June 12, 2026

The Value Chain Trap: Why Having Rare Earth Reserves Means Nothing Without Processing Power

For decades, the conventional assumption in critical minerals policy was straightforward: a country with large reserves holds strategic leverage. Reality has proven far more complicated. Across the rare earth supply chain, the decisive power sits not in the ground but in the refinery, the separation plant, and the magnet manufacturing facility. Nations that mastered downstream processing captured the economic and geopolitical value. Those that did not remained dependent, regardless of how much ore lay beneath their soil.

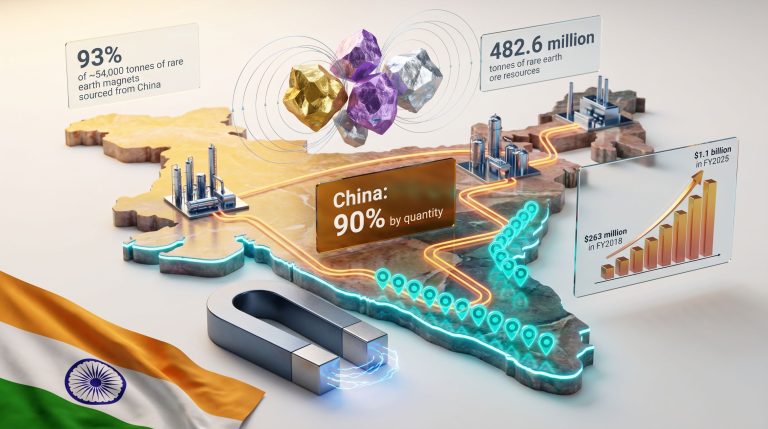

India represents the clearest example of this structural paradox. According to the Geological Survey of India, the country holds approximately 482.6 million tonnes of rare earth ore resources, placing it among the most endowed nations on earth. Yet India remains heavily reliant on imported processed rare earth materials, a dependency that flows almost entirely toward China. The gap between geological wealth and industrial capability has cost India billions in foregone value and left its clean energy manufacturing ambitions exposed to supply chain risk.

That equation is now being challenged, and the most concentrated effort to reverse it is taking shape along the coastline of Andhra Pradesh.

When big ASX news breaks, our subscribers know first

India Rare Earth Processing in Andhra Pradesh: Why the Eastern Coast Holds the Key

The decision to anchor India's rare earth processing ambitions in Andhra Pradesh is not arbitrary. The state's coastal geology produces some of the richest concentrations of heavy mineral beach sands found anywhere in South Asia, and the scale of the identified resource base is substantial.

Mapping the Mineral Resource Base

Andhra Pradesh hosts 211 million metric tonnes of beach sand mineral resources distributed across 16 identified coastal deposit zones covering 16,604 hectares. These deposits span eight districts along the state's eastern shoreline: Srikakulam, Vizianagaram, Visakhapatnam, Anakapalli, Konaseema, Kakinada, West Godavari, and Krishna.

Beach sand mineral deposits are mineralogically distinct from hard rock rare earth occurrences. They typically contain assemblages of heavy minerals including ilmenite, rutile, zircon, garnet, and critically, monazite. It is the monazite fraction that carries the rare earth payload: a phosphate mineral containing varying concentrations of cerium, lanthanum, praseodymium, neodymium, and in some deposit types, heavier rare earths including dysprosium and terbium.

The heavy mineral assemblage in beach sand deposits is the product of millions of years of coastal erosion, fluvial transport, and wave sorting. What makes India's eastern coastal placer deposits particularly valuable is the co-occurrence of multiple commercially significant mineral species within the same ore body, enabling a multi-product processing model where rare earths, titanium minerals, and zircon can all be recovered simultaneously from a single feed stream.

Andhra Pradesh accounts for approximately 30% of India's total monazite reserves, equivalent to roughly 3.8 million tonnes. This concentration of monazite within a geographically compact coastal zone creates the foundation for industrial-scale rare earth processing that would be difficult to replicate in most other Indian states. Furthermore, Andhra Pradesh's strategic push into beach sand minerals has been well documented, with state authorities actively working to unlock the full value of these coastal resources.

