May 21, 2026

When Energy Geography Becomes Economic Destiny

Across recorded economic history, the nations most exposed to resource chokepoints have consistently faced the sharpest recessions when those chokepoints close. Japan's 1973 oil shock, South Korea's industrial paralysis during the 1979 crisis, and the cascading current account collapses across South Asia during the 1990 Gulf War disruption all share a common thread: geography made the damage inevitable, but the depth of structural dependency determined how severe it became.

Today, the India oil crisis as Hormuz remains shut is tracing a disturbingly familiar arc. What separates this episode from past disruptions is not the event itself, but the extraordinary concentration of Indian energy dependency on a single 33-kilometre-wide waterway, and the compounding feedback loops that concentration has now set in motion. Understanding crude oil price dynamics helps contextualise precisely why this particular chokepoint exerts such outsized influence over an economy of 1.4 billion people.

When big ASX news breaks, our subscribers know first

The Architecture of India's Hormuz Exposure

Why 33 Kilometres Controls an Economy of 1.4 Billion People

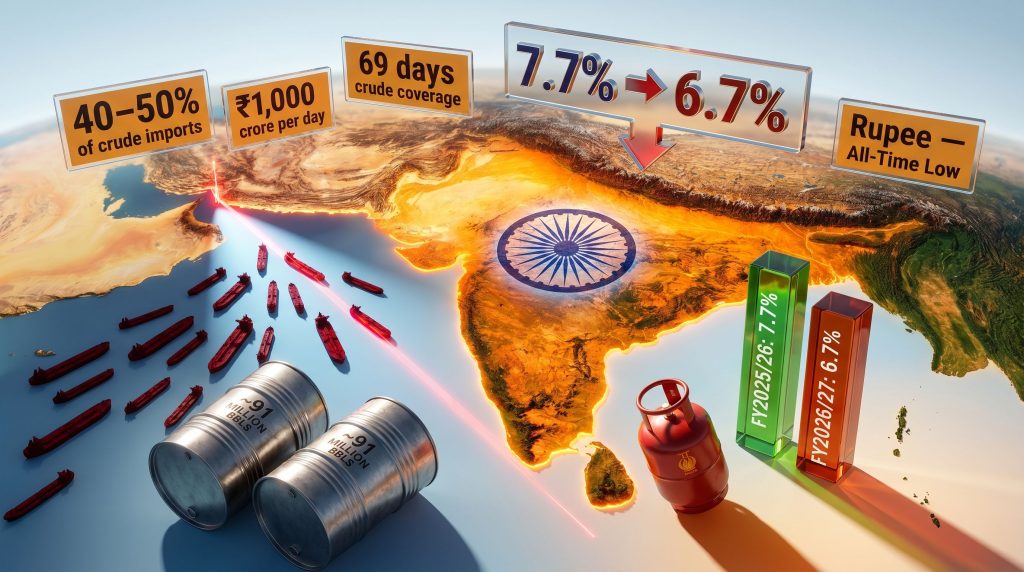

The Strait of Hormuz handles roughly 20% of all globally traded oil on any given day, making it the most consequential energy transit corridor on the planet. For India specifically, the exposure runs far deeper than that headline figure suggests.

Approximately 40 to 50% of India's total crude oil imports have historically transited through the strait, a dependency built across decades of refinery investment, shipping contract structures, and pricing relationships with Gulf producers. LPG exposure is even more concentrated: virtually the entirety of India's liquefied petroleum gas import volumes originate from Persian Gulf suppliers whose only viable export route runs through Hormuz.

Natural gas tells a similar story. Roughly 60% of India's natural gas imports come from the Middle East, with Qatar representing the dominant supplier. This is not coincidental over-concentration. It is the structural outcome of building an energy import system during decades when Persian Gulf supply was cheap, reliable, and geopolitically uncontested.

Structural insight: India's vulnerability is not simply a quantity problem. It is a systems architecture problem. The country's cooking fuel infrastructure, refining slate, and industrial energy contracts were engineered around Gulf supply chains as a foundational assumption, not as an optional preference.

Unlike Japan or South Korea, which developed more diversified LNG sourcing across Pacific Basin suppliers, India's LPG and crude procurement networks were constructed with Persian Gulf terminals as their logical and commercial anchor. That engineering decision, rational at the time, has now become the single greatest source of macroeconomic fragility in Asia. Furthermore, oil's role in the global economy means the repercussions extend well beyond India's own balance sheets.

