July 23, 2026

The Calorific Value Trap: Why Indonesia's Coal Supply Crisis Is a Quality Problem, Not a Volume Problem

Commodity markets have a tendency to misread policy signals, particularly when they originate from a single supplier with outsized influence over global trade flows. When Indonesia temporarily diverted certain export shipments in June 2026 to address domestic power shortages, seaborne coal markets responded with predictable anxiety. The ghost of January 2022, when a full export ban rattled Asian energy markets and sent benchmark prices sharply higher, loomed large over the reaction. Yet the situation unfolding in mid-2026 is structurally different from a simple Indonesia rules out coal export curbs narrative, technically more nuanced, and ultimately more instructive. Understanding why requires looking beyond the policy headline and into the engineering reality of how coal-fired power generation actually works.

When big ASX news breaks, our subscribers know first

Indonesia's Structural Position in Global Thermal Coal Trade

No single country holds more influence over the seaborne thermal coal market than Indonesia. The archipelago consistently ranks as the world's largest thermal coal exporter by volume, supplying roughly 50% of China's seaborne coal imports and absorbing a further significant share of demand from India, the Philippines, Malaysia, and South Korea. This concentration means that even a temporary, targeted adjustment to Indonesian export flows creates immediate pricing anxiety across Asian benchmark markets.

The memory of the January 2022 export ban reinforces this sensitivity. That episode, triggered by a domestic supply crunch remarkably similar to the one that emerged in mid-2026, demonstrated just how exposed regional buyers are to Indonesian policy decisions. China's thermal coal futures surged approximately 7.8% in the immediate aftermath of that announcement. The reputational cost to Indonesia as a reliable trading partner was also substantial, and policymakers have since cited the 2022 episode as a cautionary example when evaluating whether to reach for the blunt instrument of a full export ban.

Indonesia faces a fundamental tension that shapes every coal policy decision it makes. On one side sits the foreign exchange imperative: coal exports generate billions of dollars in annual revenue and remain critical to the national current account. On the other side sits the domestic electricity mandate: affordable, reliable power for a population of over 270 million people, much of it delivered through coal-fired plants operated by state utility PT Perusahaan Listrik Negara (PLN). The Domestic Market Obligation, or DMO, was designed to manage this tension. In practice, it has progressively failed to do so.

What Triggered the June 2026 Supply Crisis

Rolling Blackouts Across Java and the PLN Supply Deficit

The immediate catalyst for the June 2026 episode was a series of rolling blackouts across Java, Indonesia's most populous and economically important island. PLN confirmed a power deficit that peaked at approximately 2 gigawatts, prompting the utility to implement load shedding to stabilise the grid. Two baseload independent power plants in Cilacap and Pacitan were simultaneously offline due to technical failures, compounding a supply crunch that was already straining system resilience.

In response, Indonesia's Ministry of Energy and Mineral Resources (ESDM) established a cross-sector procurement team to accelerate the contracting of medium-calorific value coal for Java's grid power plants. Shipments were subsequently secured from major producers including Kaltim Prima Coal, Indo Tambangraya Megah (ITMG), and state-owned Bukit Asam. Specific power stations identified as experiencing fuel specification shortfalls included Suralaya units 1 to 8, Jawa 7, 9 and 10, Paiton units 1, 2, and 9, Pelabuhan Ratu, Lontar, Labuan, Indramayu, Rembang, and Tanjung Awar-Awar.

The Calorific Value Mismatch: A Technically Precise Problem

What makes this supply crisis distinctly different from a simple shortage is its technical character. The issue is not that Indonesia lacks sufficient coal. The issue is that the coal being delivered to PLN's power stations is predominantly low-calorific value material, while the plants require medium-CV coal rated above GAR 5,000 kcal/kg for blending purposes.

Understanding this distinction is essential for anyone tracking the seaborne coal market. Coal-fired power stations use calorific value specifications to maintain optimal combustion performance and boiler efficiency. When lower-rank coal is burned without adequate blending with medium-rank material, plants operate in a derated condition, meaning output falls below nameplate capacity without the plant technically going offline. This is precisely what drove the Java power deficit in June 2026: not a sudden shutdown of generation capacity, but a gradual erosion of effective output caused by fuel quality mismatch.

The Indonesia coal crisis of 2026 illustrates a principle that is underappreciated by those outside the power generation sector: coal is not a homogenous commodity. A power station designed for GAR 5,200 kcal/kg coal cannot simply substitute lower-rank material without measurable consequences for output, efficiency, and equipment wear.

