July 11, 2026

The Geography of Disruption: How Gulf Instability Is Redrawing Aluminium Trade Routes

When geopolitical shocks sever established commodity corridors, markets rarely wait patiently for normalisation. They adapt, reroute, and in doing so, permanently shift the architecture of global trade. That dynamic is now playing out in real time across the global aluminium market, where disruptions to Gulf-region supply chains have triggered a cascading search for alternative primary metal sources, with Indonesia emerging as one of the most consequential new origins in the story.

Understanding why this matters requires looking beyond the immediate shipment headlines and examining the structural forces that have converged to make Indonesia aluminium exports to the US a genuine market development rather than a fleeting arbitrage opportunity.

When big ASX news breaks, our subscribers know first

Why the Gulf Supply Shock Changed Everything

The Middle East has long functioned as a critical node in global aluminium supply, with producers in the UAE and Bahrain operating world-scale smelters that feed both Asian and Western markets. The region's competitive advantage is built on access to low-cost energy, strategic port infrastructure, and decades of accumulated industrial expertise.

That reliability made Gulf aluminium a default sourcing option for many US buyers. However, when geopolitical instability disrupted deliveries from these key suppliers in 2026, the consequences rippled through pricing with unusual speed. US aluminium spot premiums climbed to record highs in mid-2026, reflecting an acute shortage of primary metal in a market that had structurally underinvested in supply diversification. This mirrors broader concerns seen across aluminum and alumina markets in recent years.

The response from commodity markets was predictable in direction if not in scale: buyers began looking eastward, toward Southeast Asia, for replacement volume. What they found in Indonesia was not a backup supplier scrambling to fill a gap, but a newly industrialised aluminium producer with freshly commissioned smelting capacity and, critically, the scale to matter.

"The convergence of Gulf supply disruption and Indonesia's new smelting buildout created a rare alignment where geographic timing and industrial readiness met market need simultaneously."

Mapping Indonesia's Export Surge: The Volume Story

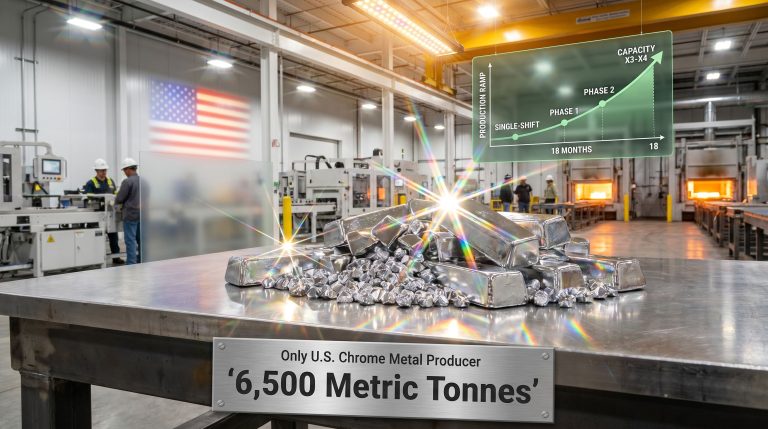

The numbers behind Indonesia's emergence as a US aluminium supplier are striking in their velocity. In March 2026, approximately 18,500 tonnes of aluminium were shipped to the US from the Weda Bay complex, a facility developed through Chinese industrial partnerships involving Tsingshan and Xinfa. That single-month figure represented a 28-month export high for the origin.

By June 2026, the pace had accelerated further. PT Kalimantan Aluminium Industry, located on the island of Borneo and a subsidiary of mining and energy group PT Alamtri Resources Indonesia, shipped 31,494 metric tonnes of primary aluminium to the United States in that month alone, alongside 3,569 tonnes to South Korea.

