July 13, 2026

When Capital Structure Becomes the Real Story in Junior Gold Mining

In the world of junior resource development, securing a binding, multi-instrument financing package is arguably the most consequential event a company can experience. It transforms a project from a well-documented aspiration into a legally committed construction program with defined timelines, capital certainty, and stakeholder accountability. For investors tracking West African gold development, understanding how these capital structures are assembled — and why their architecture matters as much as their size — is increasingly essential knowledge.

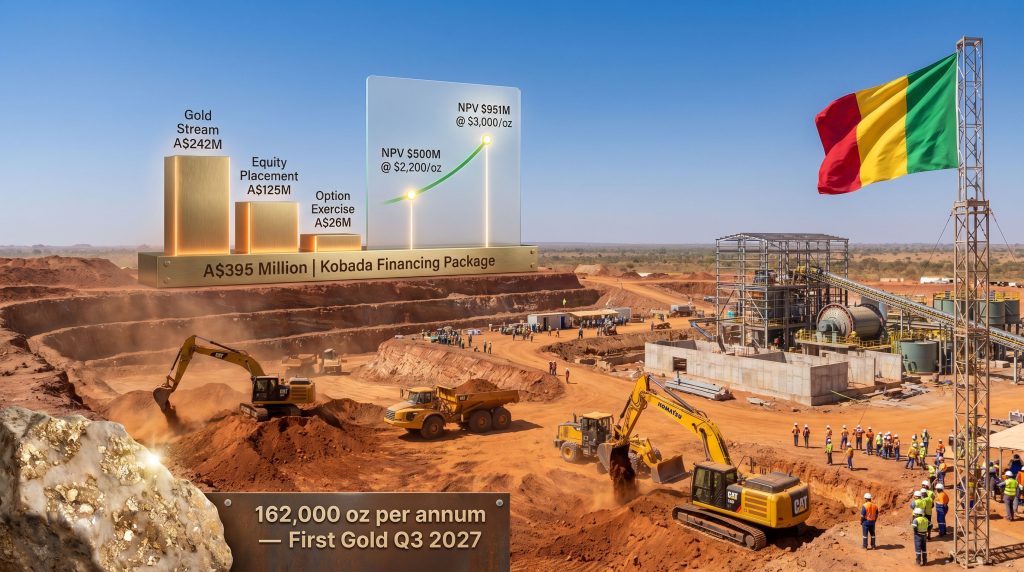

Toubani secures financing for Kobada gold mine construction represents precisely this kind of structural milestone. At A$302 million (~$208 million USD) in binding commitments, with an additional senior secured facility of up to $40 million USD (A$58 million) being progressed in parallel, the Kobada financing deserves examination not just as a corporate announcement but as a case study in how modern junior miners navigate capital markets to bring West African gold assets into production.

When big ASX news breaks, our subscribers know first

What Makes Kobada Unusual Among West African Development Projects

The Oxide Ore Advantage

Kobada's geological profile sets it apart from many comparable West African development projects. The deposit is dominated by near-surface oxide mineralisation, an ore type that carries substantial processing advantages over sulphide-hosted gold.

Oxide ores have already undergone natural weathering processes that break down sulphide minerals, meaning gold is typically liberated more readily during processing. This translates into:

- Lower energy consumption during comminution and leaching

- Higher gold recovery rates compared to refractory sulphide ores

- Significantly reduced processing plant complexity and capital cost

- Faster ramp-up to design throughput following commissioning

The Kobada Definitive Feasibility Study reflects these geological advantages directly in its economics. The plant construction cost of US$60 million is notably lean for a project targeting 162,000 ounces of annual gold production in its first seven years of operation. For context, sulphide-dominated projects of equivalent scale in West Africa frequently require processing infrastructure costing two to three times that figure, particularly where pressure oxidation or roasting circuits are required to liberate refractory gold. A definitive feasibility study of this calibre provides investors with a strong foundation for evaluating the project's economic credibility.

