July 24, 2026

India's energy security framework faces unprecedented stress as the India Iran war oil shock threatens to reshape global supply chains and economic stability. The interdependence between Middle Eastern energy exports and Asian consumption patterns has created vulnerabilities that extend far beyond simple price fluctuations. Modern economies built on energy-intensive manufacturing, transportation, and service sectors discover that their resilience depends heavily on supply chain diversity and strategic reserve management.

Energy import dependencies create cascading economic effects through currency markets, fiscal balances, and corporate profitability structures. When major energy corridors face disruption, the transmission mechanisms work through multiple channels simultaneously, affecting everything from household purchasing power to industrial competitiveness. Furthermore, the current oil price rally analysis demonstrates how geopolitical tensions amplify market volatility beyond traditional supply-demand fundamentals.

What Makes India Uniquely Vulnerable to Middle Eastern Energy Disruptions?

The Strategic Energy Dependency Matrix

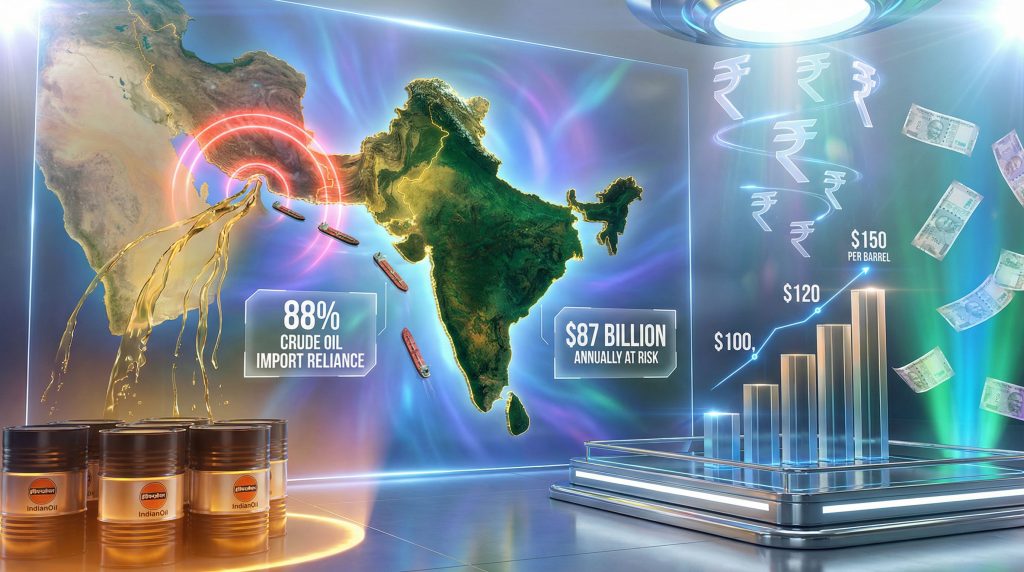

India's position as the world's third-largest oil consumer creates structural vulnerabilities that differentiate it from other major economies. The country derives approximately 90% of its gas from the Middle East, according to recent government assessments, while maintaining limited strategic reserve capacity relative to consumption levels.

The concentration of energy imports through specific geographic corridors amplifies risk exposure beyond simple volume considerations. Moreover, ongoing oil market trade tensions have highlighted the fragility of established supply relationships and pricing mechanisms.

- Critical infrastructure dependence: Gulf refineries supply specialised petroleum products configured for Indian industrial specifications

- LNG terminal capacity constraints: Regasification facilities operate near maximum capacity during peak demand periods

- Remittance flow vulnerabilities: Approximately $87 billion in annual worker transfers from Gulf nations face potential disruption during regional conflicts

- Transportation route concentration: Maritime chokepoints handle disproportionate volumes of India's energy imports

Energy Import Vulnerability Comparison

| Country | Oil Import Dependency | Gas Import Dependency | Strategic Reserve Days |

|---|---|---|---|

| India | 88% | 90% | 11 days |

| China | 72% | 45% | 90 days |

| Japan | 99% | 97% | 240 days |

| South Korea | 95% | 98% | 100 days |

The comparison reveals India's relatively limited strategic petroleum reserve capacity of 5.33 million tonnes, equivalent to approximately 11 days of consumption. This represents significantly lower buffer capacity compared to other major energy-importing economies.

Energy Security Architecture Breakdown

India's energy infrastructure reflects historical development patterns that prioritised cost efficiency over supply diversification. Refinery configurations optimised for Middle Eastern crude specifications create operational challenges when sourcing alternatives during supply disruptions.