The broader annual picture reinforces the trend:

| Period | Volume or Value | Key Detail |

|---|---|---|

| March 2026 | 18,500 tonnes | Weda Bay complex; 28-month export high |

| March 2026 (total exports) | 88,554 tonnes | 100% month-on-month increase |

| June 2026 (US-bound) | 31,494 tonnes | Kalimantan smelter; via Brownsville, Texas |

| June 2026 (South Korea) | 3,569 tonnes | Shipped to Incheon |

| Full year 2025 (US-bound) | US$161.58 million | All aluminium categories |

| Full year 2023 (US-bound) | US$143.1 million | Dominated by fabricated products |

What the annual data also reveals is a structural compositional shift in what Indonesia exports to the US. Historically, the trade relationship was dominated by fabricated aluminium products such as bars, rods, profiles, foil, and structural components. The 2023 baseline tells that story clearly:

| Product Category | Export Value (USD, 2023) |

|---|---|

| Aluminium bars, rods and profiles | $85.62 million |

| Aluminium foil (2mm or less) | $24.80 million |

| Aluminium structures and parts | $17.91 million |

| Unwrought aluminium | $1.55 million |

| Aluminium plates and sheets (over 2mm) | $1.54 million |

The contrast with 2026 flows is telling. The current export surge is being driven almost entirely by unwrought primary aluminium, the most upstream form of the metal, rather than the fabricated downstream categories that historically dominated Indonesia's trade with the US. This is not simply a volume increase; it represents a fundamental repositioning of Indonesia within the global aluminium value chain.

Kalimantan's Smelting Buildout: Why Borneo Is Now Significant

The island of Borneo, or Kalimantan as the Indonesian portion is known, has emerged as the geographic epicentre of Indonesia's new primary aluminium production capacity. This is not coincidental. The region offers a combination of infrastructure access, proximity to bauxite resources, and energy supply options that make energy-intensive smelting operations economically viable.

Aluminium smelting is among the most electricity-intensive industrial processes in existence, consuming approximately 13 to 15 megawatt-hours of electricity per tonne of aluminium produced. Access to competitively priced power, whether derived from coal generation or hydropower resources, is therefore a primary determinant of smelting economics.

PT Kalimantan Aluminium Industry began commissioning its first production phase at the end of 2025, with a stated target of up to 350,000 tonnes of aluminium ingot sales in its first full year of commercial operation, spanning both domestic and international markets. To place that figure in perspective, 350,000 tonnes would represent a meaningful share of total US aluminium imports in a given year, though not a dominant one.

Meanwhile, the Weda Bay complex, developed with the involvement of Chinese industrial capital through partnerships with Tsingshan and Xinfa, has been operational for longer and demonstrated the capacity to deliver large single-month shipment volumes to the US market.

The role of Chinese industrial capital and technology transfer in both projects is a structurally important dimension that often receives insufficient analytical attention. China is the world's dominant aluminium producer, accounting for more than 55% of global primary aluminium output. Its firms have accumulated proprietary expertise in smelter construction, electrolysis cell technology, and operational efficiency that is now being deployed in host countries across Southeast Asia, including Indonesia.

Smelting Economics: Indonesia vs. Key Competitors

| Producer Region | Key Cost Advantage | Key Cost Risk | Approximate Position |

|---|---|---|---|

| China | Scale, technology, domestic bauxite | Regulatory pressure, carbon costs | Lowest-cost dominant producer |

| Indonesia | Low energy costs, bauxite resource base | Infrastructure gaps, logistics | Rapidly improving cost position |

| Gulf Region (UAE, Bahrain) | Subsidised energy, scale | Geopolitical exposure | Competitive but disrupted |

| India | Large domestic market | High energy costs | Higher-cost established player |

| Canada | Hydropower, stable trade access | High capital costs | Premium-quality, higher-cost |

The Trading House Dimension: Mercuria, Vitol, and the Signal They Send

One of the most analytically significant aspects of Indonesia's US aluminium export surge is the identity of the buyers intermediating the trade. The June 2026 US-bound shipment of 31,494 tonnes was purchased by Mercuria, one of the world's largest commodity trading houses, and was routed to Brownsville, Texas, having departed Indonesia on June 10. The simultaneous South Korea shipment was secured by Vitol, another Tier-1 global trading firm, destined for Incheon.

