May 12, 2026

The Mineral Equation Sitting at the Heart of India's Clean Energy Ambitions

Every major energy transition in modern history has been built on a foundation of raw materials. Coal powered the industrial revolution. Oil shaped the twentieth century's geopolitical order. The clean energy era is no different, except the minerals required are far more geographically concentrated, technically demanding to process, and strategically contested than anything that came before. For India, this reality sits at the very centre of its India EV infrastructure and critical minerals challenge, and the country is only beginning to reckon with the full scale of what is required.

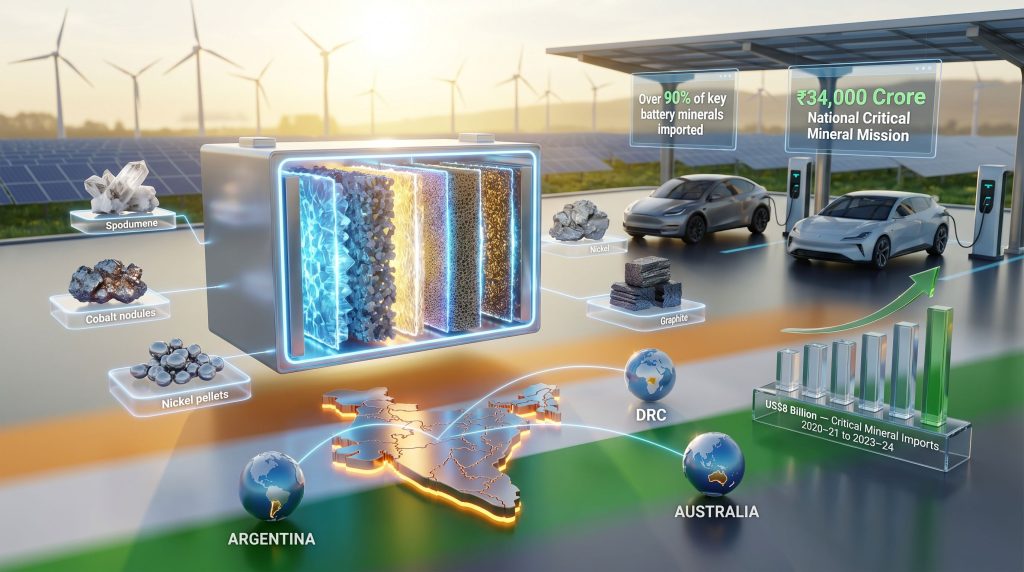

The arithmetic is sobering. India currently imports over 90% of its key battery minerals, including lithium, cobalt, and nickel. Critical mineral imports more than doubled over a three-year period, reaching approximately US$8 billion between 2020-21 and 2023-24. The primary sources of these imports include China, South Korea, Japan, and Hong Kong, concentrating supply risk in a handful of trade relationships that carry significant geopolitical complexity.

What makes this dependency particularly acute is the fact that the same minerals underpinning EV batteries are also essential for solar photovoltaic panels, wind turbines, and grid-scale storage systems, meaning demand pressure compounds across every pillar of the clean energy transition simultaneously. Furthermore, critical minerals and energy security are becoming increasingly inseparable concepts for policymakers navigating this challenge.

Energy security and mineral security are not separate conversations. They are the same conversation, viewed from different angles. Without secured access to lithium, cobalt, and rare earth elements, India's 2070 net-zero target cannot be achieved regardless of how ambitious domestic policy frameworks become.

When big ASX news breaks, our subscribers know first

What Minerals Does India Actually Need, and in What Quantities?