The cross-sector procurement target was specifically set at coal with a calorific value of GAR 5,200 kcal/kg, the minimum threshold required to restore derated plants to their rated output levels through blending. Furthermore, the coal supply challenges evident in prior years provided important context for understanding how quickly quality mismatches can escalate into grid-level emergencies.

The 13 Million Tonne Supply Gap in Context

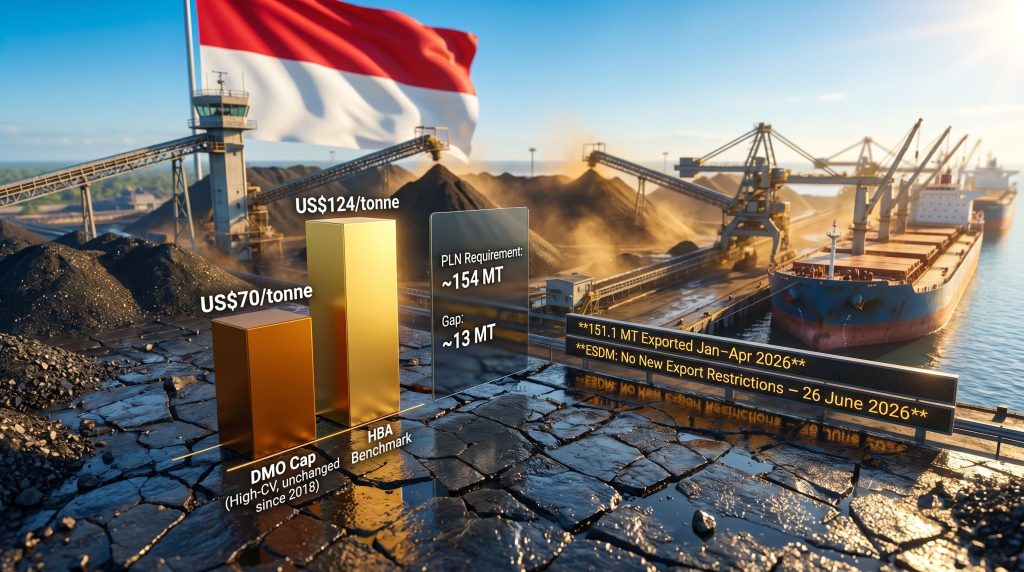

Against PLN's total annual coal requirement of approximately 154 million tonnes, supply contracts already secured at the time of the crisis totalled roughly 141 million tonnes, leaving a gap of approximately 13 million tonnes. The following table contextualises this within the broader DMO framework:

| Supply Metric | Volume |

|---|---|

| PLN total annual coal requirement | ~154 million tonnes |

| Contracted supply already secured | ~141 million tonnes |

| Remaining supply gap | ~13 million tonnes |

| Total DMO allocation | 180-190 million tonnes |

| DMO volumes committed | 160-170 million tonnes |

On paper, the DMO framework allocates far more than enough coal to cover PLN's requirements. The gap is not volumetric. It is qualitative, and understanding why requires examining the pricing architecture at the heart of the DMO.

Indonesia Rules Out Coal Export Curbs: The Official Response

Targeted Diversion, Not a Blanket Ban

On 26 June 2026, Indonesia's ESDM confirmed that no new proposals for additional export restrictions were under consideration. The ministry's position was that the existing regulatory framework, centred on the DMO, was sufficient provided it was effectively enforced. The Directorate General of Mineral and Coal (Minerba) had temporarily withheld specific export shipments as a targeted oversight measure to ensure that PLN's operational requirements for medium-CV coal could be met. As domestic supply conditions improved, exports resumed normal flows.

This distinction matters enormously for market participants. Indonesia rules out coal export curbs as a formal policy instrument, but retains the operational flexibility to redirect specific shipments when domestic supply conditions deteriorate. The difference between a blanket export prohibition and a calibrated regulatory diversion has significant implications for seaborne pricing, buyer confidence, and long-term supply contract management. In addition, the trade impacts on bulk commodities seen elsewhere in the region highlight how quickly policy ambiguity can translate into market-wide repricing.

The Multi-Agency Oversight Structure

To reinforce DMO compliance and prevent recurrence of the supply quality mismatch, a multi-agency oversight framework was activated to scrutinise PLN's primary energy procurement. The bodies involved include:

- The Financial and Development Supervisory Agency (BPKP)

- The Ministry of Energy and Mineral Resources (ESDM)

- The Directorate General of Mineral and Coal (Minerba)

- PT PLN itself

This architecture signals a shift from passive DMO administration toward active, real-time compliance monitoring. Whether it proves effective will depend on whether the underlying pricing distortion that drives producer behaviour is addressed.