What the Supply Shock Has Already Consumed

Inventory Drawdown: The Quantified Damage

Two and a half months into the Middle East conflict, India's crude inventory drawdown has consumed a significant portion of its buffer capacity. The scale of that consumption is visible in the following data:

| Metric | Pre-Crisis Level | Current Level | Change |

|---|---|---|---|

| Crude Oil Stockpiles | ~107 million barrels | ~91 million barrels | Down ~15% |

| Crude Supply Coverage | 80+ days | 69 days | Declining |

| LPG Supply Coverage | 60+ days | 45 days | Declining |

| Crude Flows Lost | Baseline | ~40% of normal volumes | Severe disruption |

Indian Oil Minister Hardeep Singh Puri has publicly confirmed that India holds 69 days of crude oil stocks and 45 days of LPG supply, framing the situation as manageable from a supply availability standpoint. However, energy analysts caution that these coverage figures are calculated against current consumption rates, which are themselves beginning to respond to price pressure and conservation directives.

As demand moderates under economic strain, coverage figures can appear more stable than the underlying supply trajectory actually warrants. According to reporting on India's deepening oil crisis, the gap between official reassurances and physical inventory trends is widening in ways that concern independent analysts.

The 15% reduction in crude stockpiles from approximately 107 million barrels to 91 million barrels is the clearest physical signal that import substitution has not yet fully replaced the Hormuz-transiting volumes that went offline. India is drawing down reserves faster than it is rebuilding them through alternative procurement channels.

The Oil Marketing Company Fiscal Mechanism

The most acute near-term financial pressure is being absorbed by India's state-owned oil marketing companies. Because the Indian government has kept retail petrol and diesel prices below the elevated international cost of procurement, OMCs are effectively buying high and selling low at scale. The resulting losses are running at reported levels of up to ₹1,000 crore per day, equivalent to approximately USD $120 million daily flowing out of the sector's balance sheets.

Oil Minister Puri has publicly acknowledged that the energy sector is bearing the primary impact of the disruption, with OMCs sustaining mounting losses to protect consumers from the full force of international price movements. This policy reflects a deliberate social and political calculation, but it carries a structural time limit.

ANZ economist Dhiraj Nim has assessed that retail fuel price increases are a matter of timing rather than possibility, with Q2 2026 identified as the probable window in which the fiscal arithmetic forces the government's hand. Neither the fiscal buffers available to the government nor the balance sheet capacity of the OMCs is sufficient to absorb a prolonged shock at this loss rate indefinitely.

The Currency and Capital Market Deterioration

The rupee has fallen to a new all-time low against the US dollar, driven by the convergence of three simultaneous pressures:

- Surging import costs as crude and LPG procurement prices rise in hard currency terms

- Foreign institutional investor outflows exceeding $20 billion from Indian equities in the first four months of 2026 alone, already surpassing the full-year record set in 2025

- Broader emerging market risk aversion as investors reduce exposure to economies with current account vulnerability during the Iran conflict

The currency deterioration is not simply a financial market inconvenience. It feeds directly back into the oil crisis through a mechanical loop: a weaker rupee increases the local-currency cost of every barrel imported, which widens the OMC loss further, which increases fiscal pressure, which erodes investor sentiment, which weakens the currency further.

This self-reinforcing dynamic is one reason PM Modi's public appeal this month extended beyond fuel conservation to include requests that Indian citizens reduce foreign travel and gold purchases, both significant sources of foreign exchange demand.

How the Shock Moves Through the Broader Economy

Inflation Dynamics and the Lagged Transmission Effect

India's annual inflation rate accelerated in April 2026 relative to March, driven primarily by energy cost pass-through into transportation, logistics, and food supply chains. The April reading came in below analyst projections, but this apparent moderation is misleading. Energy economists consistently observe a 3 to 6 month transmission lag between an initial oil price shock and its full inflationary impact across a complex economy. India is still in the early stages of that transmission curve.

