June 19, 2026

When Inventory Becomes Leverage: How Indian Refiners Are Reshaping West Asia Crude Dynamics

Global energy markets often move on the assumption that demand is constant and suppliers hold the cards. Yet periodically, a convergence of geopolitical disruption, supply chain adaptation, and deliberate procurement strategy flips that equation entirely. The situation unfolding across India's state-owned refining sector in mid-2026 is precisely one of those rare inflection points, and its consequences extend well beyond the subcontinent.

Understanding why Indian refiners crude purchases from West Asia have effectively stalled requires looking past the headline ceasefire news and into the structural mechanics of how large-scale crude procurement actually works, and why timing, not just price, determines who holds negotiating power. Furthermore, crude oil price volatility has added another layer of complexity to these already strained procurement decisions.

When big ASX news breaks, our subscribers know first

The Procurement Pause: More Strategic Than It Appears

India's state-owned refiners have accumulated approximately two months of crude inventory, a buffer that fundamentally reorders the urgency calculus in their dealings with West Asian suppliers. This is not a passive outcome of logistics or chance. It reflects deliberate procurement pivots executed during a period of acute supply disruption, and it now functions as a sophisticated piece of commercial leverage.

When buyers control timing, the pressure of unsold volumes shifts entirely to the supplier side. West Asian producers, including Abu Dhabi National Oil Company (ADNOC), have formally communicated their expectation that Indian refiners resume taking contractual volumes under existing long-term supply agreements. Those commitments have not yet materialised.

Several reinforcing factors explain the hesitation:

- Adequate existing inventory removes procurement urgency entirely

- The central government in New Delhi has not yet issued clearance on when vessels can safely return to load cargoes from the Persian Gulf region

- Rising freight rates, anticipated as global buyers scramble to secure tankers following the partial reopening of the Strait of Hormuz, erode the economics of loading-basis West Asian purchases

- Competitive alternatives, particularly Russian and South American spot cargoes, continue to offer better landed-cost outcomes

India's state refining sector purchases West Asian crude predominantly on a loading basis, meaning buyers bear full exposure to tanker market conditions. This structural feature makes freight rate volatility a first-order financial variable in any resumption decision.

Q2 2026: A Historic Low in West Asian Crude Imports

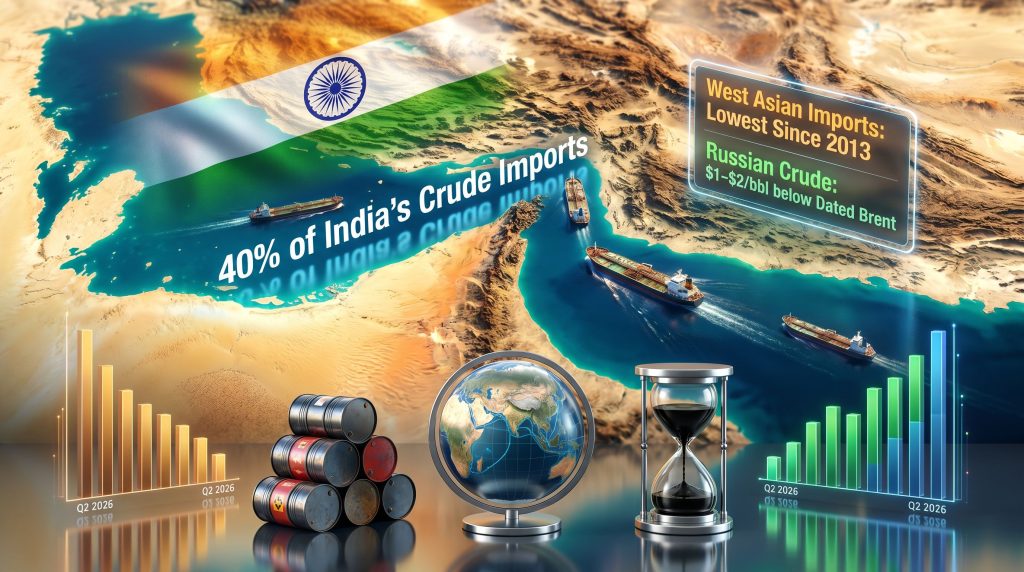

The scale of the Q2 2026 import collapse is remarkable by any historical measure. According to vessel-tracking data compiled by Kpler, India's imports of West Asian crude during the second quarter fell to their lowest recorded level since at least 2013. That represents more than a decade of procurement history, spanning multiple sanctions cycles, oil price crashes, and diplomatic realignments.

