July 17, 2026

India's Aluminium Tariff Architecture: Who Pays the Price?

Protective tariffs in commodity-intensive industries rarely hurt only the industries they target. History shows repeatedly that when raw material imports face elevated duties, the cost burden migrates downstream, absorbed by manufacturers, infrastructure budgets, and ultimately consumers. The debate surrounding India primary aluminium import duty reduction is a precise illustration of this dynamic, and the pressure to revise it is now reaching a critical threshold.

Understanding the full complexity of this debate requires separating two frequently conflated policy instruments, recognising the opposing economic interests at stake, and appreciating why a seemingly straightforward duty reduction is anything but simple to execute.

When big ASX news breaks, our subscribers know first

How India's Primary Aluminium Import Duty Actually Works

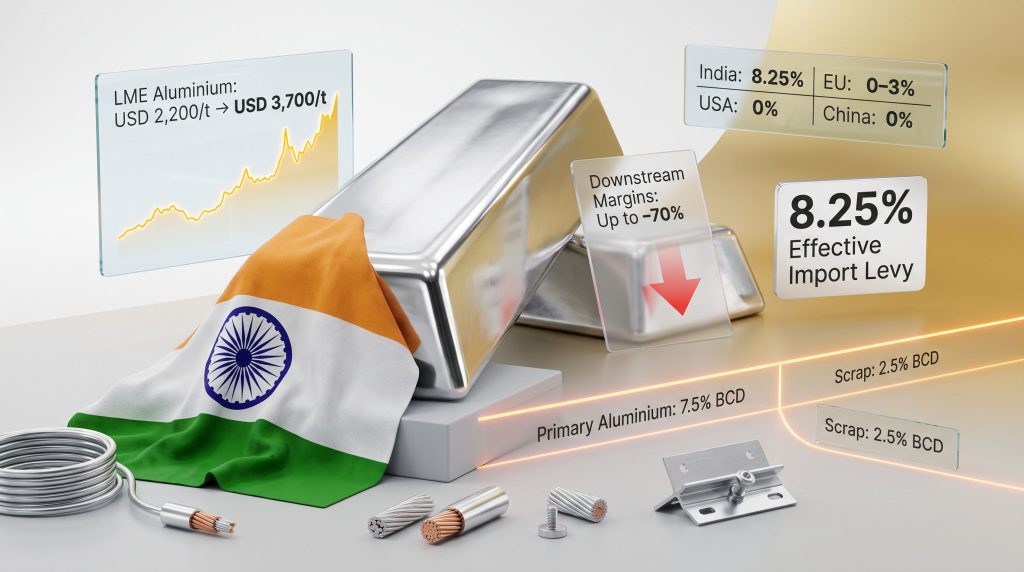

The effective levy on primary aluminium imports into India is not a single charge but a layered structure. The basic customs duty (BCD) stands at 7.5%, applied to unwrought primary aluminium entering the country. On top of this, a Social Welfare Surcharge of 0.75% is applied, bringing the combined effective burden to 8.25%.

This places India significantly above the tariff norms seen across most major economies. Furthermore, understanding the import tax structure in India reveals just how layered these arrangements can become across commodity categories. For context:

| Country / Region | Primary Aluminium Import Duty |

|---|---|

| India | 7.5% BCD (8.25% effective) |

| European Union | 0–3% (varies by product form) |

| United States | 0% (MFN rate for unwrought aluminium) |

| China | 0% (primary aluminium imports) |

| ASEAN (FTA partners) | 0–5% (varies by agreement) |

Source: WTO Tariff Profiles / World Customs Organization

A separate and often confused policy track involves aluminium scrap, which carries a lower 2.5% BCD. Notably, aluminium scrap is currently the only non-ferrous metal scrap category still subject to any import duty in India. Copper, zinc, and lead scrap all enter duty-free. The Mines Ministry has formally recommended removing the scrap duty entirely, with that recommendation progressing toward the Finance Ministry.

This is a distinct process from the primary aluminium debate, with different beneficiaries, different timelines, and a far less contentious political landscape.

The scrap duty removal and the primary aluminium duty debate are entirely separate instruments with different industry coalitions and diverging government positions. Conflating them leads to misreading the policy signals.

The Mechanism Behind Import-Parity Pricing

To understand why downstream manufacturers are distressed, it is essential to understand how import-parity pricing functions in practice.

When a protective tariff is in place on imports of a commodity, domestic producers of that same commodity gain the ability to price their output at or near the landed cost of equivalent imports, including the duty component. Since buyers cannot realistically access cheaper foreign supply without incurring the 8.25% effective levy, they lose their pricing leverage entirely.

The consequence is structural: downstream manufacturers pay elevated input costs that track the tariff-inflated import price, regardless of actual domestic production costs. The Ministry of Mines' own Aluminium Vision Document quantified this effect, estimating that import-parity pricing caused India's downstream manufacturers to collectively pay approximately USD 470 million more to domestic primary producers in 2022 alone compared to what they would have paid under a more open tariff regime.