The Thorium Complication: A Regulatory Constraint That Shapes Everything

Monazite's value as a rare earth carrier comes bundled with a significant regulatory complication. The mineral contains thorium, a naturally occurring radioactive element, at concentrations that typically range between 4% and 12% by weight depending on deposit characteristics. This thorium content places monazite directly under the jurisdiction of India's Atomic Energy Act, which classifies it as a prescribed substance and restricts its processing and handling to entities authorised under atomic energy legislation.

In practice, this has meant that IREL (India) Limited, the state-controlled entity operating under the Department of Atomic Energy, has historically dominated India's monazite-linked rare earth extraction. Private sector companies have been effectively excluded from the most thorium-rich rare earth streams, not because of commercial barriers but because of statutory ones.

This regulatory architecture creates a genuine structural constraint for any private investment in Andhra Pradesh's rare earth corridor. Companies looking to process monazite-derived rare earth concentrates face one of two paths:

- Pursuing regulatory carve-outs or public-private partnership structures that allow processing activities to proceed under IREL oversight

- Developing processing models that physically separate rare earth streams from thorium-bearing fractions at an early stage, potentially reducing the regulatory burden on downstream operations

Neither pathway is straightforward. The first requires policy reform at the central government level. The second demands processing technology capable of achieving thorium separation at commercially viable costs, which remains technically challenging at industrial scale. These difficulties reflect the broader rare earth processing challenges that nations worldwide continue to grapple with.

The Three-Cluster Architecture: Andhra Pradesh's Industrial Blueprint

The Andhra Pradesh government's rare earth corridor strategy is built around geographic concentration, co-locating processing stages within designated industrial zones to compress development timelines and reduce infrastructure duplication.

Cluster Locations and Functional Roles

| Cluster Name | Location | Primary Focus |

|---|---|---|

| Titanium Park | Srikakulam | Titanium mineral separation and processing |

| Rare Earth Corridor | Anakapalli | Rare earth refining and downstream manufacturing |

| Integrated Titanium and Rare Earth Park | Machilipatnam | Combined value chain from mining through end products |

The Machilipatnam cluster is conceptually the most ambitious of the three, attempting to house the complete rare earth value chain within a single industrial zone. The logic is compelling: by eliminating the logistics costs and handling losses involved in shipping intermediate products between processing stages, an integrated facility can potentially compete with Chinese processors on unit economics even while operating at smaller initial volumes.

Investment Targets and Incentive Architecture

The state has set a target of attracting more than ₹50,000 crore (approximately $6 billion USD) in combined rare earth and titanium investments over the next decade. To convert expressions of interest into binding commitments, the corridor policy framework incorporates capital-linked incentive structures, with enhanced benefits reserved for projects committing ₹10 billion or more in capital expenditure.

The tender issuance process is contingent on cabinet approval of the formal rare earth corridor policy, which according to sources familiar with the matter was anticipated within approximately one month of the June 2026 reporting period. This approval milestone is the critical gateway event: until the policy framework is formally adopted, companies expressing interest cannot convert that interest into enforceable licence or concession arrangements.

Andhra Pradesh's broader investment attraction record provides some credibility to these targets. The state has previously secured commitments from globally recognised names including Google and ArcelorMittal Nippon Steel, and has articulated a state-wide investment target of $1 trillion in commitments by 2029.

Which Industrial Groups Are Competing for the Corridor Opportunity?

Approximately 10 companies have formally expressed interest in establishing rare earth processing facilities in Andhra Pradesh. Three of the highest-profile names carry significant strategic logic for their involvement:

- Reliance Industries brings downstream manufacturing scale and a growing energy transition portfolio, with capital deployment capacity that few Indian private sector entities can match. Its interest signals a recognition that rare earth processing is becoming an integral input to India's emerging clean technology manufacturing sector.

- Vedanta contributes existing base metals and mining operational infrastructure. The company's experience managing complex metallurgical processes at scale provides a credible foundation for rare earth separation and refining activities, which demand similar chemical engineering capabilities.

- Adani Enterprises holds a particularly interesting strategic fit through its logistics, port infrastructure, and energy assets. Rare earth processing corridors require reliable power, efficient bulk materials handling, and access to export infrastructure, all areas where Adani's existing asset base creates potential cost advantages.

The involvement of these three diversified conglomerates is strategically significant beyond their individual capabilities. When companies of this scale express processing interest rather than simply mining interest, it signals a genuine shift in the investment thesis toward integrated value capture rather than ore extraction. This distinction matters enormously for the long-term economics of India's rare earth ambitions.