Understanding the scope of India's mineral challenge requires mapping specific materials to their applications within the EV ecosystem and then assessing where domestic availability falls short.

| Mineral | Primary EV Application | India's Domestic Availability | Key Import Sources |

|---|---|---|---|

| Lithium | Battery cathodes and electrolytes | Limited (deposits identified in Karnataka and Rajasthan) | China, Argentina, Australia |

| Cobalt | NMC battery cathodes | Negligible domestic reserves | DRC via China |

| Nickel | High-energy density batteries | Moderate | Indonesia, Philippines |

| Graphite | Battery anodes | Limited | China (dominant global supplier) |

| Rare Earth Elements | EV motors and electronics | Some deposits; largely underexplored | China |

| Copper | Wiring and charging infrastructure | Moderate | Chile, Peru, Australia |

| Aluminium | Lightweight EV structures and enclosures | Reasonably available domestically | Domestic plus imports |

The concentration of supply along China-linked routes is a structural vulnerability that has prompted India to accelerate its upstream diversification strategy with considerable urgency. What distinguishes this challenge from typical commodity procurement is that mineral refining and processing capacity, not just raw extraction rights, determines who actually controls the supply chain.

China's dominance is as much about processing infrastructure as it is about mining access, a distinction that India's industrial planners are increasingly factoring into their strategy. According to India's critical mineral import risks, import concentration remains one of the most pressing vulnerabilities requiring systematic policy attention.

The National Critical Mineral Mission: India's Upstream Policy Response

The National Critical Mineral Mission (NCMM), backed by ₹34,000 crore in funding, represents the most structurally significant policy response to India's upstream vulnerability. Rather than addressing a single point of failure, the mission targets the entire critical mineral value chain through four interconnected pillars:

-

Domestic exploration acceleration, expanding the mandate of the Geological Survey of India (GSI) to systematically map lithium, cobalt, and rare earth element deposits across previously under-surveyed regions.

-

Overseas mineral block acquisition, deploying public sector enterprises to secure extraction rights in resource-rich jurisdictions before competition from other consuming nations intensifies further.

-

Research and development investment, funding alternative battery chemistries and processing technologies that could reduce dependency on the most geopolitically sensitive minerals.

-

Workforce and capability development, building the technical expertise in mining, refining, and materials science that sustained domestic processing capacity requires.

The overseas acquisition dimension is already producing tangible results. Indian public sector undertakings have formed joint ventures and acquired five mineral blocks across Argentina lithium brines, positioning India within the South American Lithium Triangle, one of the world's most significant lithium-bearing geological zones. Bilateral mineral partnerships are also being developed with Australia targeting lithium and cobalt, and exploratory discussions are underway with Chile.

How Is India Coordinating Its Mineral Acquisition Push?

A strategically notable aspect of this push is the cross-sector convergence it involves. Coal India and oil sector public enterprises are being integrated into the mineral acquisition framework, creating an unusual alignment between industries that are typically on opposite ends of the energy transition narrative. The Ministry of Mines has also formalised a Critical Minerals List for India, establishing a prioritisation framework that guides both investment allocation and import substitution efforts.

India's overseas mineral diplomacy broadly mirrors approaches previously used by Japan through long-term bilateral agreements and public sector-led acquisitions. The critical difference is timing. The most accessible global assets have already been claimed, requiring India to pursue more sophisticated deal structures and leverage its scale as a future consumer to negotiate favourable terms.

In addition, India's lithium supply strategy with Australia represents one of the most actively developed bilateral resource partnerships currently in progress, with implications for both upstream security and downstream refining capacity.

From Scepticism to Scale: How India's EV Market Transformed

The evolution of India's domestic EV market contains a lesson about the relationship between technology, psychology, and infrastructure investment that is directly relevant to understanding where the sector goes next.

Early-generation Indian EVs offered 150 to 180 kilometres per charge, a range figure that created genuine hesitation among consumers accustomed to the refuelling convenience of petrol and diesel vehicles. That hesitation was not irrational. For a country with limited charging infrastructure and long distances between major population centres, range limitations represented a practical constraint on utility.

Current-generation vehicles have shifted the calculus substantially, with drive ranges now reaching 550 to 650 kilometres per charge. However, what is particularly revealing about India's EV adoption curve is how the psychological barrier has evolved rather than dissolved. Range anxiety has been progressively replaced by charging infrastructure anxiety, a distinct but equally potent deterrent to mainstream adoption.