LPG price increases carry particular social sensitivity in India that is qualitatively different from petrol or diesel. The cooking fuel is used by hundreds of millions of households, many of whom access it through subsidised government distribution programmes. Any meaningful LPG price increase functions simultaneously as an energy price event, a food preparation cost event, and a rural household welfare event, creating political constraints on price adjustment that compound the fiscal pressure on OMCs.

GDP Forecast Revisions: The Macroeconomic Scorecard

| Institution | Prior GDP Forecast (FY2025/26) | Revised Forecast (FY2026/27) | Primary Driver |

|---|---|---|---|

| BMI (Fitch Group) | 7.7% | 6.7% | Oil price shock |

| ANZ Bank | Baseline | Downside if fuel hike delayed | Fiscal sustainability risk |

| Reserve Bank of India | Baseline | Monetary intervention flagged | Prolonged Hormuz closure |

The 100 basis point downgrade in India's GDP growth projection, from 7.7% to 6.7%, represents a material deterioration for what had been one of Asia's most consistently high-performing major economies. RBI Governor Sanjay Malhotra has publicly indicated that monetary policy intervention may become necessary if the Hormuz closure extends further, a notable escalation in central bank communication that signals the disruption has crossed the threshold from a sector-specific problem into a macroeconomic policy challenge.

Investor alert: A 100 basis point growth downgrade in an economy of India's size and capital market depth is not a rounding error. It represents a structural repricing of risk across equity, fixed income, and currency asset classes simultaneously.

The Fiscal Trilemma: Three Policy Goals, One Choice

India's policymakers are confronting a classic emerging-market oil shock trilemma with no clean resolution:

- Protect consumers via retail price caps and tax cuts, which erodes OMC balance sheets and government revenue simultaneously

- Protect the currency via reserve intervention and capital flow management, which depletes the foreign exchange buffer needed to pay for increasingly expensive imports

- Protect fiscal sustainability via retail price pass-through, which triggers inflation acceleration and social pressure

All three objectives cannot be fully achieved at the same time. Every policy tool applied to one constraint tightens another. This is the fundamental reason the India oil crisis as Hormuz remains shut is generating such broad-based economic damage rather than remaining contained within the energy sector.

India's Response: Rerouting, Rationing, and Reserves

Import Diversification and Alternative Supply Chains

India has accelerated procurement diversification across three primary alternative supply corridors:

- Russia: Indian refiners had already built substantial purchasing relationships with Russian crude grades following the 2022 sanctions-driven discount environment. Those relationships are now being activated at scale for Hormuz-bypass procurement.

- United States: US crude grades, shipped across Atlantic and Pacific routing, bypass the Strait of Hormuz entirely and have become more commercially attractive as Gulf differentials narrow under disruption conditions.

- West Africa: Nigerian and Angolan grades, loaded at Atlantic Basin terminals, offer complete Hormuz independence. Freight costs are higher due to longer voyage distances, but supply availability is reliable.

India is also exploring direct Gulf oil loading arrangements that could potentially allow some Persian Gulf production to reach Indian refineries through alternative coastal loading or pipeline infrastructure. This is a technically complex and commercially uncertain pathway, but its active exploration reflects the urgency of the supply situation. In addition, the broader trade war impact on oil markets is compressing the range of commercially viable alternatives available to major importers like India.

Strategic Reserve Drawdown and Demand Management

Beyond import rerouting, the government is deploying a demand-side response that operates on two levels. PM Modi's public conservation appeal, covering carpooling, public transport use, and reduced discretionary fuel consumption, represents voluntary demand management. Below that, the industrial-to-household LPG reallocation represents a de facto consumption prioritisation framework that limits industrial supply to protect household cooking fuel availability, a quiet form of rationing operating without formal emergency declaration.

How India Compares to Asia's Other Exposed Economies

Vulnerability Architecture Across Major Asian Importers

| Economy | Crude Hormuz Exposure | LPG/LNG Exposure | Strategic Reserve Coverage | Currency Pressure |

|---|---|---|---|---|

| India | 40-50% of crude imports | Near-total (LPG) | ~69 days crude | Rupee at all-time low |

| Japan | High (Gulf dominant) | High (Qatar LNG) | 90+ days (IEA member) | Yen under pressure |

| South Korea | High | High | 90+ days (IEA member) | Won under pressure |

| China | Moderate (diversified) | Moderate | Large SPR capacity | Managed exchange rate |

Japan and South Korea benefit from IEA membership, which provides access to coordinated strategic reserve release mechanisms unavailable to India in the same institutional form. China's combination of a larger and more diversified SPR, managed exchange rate regime, and broader supply diversification provides greater short-term insulation, though China's absolute import volumes remain enormous.

