalt (NMC) chemistry currently holds approximately 70% market share in the electric two-wheeler segment, a position built on its superior energy density relative to alternatives. For two-wheelers where weight and range efficiency are paramount within a compact form factor, NMC's volumetric energy density advantages have made it the default choice for leading OEMs. (IESA/CES, ET EnergyWorld, May 2026)

However, NMC carries structural vulnerabilities that become increasingly relevant as India's market matures. Cobalt dependency creates supply chain exposure given that the Democratic Republic of Congo accounts for over 70% of global cobalt production, according to the United States Geological Survey (USGS, 2024). Price volatility in cobalt markets has historically introduced margin unpredictability for battery manufacturers operating on thin cost structures in price-sensitive markets like India.

LFP's Rising Strategic Position

Lithium Iron Phosphate (LFP) chemistry is gaining ground rapidly across three-wheeler, commercial vehicle, and stationary storage applications. The strategic logic is compelling:

- Thermal stability: LFP cells exhibit significantly lower thermal runaway risk, a critical consideration for fleet operators managing maintenance costs across large vehicle populations

- Cycle life: LFP chemistry typically delivers 2,000 to 4,000+ charge cycles versus 1,000 to 2,000 for many NMC formulations, reducing total cost of ownership over fleet lifetimes

- Cobalt elimination: LFP contains no cobalt, substantially reducing both cost exposure and geopolitical supply chain risk

- Cost per kWh at scale: Chinese manufacturers have driven LFP cell costs to levels that are increasingly competitive with NMC, particularly for applications where energy density is less constrained by form factor

The accelerating adoption of LFP in China's domestic market and the scale economics that Chinese cell manufacturers have achieved are directly influencing pricing dynamics available to Indian importers and OEMs. In addition, Chinese battery recycling advances are further reshaping the cost and materials landscape that Indian manufacturers must navigate. This presents a complex tension: imported LFP cells offer near-term cost efficiency, but they delay the development of domestic manufacturing capability.

The Chemistry Landscape at a Glance

| Battery Chemistry | Primary Application | Market Position | Key Advantage |

|---|---|---|---|

| NMC | Electric two-wheelers | ~70% of 2W segment | Superior energy density |

| LFP | Three-wheelers, commercial, stationary | Rapidly expanding share | Thermal safety, cycle life, cost |

| LMFP | Mid-range passenger EVs | Pre-commercial, emerging | Higher density than standard LFP |

| Sodium-ion | Price-sensitive segments | Development stage | Reduced critical mineral dependency |

| Solid-state | Premium passenger, commercial | Long-term horizon | Potential step-change in energy density |

Motor Technology: An Underappreciated Demand Signal

Alongside battery chemistry evolution, motor technology selection provides a revealing signal about market segmentation. The IESA/CES report documents that BLDC (Brushless DC) motors account for 71% of the two-wheeler market, reflecting the cost-optimised architecture favoured in high-volume, price-sensitive segments. By contrast, PMSM (Permanent Magnet Synchronous Motors) have captured over 90% of the passenger EV segment, where performance efficiency and torque characteristics justify higher component costs. (IESA/CES, ET EnergyWorld, May 2026)

This chemistry and motor technology bifurcation between vehicle segments is not merely a technical observation. Consequently, it has direct implications for supply chain architecture, component localisation strategy, and the types of manufacturing investment that will generate returns across different market phases.

Next-Generation Chemistries: What the 2025–2032 Window Realistically Holds

LMFP: The Near-Term Upgrade Path

Lithium Manganese Iron Phosphate (LMFP) represents an evolutionary step beyond standard LFP, offering improved energy density while retaining the thermal stability and cobalt-free profile that makes LFP commercially attractive. For India's mid-range passenger EV segment, where range anxiety remains a consumer concern but cost sensitivity limits NMC adoption, LMFP presents a credible bridging technology. Several Chinese manufacturers including CATL and BYD have progressed LMFP toward commercial production, which may accelerate availability and pricing for Indian OEMs within the forecast window.

Sodium-Ion: India's Strategic Wildcard

Sodium-ion battery technology carries particular strategic resonance for India that extends beyond pure technical performance. India possesses abundant sodium resources, and sodium-ion cells do not require lithium, cobalt, or nickel in their cathode chemistry, directly addressing the critical mineral import dependency that represents one of the most significant structural vulnerabilities in India's EV supply chain.

The ability to produce competitive battery cells without relying on imported lithium or cobalt is not just an economic advantage for India. It is an energy security imperative that aligns domestic industrial policy with long-term resource sovereignty objectives.