This psychological transition matters for infrastructure investment strategy. It signals that consumer confidence is no longer primarily constrained by vehicle technology but by the density, reliability, and geographic coverage of the charging network itself.

India's EV Charging Infrastructure: Where It Stands and Where It Needs to Go

India's EV infrastructure buildout is anchored by the FAME-II programme and the National Electric Mobility Mission Plan (NEMMP), with Production-Linked Incentive (PLI) schemes for Advanced Chemistry Cell (ACC) battery manufacturing providing additional industrial momentum.

The practical infrastructure deployment is following a structured geographic logic:

- National highway fast-charging corridors positioned at approximately 200 kilometre intervals to enable intercity EV travel without range anxiety.

- Urban charging networks targeting high-density residential towers, commercial districts, and fleet parking zones where overnight or daytime charging can occur.

- Fleet electrification as first-mover segments, with two-wheelers, three-wheelers, and electric buses carrying the highest volume of early EV deployment given their economic case for electrification.

How Is BPCL Accelerating India's Charging Network?

The involvement of Bharat Petroleum Corporation Ltd. (BPCL) illustrates how existing fuel retail infrastructure can be repurposed for the EV era. With 25,000 retail outlets spread across the country, BPCL possesses a distribution footprint that most dedicated EV charging operators cannot match. Of those outlets, 7,000 are technically positioned to host EV chargers, representing one of the largest pre-existing infrastructure bases available for rapid network deployment.

BPCL is also pursuing a dual-technology approach by investing in both fixed charging infrastructure and battery swapping systems simultaneously. This hedging strategy reflects the genuine uncertainty about which format will prove dominant across different use cases, with swapping potentially more advantageous for commercial fleets requiring fast turnaround.

Bioenergy is emerging as a complementary layer within this evolving infrastructure model. BPCL has outlined ambitions to establish 200 Compressed Biogas (CBG) plants, with a facility already operational in Kochi converting 150 tonnes of municipal waste into 5.6 tonnes of CBG daily.

Grid Stability: The Renewable Intermittency Problem That EVs Will Amplify

Renewable energy has crossed 50% of India's installed power generation capacity, a milestone that would have seemed distant a decade ago. The speed of this achievement, however, has created an operational challenge that now demands equal urgency: intermittency management at scale.

Solar curtailment during peak generation hours is reaching up to 70% in states such as Rajasthan and Gujarat, meaning significant quantities of generated renewable electricity are being wasted because the grid cannot absorb or store it in real time. Adding large-scale EV charging load onto a grid already struggling with intermittency management introduces a compounding challenge.

The storage technologies available to address this problem each carry distinct trade-offs:

| Storage Technology | Deployment Speed | Cost Trajectory | Best Use Case |

|---|---|---|---|

| Battery Energy Storage Systems (BESS) | Fast (months) | Declining rapidly | Short-duration balancing and EV grid support |

| Pumped Hydro Storage | Slow (years) | High capital expenditure | Long-duration and seasonal storage |

| Compressed Biogas (CBG) | Moderate | Improving | Distributed energy and waste management |

Battery storage is increasingly the preferred option for its speed of deployment and improving cost competitiveness. NTPC Renewable Energy and NTPC Green Energy are leading the transition toward round-the-clock renewable power delivery through storage integration, recognising that the grid must evolve from a supply-dispatch architecture to a demand-responsive, storage-buffered system capable of supporting EV adoption at scale. Furthermore, India's EV push and grid readiness remain deeply interconnected challenges requiring coordinated solutions across energy storage, minerals policy, and infrastructure deployment.

The next major ASX story will hit our subscribers first

The Circular Economy Dimension: Battery Recycling as a Strategic Mineral Source

The long-term sustainability of India's EV ecosystem depends not only on securing primary mineral supply but on developing the circular infrastructure that recovers critical materials from spent batteries back into the production chain. Urban mining, the recovery of metals from end-of-life batteries and consumer electronics, is emerging as a strategically important complement to primary extraction.

