June 27, 2026

Global metallurgical processing landscapes face unprecedented structural shifts as traditional supply-demand equations evolve beyond conventional market mechanisms. The intersection of government policy frameworks, infrastructure capacity limitations, and international trade dependencies creates complex scenarios that reshape entire industrial ecosystems. These dynamics particularly manifest in energy-intensive sectors where production quotas, environmental regulations, and technological constraints converge to challenge established operational models, with Indonesia nickel processing utilization emerging as a critical factor in global supply chain stability.

Understanding Indonesia's Nickel Processing Infrastructure Challenges

What Drives Indonesia's Processing Capacity Utilization Decline?

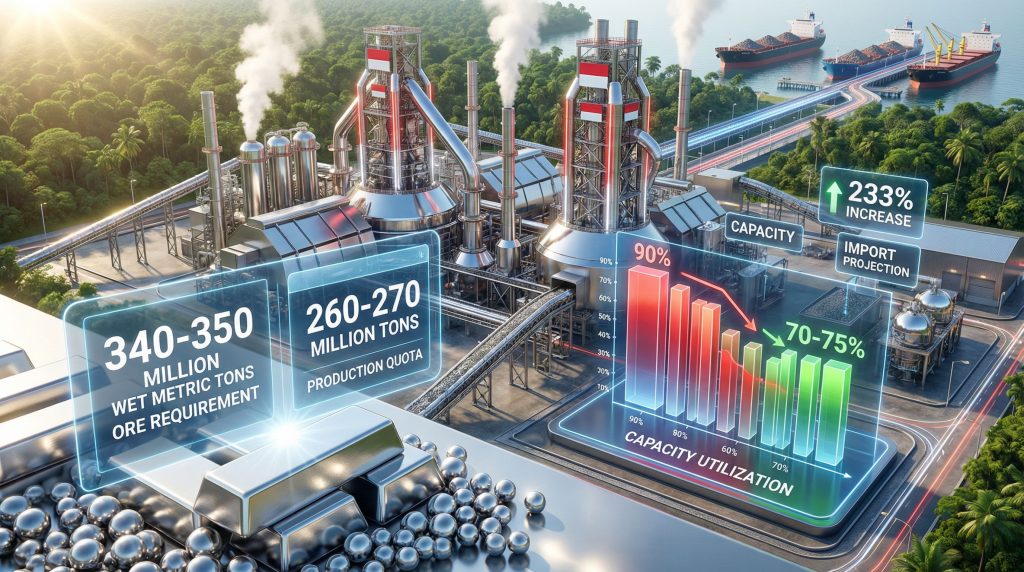

Indonesia's nickel processing sector confronts a fundamental mismatch between installed infrastructure capabilities and authorized production parameters. The nation's combined metallurgical facilities possess the technical capacity to process approximately 340-350 million wet metric tons of laterite ore annually across its 2.7 million ton processing infrastructure. However, government-mandated production quotas, known as RKAB (Rencana Kerja dan Anggaran Biaya), restrict ore extraction to 260-270 million metric tons.

This structural constraint forces Indonesia nickel processing utilization rates to decline from 90% in 2025 to an anticipated 70-75% in 2026, representing a 15-20 percentage point reduction in operational efficiency. The impact cascades through both pyrometallurgical RKEF (Rotary Kiln Electric Furnace) operations and hydrometallurgical HPAL (High Pressure Acid Leaching) facilities.

Key Infrastructure Utilization Metrics:

• Total processing capacity: 2.7 million tons annually

• Ore requirement for full utilization: 340-350 million wet metric tons

• Government production quota: 260-270 million metric tons

• Supply deficit: 70-80 million metric tons (20-23% shortfall)

• Utilization impact: 15-20 percentage point decline

The disparity reflects deliberate policy prioritisation of sustainability metrics over industrial capacity maximisation. Furthermore, industry evolution trends indicate that Energy Ministry officials view RKAB quotas as intentional environmental stewardship rather than resource availability constraints. This policy framework fundamentally alters the economic dynamics for processing companies, as fixed costs including labour, maintenance, and depreciation must be absorbed across reduced production volumes.