LNG Infrastructure Limitations:

- Dahej terminal: 17.5 MMTPA capacity

- Hazira terminal: 14 MMTPA capacity

- Kochi terminal: 5 MMTPA capacity

- Mundra terminal: 5 MMTPA capacity

Total regasification capacity operates near 85% utilisation during peak demand periods, leaving limited flexibility for alternative supply arrangements. LPG import dependency reaching 55% from Gulf sources creates additional pressure points during regional disruptions.

The technical specifications of existing infrastructure limit rapid source switching capabilities. LNG terminals require specific pressure ratings, storage configurations, and pipeline connectivity that match supplier delivery systems. Consequently, alternative sourcing often requires 4-8 week operational adjustment periods for full efficiency restoration.

When big ASX news breaks, our subscribers know first

Could Oil Prices at $120+ Per Barrel Trigger a Balance of Payments Crisis?

Historical Precedent Analysis: 1991 Gulf War Parallels

The 1991 Gulf War crisis provides important precedent for understanding how energy price shocks transmit through India's economic structure. During that period, foreign exchange reserves collapsed from $5.8 billion to approximately $1.2 billion within months, forcing IMF bailout negotiations.

1991 Crisis Timeline:

- January 1991: Oil prices surge above $40/barrel

- March 1991: Current account deficit widens to 3.2% of GDP

- July 1991: Foreign reserves reach crisis threshold of $1.2 billion

- August 1991: Rupee depreciates 20% against major currencies

- September 1991: IMF structural adjustment program implemented

However, India's economic structure in 2026 differs significantly from 1991 conditions. The current account framework operates under full capital convertibility, creating different transmission mechanisms for external shocks. Capital flight dynamics work more rapidly under modern financial integration, but the economy also maintains greater flexibility for adjustment.

Modern Economic Impact Modelling

The Finance Ministry has developed multiple scenario frameworks, including projections where crude oil averages $120 per barrel for the full year. These models incorporate direct import cost increases alongside indirect effects through transportation, manufacturing input costs, and fiscal subsidy requirements.

Oil Price Impact Scenarios:

| Crude Price | Additional Import Cost | GDP Growth Impact | Fiscal Deficit |

|---|---|---|---|

| $100/barrel | $26 billion | -0.3% | 4.3% |

| $120/barrel | $45 billion | -0.6% | 4.8% |

| $150/barrel | $65 billion | -1.0% | 5.2% |

Standard Chartered analysts project fiscal deficit expansion by 0.7 to 0.9 percentage points above the targeted 4.3%, pushing the deficit potentially above 5% of GDP. This projection incorporates higher subsidy expenditures, reduced tax collections from lower economic activity, and increased borrowing costs due to currency pressure.

Growth forecast downgrades have already begun across major institutions. The India Iran war oil shock has prompted government officials to compare the potential disruption to COVID-19 levels:

- Government target: 6.8%-7.2% for fiscal year 2027

- Goldman Sachs: 5.9% for 2026

- Oxford Economics: 6.2% for 2026

The divergence from potential growth rates of 7-7.5% threatens long-term development objectives that require sustained 8% expansion levels.

Why Are Financial Markets Already Pricing in Extended Economic Disruption?

Capital Flight Dynamics

Foreign portfolio investment outflows have accelerated dramatically, with nearly $19 billion withdrawn from local markets in the first quarter of 2026. This represents approximately 70% of the full-year record outflow recorded in 2025, indicating unprecedented capital flight velocity.

The outflow composition reveals broad-based investor concern:

- Equity markets: $12 billion in selling pressure

- Government bonds: $4.5 billion in redemptions

- Corporate debt: $2.5 billion in early exits

Currency markets reflect this pressure through rupee depreciation beyond 95 per dollar, marking an all-time low and triggering Reserve Bank of India intervention protocols. The central bank has implemented its most aggressive currency defense measures in over a decade, including restrictions on speculative derivative positions and enhanced surveillance of external commercial borrowing.

Corporate Sector Stress Indicators

Multiple industries face simultaneous pressure from energy cost inflation and reduced domestic demand. Aviation sector margins compress by 15-25% due to jet fuel cost escalation, while petrochemical companies experience working capital strain affecting operational efficiency.

Sector-Specific Impact Assessment:

- Airlines: Jet fuel comprises 35-40% of operating costs; price increases create immediate margin pressure

- Petrochemicals: Feedstock cost inflation affects 200+ listed companies with Gulf supply dependencies

- Transportation: Diesel price increases transmit through logistics networks, affecting all sectors

- Manufacturing: Energy-intensive industries face input cost inflation of 12-18%

Insurance markets have implemented 40-50% war risk surcharges on Middle East trade routes, creating additional cost pressures for companies dependent on Gulf supply chains. These surcharges reflect underlying expectations of extended disruption periods.

