July 13, 2026

The Hidden Architecture of India's Inflation Problem

Few economic indicators reveal as much about a country's structural vulnerabilities as its inflation composition. For most developed economies, rising consumer prices are primarily a demand-side phenomenon, shaped by wage growth, monetary policy, and credit cycles. India's inflation story is fundamentally different. It is built on three interlocking dependencies, each capable of amplifying the others at precisely the wrong moment.

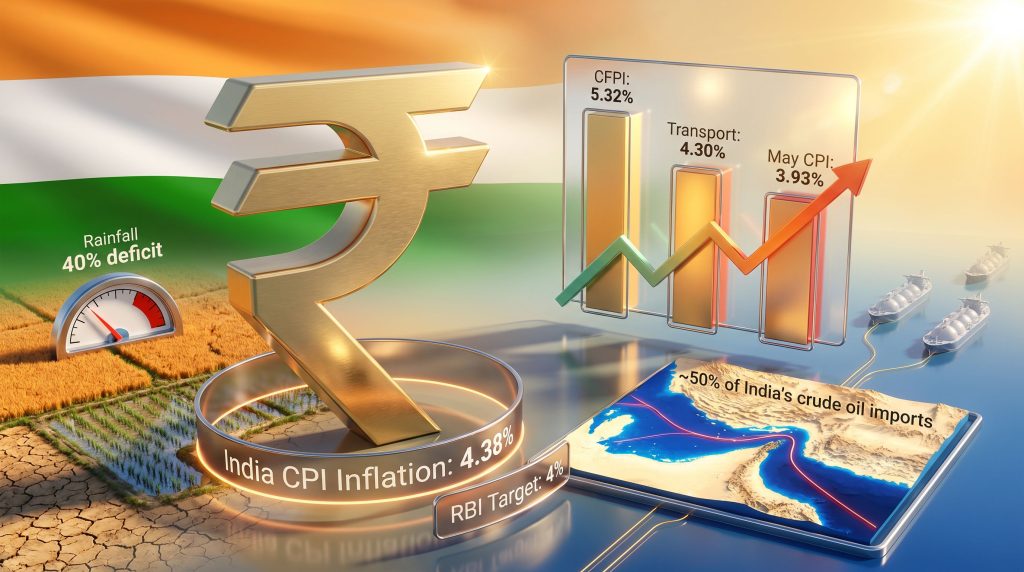

When India inflation June 4.38% was confirmed as the headline CPI reading, rising from 3.93% in May, the number itself was only marginally above consensus. What the figure concealed, however, was a convergence of geopolitical shock, agricultural stress, and energy transit risk that makes this particular inflation episode structurally more complex than any single monthly reading can capture.

When big ASX news breaks, our subscribers know first

Understanding the June 2026 Reading in Context

Released by India's Ministry of Statistics and Programme Implementation (MoSPI) on July 13, 2026, the June inflation data marked the eighth consecutive month of consumer price increases. The 4.38% headline CPI print exceeded the consensus economist forecast of approximately 4.30%, as compiled by a Reuters poll of analysts.

What makes this figure particularly significant is not the absolute level, but the acceleration. The 44 basis point jump from May's 3.93% reflects a rapid deterioration in two critical sub-categories: food and transport.

| Inflation Component | May 2026 | June 2026 | Change |

|---|---|---|---|

| Headline CPI | 3.93% | 4.38% | +0.45 pp |

| Consumer Food Price Index (CFPI) | Not specified | 5.32% YoY | Elevated |

| Transport Inflation | 1.75% | 4.30% | +2.55 pp |

| RBI Headline Forecast FY2027 | N/A | 5.10% (projected) | Above target |

| RBI Core Inflation Forecast FY2027 | N/A | 4.70% (projected) | Above target |

The 2.55 percentage point surge in transport inflation in a single month is the kind of movement that monetary policymakers track with particular concern. It signals that energy cost pressures are no longer localised at the fuel pump. They are transmitting into the broader logistics and supply chain infrastructure of the economy.

India's Energy Dependency: The Strait of Hormuz Problem

To understand why India's inflation is so sensitive to events unfolding thousands of kilometres away in the Persian Gulf, it is essential to grasp the scale of the country's energy import dependency.

India sources approximately 85% of its total fuel requirements from international markets, making it one of the most import-dependent major economies on the planet. The geographic chokepoint that concentrates this risk is the Strait of Hormuz, a narrow maritime corridor through which a substantial share of global energy supplies passes daily.

India's exposure to this single transit corridor is extensive:

- Approximately 50% of India's crude oil imports transit through the Strait of Hormuz

- Around 60% of its liquefied natural gas (LNG) supply depends on the same route, which mirrors broader concerns about the LNG supply outlook in 2025 and beyond

- Virtually all of its liquefied petroleum gas (LPG) imports flow through this corridor

Following a brief ceasefire between the United States and Iran in June 2026, hostilities resumed in early July, reigniting pressure on global crude benchmarks and directly feeding into India's domestic fuel pricing mechanisms. The resulting oil price rally saw global crude benchmarks climb as both parties contested control of the Strait, according to reporting from CNBC on July 12, 2026.

