June 12, 2026

The Governance Shift That Signals a New Chapter in Western Rare Earth Supply Chain Building

Rare earth supply chains have become one of the defining industrial battlegrounds of the 21st century. Decades of underinvestment in Western processing capacity, combined with China's deliberate consolidation of mining and downstream refining operations, have created a structural vulnerability that is now commanding serious capital and policy attention. Against this backdrop, the boardroom changes occurring at USA Rare Earth are not incidental governance housekeeping. They reflect the maturation of a company transitioning from an optionality play into a multi-jurisdictional, vertically integrated industrial enterprise.

When Mordechai Gutnick exits USA Rare Earth board, the event carries layers of meaning that extend well beyond a single directorship change. Understanding those layers requires examining the company's asset base, the family legacy behind its founding, and the financial instruments now being used to manage a stake worth more than a third of a billion dollars.

When big ASX news breaks, our subscribers know first

From Option to Empire: How a $13 Million Bet Became a Multi-Billion Dollar Enterprise

In 2015, Mordechai Gutnick established an investment vehicle with a focused mandate: secure exposure to the Round Top minerals deposit located near Sierra Blanca in the Trans-Pecos region of West Texas. The entry structure was relatively modest by today's standards, requiring a $10 million development commitment and a $3 million cash payment to acquire an option over an 80% interest in the deposit.

Round Top is not a conventional rare earth project. The deposit is hosted within a rhyolite volcanic complex and contains an unusually broad basket of critical minerals, including heavy rare earth elements such as dysprosium and terbium, which are among the most strategically valuable and least substitutable inputs for permanent magnet manufacturing. Heavy rare earths are significantly scarcer than light rare earths, and the fact that Round Top has meaningful heavy rare earth endowment gives it a geological profile that is meaningfully differentiated from most North American rare earth projects, which tend to be light-rare-earth-dominant.

That founding position became the cornerstone asset when USA Rare Earth completed its public market debut through a SPAC merger in March 2025, with Gutnick formally recognised in SEC filings as the founding investor of the company's operating entity. What began as a sub-$15 million options position had, by mid-2026, anchored a company pursuing capital commitments measured in billions.

The Serra Verde Acquisition and the Board Restructuring It Triggered

The formal announcement that Mordechai Gutnick exits USA Rare Earth board came on April 20, 2026, alongside confirmation that General Paul Kern would also not continue as a director. Both departures were pre-communicated and structurally tied to the company's $2.8 billion acquisition of Brazil's Serra Verde Group, which requires the integration of two new directors to reflect the expanded governance demands of the combined organisation.

Serra Verde operates an active rare earth mine and processing facility in Brazil, providing USA Rare Earth with something Round Top cannot yet offer: near-term production capacity. This is a critical distinction in the rare earth investment landscape, where the gap between exploration-stage assets and operating cashflow can span a decade or more.

The strategic logic of the Serra Verde deal is compelling:

- It provides geographic diversification, reducing the company's exposure to single-jurisdiction sovereign and regulatory risk

- It adds operating cash flow potential ahead of Round Top's projected 2028 commercial production date

- It deepens USA Rare Earth's processing capabilities across two continents, complementing the separately announced $204 million France-linked processing expansion

- It signals to institutional investors that the company is executing a deliberate, asset-by-asset construction of a vertically integrated supply chain

Vertical integration across mining, processing, and magnet manufacturing is the model that China spent three decades building. Western companies attempting to replicate that structure in compressed timeframes face both enormous capital requirements and significant execution complexity.

USA Rare Earth's Capital Structure and Key Financial Milestones

The financial trajectory of USA Rare Earth over the past 18 months has been remarkable. The table below summarises the key capital events shaping the company's current position:

| Event | Value | Timing |

|---|---|---|

| Federal government funding arrangement | Up to $1.6 billion | January 2026 |

| US government equity stake acquired | 10% | January 2026 |

| Serra Verde Group (Brazil) acquisition | $2.8 billion | April 2026 |

| France processing expansion commitment | $204 million | 2026 |

| Share price gain year-to-date | +90% | As of June 2026 |

| Gutnick trust stake valuation | ~$351 million | As of June 2026 |

The federal funding arrangement, in which the US government agreed to acquire a 10% equity stake in USA Rare Earth as part of a broader $1.6 billion commitment, represents an unusual structural feature. Direct government equity participation in a listed mining company is rare in the US context and introduces a governance dynamic that differs materially from conventional private-sector capital structures.

Furthermore, this arrangement introduces a layer of political risk: a US House Democrat has formally described the Commerce Department's involvement as highly concerning, raising the prospect of ongoing congressional scrutiny that investors should monitor carefully.