The involvement of firms of this calibre carries a specific signal value for market observers. Commodity trading houses at this scale do not engage with nascent supply corridors opportunistically or without substantial due diligence. Their participation implies:

- Confidence in the physical quality and specification of Indonesian primary aluminium

- Conviction that freight economics support the trade at current premium levels

- Existing or developing offtake relationships with the Indonesian smelting operations

- An assessment that the supply corridor has repeatable, scalable characteristics

Brownsville, Texas functions as a strategically located entry point for primary metal distribution into the broader US industrial supply chain, providing access to Gulf Coast aluminium consuming industries in automotive, construction, and manufacturing sectors.

South Korea's inclusion in the June 2026 shipment data is also notable. Like the US, South Korea has historically relied on Gulf smelters for a significant portion of its primary aluminium imports. The country's exposure to the same supply disruption dynamic that elevated US premiums created parallel incentive structures for Korean buyers to diversify sourcing, making Indonesia a logical candidate given proximity and new capacity availability.

Trade Policy: The Antidumping Complication

Any assessment of the sustainability of Indonesia's aluminium export growth into the US market must engage seriously with trade policy risk. In October 2024, the US Department of Commerce issued a finding that aluminium extrusions from Indonesia were being sold in the US market at less than fair value, the definitional threshold for antidumping duty application. Furthermore, the broader landscape of US aluminium tariffs continues to shape sourcing decisions across the sector.

This distinction between aluminium extrusions (the fabricated product category subject to antidumping scrutiny) and unwrought primary aluminium (the product driving the current export surge) is critical for understanding the current trade landscape. The two product categories are treated differently under US trade remedy frameworks, and the June 2026 shipments consist of primary ingot rather than extruded product, placing them outside the scope of the existing antidumping finding.

However, the precedent carries forward-looking implications:

- Rapid growth in unwrought aluminium imports from Indonesia could attract fresh scrutiny under US trade remedy mechanisms

- The political environment surrounding aluminium imports has been consistently protective in recent years

- Indonesian exporters and their trading counterparts may structure future shipments with trade policy risk explicitly modelled

"Trade policy risk is asymmetric in the aluminium sector. Duties, once applied, can restructure bilateral trade flows almost immediately. The absence of current duties on unwrought Indonesian aluminium should not be interpreted as permanent clearance."

Trade Risk Comparison Across Key US Aluminium Supply Sources

| Supplier Origin | Trade Remedy Status | Geopolitical Supply Risk | Current Volume Scale |

|---|---|---|---|

| Gulf Region | Low duty exposure | High (2026 disruption) | Large but disrupted |

| China | High (tariffs and duties) | Medium | Very large, mostly excluded |

| Canada | Minimal | Very low | Very large, preferred source |

| Indonesia (extrusions) | Antidumping finding (Oct 2024) | Low-medium | Growing |

| Indonesia (unwrought) | Currently low exposure | Low-medium | Rapidly accelerating |

| Malaysia | Low-moderate | Low | Moderate |

The next major ASX story will hit our subscribers first

Indonesia's Industrial Policy Framework: This Is Not Opportunism

A critical contextual point for understanding Indonesia's aluminium export trajectory is that the current surge is not a reactive, short-term arbitrage play. It is the export manifestation of a deliberate, multi-year industrial policy framework that Indonesia has been executing across its entire minerals processing sector.

Indonesia implemented a bauxite export ban in 2023, prohibiting the export of unprocessed bauxite ore in a direct parallel to its earlier nickel ore export restrictions. The policy intent was explicit: force domestic processing of raw materials before export, capturing more value within Indonesia's economy and developing industrial capability across the supply chain. In addition, bauxite supply growth from neighbouring regions has further influenced how market participants view upstream resource availability.