RKEF smelters, which convert laterite ore through high-temperature pyrometallurgy to produce ferronickel and stainless steel-grade products, face particular challenges with capacity underutilisation. These facilities require consistent high-volume throughput to maintain thermal efficiency and optimise energy consumption patterns. Reduced utilisation increases per-unit energy costs and may necessitate modified operational cycling that impacts furnace refractory lifespan.

HPAL plants, designed for battery-grade nickel sulphate production through pressure leaching technology, encounter different but equally significant constraints. These facilities process saprolite laterite ore under extreme conditions (approximately 250°C at 35+ bar pressure) and require precise chemical balance maintenance. Reduced throughput can compromise process chemistry optimisation and affect final product specifications critical for battery manufacturing applications.

How Production Quotas Create Supply-Demand Imbalances

The quota methodology employed by Indonesian authorities balances multiple competing objectives including environmental protection, resource conservation, and international trade relationships. However, this approach creates systematic supply-demand disconnects that ripple through regional and global trade impacts affecting nickel markets worldwide.

Industry representatives indicate that the timeline for experiencing acute raw material scarcity begins in Q2 2026, when accumulated inventory buffers become insufficient to maintain processing operations. This timing coincides with traditional seasonal patterns in Southeast Asian mining operations, where monsoon weather conditions historically reduce ore extraction and transportation efficiency.

Supply-Demand Imbalance Progression:

- Phase 1 (Q1 2026): Inventory drawdown from existing stockpiles

- Phase 2 (Q2 2026): Raw material scarcity emergence

- Phase 3 (Q3-Q4 2026): Full impact on processing capacity utilisation

- Phase 4 (2027+): Structural adjustment or policy modification requirements

The mathematical reality of this constraint becomes apparent through capacity analysis. Processing facilities designed for 340-350 million tons of annual ore throughput cannot achieve design efficiency with 260-270 million tons of available raw material. This creates a minimum 70-80 million ton deficit that must be addressed through alternative supply mechanisms or operational adjustments.

Price volatility patterns emerge as immediate market responses to ore availability constraints. Domestic Indonesian laterite prices experience upward pressure as processing companies compete for limited quota-allocated production. This dynamic incentivises investment in import infrastructure and supply chain diversification strategies.

When big ASX news breaks, our subscribers know first

Strategic Import Dependencies and Regional Supply Chain Shifts

Philippines as Indonesia's Primary Ore Source

The restructuring of Southeast Asian nickel ore trade flows represents one of the most significant supply chain adaptations in recent metallurgical history. Indonesia's import requirements are projected to surge from approximately 15 million metric tons in 2025 to 50 million metric tons in 2026, representing a 233% year-over-year increase that fundamentally alters regional trade balances.

The Philippines emerges as the primary alternative source, with approximately 30 million metric tons expected to flow into Indonesian processing facilities. This allocation represents 60% of total projected imports and establishes the Philippines as a critical supply chain partner for Indonesian metallurgical operations, according to recent industry analysis.

Import Surge Analysis:

| Year | Import Volume | Philippines Share | Growth Rate | Remaining Sources |

|---|---|---|---|---|

| 2025 | 15M tons | ~10M tons (67%) | – | 5M tons |

| 2026 | 50M tons | 30M tons (60%) | +233% | 20M tons |

However, Philippine ore supply flows demonstrate significant weather dependency that introduces seasonal volatility into Indonesian processing schedules. Current import volumes remain constrained to small quantities pending improved weather conditions, indicating that monsoon patterns significantly impact maritime transportation logistics.

The geological characteristics of Philippine laterite deposits offer both opportunities and challenges for Indonesian processors. Philippine ores typically exhibit different mineralogical compositions compared to Indonesian domestic laterite, requiring process parameter adjustments in both RKEF and HPAL facilities. These adaptations may affect energy consumption patterns, recovery rates, and final product specifications.