What Emergency Fiscal Measures Could India Deploy?

COVID-Era Policy Toolkit Adaptation

Government officials are developing a credit guarantee scheme worth 2-2.5 trillion rupees ($26.8 billion) targeting small and medium enterprises affected by energy cost inflation and supply chain disruptions. This framework adapts successful pandemic-era interventions that provided 100% guaranteed, collateral-free loans during the 2020 crisis.

Policy Toolkit Components:

- Direct liquidity support: Credit guarantees for working capital requirements

- Fuel subsidy mechanisms: Price stabilisation through strategic petroleum reserve releases

- Export incentive packages: Support for sectors facing Middle East market disruption

- Infrastructure acceleration: Fast-tracking renewable energy projects for import substitution

The government has established a $6.2 billion economic stabilisation fund specifically designed to absorb global shock transmission effects. This fund provides fiscal space for targeted interventions without immediately affecting deficit calculations.

Monetary Policy Coordination Requirements

The Reserve Bank of India faces complex trade-offs between currency defense and inflation targeting objectives. Traditional monetary policy frameworks require adaptation during periods of external supply shocks that create simultaneous currency pressure and inflation acceleration.

RBI Policy Dilemmas:

- Interest rate policy: Raising rates to defend currency versus maintaining growth support

- Liquidity management: Foreign exchange intervention depleting rupee liquidity

- Inflation targeting: Supply-side price increases challenging headline inflation objectives

- Financial stability: Banking sector exposure to energy-intensive corporate borrowers

Recent policy decisions reflect this complexity, with the central bank maintaining rates whilst implementing administrative measures to reduce speculative currency trading. Some analysts suggest rate increases may become necessary if inflation pressures intensify beyond supply-side effects.

How Might Supply Chain Disruptions Cascade Through Key Industries?

Manufacturing Sector Vulnerability Assessment

India's manufacturing ecosystem faces multifaceted supply chain challenges extending beyond direct energy inputs. Fertiliser production depends on 85% raw material imports from Gulf sources, including phosphates and potash essential for agricultural productivity.

Critical Input Dependencies:

- Fertiliser industry: Phosphoric acid, potash, sulphur from Gulf suppliers

- Pharmaceutical sector: 15% of API intermediate chemicals sourced from Iran

- Steel production: Coking coal alternative sourcing from Australia requires 6-8 week shipping lead times

- Textile manufacturing: Petrochemical fibre inputs affecting 40% of production capacity

The pharmaceutical sector faces particular complexity due to specialised chemical intermediate requirements. Iranian suppliers provide specific API compounds that require regulatory approval for alternative sourcing, potentially creating 3-6 month approval delays for substitute suppliers. Additionally, the broader challenges of energy transition challenges compound manufacturing sector vulnerabilities.

Agricultural Input Cost Inflation

Agriculture faces dual pressure from diesel price increases and fertiliser cost inflation. Diesel price transmission affects farming operations through multiple channels:

- Irrigation systems: Electric pump operation and diesel backup systems

- Transportation: Farm-to-market logistics for both inputs and outputs

- Processing facilities: Agricultural product processing and storage

- Mechanisation: Tractor and harvesting equipment operation

Agricultural Cost Impact Estimates:

| Input Category | Cost Increase | Budget Impact |

|---|---|---|

| Diesel fuel | 18-25% | ₹15,000 crore |

| Fertiliser subsidies | 35-40% | ₹50,000 crore |

| Transportation | 12-15% | ₹8,000 crore |

Total agricultural input cost inflation could reach 12-18%, creating food inflation transmission effects throughout the economy. The government's fertiliser subsidy burden may expand by ₹50,000 crore to maintain farmer affordability levels.

What Long-Term Structural Changes Could Emerge?

Energy Transition Acceleration Scenarios

Energy security concerns are accelerating renewable capacity addition targets beyond previously established timelines. Government officials discuss increasing annual renewable installations from 25 GW current pace to 50 GW annually to reduce import vulnerability.

Renewable Energy Acceleration Framework:

- Solar capacity: Targeting 100 GW additional capacity over 3 years

- Wind installations: Offshore wind development in Gujarat and Tamil Nadu

- Green hydrogen: Industrial applications for fertiliser and steel production

- Battery storage: Grid stabilisation and peak demand management

Electric vehicle adoption curves may steepen significantly amid sustained fuel cost concerns. Transportation electrification provides dual benefits of reduced import dependency and improved urban air quality, creating policy alignment for accelerated implementation. Furthermore, recent battery recycling breakthrough technologies could support this transition by reducing raw material dependencies.