DFS Economics at a Glance

| Metric | Value |

|---|---|

| Annual production (years 1–7) | 162,000 oz gold |

| Primary ore type | Near-surface oxide |

| Total development capital | US$216 million |

| Plant construction cost | US$60 million |

| Non-process infrastructure | US$43 million |

| Post-tax NPV at $2,200/oz | $500 million |

| IRR at $2,200/oz | 50% |

| Post-tax NPV at $3,000/oz | $951 million |

| IRR at $3,000/oz | 79% |

The sensitivity of Kobada's NPV to gold price is striking. A move from $2,200/oz to $3,000/oz nearly doubles the project's post-tax net present value, from $500 million to $951 million. Considering the current gold price outlook, investors should note that DFS base-case projections may materially understate the project's economic potential, though this remains speculative and subject to commodity price volatility.

Disclaimer: All financial projections referenced in this article are drawn from company DFS documentation and involve forward-looking assumptions. Actual outcomes may differ materially from modelled results. This article does not constitute financial advice.

How Toubani Secures Financing for Kobada Gold Mine Construction: The Three-Pillar Structure

Pillar One: The Gold Stream Agreement

The cornerstone of the binding financing package is a $160 million USD (A$232 million) gold stream executed with Eagle Eye Assets (EEA), Toubani's major strategic shareholder. Under the terms of this instrument, EEA receives an 11.1% share of Kobada's future gold production, purchased at 20% of prevailing spot gold price.

Gold streaming is a financing mechanism that is often misunderstood by investors unfamiliar with the mining sector. It is worth clarifying what distinguishes it from conventional debt:

- No fixed repayment schedule. The obligation is fulfilled through gold deliveries once production commences, meaning there is no principal repayment pressure during construction or ramp-up.

- No interest rate exposure. Unlike senior debt, streaming instruments are not subject to floating rate risk, which is a material advantage in environments where interest rates are elevated.

- Production-linked structure. If production is delayed or temporarily curtailed, the delivery obligation adjusts accordingly, reducing the risk of technical default scenarios that can arise under rigid debt covenants.

- Opportunity cost for the streaming counterparty. EEA is effectively acquiring future gold at a substantial discount to spot price, compensating them for the upfront capital deployment and construction-phase risk.

First drawdown of the gold stream is expected during Q3 2025, with construction activities already well advanced at the time of the financing announcement.

Pillar Two: Strategic Equity Placement

Alongside the gold stream, Toubani has executed a fully underwritten A$70 million accelerated non-renounceable entitlement offer. This equity component serves a distinct purpose within the capital stack: it funds balance sheet liquidity requirements that are not easily addressed through production-linked instruments. Furthermore, understanding the range of ASX capital raising methods available to junior miners helps contextualise why this structure was chosen over alternatives.

A key and often overlooked element of the equity component is its specific allocation toward recoverable VAT payments that become due during the construction phase. In West African jurisdictions including Mali, VAT recovery on construction-phase expenditures can create significant working capital pressure. Governments typically refund VAT, but timing mismatches between VAT outflows and refund receipts can strain liquidity if not proactively funded. The equity component explicitly addresses this risk.

EEA has committed to maintaining its pro-rata ownership interest through the offer structure.

Pillar Three: Option Exercise by EEA

EEA has exercised 78 million existing options at A$0.336 per option, generating an additional A$26 million in equity capital. This exercise increases EEA's total ownership in Toubani to approximately 35%, creating significant governance alignment between the largest shareholder and the broader investor base.

The binding commitments across all three pillars combine to form the total package as announced, with the additional senior secured facility providing supplementary balance sheet capacity against construction contingencies.

The Eagle Eye Assets Dual-Commitment Architecture

Why Anchor Investor Structure Matters More Than Most Investors Realise

EEA's position in this transaction is architecturally unusual and worth examining in depth. Most junior mining financings involve a clear separation between debt providers, streaming counterparties, and equity holders. These groups frequently have misaligned incentives: debt providers prioritise capital preservation and covenant compliance, while equity holders prioritise growth and production volume.

