July 13, 2026

India's Hidden Energy Subsidy Architecture: Why the Price Freeze Was Never Sustainable

Across the global economy, few policy mechanisms carry as much political weight as retail fuel pricing. For large, import-dependent democracies, the decision of when to absorb commodity price shocks versus when to pass them directly to consumers is rarely driven by economics alone. It sits at the intersection of electoral mathematics, state enterprise viability, and macroeconomic stability. When India raises fuel prices after a four-year freeze, as it did in May 2026, it offers one of the most instructive examples of this tension playing out in real time.

Understanding why India raises fuel prices when it does, and why it resists doing so for as long as politically possible, requires examining the architecture of its domestic energy pricing system from the inside out.

When big ASX news breaks, our subscribers know first

How India's Retail Fuel Pricing System Actually Functions

India's fuel pricing framework operates as a hybrid model, sitting somewhere between full market liberalisation and administered pricing. The dynamic pricing mechanism introduced in 2010 was designed to link retail fuel costs to international crude benchmarks on a fortnightly basis, theoretically insulating state oil companies from sustained under-recovery periods. In practice, the government retains enormous discretionary power over when the mechanism is actually applied.

Three state-owned oil marketing companies (OMCs) dominate this system entirely. Indian Oil Corporation, Hindustan Petroleum Corporation (HPCL), and Bharat Petroleum Corporation (BPCL) collectively control more than 90% of India's 103,000-station fuel retail network. These entities set prices in coordination, meaning that a decision to freeze or adjust prices operates as a de facto national policy rather than a competitive market outcome.

The price consumers ultimately pay at the pump is assembled through a layered structure:

- Crude import cost is calculated from international benchmarks, primarily Brent and Dubai crude grades

- Refinery processing costs and applicable margins are added to arrive at the ex-refinery price

- Central government excise duty is applied, representing a significant revenue stream for New Delhi

- Dealer commissions are incorporated at the distribution level

- State-level VAT and local levies are layered on top, creating the primary source of price variation across the country

- Final retail price is declared by the three OMCs in tandem across the national network

State VAT rates vary dramatically across India's regions, ranging from roughly 15% in lower-tax jurisdictions to upwards of 35% in states with high fiscal dependence on fuel tax revenues. This explains why Delhi's prices serve as the standard national benchmark: at ₹98.64 per litre for petrol and ₹91.58 per litre for diesel following the May 2026 adjustments, they represent the lower end of the national price spectrum. Consumers in states like Maharashtra or Rajasthan routinely pay substantially more. For a real-time view of current petrol prices across India, regional breakdowns highlight just how wide this disparity can be.

Key Structural Insight: India's fuel pricing model is not a market mechanism in any conventional sense. It is an administratively managed system where political timing, OMC financial health, and electoral calendars all influence price-setting decisions as much as global crude benchmarks do.

The Four-Year Freeze: An Extraordinary Departure from Dynamic Pricing Norms

To appreciate the significance of the 2026 adjustment, it is essential to understand just how unusual a four-year pricing freeze actually is within the context of India's dynamic pricing framework. The mechanism was explicitly designed to prevent exactly this kind of multi-year divergence between international costs and domestic retail prices.

During this freeze period, India's OMCs absorbed the full gap between rising global crude costs and fixed domestic retail prices through their own balance sheets. The scale of this under-recovery reached a disclosed daily loss of ₹7.5 billion across state fuel retailers by the time of the May 2026 adjustment, according to a senior official from the federal oil ministry. With no government financial support forthcoming for the OMCs, the pricing correction became structurally unavoidable.

The financial logic is straightforward: if state enterprises are required to sell products below cost for extended periods without compensation, the resulting balance sheet deterioration eventually threatens their capacity to fund capital expenditure programmes, refinancing obligations, and operational continuity. The hidden liability accumulated not on government fiscal accounts but within OMC income statements, creating a pressure that could only be resolved through pricing action.

Policy Risk Callout: When retail fuel prices are maintained below cost-recovery levels across a sustained period, the financial stress migrates from the government's books onto state-owned enterprise balance sheets. This creates a deferred fiscal liability that eventually forces abrupt or compressed pricing corrections, often at the worst possible macro moment.