Geopolitical Realignment Implications

Energy supply diversification requires developing alternative supplier relationships outside traditional Middle Eastern sources. Russia-India energy partnerships face complexity due to sanctions frameworks, but African crude sourcing presents opportunities for strategic diversification.

Alternative Supply Development:

- African suppliers: Nigeria, Angola, Chad exploration partnerships

- Western Hemisphere: Venezuela, Brazil potential supply agreements

- Domestic production: Coal-to-liquids technology development for emergency scenarios

- Regional cooperation: BRICS energy security initiative expansion

These relationships require multi-year development timelines for infrastructure adaptation, contract negotiation, and regulatory approval processes. Short-term supply substitution remains limited by technical and logistical constraints.

The next major ASX story will hit our subscribers first

Which Sectors Present Investment Opportunities During Crisis?

Defensive Sector Analysis

Certain sectors benefit from accelerated policy support and structural demand changes during energy crises. Renewable energy equipment manufacturers gain from government acceleration of domestic production targets and import substitution incentives.

Investment Theme Opportunities:

- Solar panel manufacturing: Domestic production incentives reducing China dependency

- Wind turbine assembly: Offshore wind expansion creating equipment demand

- Battery technology: Electric vehicle and grid storage applications

- Energy efficiency solutions: Industrial automation and conservation technologies

Domestic oil exploration companies with proven reserves benefit from higher price environments and government incentives for production acceleration. Enhanced oil recovery technologies become economically viable at sustained higher price levels.

Contrarian Investment Themes

Crisis periods create opportunities for strategic investments in sectors facing temporary challenges. Refinery modernisation for crude slate flexibility positions companies for long-term competitive advantage when supply normalisation occurs.

Strategic infrastructure development in alternative energy logistics and distribution networks provides essential foundation for future energy security. These investments require patient capital but offer substantial returns during recovery phases.

Companies developing alternative energy sources and efficiency technologies benefit from both crisis-driven demand and long-term structural transition trends. The convergence of immediate necessity with strategic transformation creates compelling investment dynamics.

How Do Global Precedents Inform India's Crisis Response Strategy?

International Crisis Management Benchmarks

Historical analysis of other major economies' crisis responses provides frameworks for policy optimisation. Japan's 1973 oil shock response emphasised industrial restructuring and efficiency improvements that enhanced long-term competitiveness despite short-term adjustment costs.

Global Crisis Response Patterns:

- Japan 1973: Industrial policy focused on energy efficiency and technology development

- South Korea 1997-98: Fiscal consolidation combined with targeted sector support

- Brazil 2000s: Currency flexibility with inflation targeting frameworks

- European Union 2022: Emergency energy procurement and storage capacity expansion

Each precedent demonstrates the importance of combining immediate crisis management with structural reforms that enhance future resilience. Short-term fiscal support must align with long-term strategic objectives to maximise effectiveness.

Policy Framework Optimisation

Effective crisis response requires coordination between automatic stabiliser mechanisms and discretionary intervention policies. India's framework emphasises targeted support for critical sectors whilst maintaining overall fiscal discipline through strategic reserve utilisation.

Integrated Policy Approach:

- Automatic stabilisers: Tax adjustment mechanisms responding to energy price movements

- Strategic reserves: Petroleum release protocols for price smoothing

- Public-private partnerships: Risk sharing for alternative energy infrastructure development

- Regional cooperation: BRICS energy security coordination for collective bargaining power

The success of these frameworks depends on implementation coordination across federal and state levels, ensuring consistent policy signals for private sector investment decisions. In addition, broader US-China trade impact considerations affect India's strategic positioning in global energy markets.

Modern crisis management emphasises flexibility and rapid adaptation rather than rigid policy frameworks. India's approach combines lessons from historical precedents with innovations adapted to contemporary economic structures and global financial integration patterns. The India Iran war oil shock represents a critical test of these adaptive capabilities, requiring coordinated policy responses across multiple sectors and institutions.

According to Bloomberg analysis, government officials view the current energy crisis as potentially "as disruptive as COVID-19" in terms of economic impact and policy response requirements.

Investment Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Energy market forecasts involve significant uncertainty, and actual outcomes may differ substantially from projections discussed. Investors should conduct independent research and consult qualified financial advisors before making investment decisions.

Are You Seeking Opportunities in Energy Security-Related Investments?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, including critical energy transition commodities that could benefit from heightened demand during global supply disruptions. Discover how major mineral discoveries can generate substantial returns by exploring historical examples of exceptional market outcomes during periods of resource scarcity. Begin your 14-day free trial today to position yourself ahead of market movements in this rapidly evolving energy landscape.