Domestic battery recycling companies are scaling operations to recover lithium, cobalt, nickel, graphite, and other metals from spent EV batteries. Furthermore, developing robust battery recycling processes is increasingly recognised as a critical component of long-term supply chain resilience, reducing the volume of critical minerals lost to landfill.

Simultaneously, the shift toward Lithium Iron Phosphate (LFP) battery chemistry offers a parallel route to reducing import dependency. LFP batteries carry several structural advantages for India's strategic position:

- They eliminate cobalt dependency entirely, removing one of the most geopolitically sensitive minerals from the supply equation.

- They significantly reduce nickel requirements, another high-risk import category.

- They deliver a lower cost per kilowatt-hour, improving EV affordability in a price-sensitive consumer market.

- They are particularly well-suited to two-wheelers, three-wheelers, and commercial fleet vehicles, the highest-volume segments in India's EV market.

LFP chemistry still requires lithium and graphite, meaning upstream diversification remains essential. However, a coordinated strategy combining LFP adoption, domestic recycling infrastructure development, and overseas lithium asset acquisition could meaningfully reduce India's critical mineral import exposure over the coming decade.

How India's Critical Mineral Strategy Compares Globally

Placing India's approach within a global comparative framework reveals both the strengths of its strategy and the competitive headwinds it faces.

| Country | Key Strategy | Domestic Mining | Overseas Acquisition | Recycling Maturity |

|---|---|---|---|---|

| China | Vertically integrated global dominance | Extensive | Extensive across Africa and Latin America | Advanced |

| United States | IRA-driven friend-shoring | Moderate | Active in Canada and Australia | Developing |

| European Union | Critical Raw Materials Act | Limited | Partnership-based | Advanced |

| Japan | Long-term bilateral agreements | Minimal | Extensive in Australia and Chile | Advanced |

| India | NCMM plus PLI plus overseas joint ventures | Emerging | Active in Argentina and Australia | Early-stage |

India's model most closely resembles Japan's historical approach, combining bilateral diplomacy with public sector-led overseas acquisition. With a population of 1.4 billion people and accelerating EV adoption, India's mineral requirements will become globally significant within a decade, giving it far greater leverage as a consumer nation than Japan possesses. Consequently, India lithium refining capacity will need to expand substantially to translate upstream acquisition gains into genuine domestic processing independence.

The Commercial Mobility Gap: Heavy Transport and the Infrastructure Challenge

While passenger EV adoption has generated the majority of policy and media attention, the electrification of heavy commercial transport presents a distinct and arguably more difficult set of problems. Fleet operators running heavy-duty freight vehicles face higher power cost burdens than passenger EV users, and the economics of switching become viable only when a combination of diesel price pressure, financing structures, and infrastructure density reaches a threshold that the market has not yet consistently achieved.

Charging infrastructure density along major freight corridors remains insufficient for reliable long-haul commercial EV operation, making battery swapping an increasingly important alternative that enables faster vehicle turnaround and reduces downtime for fleet operators. Rising diesel prices are functioning as a market-driven accelerant toward cleaner commercial alternatives. CNG and LNG pricing rationalisation has been identified as a near-term lever for bridging the commercial transport gap while heavy-duty EV infrastructure reaches operational maturity.

The Additive Energy Vision: Why India's Transition Is Not a Replacement Story

One of the most analytically important insights to emerge from senior industry discussions is the reframing of India's energy transition as an additive rather than substitutive process. The country remains approximately 90% dependent on oil imports, a structural vulnerability that makes energy diversification a national security imperative as much as an environmental commitment.

Rather than a linear replacement of fossil fuels with renewables, India is building a layered ecosystem where oil, gas, renewables, bioenergy, hydrogen, and electric mobility coexist and complement one another across different geographies, use cases, and timeframes. The strategic challenge is not choosing between these layers but synchronising their development so that mineral security, grid readiness, storage capacity, and charging infrastructure scale together rather than in isolation.