The Geopolitical Trigger: Strait of Hormuz and the $120 Oil Shock

What Caused the Sudden Crude Price Surge?

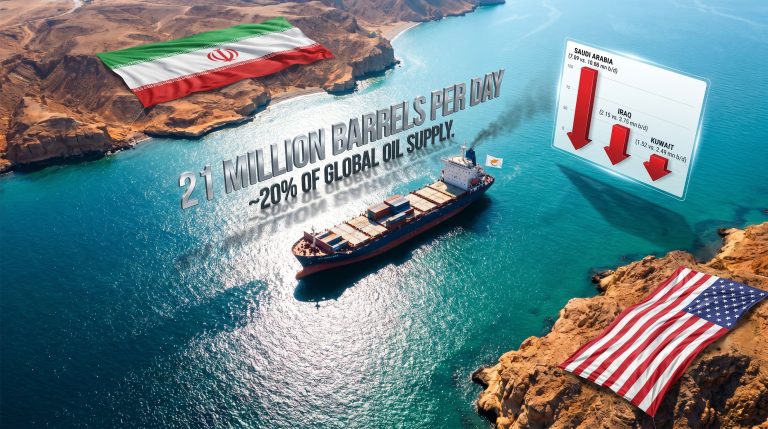

The immediate catalyst for India raising fuel prices was a geopolitical event with direct implications for global oil supply architecture. Military conflict involving the United States and Israel with Iran triggered the effective closure of the Strait of Hormuz, the narrow waterway through which approximately 20% of global seaborne oil trade passes daily. Furthermore, the resulting supply anxiety drove international crude prices above $120 per barrel before a partial pullback. These geopolitical oil price risks had been flagged by analysts well before the shock materialised.

For India, this was not an abstract commodity market development. As the world's third-largest oil importer and consumer, behind only the United States and China, India sources approximately 85 to 87% of its crude oil requirements from international markets. The Gulf region represents the largest single component of that supply mix, making Strait of Hormuz disruptions disproportionately impactful on India's import costs compared with most other major economies.

The currency dimension compounded this exposure. With the Indian rupee trading at approximately ₹96.35 per US dollar at the time of the adjustment, every dollar increase in crude prices translated into a larger rupee cost increase than it would have at a stronger exchange rate. The combination of elevated crude and a weaker rupee created a double pressure on OMC economics that the frozen retail price could not accommodate. Indeed, weakening confidence in the US dollar has added an additional layer of complexity to emerging market import cost calculations globally.

How India's Response Compared to Global Peers

India's adjustment, while significant domestically, remained modest relative to the underlying crude price shock when benchmarked against comparable economies:

| Economy | Fuel Price Response to Oil Shock | Adjustment Magnitude |

|---|---|---|

| United States | Immediate market pass-through | ~44% price increase |

| United Arab Emirates | Immediate market pass-through | ~52% price increase |

| India | Delayed administrative adjustment | ~3 to 4% cumulative hike |

| Indonesia | Partial administered adjustment | Varies by fuel grade |

| Other emerging markets | Mixed — rationing or large hikes | Varies widely |

Note: Comparative figures represent approximate cross-market analysis of fuel pricing responses to the 2026 oil shock. Individual country figures may vary by fuel grade and measurement period.

India's cumulative increase of approximately ₹3.9 per litre across two adjustments within a single week — first a ₹3.00 per litre increase then a further ~₹0.90 per litre days later — amounted to a fraction of the underlying cost shock. This deliberate under-correction reflects the political constraints under which the pricing decision was made, not an indication that OMC losses had been fully resolved. Notably, India's fuel hike remained among the lowest globally relative to the scale of the commodity price shock, reinforcing the degree to which domestic political considerations constrained the adjustment.

The Electoral Calculus Behind the Four-Year Delay

Few aspects of India's fuel pricing history are as revealing as the consistent alignment between price freezes and election cycles. Analysts and political observers have long noted this recurring pattern: retail fuel prices tend to remain suppressed during periods of significant electoral activity, then adjust after political outcomes are secured.

The 2026 freeze followed this pattern with notable precision. Key state assembly elections created a strong structural disincentive for the ruling Bharatiya Janata Party to impose visible consumer price increases. The BJP ultimately secured victories in two of the four key contested states before the pricing correction was implemented in May 2026. This sequencing is consistent with a broader historical pattern in Indian fuel policy where electoral outcomes precede pricing corrections rather than following them.