The bauxite ban created an upstream policy imperative for alumina refining and aluminium smelting investment, which is now manifesting in export volumes. Foreign direct investment, particularly from Chinese industrial groups with existing relationships in Indonesia's nickel sector, provided the capital and technology required to construct smelting infrastructure at pace.

This policy architecture means that Indonesian aluminium smelting capacity is likely to continue expanding regardless of short-term Gulf supply dynamics, because the economics are supported by a captive upstream resource base and a policy framework that mandates domestic value addition. Consequently, global bauxite production patterns are increasingly being shaped by Indonesia's upstream policy decisions.

Scenario Analysis: Three Pathways for the Indonesia-US Aluminium Corridor

Scenario A: Sustained Trade Corridor

Gulf supply disruptions persist, US buyers formalise long-term offtake arrangements with Indonesian producers, and the trading house intermediation model gives way to direct industrial buyer relationships. Indonesian smelters reach nameplate capacity, enabling consistent quarterly shipments.

Scenario B: Normalisation and Partial Reversion

Gulf supply routes recover as geopolitical conditions stabilise, US aluminium premiums compress, and Indonesian exports rebalance toward Asian regional markets where freight economics are intrinsically more favourable. The US corridor persists but at lower volumes.

Scenario C: Trade Policy Redirection

Rising volumes attract antidumping or countervailing duty investigations targeting unwrought aluminium from Indonesia. Indonesian producers pivot toward higher-specification fabricated products or redirect export flows toward Japan, India, and European markets where trade remedy exposure is lower.

The most analytically defensible near-term view is a blend of Scenarios A and B. Indonesia is likely to capture a meaningful supplementary share of US primary aluminium imports during periods of Gulf supply stress, while functioning as a secondary rather than primary supplier when traditional routes operate normally. Understanding how major aluminium producers respond to this shift will be equally important in determining long-term market structure.

Frequently Asked Questions

How much aluminium did Indonesia ship to the US in June 2026?

PT Kalimantan Aluminium Industry shipped 31,494 metric tonnes of primary aluminium to the United States in June 2026, purchased by trading house Mercuria and delivered to Brownsville, Texas.

Why are US buyers sourcing aluminium from Indonesia?

Geopolitical instability disrupted aluminium deliveries from Gulf-region smelters, pushing US spot premiums to record highs and compelling buyers to identify alternative large-volume sources. Indonesia's newly commissioned smelting capacity offered a viable and scalable alternative, making Indonesia aluminium exports to the US an increasingly significant trade corridor.

Are Indonesian aluminium exports subject to US tariffs?

Indonesian aluminium extrusions were found to be sold below fair value by the US Department of Commerce in October 2024, making them subject to antidumping measures. However, the current export surge consists of unwrought primary aluminium, which currently faces a less restricted trade remedy environment.

What is driving Indonesia's new smelting capacity?

A combination of Indonesia's 2023 bauxite export ban, foreign direct investment primarily from Chinese industrial groups, and the geographic advantages of Kalimantan for energy-intensive smelting operations has underpinned a rapid buildout of primary aluminium production capacity since late 2025.

Who are the main buyers of Indonesian aluminium being shipped to the US?

Mercuria, one of the world's largest commodity trading houses, purchased the June 2026 US-bound cargo. Vitol handled the South Korea shipment. The involvement of Tier-1 trading firms signals strong commercial confidence in Indonesian supply quality and logistics reliability.

What is the annual export value of Indonesian aluminium to the US?

In 2025, Indonesia aluminium exports to the US reached approximately US$161.58 million worth of aluminium products across all categories, up from US$143.1 million in 2023. The trajectory for 2026 points to a substantially higher figure as primary smelting volumes accelerate.

Want to Stay Ahead of the Commodity Shifts Reshaping Global Markets?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across aluminium, bauxite, and more than 30 other commodities — turning complex market data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major market move.