The immediate cause was the near-total blockade of the Strait of Hormuz, the result of simultaneous Iranian and US naval posturing that brought commercial energy shipping through the waterway to a near standstill. The downstream effect on Indian procurement was immediate and severe. In addition, oil market trade disruptions arising from broader geopolitical tensions compounded the difficulties faced by Indian buyers seeking alternative supply routes.

| Supply Region | Q2 2026 Import Status | Key Development |

|---|---|---|

| West Asia (Overall) | Lowest since 2013 | Strait of Hormuz blockade |

| Iraq | Shipments fell to near-zero | No alternative Gulf export routes |

| Saudi Arabia and UAE | Partial supply maintained | Alternative routing explored |

| Russia | Increased spot volumes | Delivered-basis pricing advantage |

| Brazil and Venezuela | Supplementary sourcing | Spot market diversification |

| Iran | Re-entered procurement mix | Volumes confirmed by petroleum ministry |

Among all West Asian exporters, Iraq faces disproportionate exposure to any Hormuz closure. Unlike Saudi Arabia or the UAE, Iraq lacks the pipeline infrastructure or alternative export terminals needed to redirect volumes away from Gulf loading points. When the strait closes, Iraqi export capacity to Asia effectively closes with it.

The Hormuz Chokepoint: Why 40% Creates Systemic Vulnerability

Approximately 40% of India's total crude imports have historically transited through the Strait of Hormuz, making it the single most consequential maritime chokepoint in the country's energy security architecture. No other shipping lane comes close to this concentration of supply risk.

The Q2 2026 disruption was not the first stress test of this vulnerability, but it was arguably the most severe in modern history. The simultaneous blockade by both Iranian naval forces and US naval posturing created a scenario that energy security planners had modelled theoretically but had never encountered operationally at this scale.

What makes the Hormuz closure particularly dangerous for India compared to other import-dependent economies is the loading-basis procurement model used for Gulf crude. Because Indian state refiners arrange and pay for shipping independently, any disruption to freight availability or safety of passage directly increases landed costs, even if the crude price itself remains unchanged.

The Hormuz chokepoint is not merely a physical risk — it is a pricing mechanism. When it closes or becomes contested, the effective cost of West Asian crude rises for loading-basis buyers regardless of benchmark crude valuations.

Russia's Structural Advantage: The Delivered-Basis Difference

The delivered-basis pricing model used for Russian crude exports to India is frequently misunderstood as simply a discount story. The commercial reality is more nuanced. When Russian barrels arrive with freight costs already embedded in the price, Indian refiners are insulated from the freight market entirely. This becomes commercially decisive in precisely the conditions that now prevail: a contested shipping environment, rising tanker charter rates, and uncertainty about the durability of any ceasefire arrangement.

As of mid-June 2026, Russian crude was trading at discounts of approximately $1 to $2 per barrel below Dated Brent, with the potential for those discounts to widen further as Russian supply availability improves. The Russian oil sanctions impact has, however, introduced additional complexity into procurement channels that Indian refiners must continue to navigate carefully. Despite the expiry of US sanction waivers on Russian crude purchases, Indian refiners are expected to continue sourcing these barrels, having developed operational frameworks that allow procurement to proceed.

The competitive calculus looks like this:

- West Asian crude: Benchmark-linked pricing, loading-basis purchase, full freight exposure, uncertainty over shipping lane durability

- Russian crude: Sub-Brent pricing, delivered-basis purchase, zero freight exposure, established operational channels despite sanctions complexity

- South American crude: Spot market pricing, moderate freight costs, geopolitically neutral, limited volume scalability

In the current environment, the delivered-basis advantage of Russian barrels is arguably more valuable than the headline discount figure suggests. A $1.50 per barrel discount that comes with embedded freight costs may represent a $3 to $5 per barrel landed-cost advantage relative to Gulf crude when VLCC charter rates are elevated.