The political economy logic is straightforward: fuel prices are among the most visible and immediate economic variables experienced by Indian voters. A ₹3 per litre increase in petrol prices translates directly and immediately into higher commuting costs for hundreds of millions of households, creating salient consumer pain that any incumbent government would prefer to avoid during contested electoral periods.

Inflationary Transmission: How a Fuel Hike Spreads Through India's Economy

When India raises fuel prices, the inflationary consequences extend well beyond the pump. Fuel is a foundational input cost across India's logistics infrastructure, and road freight accounts for approximately 65 to 70% of goods movement by volume across the country. This means virtually every consumer product category carries an embedded sensitivity to fuel price movements.

The transmission mechanism operates through several distinct channels:

- Direct transport cost inflation: Road freight operators pass fuel cost increases through to shippers, raising the delivered cost of goods across all categories

- Agricultural produce pricing: Farm-to-market transport chains are particularly sensitive to diesel price movements, creating upward pressure on food prices

- Cold chain and last-mile logistics: Temperature-controlled supply chains and urban delivery networks carry higher fuel intensity than bulk freight

- Manufacturing input cost escalation: Even sectors with relatively low direct fuel exposure experience second-round cost increases as logistics and energy costs rise

Historical Reserve Bank of India analysis suggests that a ₹1 per litre increase in fuel prices has contributed roughly 10 to 15 basis points to headline consumer price inflation in India, with the full pass-through typically unfolding over several months rather than immediately. A cumulative ₹3.9 per litre increase therefore carries a meaningful inflationary signal, particularly if it coincides with already-elevated food prices or further supply chain disruptions.

Sector-by-Sector Inflation Exposure

| Sector | Fuel Cost Exposure | Expected Price Pressure |

|---|---|---|

| Road freight and logistics | High (direct fuel cost) | Moderate to significant |

| Agricultural produce | High (transport-dependent) | Moderate |

| Manufacturing and FMCG | Medium (indirect input) | Low to moderate |

| Aviation (jet fuel linked) | High | Moderate |

| Consumer commuting costs | Direct (petrol/diesel) | Immediate and visible |

Prime Minister Modi's concurrent public messaging, urging citizens to limit discretionary travel and reduce gold purchases, reflects an awareness that demand-side behavioural management can complement supply-side pricing adjustments. The gold import restriction is particularly notable: it forms part of a broader import compression strategy designed to reduce foreign exchange outflows and defend the rupee at a time when elevated crude costs are widening India's current account deficit.

Macro Context: India's fuel price adjustment is one element of a coordinated import management response that also encompasses restrictions on gold and silver imports. The underlying objective across all three measures is the same: reduce foreign exchange demand, limit current account deterioration, and defend the rupee during an elevated commodity price environment.

The next major ASX story will hit our subscribers first

India's Oil Import Dependency: The Structural Vulnerability

The 2026 oil shock has exposed a structural vulnerability in India's energy economy that short-term price adjustments alone cannot resolve. Sourcing 85 to 87% of crude requirements from international markets while ranking as the world's third-largest consumer creates a permanent macro sensitivity to supply chain disruptions, currency movements, and geopolitical events in producing regions.

At $120 per barrel crude, India's annualised import bill escalates dramatically from prior baseline assumptions, placing sustained upward pressure on the current account deficit and the rupee simultaneously. This dynamic creates a self-reinforcing feedback loop: a weaker rupee increases the rupee cost of crude imports even at a constant dollar price, which widens the trade deficit further, which puts additional pressure on the currency.

India's strategic petroleum reserves provide some buffer against short-term disruptions but are not sized to absorb sustained elevated pricing over quarters. The reserve infrastructure represents days to weeks of consumption coverage, not months, limiting its utility as a policy tool against anything other than transient supply interruptions. In addition, oil markets under trade war pressure have further complicated India's ability to secure favourable long-term supply agreements, adding another layer of strategic uncertainty to its import dependency.