EEA's simultaneous participation as both the gold stream counterparty and a major equity investor eliminates a significant portion of this misalignment. Its financial return is directly tied to both the successful execution of construction and the long-term production performance of the mine. This creates an unusually strong incentive for constructive engagement if operational challenges arise during construction or ramp-up.

In junior mining finance, the governance structure surrounding construction-phase capital is frequently as important as the quantum of funding secured. An anchor investor with economic exposure across multiple instruments has a stronger incentive to support solutions during difficulties than a traditional project debt provider operating under rigid covenant frameworks.

Following the completion of all financing instruments, EEA holds approximately 35% of Toubani's issued capital, making it by far the largest single shareholder and a dominant voice in any future capital decisions.

Mali's Regulatory Framework and What the 2023 Mining Code Changes

Sovereignty, State Participation, and the New Normal in West African Mining

Mali's 2023 mining code revised the terms under which major projects operate in the country, most significantly through the formalisation of mandatory state equity participation. Under this framework, the Malian State holds a 35% equity interest in Kobada, including a 10% free carried interest that requires no capital contribution from the state.

This structure reflects a broader trend across West Africa, where resource nationalism has become embedded in legislative frameworks rather than pursued through ad hoc negotiations. For investors assessing Kobada specifically, several points are worth understanding:

- The mining licence for Kobada was formally transferred to Toubani in January 2026, confirming that all sovereign risk hurdles related to licence ownership have been navigated.

- Toubani retains a 65% operating interest, with full responsibility for project execution and associated capital deployment.

- The free carried interest means the Malian State benefits from project economics without contributing to construction capital, which is standard under the revised code but reduces the equity available to fund construction relative to a 100%-owned structure.

- Ausenco, a globally recognised EPCM contractor, has been appointed to lead engineering, procurement, and construction management, providing independent technical oversight that should satisfy both institutional investors and regulatory stakeholders.

Construction Progress: Where Kobada Stands Right Now

Key Milestones and Timeline

| Milestone | Status / Target Date |

|---|---|

| Final Investment Decision (FID) | Approved March 2026 |

| Mining Licence Transfer | January 2026 |

| Capital Expenditure Committed | Over 60% as of mid-2026 |

| Personnel Mobilised On Site | More than 500 |

| First Gold Production Target | Q3 2027 |

The over-60% capital commitment figure is particularly significant from a project risk perspective. In mining construction, the period between FID and approximately 50–60% capital commitment represents the highest execution risk window, as this is when contractor mobilisation, materials procurement, and site establishment are occurring simultaneously. Beyond this threshold, the critical path to completion becomes substantially more defined and controllable.

Toubani's managing director described the project as on schedule, with major construction activities commencing as key contractors and critical materials reached site. The combination of personnel numbers and capital commitment levels suggests the project is well into active construction rather than early-stage mobilisation.

The next major ASX story will hit our subscribers first

Comparing Kobada's Financing Model to Conventional Project Finance

Stream-Plus-Equity vs. Traditional Debt Structures

| Feature | Gold Streaming | Senior Project Debt | Equity-Only |

|---|---|---|---|

| Repayment obligation | Production-linked | Fixed principal + interest | None |

| Dilution to shareholders | Minimal | None | High |

| Cash flow during ramp-up | Reduced by stream offtake | Debt service pressure | Full cash retention |

| Alignment with production | High | Moderate | High |

| Flexibility under operational stress | High | Low (covenant risk) | High |

Kobada's hybrid structure is deliberately designed to minimise fixed financial obligations during the construction and early production phases, while maintaining sufficient equity capital to absorb unforeseen costs. The senior secured facility being progressed separately functions as a contingency buffer rather than a primary construction funding instrument.