Alternative Sourcing Strategies for Indonesian Processors

Beyond Philippine supply, Indonesian processors must identify additional sources to address the remaining 20 million metric ton import requirement. Potential suppliers include Madagascar, Vietnam, New Caledonia, Solomon Islands, and smaller Pacific Island nations with laterite deposits.

Geographic diversification considerations:

• Madagascar: Large laterite reserves but limited existing export infrastructure

• Vietnam: Established mining operations with potential export capacity expansion

• New Caledonia: High-grade ore but geographically distant, increasing transportation costs

• Solomon Islands: Emerging producer with developing extraction capabilities

• Other Pacific sources: Limited individual capacity but collective potential significance

Transportation infrastructure requirements become critical success factors for sustained import operations. Indonesian ports must accommodate significantly increased ore handling volumes, requiring expansion of storage facilities, loading equipment, and inland transportation networks. The logistics premium associated with imported ore adds cost pressures that processing companies must absorb or pass through to final product pricing.

Cost-benefit analysis reveals that import dependency fundamentally alters the economic structure of Indonesian nickel processing. Domestic ore extraction costs typically range significantly below seaborne ore procurement, transportation, and handling expenses. This shift requires processing companies to optimise operational efficiency to maintain competitive positioning in global nickel markets.

Weather-dependent logistics challenges affect consistent supply flow maintenance throughout the year. Monsoon seasons impact both ore extraction at source countries and maritime transportation scheduling. Processing facilities must develop flexible inventory management strategies to accommodate seasonal supply variations.

Processing Technology Utilisation Under Capacity Constraints

RKEF Smelter Performance Optimisation

RKEF technology represents the dominant pyrometallurgical pathway for converting laterite ore into ferronickel and nickel pig iron products. These facilities subject raw ore to rotary kiln roasting at approximately 1,200°C followed by electric arc furnace smelting to achieve final product specifications. The capital-intensive nature of RKEF operations makes capacity utilisation optimisation critical for economic viability.

Under constrained ore availability scenarios, RKEF operators must implement sophisticated capacity allocation strategies that balance throughput optimisation with cost management. Reduced utilisation from 90% to 70-75% fundamentally alters the fixed cost absorption dynamics, potentially increasing per-unit production costs by 15-20% assuming linear cost relationships.

RKEF Optimisation Strategies:

• Feed quality enhancement: Implementing ore beneficiation to maximise nickel recovery per ton

• Energy efficiency improvements: Upgrading burner technology and waste heat recovery systems

• Process parameter optimisation: Adjusting temperature profiles and residence times for different ore sources

• Maintenance scheduling coordination: Aligning planned shutdowns with ore availability constraints

• Product mix optimisation: Prioritising highest-value ferronickel grades and specifications

The technical challenges of processing imported ore with different characteristics require operational flexibility that many RKEF facilities were not originally designed to accommodate. Philippine laterite may exhibit different moisture content, iron ratios, and mineralogical structures compared to Indonesian domestic ore, necessitating process modifications.

Operational efficiency improvements become essential for maintaining competitiveness under reduced utilisation scenarios. Advanced process control systems, automated material handling, and predictive maintenance technologies offer pathways to maximise output per unit of available ore while minimising operational disruptions, aligning with data-driven operations trends.

HPAL Plant Adaptation Strategies

High Pressure Acid Leaching technology processes saprolite laterite ore through pressure leaching in sulphuric acid at extreme conditions, typically around 250°C and 35+ bar pressure. HPAL plants produce intermediate nickel hydroxide or final nickel sulphate products suitable for battery manufacturing applications, commanding premium pricing compared to stainless steel-grade materials.

Battery-grade nickel production prioritisation emerges as a strategic response to capacity constraints, as higher-value products justify premium ore procurement costs and process optimisation investments. Battery-grade nickel sulphate typically commands 5-15% price premiums compared to standard industrial-grade nickel products.