Disclaimer: Past share price performance is not indicative of future returns. The capital commitments and valuations cited reflect publicly reported figures as of June 2026 and are subject to change. This article does not constitute financial advice.

Understanding the Variable Prepaid Forward: A Sophisticated Liquidity Tool

One of the lesser-understood aspects of Gutnick's transition involves his entry into a variable prepaid forward contract with JPMorgan Chase & Co., covering approximately one quarter of his total shareholding, which itself represents roughly 7% of USA Rare Earth's total issued capital held through a trust structure.

A variable prepaid forward is a financial instrument that allows a significant shareholder to receive an upfront cash payment from a counterparty (in this case JPMorgan) in exchange for an obligation to deliver a variable number of shares at a future date. The number of shares ultimately delivered depends on the stock price at settlement, which is why it is described as "variable."

Key characteristics of this structure include:

- It does not constitute an immediate market sale of the underlying shares

- The shares subject to the contract typically remain on the shareholder's register during the contract period

- It provides liquidity access without the market impact of a block sale announcement

- It defers the formal disposal event, which may have tax planning implications depending on jurisdiction

- It is commonly used by founders and early investors in listed companies to monetise a portion of a concentrated position

The table below contextualises the scale of the position:

| Factor | Detail |

|---|---|

| Total Gutnick stake | ~7% of USA Rare Earth |

| Shares covered by forward contract | ~25% of his total position |

| Approximate implied stake affected | ~1.75% of total company |

| Counterparty | JPMorgan Chase & Co. |

| Instrument type | Variable prepaid forward |

A variable prepaid forward is a tool of capital management, not capitulation. Its use reflects sophisticated estate and liquidity planning consistent with the behaviour of a long-term holder managing a concentrated, high-value position.

The Gutnick Family: Mining Dynasties, Regulatory History, and Independent Legacies

No analysis of Mordechai Gutnick's role at USA Rare Earth is complete without acknowledging the broader family context, while carefully distinguishing between two individuals whose professional trajectories have diverged significantly.

Joseph "Diamond Joe" Gutnick, 74, built one of Australia's most recognisable mining fortunes across several decades. Acting on spiritual counsel, he pursued gold and diamond exploration in remote areas of the Australian outback, ultimately being credited with discoveries tied to Jundee, Bronzewing, Plutonic, and the Duketon Belt, each of which contributed to significant wealth creation during the Australian gold boom of the 1980s and 1990s.

He served as a director of the World Gold Council, presided over an Australian rules football club, and reportedly played a role in financing Benjamin Netanyahu's 1996 Israeli electoral campaign.

The later chapters of Joseph's career were more turbulent. He declared bankruptcy in 2016 with debts of approximately A$275 million (~$194 million USD), primarily connected to a collapsed fertilizer supply arrangement. In 2024, Australia's corporate regulator ASIC determined he had failed to meet his director obligations across multiple companies and imposed a four-year ban from managing corporations.

One of those companies, Merlin Diamonds, was forced into liquidation after it was found to have directed approximately A$13.7 million in investor funds to a private company associated with Joseph.

Mordechai assumed the managing director role at Merlin Diamonds in 2016 following Joseph's resignation, which introduced an association with that chapter of the family's corporate history. However, his founding of the Round Top investment vehicle in 2015 predates those events and represents an independently conceived investment thesis that has, by any measure, produced exceptional outcomes.

The next major ASX story will hit our subscribers first

Round Top's Geological Edge: Why Location and Mineralogy Matter

The Round Top deposit deserves closer technical scrutiny, because its geological characteristics help explain why it attracted serious institutional capital rather than languishing as one of many undeveloped rare earth projects globally.

Round Top is hosted in a peralkaline rhyolite complex, a geological setting that tends to concentrate heavy rare earth elements rather than the lighter elements that dominate most other deposits. The heavy rare earth elements, particularly dysprosium and terbium, command significant price premiums because they are essential for high-performance permanent magnets that must operate at elevated temperatures, such as those used in electric vehicle drivetrains and advanced defence systems.

This mineralogical profile creates a commercial dynamic that differs from better-known projects. In addition, the broader setting compounds Round Top's appeal across several dimensions:

- Heavy rare earth content is generally less abundant globally, creating a more defensible supply position

- The deposit also contains lithium, beryllium, and uranium byproducts, which may offer additional revenue streams

- The West Texas location provides infrastructure access and proximity to US industrial end-users, reducing logistics costs relative to offshore suppliers

- Heap leach processing methodologies being explored for Round Top could offer relatively lower capital intensity compared to conventional rare earth processing routes

Competitive Landscape and the Race to Build Western Supply Chains

USA Rare Earth's integrated strategy places it in direct competition with a small number of serious non-Chinese rare earth developers. MP Materials, which operates the Mountain Pass mine in California, represents the most advanced US-based peer, but its asset base is geographically concentrated and skewed toward light rare earths. USA Rare Earth's multi-jurisdictional footprint, spanning Texas, Brazil, and France, provides a broader exposure across the rare earth value chain.