The industrial conglomerate Vedanta illustrates how domestic industrial capacity is aligning with this additive vision. Multi-billion rupee capacity expansions in aluminium, zinc, and copper, materials directly critical to EV manufacturing and charging infrastructure, are positioning domestic processing capability to serve the transition across multiple dimensions. These investments align with the broader Atmanirbhar Bharat industrial vision of reducing dependence on imported processed materials.

India's energy transition challenge is ultimately a systems integration problem. The technology is proven. The policy architecture is being built. The capital is beginning to mobilise. The binding constraint, and simultaneously the greatest strategic opportunity, lies upstream: securing and processing the critical minerals that make every other layer of the clean energy ecosystem viable.

Frequently Asked Questions: India EV Infrastructure and Critical Minerals

What is India's National Critical Mineral Mission?

The National Critical Mineral Mission (NCMM) is a government initiative backed by ₹34,000 crore in funding, designed to secure India's access to minerals essential for EV batteries, renewable energy systems, and clean technology manufacturing. It covers domestic exploration, overseas acquisition, research and development, recycling infrastructure, and workforce development across the critical minerals value chain.

Which minerals are most critical for India's EV sector?

The highest-priority minerals for India's EV ecosystem are lithium, cobalt, nickel, graphite, and rare earth elements for battery and motor systems, alongside copper and aluminium for electrical infrastructure and lightweight vehicle structures. Of these, lithium, cobalt, and graphite carry the most acute import dependency risk given India's limited domestic reserves and China's dominant position in global processing capacity.

Why does India import over 90% of its key battery minerals?

India has limited domestic reserves of the core battery minerals and has historically underinvested in geological exploration and refining infrastructure for these materials. The result is structural import dependence concentrated in China-linked supply chains, creating both price risk and geopolitical exposure that the National Critical Mineral Mission is designed to systematically reduce.

How is India's EV charging infrastructure being built out?

India is developing fast-charging corridors along national highways at approximately 200 kilometre intervals, with major fuel retailers like BPCL positioning chargers across 7,000 eligible outlets from their existing 25,000-outlet network. Urban charging infrastructure is expanding across high-density residential and commercial zones, while battery swapping is being developed as a parallel option particularly suited to commercial fleet operations.

How does grid-scale energy storage connect to India's EV goals?

Grid-scale storage is essential for stabilising a renewable-heavy power system that will supply India's EV charging network. Without adequate battery or pumped hydro storage capacity, solar curtailment rates currently reaching up to 70% during peak generation hours in states like Rajasthan and Gujarat will undermine both renewable energy economics and the reliability of EV charging at scale.

What is LFP battery chemistry and why does it matter for India?

Lithium Iron Phosphate (LFP) is a battery chemistry that eliminates cobalt and significantly reduces nickel requirements compared to NMC chemistries used in many current EV batteries. For India EV infrastructure and critical minerals planning, wider LFP adoption reduces exposure to two of its most geopolitically sensitive import dependencies while delivering lower cost per kilowatt-hour. LFP is particularly well-matched to India's highest-volume EV segments including two-wheelers, three-wheelers, and commercial fleet vehicles.

Disclaimer: This article contains forward-looking statements, projections, and analysis based on publicly available information and industry commentary. Figures and timelines relating to mineral import values, mission funding, infrastructure deployment targets, and EV adoption forecasts are sourced from reported data and expert commentary and may be subject to revision. This article does not constitute financial advice. Readers should conduct independent due diligence before making any investment or business decisions based on the information presented here.

Want to Track the Next Major Mineral Discovery Powering the Clean Energy Transition?

As demand for lithium, cobalt, and critical minerals accelerates alongside India's EV ambitions, Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, turning complex geological data into actionable investment insights — explore historic discoveries and their market returns, then begin your 14-day free trial to position yourself ahead of the market.