Forward-Looking Scenarios: What Happens to India's Fuel Pricing Policy from Here

Three distinct pathways are plausible from the current pricing inflection point:

Scenario 1: Continued staged corrections (base case)

OMCs implement further incremental price adjustments over subsequent weeks as crude prices stabilise. Inflation rises modestly but remains within the RBI's target tolerance. The government avoids a single large politically visible correction by spreading the adjustment across multiple smaller steps.

Scenario 2: Crude price normalisation provides relief

If the Strait of Hormuz reopens and crude retreats below $90 per barrel, the pressure for further retail price increases diminishes. OMCs recover margins without additional consumer-facing adjustments. Political pressure to reverse some of the recent hike may re-emerge ahead of future election cycles, creating the conditions for the next freeze-and-correct cycle.

Scenario 3: Sustained elevated crude forces structural reform

If international oil prices remain above $110 per barrel for an extended period, the current pricing architecture becomes untenable without either sustained OMC balance sheet damage or a fundamental reform of how excise duties and the price adjustment mechanism are structured. This scenario is speculative but would likely accelerate EV adoption incentives and longer-term demand-side energy diversification as complementary policy responses. Furthermore, India's LNG tax structure may come under renewed scrutiny as policymakers assess whether the broader energy import framework is fit for purpose in a persistently elevated price environment.

Disclaimer: The scenarios above represent analytical projections based on current market conditions and historical policy patterns. They do not constitute financial advice. Future outcomes will depend on numerous variables including geopolitical developments, crude price trajectories, and domestic political conditions that cannot be reliably predicted.

Key Reference Data: India's Fuel Price Adjustment at a Glance

| Metric | Detail |

|---|---|

| First price hike in | Four years |

| First adjustment (May 2026) | ₹3.00 per litre (petrol and diesel) |

| Second adjustment (within one week) | ~₹0.90 per litre |

| Delhi petrol price post-adjustment | ₹98.64 per litre |

| Delhi diesel price post-adjustment | ₹91.58 per litre |

| OMC daily loss at time of hike | ₹7.5 billion |

| Global crude price at trigger point | Above $120 per barrel |

| Exchange rate reference | ₹96.35 per USD |

| India's global oil import rank | 3rd largest importer and consumer |

| OMC retail network coverage | 103,000 stations, 90%+ market share |

| Crude import dependency rate | ~85 to 87% of requirements |

Frequently Asked Questions: India Raises Fuel Prices

Why has India raised fuel prices now?

State-owned oil marketing companies were recording daily losses of ₹7.5 billion due to the divergence between frozen retail prices and elevated international crude costs, which surged above $120 per barrel following Strait of Hormuz disruptions. With no government financial support allocated to OMCs, a pricing correction became unavoidable. The global oil price rally triggered by the conflict also removed any remaining justification for maintaining the freeze.

How much have petrol and diesel prices increased?

Two adjustments were implemented within a single week: an initial rise of ₹3.00 per litre followed by a further increase of approximately ₹0.90 per litre, bringing Delhi petrol to ₹98.64 per litre and diesel to ₹91.58 per litre.

Why do fuel prices vary across Indian states?

State governments apply varying VAT rates and local levies on top of central excise duty, creating significant regional price dispersion. States with higher fiscal dependence on fuel tax revenues tend to have substantially higher consumer prices than the Delhi benchmark.

Will the fuel price hike cause significant inflation?

Fuel costs underpin India's road freight network, which moves the majority of goods by volume. Economists generally expect a cumulative increase of this magnitude to add upward pressure to headline CPI, particularly through food and manufactured goods transport costs, though the full pass-through typically takes several months to fully materialise.

Why did India wait four years to raise fuel prices?

Multiple state and national election cycles during this period created strong political incentives to suppress visible consumer price increases. The pricing correction was implemented after the BJP secured electoral outcomes in key contested states, consistent with a longer historical pattern of price freezes preceding Indian election cycles.

Want to Track the Next Big Commodity Market Shift Before the Crowd Does?

India's fuel pricing crisis illustrates how geopolitical shocks — from Strait of Hormuz disruptions to $120-per-barrel crude — can rapidly reshape commodity markets and create significant investment opportunities. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they hit the market, transforming complex commodity data into actionable insights for both short-term traders and long-term investors — explore historic discoveries and the returns they generated to see why a 14-day free trial could be your most informed market decision yet.