India's Supplier Hierarchy: How the Import Mix Actually Works

India's state refining sector does not operate with a single-origin supply strategy. The procurement architecture is deliberately diversified across three functional tiers, each serving a different purpose in the overall supply equation.

Tier 1: Baseline Term Suppliers (Currently Under Review)

- Saudi Arabia

- UAE via ADNOC

- Iraq

Tier 2: Opportunistic and Spot Suppliers (Currently Active)

- Russia, on delivered basis with sub-Brent pricing

- Brazil, as a spot market complement

- Venezuela, for volume diversification

Tier 3: Geopolitically Sensitive and Conditional Suppliers

- Iran, with volumes confirmed but undisclosed, subject to ongoing sanctions monitoring

This tiered architecture is a deliberate design feature, not an improvised response to disruption. During normal operating conditions, Tier 1 suppliers handle the majority of volume through long-term contracts. When those flows are interrupted, Tiers 2 and 3 expand to fill the gap. The Q2 2026 disruption tested this system at an unprecedented scale and, by most assessments, it performed its intended function. For a broader perspective on how these dynamics interact globally, the global crude market overview provides useful context on pricing and supply conditions.

The next major ASX story will hit our subscribers first

The IOC Tanker Tender: Market Intelligence, Not a Signal

Indian Oil Corporation recently issued a tender to charter a Very Large Crude Carrier (VLCC), a Suezmax tanker, and a Very Large Gas Carrier (VLGC) to lift crude and liquefied petroleum gas from ports behind the Strait of Hormuz. This generated considerable market speculation about imminent procurement resumption.

The reality is more cautious. Industry sources familiar with the matter indicate this tender represents market-testing for vessel availability rather than a committed procurement decision. Understanding the difference matters for anyone tracking Indian import flows.

A VLCC tender of this type serves several functions beyond actual cargo lifting:

- It establishes a current baseline for tanker charter rates in a disrupted market

- It signals market readiness to suppliers without committing to volume

- It provides freight market intelligence for internal procurement cost modelling

- It maintains optionality without triggering contractual obligations

The IOC tender should be read as an information-gathering exercise operating within a broader wait-and-see framework, not as confirmation of a procurement decision.

Ceasefire Durability: Why Caution Outlasts Headlines

The US-Iran interim peace arrangement reached in mid-June 2026 has, in principle, reopened the Strait of Hormuz to commercial shipping. In practice, Indian refiners are treating this development with measured deliberation rather than enthusiasm. Two interconnected concerns drive this caution.

First, the interim nature of the ceasefire creates genuine uncertainty about its durability. An agreement that might unravel within 30 to 60 days is not a reliable foundation for committing to loading-basis crude purchases that require vessel deployment, port scheduling, and freight contracting.

Second, and perhaps less intuitively, the ceasefire itself creates a freight market problem. As global buyers rush to secure tankers in anticipation of resumed Gulf flows, VLCC charter rates are expected to rise sharply in the near term. This front-running effect means that the economics of West Asian loading-basis purchases may actually deteriorate in the weeks immediately following a ceasefire announcement, even as the physical shipping lanes reopen. According to Reuters, India's biggest refiner has already demonstrated a willingness to pivot between US and Middle East crude depending on prevailing conditions, further illustrating the flexibility at play.

| Scenario | Trigger Condition | Likely Indian Response |

|---|---|---|

| Durable Ceasefire | Sustained Hormuz access over 60 days | Gradual term contract resumption with ADNOC and Saudi Aramco |

| Ceasefire Breakdown | Renewed disruption within 30 to 60 days | Extended reliance on Russian and South American spot cargoes |

| Partial Access | Intermittent or contested shipping lanes | Hybrid procurement combining partial term volumes with spot diversification |

Structural Lessons: What the Disruption Revealed About India's Energy Architecture

Beyond the immediate procurement dynamics, the Q2 2026 Hormuz disruption has validated and stress-tested several principles that underpin India's long-term energy security thinking.

Inventory buffers are a strategic asset with commercial utility, not merely an operational safety margin. A two-month crude cushion converts a procurement emergency into a negotiating position, altering the power dynamic with suppliers in ways that have lasting contract renegotiation implications.