This is not an India-specific phenomenon. Import-parity pricing is a well-documented consequence of protective tariff structures in commodity-intensive industries globally, and it consistently transfers value from mid-chain manufacturers to upstream producers while suppressing investment in value-added processing. Consequently, aluminium tariff impacts of this kind are being scrutinised in multiple major economies simultaneously.

Who Absorbs the Cost?

The economic burden is distributed unevenly across the downstream ecosystem:

- Cable and conductor manufacturers face direct input cost exposure, with pricing implications that flow through to transmission infrastructure contracts

- Utensil and cookware producers, predominantly MSMEs, operate with minimal pricing power and cannot pass cost increases downstream

- Renewable energy supply chains face higher costs for aluminium-intensive solar mounting systems and associated hardware

- Government infrastructure budgets across power transmission, railways, metro networks, and defence procurement absorb inflated aluminium input pricing through elevated contract costs

The Downstream Industry's Formal Case for Reduction

In July 2026, two major downstream industry associations, the Federation of All India Aluminium Utensils Manufacturers (FAIAUM) and the Cable and Conductor Manufacturers Association of India (CACMAI), submitted a joint representation to India's Ministry of Mines calling for immediate rationalisation of the 8.25% effective import levy on primary aluminium.

Their case rests on several reinforcing arguments:

- Margin compression of up to 70% has been reported across downstream segments including cables, conductors, utensils, and value-added aluminium products

- Global LME aluminium prices surged from approximately USD 2,200 per tonne in 2023 to over USD 3,700 per tonne, representing a rise of roughly 68%, driven by Middle East geopolitical tensions, logistics disruptions, elevated freight rates, and energy market volatility

- Input costs increased by an estimated 20–35% over just a three-month window, outpacing the adjustment capacity of most MSMEs

- Finished aluminium product imports reached USD 4.1 billion in FY2025-26, with approximately one-quarter entering under Free Trade Agreements at zero or near-zero duty

That final point exposes a structural paradox at the heart of India's current tariff architecture. Foreign competitors exporting finished aluminium goods into India face minimal or no import barriers under FTAs, while Indian manufacturers importing the raw primary aluminium they need to produce those same goods face an 8.25% effective levy. The policy inadvertently advantages the finished import over the domestically manufactured equivalent.

CACMAI President Sanjay Saboo argued publicly that because India's transmission infrastructure sector is predominantly funded through public investment, the cost inflation caused by the duty-linked pricing mechanism flows directly into government expenditure, meaning taxpayers bear the financial consequence of higher-priced cables and conductors across the country's power grid expansion.

The Upstream Counterargument: Why Producers Resist

The domestic primary aluminium industry, represented through bodies including the Aluminium Association of India (AAI), presents an equally substantive counter-position. However, their arguments should not be dismissed. Reviewing the landscape of top aluminium companies operating globally makes clear why upstream producers guard tariff protection so carefully:

- The 7.5% BCD provides essential protection for India's capital-intensive smelting capacity against lower-cost global producers, particularly those benefiting from subsidised energy or state support

- Some producer-aligned voices have advocated for raising duties to 10–15%, arguing that current margins are already under pressure from global price volatility

- Weakening import protection risks deterring future smelter investment at a time when India is actively seeking to expand domestic primary production capacity as part of its broader industrial strategy

This creates a genuine policy dilemma. Upstream smelters require long-term price certainty to justify the capital expenditure required for new capacity. A reduction in tariff protection, even a partial one, introduces uncertainty into investment models that typically span decades.

MSME Vulnerability: A Structural Breakdown

The risk profile for downstream MSMEs operating under the current tariff regime is well-documented:

| Risk Factor | Impact on Downstream MSMEs |

|---|---|

| Margin compression | Up to 70% reduction in operating margins reported |

| Input cost escalation | 20–35% increase over three months |

| Capital expenditure | Curtailed investment in technology and pollution controls |

| Workforce risk | Increased probability of layoffs and unit closures |

| Export competitiveness | Weakened by higher domestic input costs vs. global peers |

The combined effect of these pressures is not merely financial. Reduced reinvestment capacity limits technology upgrades and environmental compliance, weakening the long-term competitiveness of India's downstream aluminium manufacturing base. This is particularly concerning given that raw materials and green transition demands are accelerating global appetite for aluminium-intensive products.

The next major ASX story will hit our subscribers first

The Public Finance Dimension: Infrastructure Cost Inflation

A June 2026 report by the Global Trade Research Initiative (GTRI) added a public finance lens to the debate. The research estimated that import-parity pricing inflates the cost of aluminium-intensive public infrastructure projects by approximately 3%, affecting sectors including power transmission networks, railways, metro systems, renewable energy installations, and defence procurement.