Danantara Sumberdaya Indonesia: Monitoring, Not Market Control

Indonesia also established a state-owned entity, Danantara Sumberdaya Indonesia, to centralise coal export transactions. Initial market interpretation raised concerns that this could function as a tool for restricting or controlling export volumes. However, authorities subsequently clarified that Danantara's primary mandate is trade monitoring, specifically targeting the prevention of under-invoicing fraud. All coal exports are expected to be routed through the entity, consistent with the original policy announcement, but it does not represent a new mechanism for imposing export limitations. According to reporting on Indonesian coal export uncertainty, the market's initial anxiety around Danantara reflected broader concerns about state intervention rather than any confirmed policy shift.

The DMO Pricing Problem: Why the System Keeps Failing

A Price Cap Unchanged Since 2018

The structural root cause of Indonesia's recurring domestic coal supply crises sits inside the DMO pricing regime. Under the framework, coal producers are required to allocate 25% of annual production to the domestic market at government-regulated prices. The price cap for high-CV coal at GAR 6,322 kcal/kg has been fixed at US$70 per tonne since 2018, a level that has not been adjusted despite dramatic movements in global benchmark prices over the intervening eight years.

The following table illustrates the scale of the margin distortion this creates:

| Coal Grade | DMO Price Cap | HBA Benchmark | Producer Effective Margin |

|---|---|---|---|

| High-CV (GAR 6,322 kcal/kg) | US$70/tonne | ~US$124/tonne | Significantly negative vs. export |

| Medium-CV (~GAR 5,000 kcal/kg) | ~US$35-40/tonne | ~US$60/tonne | Negligible to negative |

The economics are unambiguous. A producer supplying high-CV coal into the domestic DMO market at US$70 per tonne is forgoing approximately US$54 per tonne compared with the prevailing HBA benchmark price of around US$124 per tonne. For medium-CV coal, the margin sacrifice is proportionally even more damaging in operational terms, as the DMO cap of US$35-40 per tonne against an HBA benchmark of roughly US$60 per tonne leaves producers with virtually no incentive to prioritise domestic delivery.

The DMO's pricing mechanism, as currently structured, systematically channels the most operationally critical coal grades toward the export market. Every producer rational enough to maximise returns will prioritise export allocations for their mid-CV product, which is exactly the material PLN's blending operations require. The policy creates the problem it was designed to prevent.

Industry Proposals for Reform

Two major industry bodies have advanced competing proposals to address the pricing distortion:

- Perhapi (Indonesian Mining Professionals' Association): Proposes raising the DMO price cap to US$80-90 per tonne, which would partially close the margin gap but would not eliminate the export premium entirely at current benchmark prices.

- APBI (Indonesian Coal Mining Association): Advocates for a dynamic indexation mechanism that links the DMO price to a defined percentage of the HBA benchmark price, creating automatic adjustment as market conditions change.

Neither proposal has been formally adopted, leaving the structural distortion unresolved. Without reform, the calorific value mismatch is likely to recur whenever domestic power demand tightens and producer export incentives remain dominant. Consequently, the resource export pressures felt by competing exporters may intensify further as Indonesian supply reliability continues to be questioned.

Production Quotas and the Tightening Supply Headroom

The 2026 RKAB Reduction

A compounding factor in the current supply environment is Indonesia's decision to cut its 2026 annual production quotas, known as RKABs, to approximately 600 million tonnes, down sharply from 817 million tonnes in 2025. This reduction of roughly 26.6% in permitted output has materially compressed the buffer that previously allowed producers to manage domestic supply shortfalls without sacrificing export volumes.

Output data for the first four months of 2026 reflects this constraint, with production estimated at 230-235 million tonnes, compared with a revised 250.5 million tonnes in the equivalent period of 2025. Export volumes have followed a similar trajectory, with Indonesia shipping 151.1 million tonnes of all coal types in January-April 2026, representing a 6.9% year-on-year decline.

Market participants have indicated that Indonesia may conduct a mid-year review of 2026 RKABs in July. Any upward revision would ease supply headroom but would need to be balanced against broader environmental commitments and the regulatory rationale for the original quota reduction.