Understanding the Full Rare Earth Value Chain

One of the most commonly misunderstood aspects of rare earth economics is the scale of value addition that occurs at each processing stage. The difference in unit value between raw ore, separated mineral concentrates, refined oxides, metals, and finished magnets is not incremental but exponential.

From Beach Sand to Permanent Magnet: The Five Processing Stages

- Mining and mineral separation extracts heavy mineral concentrates from beach sand through physical gravity and magnetic separation techniques. The rare earth-bearing monazite fraction is isolated at this stage.

- Rare earth oxide production involves chemical digestion of the monazite concentrate, separation of individual rare earth elements through solvent extraction circuits, and precipitation of individual rare earth oxides to specified purity grades. This stage is technically the most demanding and represents the core processing bottleneck that India currently lacks at industrial scale.

- Metal and alloy manufacturing converts rare earth oxides into usable metal forms through electrochemical reduction processes. Neodymium metal production for magnet applications is a primary output target.

- Magnet manufacturing combines neodymium, iron, and boron in precise proportions under controlled atmospheric conditions to produce neodymium-iron-boron (NdFeB) permanent magnets, the workhorse component of EV traction motors and wind turbine generators.

- End-use integration delivers finished magnets to motor manufacturers, wind turbine producers, defence electronics firms, and other high-value end users.

India's historical participation in this chain has been confined largely to stages one and occasionally two, with the vast majority of value addition occurring offshore, predominantly in China. However, critical minerals demand driven by the global energy transition is now creating powerful incentives for India to move decisively up this value chain.

How India's Rare Earth Position Compares Globally

India's challenge around India rare earth processing in Andhra Pradesh is shared, to varying degrees, by every nation attempting to reduce dependence on Chinese refining capacity. However, the specific character of each country's constraints differs meaningfully.

| Country | Strategy | Key Advantage | Key Challenge |

|---|---|---|---|

| India (Andhra Pradesh) | Integrated coastal processing corridors | Large domestic reserves; growing EV demand | Thorium regulations; processing technology gaps |

| Australia | Mine-to-refinery vertical integration | World-class deposits; Western alliance alignment | High processing costs; limited domestic demand |

| United States | Loan guarantees and defence procurement mandates | Strong policy support; existing magnet demand | Decades-long processing capability gap |

| Canada | Critical minerals strategy with allied offtake | Stable regulatory environment | Limited refining infrastructure |

India's structural differentiator in this comparison is its domestic demand story. Unlike Australia, which must export essentially all of its rare earth production, or Canada, which faces a limited home market, India has a rapidly growing internal demand base for rare earth-dependent products. The country's EV manufacturing sector is scaling, its defence sector is expanding its rare earth-dependent technology requirements, and its renewable energy build-out is accelerating demand for permanent magnet generators.

This domestic demand foundation means Indian rare earth processors could in principle serve home market needs before competing for export volumes, reducing the commercial risk profile of early-stage projects.

The next major ASX story will hit our subscribers first

The Federal Policy Framework Supporting State-Level Action

Andhra Pradesh's corridor strategy operates within a broader national policy architecture. The state was among four states designated in India's February federal budget for rare earth corridor development, a framework that encompasses mining rights, processing licences, and magnet manufacturing incentives across integrated zones.

The central government has also committed ₹73 billion through a programme approved in November to support rare earth permanent magnet manufacturing, creating the financial scaffolding within which state-level investment attraction operates. It is important to note that this programme establishes a general support framework for rare earth magnet manufacturing nationally, and individual projects within Andhra Pradesh would need to meet the programme's specific eligibility criteria to access these funds. In addition, the emerging critical minerals coalition among allied nations is providing further diplomatic and financial momentum behind these domestic initiatives.