Multi-origin diversification generates genuine commercial leverage beyond supply security. The ability to source competitively from Russia, Brazil, Venezuela, and Iran simultaneously is not just a risk management tool — it is a pricing tool that disciplines term contract suppliers.

Delivered-basis procurement from non-Gulf suppliers reduces systemic freight exposure in ways that loading-basis procurement cannot replicate. This distinction deserves greater weight in energy security planning frameworks.

Spot market agility is structurally equivalent in value to long-term contract stability in a geopolitically volatile environment. The Q2 2026 experience demonstrated that Indian refiners could absorb a near-complete collapse in their primary supply region without a corresponding operational crisis, largely because spot market alternatives existed at competitive prices.

What This Means for West Asian Producers and Global Oil Pricing

India is the world's third-largest crude oil importer. Its purchasing decisions carry material weight in global oil market pricing, particularly for Gulf crude grades. A prolonged pause in term contract fulfilment by Indian state refiners creates several pressure points for West Asian producers. Consequently, OPEC's market influence over pricing and supply allocation may also come under renewed scrutiny as India's diversified procurement strategy continues to evolve.

- Downward price pressure on Gulf crude grades as unsold contracted volumes accumulate

- Incentive to offer more competitive pricing or flexible terms to accelerate volume resumption

- Validation of Russia's structural market penetration in Asian crude demand, even under sustained sanctions complexity

- Longer-term questions about the optimal structure of term contracts with loading-basis buyers in high-volatility shipping environments

The broader implication is that the geopolitical disruption of Q2 2026, while temporary in its physical dimension, may have lasting consequences for the commercial architecture of Indian refiners crude purchases from West Asia trade relationships. Buyers who demonstrate they can operate competitively without their primary suppliers for extended periods tend to negotiate better terms when they return. Bloomberg reports that shifts in Indian buying behaviour have already prompted considerable re-evaluation of supply assumptions among global producers.

Frequently Asked Questions: Indian Refiners and West Asia Crude Purchases

Why are Indian refiners not immediately resuming purchases from West Asia after the Hormuz ceasefire?

Indian state refiners hold approximately two months of secured crude inventory, removing procurement urgency. Government vessel safety clearance has not yet been issued, and rising freight rates in the wake of the ceasefire are eroding the economics of loading-basis Gulf purchases.

How low did India's West Asian crude imports fall during Q2 2026?

According to vessel-tracking data from Kpler, India's imports of West Asian crude in Q2 2026 fell to their lowest level since at least 2013.

What alternative suppliers did India use during the Hormuz disruption?

Indian refiners increased spot cargo procurement from Russia on a delivered basis, supplemented by Brazilian and Venezuelan barrels, and also sourced Iranian crude in volumes confirmed but undisclosed by India's petroleum ministry.

What is the current discount on Russian crude relative to benchmark pricing?

Russian crude was trading at approximately $1 to $2 per barrel below Dated Brent as of mid-June 2026, with the potential for discounts to widen as supply availability improves.

What does the Indian Oil Corporation tanker tender signal?

IOC's tender for a VLCC, Suezmax, and VLGC represents market-testing for vessel availability, not a confirmed commitment to resume Indian refiners crude purchases from West Asia imminently.

How much of India's crude historically transits the Strait of Hormuz?

Approximately 40% of India's total crude imports have historically moved through the Strait of Hormuz, making it the most critical maritime energy chokepoint in India's import architecture.

Readers seeking broader context on India's energy import strategy and global crude oil market dynamics can explore additional coverage at ET EnergyWorld's Oil & Gas section. This article contains forward-looking analysis based on available market information as of mid-June 2026. Procurement decisions, freight market conditions, and geopolitical developments may change materially. Nothing in this article constitutes financial or investment advice.

Want to Stay Ahead of the Next Major Commodity Market Shift?

When geopolitical disruptions reshape global energy flows, the ripple effects reach every corner of the commodities market — including ASX-listed mineral and energy explorers. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly cutting through market noise to surface actionable opportunities the moment they emerge. Explore historic discoveries and their extraordinary returns on Discovery Alert's dedicated discoveries page, or start your 14-day free trial today to position yourself ahead of the market.