HPAL process modifications for handling imported ore with different characteristics present both technical opportunities and challenges:

Technical Adaptation Requirements:

- Pressure vessel optimisation: Adjusting leaching parameters for different ore mineralogy

- Iron precipitation enhancement: Managing higher iron content in some imported ores

- Impurity removal systems: Upgrading purification processes for battery-grade specifications

- Cobalt recovery integration: Capturing cobalt byproducts for additional revenue generation

- Process water management: Optimising acid consumption and recycling systems

Integration challenges between domestic and imported ore processing require sophisticated blending strategies that maintain consistent product quality while accommodating variable feed characteristics. HPAL operators must develop expertise in handling diverse ore types without compromising process efficiency or final product specifications.

The shift toward battery-grade production aligns with green transition strategies and offers strategic positioning for Indonesian processors in higher-value market segments. However, this transition requires significant technical expertise development and potentially substantial capital investment in purification and quality control systems.

Market Impact Analysis and Price Dynamics

Nickel Ore Price Escalation Patterns

The fundamental supply-demand recalibration in Indonesian nickel ore markets creates predictable price escalation patterns that reflect both immediate scarcity and longer-term structural adjustments. Historical analysis reveals that supply constraint periods typically generate 15-25% price premiums for available ore, with additional volatility depending on seasonal factors and alternative supply availability.

Price Impact Analysis:

| Supply Constraint Level | Historical Price Impact | Duration | Recovery Pattern |

|---|---|---|---|

| 10-15% shortage | 5-10% price increase | 3-6 months | Gradual normalisation |

| 20-25% shortage | 15-25% price increase | 6-12 months | Extended adjustment |

| 25%+ shortage | 25%+ price increase | 12+ months | Structural reset |

Regional price differentials between Indonesian domestic ore and imported alternatives reflect transportation costs, quality premiums, and supply security considerations. Seaborne ore pricing typically includes freight costs ranging from $8-15 per wet metric ton depending on source location, plus handling and port charges that can add another $3-5 per ton.

Forward contract implications for processing companies become increasingly complex as price volatility increases and supply security concerns intensify. Traditional annual contract structures may prove inadequate for managing risk under highly variable supply scenarios, potentially driving industry adoption of more sophisticated hedging mechanisms.

The emergence of ore availability constraints forces processing companies to reevaluate their procurement strategies, potentially shifting from cost-optimisation approaches toward supply security prioritisation. This fundamental change in procurement philosophy has long-term implications for supplier relationships and contract structuring.

Processing Cost Structure Evolution

Fixed cost absorption challenges represent the most immediate financial impact of reduced Indonesia nickel processing utilization rates. Processing facilities with significant capital investments in equipment, infrastructure, and personnel must spread these fixed costs across reduced production volumes, creating upward pressure on per-unit costs.

Cost Structure Impact Analysis:

• Fixed costs (40-50% of total): Depreciation, labour, maintenance, insurance

• Variable costs (50-60% of total): Ore, energy, consumables, transportation

• Utilisation impact: 15-20% reduction increases unit fixed costs proportionally

• Variable cost pressure: Premium pricing for imported ore adds 10-15% to raw material costs

Variable cost increases from premium-priced imported ore compound the fixed cost absorption challenges. Processing companies face simultaneous pressure from reduced economies of scale and higher input costs, potentially creating 25-35% overall increases in production costs per unit of final product.

Competitive positioning impacts for Indonesian nickel products in global markets depend heavily on how effectively companies manage these cost pressures. Facilities that successfully optimise operations and secure cost-effective ore supply chains may gain competitive advantages, while less efficient operations face margin compression or potential viability challenges.

The evolution of processing cost structures may accelerate industry consolidation as smaller or less efficient operators struggle to maintain profitability under the new economic dynamics. This consolidation could lead to increased market concentration and potentially different competitive dynamics in global nickel markets, as highlighted in analysis of nickel industry challenges.

Industry Adaptation Scenarios and Strategic Responses

Scenario 1: Sustained Low Quota Environment

Under a sustained low quota environment, Indonesian nickel processors must develop comprehensive adaptation strategies that assume current RKAB restrictions remain in place for an extended period. This scenario requires fundamental business model adjustments and significant infrastructure investments.