Key Risks That Investors and Observers Should Monitor

Regulatory and Legal Constraints

- The Atomic Energy Act's jurisdiction over thorium-bearing minerals remains the single largest structural barrier to private sector participation at full processing scale

- Environmental clearance requirements for coastal industrial development in ecologically sensitive zones could extend approval timelines significantly

- Land acquisition and community consent processes in coastal areas with established fishing and agricultural communities carry social licence risks

Technical and Commercial Challenges

- India currently lacks commercially proven rare earth separation and refining technology at industrial scale, meaning new processing facilities would need to either licence foreign technology or develop proprietary processes

- The capital intensity of rare earth processing infrastructure, combined with long lead times before meaningful revenue generation, creates financing challenges that incentive structures alone may not fully resolve

- Established Chinese processors, benefiting from decades of accumulated process optimisation and scale economics, can potentially undercut new entrant pricing during the critical ramp-up phase

Geopolitical Variables

The pace and urgency of India's domestic capacity building is sensitive to the trajectory of India-China diplomatic and trade relations. A sustained deterioration in bilateral relations accelerates the strategic imperative for domestic processing capacity. Consequently, China's rare earth strategy continues to loom large over the decisions of every nation seeking to build independent processing infrastructure.

Quad-aligned nations including Australia, Japan, and the United States have demonstrated increasing interest in co-investing in or establishing offtake agreements with non-Chinese rare earth processing capacity, and Indian projects that achieve technical credibility could become attractive partnership targets. European and American EV manufacturers operating under tightening supply chain diversification mandates represent a potential demand catalyst for Indian rare earth processing output that extends well beyond the domestic market.

Frequently Asked Questions: India Rare Earth Processing in Andhra Pradesh

What rare earth minerals are found in Andhra Pradesh?

Andhra Pradesh's coastal beach sand deposits contain a range of heavy minerals including monazite, which carries rare earth elements such as lanthanum, cerium, praseodymium, and neodymium. Co-occurring minerals include ilmenite, rutile, zircon, and garnet. The state holds an estimated 30% of India's total monazite reserves, or roughly 3.8 million tonnes.

How much investment is Andhra Pradesh targeting in rare earth development?

The state is targeting more than ₹50,000 crore (approximately $6 billion USD) in combined rare earth and titanium investments over the next decade, supported by capital-linked incentive structures for projects committing ₹10 billion or more.

Why has India struggled to develop its rare earth processing capacity despite large reserves?

The primary constraints are regulatory (thorium content in monazite placing it under the Atomic Energy Act), technological (absence of industrial-scale separation and refining infrastructure), and structural (historical concentration of processing rights within state-controlled entities like IREL).

What is the Andhra Pradesh rare earth corridor?

A planned integrated industrial zone covering the full value chain from mining and mineral separation through refined oxide production, metal manufacturing, and permanent magnet output, organised across three specific cluster locations at Srikakulam, Anakapalli, and Machilipatnam.

Are rare earth elements essential for electric vehicles?

Rare earth permanent magnets, particularly those containing neodymium and dysprosium, are critical components in the traction motors used in battery electric vehicles. As India's EV manufacturing sector scales, India rare earth processing in Andhra Pradesh becomes an increasingly important strategic input to sustaining that growth.

The Larger Stakes: From Passive Reserve Holder to Active Processing Nation

If Andhra Pradesh's rare earth corridor achieves even a fraction of its stated ambitions, the implications extend well beyond state-level economics. India capturing 20 to 30% of its current rare earth processing needs domestically would represent a meaningful reduction in a structural import dependency that currently leaves the country's clean energy and defence manufacturing sectors exposed to supply chain disruption.

The employment and industrial development multiplier effects of establishing processing clusters in coastal Andhra Pradesh would be substantial. Rare earth processing facilities are capital-intensive but generate significant indirect employment across logistics, chemicals supply, engineering services, and downstream manufacturing. The Machilipatnam integrated cluster model, if realised, could anchor an entire industrial ecosystem rather than a single facility.

More broadly, successful execution of the Andhra Pradesh corridor model would position India as a credible alternative supplier within the global rare earth processing hierarchy, at precisely the moment when Western EV manufacturers, defence procurement agencies, and renewable energy developers are actively seeking to reduce their exposure to single-source Chinese supply chains.

The geological assets are already in place. The policy architecture is taking shape. The industrial interest is demonstrably real. What remains to be resolved is whether India's regulatory framework, financing structures, and processing technology capabilities can be assembled quickly enough to capitalise on a window of strategic opportunity that may not stay open indefinitely.

Readers seeking additional context on India's critical minerals strategy and the global rare earth supply chain landscape may find value in related reporting published by ET EnergyWorld, which covers ongoing developments in India's energy and industrial minerals sectors.

Want to Identify the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly translating complex mineral data across more than 30 commodities into clear, actionable investment insights — giving subscribers a decisive edge in fast-moving critical minerals markets like rare earths. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the next significant find.