This approach reflects a sophisticated understanding of construction-phase financial risk. Fixed debt service obligations during ramp-up periods have historically been a primary source of distress for junior miners, particularly where commissioning timelines extend or gold recoveries are below initial expectations during plant optimisation. Consequently, understanding the broader spectrum of junior mining risks and rewards remains critical for investors evaluating Kobada's investment case.

Resource Growth Strategy Running Alongside Construction

Why Management Is Drilling While Building

One of the less-discussed aspects of Kobada's development strategy is Toubani's explicit commitment to pursuing resource growth concurrently with construction. The primary exploration target is additional near-surface oxide mineralisation with the potential to extend mine life beyond the current DFS schedule.

This concurrent approach carries both strategic logic and financial risk. On the positive side:

- Extending mine life from a fully funded, operating project is exponentially cheaper than developing a new deposit.

- Additional oxide resources discovered proximal to existing infrastructure require minimal incremental capital for exploitation.

- Extending reserve life improves the project's attractiveness to potential acquirers or strategic partners in the post-production phase, particularly given heightened gold M&A activity across the sector.

The risk, however, is that exploration capital deployed during construction competes with contingency reserves. The binding financing package appears to have specifically allocated capacity for this parallel strategy, suggesting management has modelled the capital requirements carefully.

Frequently Asked Questions

What is the total binding financing package for Kobada?

The binding financing package totals A$302 million (~$208 million USD), comprising a $160 million USD gold stream, a A$70 million fully underwritten equity placement, and a A$26 million option exercise by Eagle Eye Assets. An additional senior secured facility of up to $40 million USD is being pursued to provide supplementary balance sheet flexibility.

When is first gold production expected at Kobada?

Toubani has targeted Q3 2027 for first gold production, following FID approval in March 2026 and with construction now more than 60% committed by capital expenditure.

What is the Malian State's stake in Kobada?

The Malian State holds a 35% equity interest in Kobada under Mali's 2023 mining code, including a 10% free carried interest. Toubani retains a 65% operating interest.

How does a gold stream differ from a mining royalty?

A gold stream involves the purchase of a percentage of physical gold production at a predetermined discount to spot price. A royalty, by contrast, is typically a percentage of revenue or production value paid to the royalty holder without physical delivery obligations. Streams generally involve larger upfront capital commitments from the streaming counterparty than royalties.

What gold price assumptions underpin Kobada's DFS returns?

The DFS models a post-tax NPV of $500 million and an IRR of 50% at a gold price of $2,200/oz, rising to a $951 million NPV and 79% IRR at $3,000/oz. These projections involve forward-looking assumptions and should not be treated as guaranteed outcomes.

What the Kobada Financing Package Signals for the Sector

For investors and industry observers tracking West African gold development, the Kobada financing provides several instructive data points:

- Fully funded certainty through a hybrid instrument stack shifts execution risk from capital availability to construction delivery — a fundamentally different and more manageable risk category.

- Anchor investor dual-commitment structures are emerging as a viable alternative to traditional project finance for junior developers operating in jurisdictions where senior lenders apply conservative risk premiums.

- Oxide-focused development projects with lean capital structures continue to attract capital in environments where gold prices support strong project economics, even in jurisdictions carrying elevated sovereign risk perception.

- Concurrent resource growth strategies signal management confidence in the geological prospectivity of the broader Kobada land package, though investors should monitor the allocation of exploration capital carefully relative to construction contingency reserves.

This article is intended for informational purposes only and does not constitute investment advice. All financial figures, timelines, and projections referenced are drawn from company-disclosed documentation and publicly available sources. Readers are encouraged to conduct independent due diligence before making investment decisions.

Want to Track the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, cutting through complex data to surface actionable opportunities the moment they are announced — explore historic discoveries and their returns to understand what early positioning can mean for a portfolio, then begin your 14-day free trial at Discovery Alert to gain a genuine market-leading edge.