Long-term adaptation requirements:

• Import infrastructure development: Expanding port facilities, storage capacity, and inland transportation networks

• Supply chain partnerships: Establishing long-term contracts with multiple ore suppliers across different geographic regions

• Technology investments: Implementing advanced ore beneficiation and process optimisation technologies

• Financial restructuring: Adjusting capital structures to accommodate higher working capital requirements and different cash flow patterns

Strategic partnerships with regional ore suppliers become critical success factors, requiring Indonesian companies to develop expertise in international mining operations, logistics coordination, and cross-border trade management. These partnerships may evolve into joint ventures or strategic investments that provide greater supply security.

Technology investments focus on maximising output per unit of available ore through improved recovery rates, enhanced ore preparation techniques, and optimised process parameters. Advanced metallurgical research and development become competitive advantages in resource-constrained environments, particularly when considering decarbonisation benefits that align with environmental regulations.

Scenario 2: Quota Normalisation Timeline

Government policy adjustment triggers could include economic pressure from reduced export revenues, industry lobbying effectiveness, or changes in environmental policy priorities. The probability and timing of quota adjustments depend on multiple political, economic, and environmental factors.

Policy modification catalysts:

- Economic impact assessment: Quantifying GDP and employment impacts from reduced processing utilisation

- Export revenue analysis: Measuring lost foreign exchange earnings from underutilised processing capacity

- Environmental compliance demonstration: Proving that increased production can meet sustainability standards

- Industry consolidation pressure: Addressing potential job losses and regional economic impacts

Industry lobbying effectiveness relies on demonstrating that processing capacity underutilisation creates economic inefficiencies without corresponding environmental benefits. This argument requires comprehensive data on energy efficiency, waste management, and environmental compliance across the processing sector.

Environmental compliance integration with production targets may offer pathways for quota increases if operators can demonstrate superior environmental performance, advanced waste management systems, or contributions to broader sustainability objectives.

Scenario 3: Alternative Processing Technology Adoption

Technological innovation pathways offer potential solutions to ore supply constraints through more efficient processing methods, alternative feedstock utilisation, or integrated recycling systems. These innovations could fundamentally alter the ore intensity requirements of Indonesian nickel processing.

Technology innovation opportunities:

• Direct reduction ironmaking (DRI) adaptations: Applying DRI technology principles to nickel laterite processing

• Hydrometallurgical process innovations: Developing more efficient acid leaching and purification methods

• Recycling integration: Incorporating battery recycling inputs to supplement primary ore requirements

• Ore beneficiation advances: Improving pre-processing to increase nickel content per ton of raw material

Recycling integration represents a particularly promising avenue as global battery adoption increases and end-of-life battery volumes grow substantially. Indonesian processors could position themselves as integrated recycling and primary production facilities, reducing dependence on mined ore while capturing value from secondary materials.

Hydrometallurgical process innovations focus on reducing energy consumption, improving recovery rates, and enabling processing of lower-grade or alternative ore types. Advanced leaching technologies, improved separation methods, and enhanced purification systems offer pathways to maintain production levels with reduced ore inputs.

Global Supply Chain Implications

Downstream Industry Impact Assessment

The constraints on Indonesia nickel processing utilization create ripple effects throughout global supply chains that depend on Indonesian nickel products. Stainless steel manufacturers, battery producers, and other downstream industries must assess supply security risks and potentially restructure their procurement strategies.

Downstream impact analysis:

| Industry Segment | Indonesian Supply Dependence | Impact Severity | Adaptation Timeline |

|---|---|---|---|

| Stainless steel | 35-40% global supply | High | 6-12 months |

| Battery chemicals | 15-20% global supply | Moderate | 12-18 months |

| Specialty alloys | 25-30% global supply | High | 3-6 months |

| Chemical applications | 20-25% global supply | Moderate | 9-12 months |

Stainless steel production faces the most immediate impact due to high dependence on Indonesian ferronickel and nickel pig iron. Major stainless steel producers may need to qualify alternative suppliers, adjust product specifications, or invest in supply chain diversification to maintain production continuity.