The next major ASX story will hit our subscribers first

Seaborne Market Implications and Importing Nation Exposure

The decision that Indonesia rules out coal export curbs as formal policy provides important near-term clarity for seaborne buyers, but underlying vulnerabilities remain. The following table summarises the exposure profile of key importing nations:

| Importing Country | Approximate Share of Indonesian Imports | Alternative Supply Sources |

|---|---|---|

| China | ~50% | Australia, Mongolia, Russia |

| India | Significant | Australia, South Africa, Russia |

| Philippines | Moderate | Australia, Colombia |

| Malaysia | Moderate | Australia, Russia |

| South Korea | Moderate | Australia, United States |

China's position is particularly notable. Mongolia's coal production surged by 54.1% year-on-year to 46.45 million tonnes in the first five months of 2026, providing some additional supply optionality for Chinese buyers. However, Mongolia's output is predominantly coking coal rather than thermal, limiting its substitutability for power generation use. For further context on China commodity demand dynamics, shifting import strategies in Beijing are already reshaping how regional suppliers position themselves.

The El Nino weather pattern adds a near-term demand-side risk. Elevated temperatures across Asia are amplifying electricity consumption at precisely the moment when Indonesian domestic supply is under pressure, increasing the probability that PLN's 13 million tonne gap could widen rather than narrow through the peak summer period. Moreover, energy market geopolitics across the broader region continue to influence how buyers assess the reliability of any single-source supply dependency.

Frequently Asked Questions: Indonesia Coal Export Policy

Has Indonesia banned coal exports in 2026?

No. Indonesia has not imposed a formal coal export ban in 2026. The government temporarily withheld specific export shipments to address a domestic supply shortfall, but this was a targeted regulatory measure rather than a blanket prohibition. Exports have since resumed normal flows.

Why is PLN experiencing supply shortages if DMO volumes appear sufficient?

The shortage is a quality allocation problem, not a volume deficit. PLN's coal-fired plants require medium-CV coal above GAR 5,000 kcal/kg for blending purposes. The DMO pricing mechanism provides insufficient compensation for mid-CV coal, incentivising producers to direct this grade toward the export market where margins are materially higher.

What is Danantara Sumberdaya Indonesia?

It is a state-owned entity established to centralise Indonesia's coal export transactions. Its primary function is trade monitoring to prevent under-invoicing fraud, not to restrict export volumes. Analysis of coal price movements following the Danantara announcement illustrates how quickly the market interpreted monitoring measures as potential supply restrictions.

Could Indonesia reimpose a full export ban?

While no formal restrictions are planned, a significant escalation in domestic power shortages — particularly if the 13 million tonne gap widens and DMO pricing reform stalls — could increase political pressure for more interventionist measures. The 2022 ban is widely regarded as a cautionary example of the reputational and market disruption costs associated with such action.

Three Structural Reforms That Would Reduce Future Export Restriction Risk

Resolving Indonesia's recurring domestic coal supply crises requires addressing root causes rather than symptoms. Three reforms stand out as structurally necessary:

- DMO Price Reform: Adjusting the cap to reflect current market conditions, whether through a fixed increase to US$80-90 per tonne as Perhapi proposes, or through dynamic HBA indexation as APBI advocates, would materially reduce the economic incentive to divert medium-CV coal away from PLN's plants.

- Grade-Specific DMO Obligations: Introducing calorific value-differentiated DMO requirements that explicitly mandate the supply of medium-rank coal, rather than allowing producers to fulfil obligations with lower-grade material, would directly target the quality mismatch problem at its source.

- Mid-Year RKAB Flexibility: Building structured review mechanisms into the annual production quota system would allow supply headroom to be adjusted in response to domestic demand conditions without resorting to export diversions or blanket restrictions.

Indonesia's power sector will remain heavily dependent on coal-fired generation for the foreseeable future, regardless of the country's stated energy transition ambitions. That dependence makes effective DMO governance not just an administrative priority but a fundamental energy security necessity. Until the pricing architecture that governs the domestic market is reformed to reflect the economic reality faced by producers, the calorific value trap will continue to generate periodic supply crises and the market anxiety that accompanies them.

This article contains forward-looking analysis and market observations based on publicly available information. It does not constitute financial or investment advice. Commodity markets are subject to rapid change, and readers should seek independent professional guidance before making any investment or trading decisions.

Want To Stay Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, cutting through complex commodity data to surface actionable opportunities for both traders and long-term investors — explore historic discovery returns on the Discovery Alert discoveries page and begin your 14-day free trial to secure a market-leading edge.