This is not merely a temporary geopolitical headline risk. For India, disruption to Strait of Hormuz transit is a direct inflationary mechanism, one that bypasses the central bank's toolkit entirely and strikes at the cost base of virtually every sector of the economy.

The transport inflation surge from 1.75% to 4.30% between May and June is the clearest statistical fingerprint of this transmission. When fuel costs rise, freight costs follow. When freight costs rise, input costs across manufacturing, retail, and services follow. This sequential pass-through is the pipeline through which geopolitical risk becomes kitchen-table inflation.

The Monsoon Variable: Why Rainfall Patterns Are an Inflation Instrument

India's agricultural sector operates under a climate dependency that has no equivalent in most large economies. Monsoon rainfall does not merely influence farm output; it shapes rural incomes, sowing decisions, crop health, and ultimately the food price index that constitutes a significant portion of the CPI basket.

The 2026 monsoon season has been characterised by extreme oscillation rather than simple deficiency:

- June 2026 recorded a 40% rainfall deficit against the long-period average

- A rapid monsoon advancement reduced the all-India deficit to 15% by July 8, 2026

- Despite this partial recovery, the India Meteorological Department (IMD) forecast July rainfall at 6% below the long-period average

Crisil, the S&P Global-owned Indian research and ratings firm, highlighted in a July 2026 report that extreme swings between rainfall scarcity and surplus can be as economically damaging to agriculture as a prolonged dry spell. The reasoning is counterintuitive but well-supported: when rainfall arrives in sudden, heavy bursts after a dry period, it disrupts sowing schedules, damages crops in early growth stages, and creates logistical chaos in rural supply chains.

This dynamic is often underappreciated in mainstream inflation analysis, which tends to focus on total rainfall volume rather than its temporal distribution. A monsoon season that delivers adequate total rainfall in an uneven pattern can still produce food supply shortfalls and price volatility.

El Niño: The Medium-Term Agricultural Risk Factor

Beyond the immediate monsoon season, India faces the additional complication of El Niño weather patterns in 2026. El Niño events historically correlate with weaker and more erratic South Asian monsoons, and the Reserve Bank of India has explicitly flagged crop shortage risk from this phenomenon in its forward guidance.

This matters for inflation forecasting because agricultural price pressures driven by El Niño can persist for multiple growing seasons. Consequently, the food inflation component of India's CPI may not normalise quickly even if geopolitical tensions ease.

How the RBI Is Navigating a Classic Policy Dilemma

At its most recent policy meeting, the Reserve Bank of India maintained interest rates at existing levels, a decision that reflected the complexity of the trade-offs facing the central bank rather than any confidence that inflation is under control.

The RBI's forward guidance was notably cautious. The bank projects:

- Headline inflation reaching 5.1% in the financial year ending March 2027

- Core inflation reaching 4.7% over the same period

- Economic growth moderating alongside rising prices, creating a mild stagflationary risk profile

Furthermore, the RBI's emphasis on core inflation as its primary policy anchor is a technically important distinction. Core inflation strips out the volatile food and fuel components that the central bank cannot directly control through interest rate adjustments. These inflation projections mirror concerns seen globally, where persistent cost pressures complicate central bank decision-making.

The bank's concern is that if energy and food price pressures persist for long enough, they will begin feeding into core categories through higher input costs, transportation expenses, and operational overheads. The transmission mechanism works in sequential steps:

- Elevated global oil prices push domestic fuel costs higher

- Higher fuel costs increase freight and logistics expenses across supply chains

- Rising logistics costs inflate manufacturing and retail input costs

- Persistent input cost pressure begins lifting prices across core goods and services

- Core inflation above 4.7% creates pressure for the RBI to consider rate increases

- Rate increases risk slowing growth in an economy already navigating external headwinds

This is the dilemma the RBI is managing in real time. Rate cuts would support growth but risk entrenching inflation above target. However, rate hikes would address price pressures but could suppress consumption and investment in an already externally pressured economy.

India in the Regional Inflation Landscape

Placing India inflation June 4.38% within its regional and global context helps illustrate both the relative moderation of the headline figure and the structural distinctiveness of India's inflation drivers.

| Economy | Approximate Inflation Rate (Mid-2026) | Primary Driver |

|---|---|---|

| India | 4.38% (June 2026) | Food, fuel, monsoon volatility |

| China | Below 2% (deflationary pressure) | Weak domestic demand |

| Indonesia | Approximately 3-4% | Energy subsidy adjustments |

| Brazil | Approximately 5-6% | Currency depreciation, food costs |

| United States | Moderating post-cycle | Services, shelter inflation |

Note: Regional figures are directional estimates. Readers should consult respective national statistics agencies for current, precise data.

India occupies a unique position in this comparison. Its inflation rate is neither alarmingly high by emerging market standards nor comfortably within target. What distinguishes it is the structural composition of its price pressures: an import-heavy energy sector, a monsoon-dependent agricultural system, and a geographic concentration of energy transit risk in a single maritime chokepoint.