Battery manufacturing supply security concerns focus on nickel sulphate availability for cathode production. While Indonesian HPAL production represents a smaller share of global battery-grade nickel supply, any reduction in output contributes to broader supply tightness in rapidly growing EV markets.

Strategic metal inventory management across global value chains becomes increasingly sophisticated as supply uncertainty increases. Downstream companies may need to carry higher inventory levels, implement more complex hedging strategies, or develop alternative supplier qualifications to manage supply risk.

Competitive Landscape Shifts

Market share redistribution opportunities emerge for non-Indonesian nickel producers as processing capacity constraints create supply gaps in global markets. Producers in Australia, Canada, Russia, and other nickel-producing regions may benefit from increased demand for their products.

Competitive positioning changes:

• Australian producers: Potential market share gains in Asian stainless steel markets

• Canadian miners: Opportunities in North American and European supply chains

• Russian suppliers: Strategic positioning despite geopolitical constraints

• African projects: Accelerated development timelines for laterite projects

• Recycling operators: Enhanced economics for secondary nickel recovery

Investment attraction to alternative nickel processing jurisdictions accelerates as global buyers seek supply diversification. Countries with laterite deposits and available processing capacity may experience increased foreign investment interest and technology transfer opportunities.

Technology transfer acceleration develops as Indonesian processors seek efficiency improvements and alternative suppliers invest in capacity expansion. This knowledge transfer contributes to global processing capability development and potentially reduces long-term dependence on Indonesian supply.

The fundamental shift in competitive dynamics may persist even if Indonesian quota restrictions are eventually lifted, as supply chain diversification strategies implemented during constraint periods often become permanent risk management practices.

The next major ASX story will hit our subscribers first

Investment and Financial Market Considerations

Processing Company Valuation Impacts

Indonesia nickel processing utilization constraints create complex valuation challenges for processing companies as traditional financial metrics become less reliable under highly variable capacity utilisation scenarios. Investment analysts must develop new frameworks for evaluating companies operating under structural supply constraints.

Valuation impact factors:

• Cash flow volatility: Reduced predictability requires higher risk premiums

• Capital efficiency metrics: Traditional capacity-based valuations become misleading

• Working capital requirements: Increased inventory and receivables management complexity

• Strategic asset value: Premium for companies with secure ore supply arrangements

Cash flow projections under reduced utilisation scenarios require sophisticated modelling of variable cost structures, seasonal supply patterns, and market price volatility. Companies with flexible cost structures and diversified supply chains may command valuation premiums compared to operations dependent on domestic ore quotas.

Capital allocation priorities shift toward supply chain security investments, operational flexibility enhancements, and technology upgrades that improve ore utilisation efficiency. Traditional capacity expansion investments become less attractive until supply constraints are resolved.

Merger and acquisition opportunities arise in a consolidating market as smaller operators face viability challenges and larger companies seek to acquire strategic assets, technology capabilities, or supply chain advantages. This consolidation activity may accelerate industry restructuring.

Infrastructure Investment Requirements

The transformation of Indonesian nickel processing from domestic ore reliance to import dependency necessitates substantial infrastructure investments across multiple sectors. These investments represent both immediate operational requirements and longer-term strategic positioning initiatives.

Infrastructure development priorities:

- Import terminal capacity expansion: Upgrading port facilities to handle increased ore volumes

- Storage and handling systems: Developing covered storage for weather-sensitive operations

- Transportation network optimisation: Improving road and rail connections between ports and processing facilities

- Logistics technology integration: Implementing advanced inventory management and tracking systems

- Quality control facilities: Establishing testing and blending capabilities for diverse ore sources

Import terminal capacity expansion requires significant capital investment in specialised ore handling equipment, storage facilities, and ship unloading infrastructure. The economics of these investments depend on long-term import volume projections and utilisation assumptions.