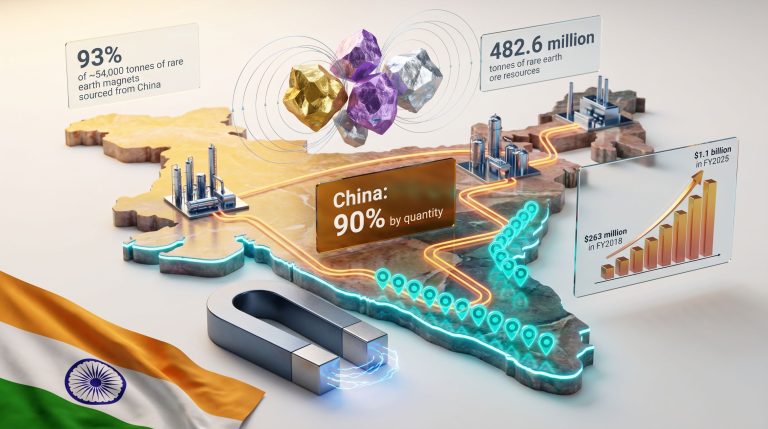

China currently controls an estimated 60% or more of global rare earth mining output and a substantially larger share of downstream separation and permanent magnet manufacturing capacity. Consequently, that concentration represents a systemic risk for industries ranging from electric vehicle production to wind energy and defence electronics. Understanding the full scope of China's rare earth strategy is therefore essential context for evaluating the urgency behind USA Rare Earth's expansion.

The broader Western supply chain realignment effort faces several structural challenges that investors should weigh carefully. Moreover, the rare earth processing challenges specific to non-Chinese operators compound these difficulties considerably:

- Processing complexity: Rare earth separation is chemically intensive and has historically been optimised in China over decades of industrial investment

- Timeline risk: Moving from deposit to commercial production typically takes 10 to 15 years; USA Rare Earth's 2028 target for Round Top represents an ambitious schedule

- Price volatility: Rare earth prices are notoriously cyclical and can move dramatically based on Chinese export policy decisions

- Capital intensity: Building a fully integrated supply chain outside China requires sustained multi-billion dollar commitments across multiple asset classes

- Talent scarcity: Western rare earth processing expertise is genuinely limited, making human capital a potential bottleneck

Key Factors for Investors and Industry Observers to Monitor

As the governance transition associated with Mordechai Gutnick's board exit is completed and USA Rare Earth enters its next phase of execution, several watchpoints stand out. The US rare earth supply chain context makes these developments all the more consequential for the broader industry.

- Identity of the two incoming Serra Verde-linked directors: Their backgrounds will signal whether the board is strengthening operational, financial, or political expertise

- Round Top production timeline adherence: The 2028 commercial production target is the most critical near-term operational milestone for validating the company's investment thesis

- Federal equity dynamics: The US government's 10% stake creates an unconventional governance overlay that could influence future capital raises, dividend policy, and strategic decisions

- Congressional scrutiny trajectory: The bipartisan concerns raised about the Commerce Department's $1.6 billion arrangement could escalate or dissipate depending on political developments

- Serra Verde integration execution: Large cross-border acquisitions in the mining sector carry significant integration risk; early operational and financial reporting from the Brazilian asset will be closely watched

- Gutnick's retained 7% stake: His continued economic exposure through a trust structure maintains long-term alignment with shareholder outcomes despite the board exit, which is a constructive signal for governance continuity

Furthermore, the shifting rare earth geopolitics reshaping global mineral competition mean that board changes at USA Rare Earth will continue to attract attention well beyond conventional investor audiences.

Important disclaimer: This article contains forward-looking statements, financial estimates, and analysis that involve inherent uncertainty. Readers should conduct independent due diligence and consult qualified financial advisers before making any investment decisions related to companies or assets discussed herein.

Ready to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements across more than 30 commodities — including critical minerals and rare earths — delivering real-time alerts on significant discoveries so investors can act before the broader market catches on. Explore how historic mineral discoveries have generated extraordinary returns, then start your 14-day free trial at Discovery Alert to secure your edge in the rapidly evolving critical minerals landscape.