Current sodium-ion energy density lags lithium-ion alternatives, making it better suited for short-range, lower-speed applications in the near term. However, the technology trajectory suggests meaningful improvements through 2028–2030 that could expand its addressable vehicle segments. Domestic research institutions and international battery manufacturers are actively engaged in sodium-ion development programmes, though commercially viable mass production at cost-competitive price points remains a work in progress for the 2025–2032 forecast window.

Solid-State: The Long-Term Horizon

Solid-state battery technology remains a premium-tier development programme rather than a near-term commercial reality for India. While offering theoretical step-change improvements in energy density and safety, solid-state manufacturing at scale involves materials and processes that have not yet been commercially resolved by any manufacturer globally. Investors and OEM strategists should treat solid-state as a post-2030 consideration for Indian market applications, with 2032 timelines for meaningful commercial deployment representing an optimistic rather than base-case scenario.

Localisation: Where the Real Economic Value Is Being Competed For

The IESA framing of India's EV opportunity as extending well beyond vehicle assembly reflects a sophisticated understanding of where value is actually created in the battery supply chain. As Debmalya Sen, President of IESA, has stated, the industry's next phase of growth will be driven by localisation, advanced chemistry, and resilient supply chains — a view that positions domestic manufacturing capability as the central strategic prize rather than vehicle sales volume alone. (ET EnergyWorld, May 2026)

The supply chain value stack that India needs to develop domestically includes several distinct tiers:

- Cell manufacturing (capital-intensive, technology-dependent, highest strategic value)

- Pack assembly (near-term localisation opportunity with existing industrial capability)

- Battery Management Systems (electronics and software, higher margin, IP-intensive)

- Thermal management and structural components (underappreciated opportunity in conventional manufacturing)

- Battery recycling and second-life applications (long-term feedstock security strategy)

The gap between India's current domestic content levels and the localisation trajectory embedded in government policy frameworks remains substantial, particularly at the cell manufacturing level. India's lithium supply strategy is increasingly focused on securing upstream materials to support this localisation ambition. Production-linked incentive (PLI) schemes are designed to bridge this gap by making domestic cell manufacturing economically viable against imported alternatives, but the investment quantum required for gigafactory-scale cell production creates barriers that PLI incentives alone may not be sufficient to overcome.

India's Competitive Position in the Global Battery Manufacturing Race

How India Compares to Other Major EV Markets

India's demand profile is structurally distinct from the battery markets that have shaped global cell manufacturing economics. China and Europe's battery demand is dominated by passenger vehicles carrying large pack sizes, which drives the GWh economics that justify gigafactory investment. India's current demand profile, concentrated in two-wheelers and three-wheelers, produces high unit volumes at lower average kWh per vehicle.

This distinction creates both challenges and opportunities for international battery manufacturers evaluating India market entry:

| Market | Demand Profile | Avg. Pack Size (kWh) | Primary Chemistry | Manufacturing Stage |

|---|---|---|---|---|

| China | Passenger-led | 50–80+ | LFP dominant | Mature, globally exporting |

| Europe | Passenger and commercial | 60–100+ | NMC/LFP mix | Scaling, import-dependent |

| USA | Passenger and SUV | 70–100+ | NMC dominant | Expanding domestic capacity |

| India | Two/three-wheeler led | 2–10 (current) | NMC/LFP dual | Early-stage domestic |

| Southeast Asia | Mixed, early-stage | Varied | Mixed | Nascent |

The China-Plus-One Window and Its Time Constraints

Global supply chain diversification strategies driven by US-China trade tensions and European critical supply resilience concerns have created genuine openings for alternative manufacturing destinations. India is positioning itself as a credible China-plus-one option for battery manufacturing investment, with advantages including domestic market scale that justifies localisation, an engineering talent base with established electronics and automotive manufacturing credentials, and relative policy continuity compared to some Southeast Asian competitors.

However, this window has structural time constraints. Supply chain investment decisions in battery manufacturing involve long lead times for equipment procurement, facility construction, workforce development, and supplier qualification. Strategic commitments being made in the 2025–2028 period will substantially determine where global battery manufacturing capacity is anchored through the mid-2030s. India's ability to attract and retain investment commitments during this specific window will define whether it emerges as a genuine manufacturing hub or remains a large import-dependent consumption market.

Furthermore, the development of a domestic battery-grade lithium refinery is increasingly viewed as a prerequisite for India to compete credibly in global cell manufacturing, rather than simply assembling imported cells.