Given the scale of India's planned infrastructure investment, a 3% cost premium on aluminium-intensive projects represents a meaningful and recurring drain on public budgets. This framing reorients the debate from a narrow industrial policy question to a broader fiscal efficiency concern.

A tariff designed to protect one upstream sector may be quietly inflating the cost of national infrastructure at a scale that warrants serious quantification by the Finance Ministry.

The FTA Paradox and Its Strategic Implications

The structural anomaly created by India's FTA trade relationships deserves particular attention. With USD 4.1 billion in finished aluminium products imported in FY2025-26 and roughly 25% entering at zero or minimal duty under FTA arrangements, the tariff architecture effectively creates a two-tier competitive environment.

Foreign manufacturers, sourcing primary aluminium in global markets without the 8.25% levy, can export finished goods into India with little friction. In addition, Indian manufacturers sourcing the same raw material domestically under import-parity pricing conditions face structurally higher input costs and cannot compete on equivalent terms.

This dynamic runs counter to the objectives of initiatives like Make in India and the Production Linked Incentive (PLI) framework, both of which aim to build domestic value-added manufacturing capacity. Moreover, broader issues around tariffs and supply chains globally demonstrate that poorly calibrated protective duties often undermine the manufacturing ambitions they are designed to support.

Where the Government Currently Stands

| Policy Area | Current Duty | Proposed Change | Government Status |

|---|---|---|---|

| Primary aluminium (unwrought) | 7.5% BCD (8.25% effective) | Downstream bodies advocate reduction to 0% | No confirmed action |

| Aluminium scrap | 2.5% BCD | Mines Ministry recommends full removal | Recommendation advancing to Finance Ministry |

The government's more advanced movement on scrap duty reflects a less contested political landscape. Scrap duty removal aligns with circular economy objectives and does not directly threaten upstream smelter economics. Any revision to the India primary aluminium import duty reduction debate, by contrast, requires navigating significant opposition from a well-capitalised and politically connected upstream industry. For a detailed breakdown of how these tariff impacts on aluminium are being assessed heading into 2026, further analysis is available from industry researchers tracking these developments closely.

What a Duty Reduction Would and Would Not Achieve

Potential Benefits

- Lower input costs for cable, conductor, utensil, and construction product manufacturers

- Improved MSME viability, reducing closure risk and supporting employment across manufacturing clusters

- More competitive export pricing for aluminium-intensive finished goods in international markets

- Reduced public infrastructure costs, particularly across power transmission and renewable energy supply chains

- Structural alignment with FTA logic, removing the paradox where finished imports face lower barriers than raw material inputs

Potential Risks

- Reduced price protection for domestic smelters, potentially compressing upstream margins during periods of global price weakness

- Possible deterrent effect on long-term upstream investment in new smelting capacity

- Increased strategic dependence on imported primary aluminium, creating supply chain exposure during periods of global disruption

Analysts at CUTS International have further examined how tariff rationalisation in the aluminium ecosystem could support MSME growth, offering an independent policy perspective that complements the industry submissions currently before the Ministry.

Frequently Asked Questions

Has India reduced its primary aluminium import duty?

As of mid-2026, the basic customs duty on primary aluminium remains at 7.5%, with an effective levy of 8.25% including the Social Welfare Surcharge. No reduction has been confirmed.

What is import-parity pricing and why does it matter?

Import-parity pricing occurs when domestic producers price their output at the landed cost of equivalent imports, inclusive of the duty margin. It eliminates buyers' ability to use cheaper imports as a negotiating tool, effectively locking in elevated input costs for downstream manufacturers.

Who is lobbying for a duty reduction?

FAIAUM and CACMAI submitted a formal joint representation to the Ministry of Mines in July 2026, calling for immediate rationalisation of the 8.25% effective levy. The India primary aluminium import duty reduction question is now squarely on the policy agenda.

Who opposes it?

Domestic primary aluminium producers and representative bodies including the Aluminium Association of India oppose any reduction, citing the need to protect smelting capacity and support upstream capital investment.

How does this affect government budgets?

GTRI estimates that import-parity pricing inflates aluminium-intensive public infrastructure costs by approximately 3%, translating into higher expenditure on power transmission, railways, metro systems, and defence procurement funded by taxpayers.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or policy advice. Forecasts, estimates, and projections referenced herein are derived from third-party research and industry submissions and should not be relied upon as definitive outcomes. Readers should conduct independent research before making investment or business decisions.

Want to Track the ASX Mineral Discoveries Shaping the Commodities Landscape?

As aluminium tariff debates reshape global supply chains and commodity markets, Discovery Alert's proprietary Discovery IQ model instantly identifies significant ASX mineral discoveries — including those in aluminium and other key industrial metals — translating complex data into clear, actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their extraordinary returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial to position yourself ahead of the next major market-moving announcement.