India's particular combination of high Hormuz exposure, relatively limited SPR depth, and a freely floating currency creates an asymmetric vulnerability profile that no other major Asian importer fully replicates. However, any sustained oil price rally driven by prolonged disruption would amplify these pressures across all regional importers simultaneously.

The next major ASX story will hit our subscribers first

Scenario Pathways: Where the Economics Lead from Here

Three Scenarios for India's Economic Trajectory

Scenario A: Resolution Within 30-60 Days

OMC losses remain manageable through existing fiscal and balance sheet buffers. The rupee stabilises as oil import pressure eases. GDP growth settles near the 6.7% revised forecast. Any retail fuel price adjustment is modest and politically contained.

Scenario B: Disruption Extends 3-6 Months

Retail fuel prices rise during Q2 2026 as OMC losses exceed sustainable thresholds. Inflation accelerates meaningfully beyond April's pace as the full transmission lag works through the economy. The RBI implements monetary tightening to defend the rupee and anchor inflation expectations. GDP growth faces further downward revision toward 6.0 to 6.3%, and foreign capital outflows continue as emerging market risk aversion persists.

Scenario C: Prolonged Closure Beyond 6 Months

Refinery run cuts become necessary as crude procurement volumes fall below minimum operational thresholds. Domestic fuel availability tightens, requiring formal rationing frameworks rather than voluntary conservation measures. Structural current account deterioration forces more aggressive reserve intervention. India's growth premium over other emerging markets narrows substantially, triggering potential sovereign rating watch actions from major credit agencies. Furthermore, OPEC's market influence over non-Gulf supply sources becomes increasingly critical as a pricing and allocation factor under this extended scenario.

Disclaimer: The scenario projections above represent analytical frameworks for understanding possible economic trajectories and do not constitute financial advice or investment recommendations. Actual outcomes will depend on the geopolitical resolution timeline, global energy market dynamics, and Indian government policy responses, all of which carry significant uncertainty.

Frequently Asked Questions: India Oil Crisis and the Hormuz Shutdown

What percentage of India's oil imports pass through the Strait of Hormuz?

Approximately 40 to 50% of India's crude oil imports historically transited the Strait of Hormuz, with LPG exposure even higher. Virtually all of India's LPG imports originate from Middle Eastern suppliers that depend on Hormuz for export routing.

How many days of oil supply does India currently have in reserve?

As of mid-May 2026, Indian authorities have confirmed approximately 69 days of crude oil stocks and 45 days of LPG supply, figures that are declining as import volumes remain disrupted. Reporting from the Times of India confirms that stocks are down approximately 15% since the conflict began, underlining the pace of drawdown.

Why are Indian oil marketing companies losing money during the crisis?

The government has kept retail petrol and diesel prices below global market levels to protect consumers, while OMCs are purchasing crude and gas at elevated international prices. This gap between procurement cost and retail selling price is generating reported losses of up to ₹1,000 crore, approximately USD $120 million, per day across the sector.

Will India raise fuel prices because of the Hormuz crisis?

Analysts and the Reserve Bank of India Governor have both indicated that retail fuel price increases are likely if the Middle East disruption persists, with Q2 2026 identified as the probable adjustment window.

How has the crisis affected the Indian rupee?

The rupee has fallen to a new all-time low against the US dollar, driven by higher oil import costs, foreign investor outflows exceeding $20 billion in the first four months of 2026, and broader emerging market risk aversion.

What is India's GDP growth forecast for fiscal 2026/2027?

BMI, part of the Fitch Group, has revised India's GDP growth forecast down to 6.7% for fiscal year 2026/2027, compared to 7.7% recorded in 2025/2026, attributing the slowdown primarily to the oil price shock stemming from the India oil crisis as Hormuz remains shut and the broader disruption to Gulf supply chains.

Want To Spot The Next Major ASX Mineral Discovery Before The Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into clear, actionable insights for investors at every experience level — explore the historic returns major discoveries have generated and begin your 14-day free trial today to secure a genuine market-leading edge.