The next major ASX story will hit our subscribers first

Investment Implications Across the Value Chain

For investors evaluating exposure to India EV battery demand growth, the value chain presents materially different risk-return profiles across segments:

| Value Chain Segment | Investment Thesis | Risk Profile | Realistic Time Horizon |

|---|---|---|---|

| Cell Manufacturing | Highest strategic value, policy-supported | High capex, technology competition, long payback | 5–10 years |

| Pack Assembly | Near-term domestic opportunity, lower barriers | Moderate capex, margin compression risk | 2–5 years |

| BMS and Electronics | IP-driven, higher margins, software defensibility | Technology competition, import alternatives | 3–7 years |

| Battery Recycling | Long-term feedstock security, regulatory tailwinds | Volume timing, technology maturity | 7–15 years |

| Charging Infrastructure | Demand enabler with recurring revenue potential | Utilisation risk, geographic concentration | 3–8 years |

| Raw Material Processing | Upstream security, import substitution | Capital intensity, development timelines | 8–15 years |

Disclaimer: The investment analysis presented in this table is intended for informational and educational purposes only and does not constitute financial advice. All investment decisions involve risk, and past performance or projected market trajectories do not guarantee future returns. Readers should seek independent financial advice before making investment decisions.

Key Questions for Stakeholders Navigating India's Battery Market

What is the verified basis for the 200 GWh demand forecast?

The projection originates from the India EV and EV Component Market Outlook 2025-2034 report developed by the Indian Energy Storage Alliance (IESA) in conjunction with Customized Energy Solutions (CES), as reported by ET EnergyWorld in May 2026. It represents a tenfold increase from an estimated baseline of 20 GWh in 2025. Indeed, market analysis on EV battery growth further supports this trajectory as the domestic ecosystem matures.

Which vehicle segments will drive the next phase of demand acceleration?

Current volumes are driven by electric two-wheelers and three-wheelers, which collectively accounted for over 2.2 million of the 2.5 million EV units sold in 2025. The next demand amplification is expected from passenger EVs and light commercial vehicles, where larger pack sizes will significantly multiply GWh demand relative to unit volume growth.

What are the principal risk factors to the growth trajectory?

Key risks include critical mineral supply chain disruptions affecting lithium and cobalt availability; slower-than-projected charging infrastructure deployment constraining consumer confidence; technology transition timing risk if next-generation chemistries face commercialisation delays; macroeconomic pressure on consumer purchasing power in price-sensitive segments; and the possibility that cell manufacturing investment fails to materialise at sufficient scale within the necessary timeframe, leaving India dependent on imports even as demand scales.

Why does battery chemistry selection matter for supply chain strategy?

Chemistry choices determine raw material requirements, supplier relationships, manufacturing process requirements, and ultimately the geographic location of value creation. A market that standardises on NMC will have fundamentally different supply chain dependencies than one that transitions toward LFP or sodium-ion, with corresponding differences in geopolitical exposure, cost structures, and domestic manufacturing feasibility. Technologies such as direct lithium extraction are also emerging as potential enablers of more flexible and efficient upstream supply.

The Strategic Moment India Cannot Afford to Defer

The arithmetic of India EV battery demand growth is straightforward. A tenfold increase in GWh demand over seven years represents a complete industrial reconstitution of the energy storage sector, not an incremental expansion of existing capacity. What began as a policy-driven pilot programme has, as the IESA observes, evolved into a sprawling industrial ecosystem encompassing batteries, motors, power electronics, advanced chemistries, localised manufacturing, and robust supply chain investments. (ET EnergyWorld, May 2026)

The central strategic question is not whether 200 GWh of annual battery demand will materialise. The demand trajectory is supported by compounding structural drivers across multiple vehicle segments, cost dynamics, and infrastructure development. The question is whether India will produce, assemble, and capture the value embedded in that demand domestically, or whether the majority of that value will flow to overseas cell manufacturers through import dependency.

As the Customized Energy Solutions Managing Director Vinayak Walimbe has articulated, stakeholders from OEMs to investors require strategic direction to capitalise on these emerging opportunities. (ET EnergyWorld, May 2026) That direction points consistently toward the same conclusion: localisation is not a policy preference but an economic necessity, and the investment decisions made in the next three years will determine whether India claims its position as a global battery manufacturing hub or remains a large, strategically vulnerable consumption market.

Want to Track the Next Major Mineral Discovery Driving the Energy Transition?

India's tenfold battery demand surge is creating enormous upstream demand for lithium and other critical minerals — and Discovery Alert's proprietary Discovery IQ model instantly notifies subscribers of significant ASX mineral discoveries the moment they are announced, turning complex data into actionable opportunities. Explore Discovery Alert's discoveries page to see the historic returns major mineral discoveries have delivered, and begin your 14-day free trial to position yourself ahead of the market.