The trade war impacts reshaping global supply chains add yet another layer of complexity, as disrupted trade flows create additional cost pressures that ripple through import-dependent economies like India.

Most major economies face one or two of these vulnerabilities. India faces all three simultaneously, and their effects are mutually reinforcing rather than independent.

The next major ASX story will hit our subscribers first

Three Scenarios for India's Inflation Trajectory

Investors and policymakers tracking India's macro outlook need to consider a range of forward scenarios, each with materially different implications for growth, monetary policy, and asset markets.

Scenario A: Geopolitical De-escalation

If U.S.-Iran hostilities ease and Strait of Hormuz transit normalises, global crude prices would likely moderate, reducing the fuel-driven component of India's inflation. Combined with a normalising monsoon, this could see headline CPI retreating toward the RBI's 4% target by early FY2027, preserving the bank's rate-hold stance and supporting the growth trajectory.

Scenario B: Prolonged External Shock

If Strait of Hormuz disruptions persist through the second half of 2026, fuel costs remain elevated, and El Niño produces meaningful crop shortfalls, India's India inflation June 4.38% reading may prove to be merely the beginning of a more sustained upward trajectory. In this scenario, core inflation would likely breach 4.7%, creating genuine pressure for a rate hike cycle that would moderate growth more sharply than current projections indicate.

Scenario C: Domestic Demand Resilience

A scenario in which rural income recovery, supported by a late but adequate monsoon, offsets food price pressure, while government intervention through fuel subsidy adjustments or strategic food reserve releases dampens the CPI trajectory. In addition, in this case, inflation could peak below the RBI's forecast, enabling a soft landing without requiring rate hikes.

What Investors Should Watch in the Months Ahead

For those monitoring India's macroeconomic trajectory, several indicators will be decisive in determining which scenario plays out:

- IMD monthly monsoon updates: Rainfall distribution in July and August will determine kharif crop outcomes and the near-term food inflation trajectory

- Brent crude benchmarks: Global oil price direction, shaped heavily by U.S.-Iran conflict developments, will drive the transport and fuel inflation components

- RBI policy meeting minutes: Any shift in tone from the central bank's communications will signal whether a rate adjustment is being actively considered

- MoSPI monthly CPI releases: Watching whether transport and food inflation components moderate or accelerate through Q3 2026

- IMF and World Bank growth revisions: External assessments of India's FY2027 growth outlook will reflect whether the stagflation risk scenario is gaining credibility

The consumer price impacts of sustained energy and food pressures will ultimately determine whether Indian households face an extended period of purchasing power erosion through the remainder of 2026.

Frequently Asked Questions

What was India's inflation rate in June 2026?

India's headline Consumer Price Index inflation for June 2026 came in at 4.38%, up from 3.93% in May 2026. The figure was released by MoSPI on July 13, 2026, and exceeded the consensus forecast of 4.30% from a Reuters poll of economists. According to CNBC's analysis, the reading has significant implications for RBI rate decisions in the months ahead.

Why did India's inflation rise so sharply between May and June 2026?

The acceleration was driven by a combination of higher food prices (Consumer Food Price Index at 5.32% year-on-year), a significant jump in transport inflation from 1.75% to 4.30%, and elevated global fuel costs linked to the resumption of U.S.-Iran hostilities and associated pressures on Strait of Hormuz energy transit routes.

What is the RBI's inflation forecast for FY2027?

The Reserve Bank of India projects headline inflation at 5.1% and core inflation at 4.7% for the financial year ending March 2027, reflecting sustained fuel price pressure and agricultural risk from El Niño weather patterns.

Is 4.38% above the RBI's official inflation target?

Yes. The RBI's headline inflation target is 4%. June 2026's reading of 4.38% places the economy above this threshold, and the bank's own projections suggest inflation will remain above target through FY2027.

How does the U.S.-Iran conflict affect Indian consumers?

India imports approximately 85% of its fuel requirements from international markets and relies on the Strait of Hormuz for around half of its crude oil, 60% of its LNG, and virtually all of its LPG. When conflict disrupts this corridor, domestic fuel prices rise, which then transmits into transport, logistics, manufacturing costs, and ultimately consumer prices across the entire economy.

What role does the monsoon play in India's inflation?

India's food price index is heavily shaped by monsoon rainfall patterns. A deficient or erratic monsoon disrupts crop yields, sowing decisions, and rural supply chains. In 2026, extreme swings between rainfall scarcity and surplus have created agricultural uncertainty that is contributing to elevated food inflation, with the Consumer Food Price Index running at 5.32% year-on-year in June. For historical context on how Indian CPI has behaved across economic cycles, the World Bank's India inflation data provides a valuable long-term perspective.

This article is for informational purposes only and does not constitute financial or investment advice. Forecasts, scenario projections, and forward-looking statements are subject to material uncertainty. Readers should consult qualified financial advisors and primary data sources before making any investment or economic decisions based on the information presented here.

Want to Stay Ahead of the Market Shifts Driving Commodity and Resource Sector Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex resource data into actionable investment insights — explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.