Ore handling and storage facility development becomes critical for managing seasonal supply variations and quality consistency requirements. Covered storage facilities protect ore from weather-related degradation and enable inventory management strategies that optimise processing schedules.

Transportation network optimisation focuses on reducing logistics costs and improving supply chain efficiency for ore movement from ports to processing facilities. Infrastructure improvements may include dedicated rail lines, upgraded road connections, and automated material handling systems.

Regulatory and Policy Framework Evolution

Government Balancing Act Analysis

Indonesian policymakers navigate complex tradeoffs between economic development objectives, environmental sustainability goals, and international trade relationships. The RKAB quota system represents an attempt to balance these competing priorities, but its implementation creates unintended economic consequences that may require policy refinement.

Policy objective tensions:

• Economic development: Maximising value-added processing and export revenues

• Environmental sustainability: Managing extraction rates and ecological impacts

• Resource conservation: Preserving ore reserves for future generations

• International relations: Maintaining trade partnerships and supply chain commitments

• Industry competitiveness: Supporting Indonesian processing companies in global markets

Revenue optimisation challenges arise as reduced processing utilisation potentially decreases export revenues despite higher per-unit prices. Government analysts must evaluate whether quota restrictions achieve intended environmental benefits while minimising economic costs.

International trade relationship management becomes increasingly complex as Indonesian processors increase import dependence. Diplomatic considerations include maintaining positive relationships with ore supplier countries while managing potential trade balance impacts.

The policy framework may evolve toward more sophisticated approaches that maintain environmental protection while enabling higher processing utilisation through technology standards, efficiency requirements, or performance-based quota allocations.

Compliance and Operational Risk Management

Environmental standard enforcement during capacity optimisation periods requires careful balance between maintaining compliance and maximising productive utilisation of available resources. Processing companies must demonstrate that operational changes do not compromise environmental performance.

Compliance considerations:

• Air quality management: Ensuring emissions standards are met despite operational adjustments

• Water resource protection: Maintaining discharge quality standards with variable throughput

• Waste management systems: Properly handling waste streams from diverse ore sources

• Energy efficiency monitoring: Demonstrating responsible energy use despite reduced utilisation

• Community impact assessment: Managing local environmental and social effects

Worker safety considerations become more complex during intensive processing operations as companies attempt to maximise output from available ore supplies. Safety protocols must accommodate operational flexibility while maintaining protective standards.

Supply chain transparency requirements for imported materials may increase compliance complexity as companies source ore from multiple international suppliers with varying standards and documentation practices. Traceability systems become essential for regulatory compliance and customer requirements.

Future Outlook and Strategic Planning Considerations

Technology Development Priorities

The structural constraints on Indonesia nickel processing utilization accelerate innovation priorities as companies seek technological solutions to supply limitations. Research and development investments focus on maximising value extraction from available raw materials while improving operational efficiency.

Innovation focus areas:

• Ore beneficiation improvements: Advanced separation and concentration technologies

• Process automation systems: Reducing labour dependency and optimising operational parameters

• Environmental impact minimisation: Cleaner processing technologies and waste reduction methods

• Energy efficiency enhancements: Reducing power consumption per unit of output

• Product quality optimisation: Maximising value from processed materials

Ore beneficiation improvements enable processing companies to extract higher nickel recovery rates from lower-grade materials, effectively extending the productive capacity of available ore supplies. Advanced magnetic separation, flotation techniques, and chemical beneficiation methods offer potential efficiency gains.

Process automation reduces operational complexity while improving consistency and efficiency under variable supply conditions. Automated systems can optimise processing parameters in real-time, adjust for ore quality variations, and minimise waste generation.

Environmental impact minimisation technologies support policy compliance while potentially enabling quota increases for operators who demonstrate superior environmental performance. Clean processing innovations may provide competitive advantages in regulatory environments.

Market Positioning Strategies

Product mix optimisation becomes essential for maintaining profitability under capacity constraints as companies focus production on highest-value applications and customer segments. Strategic positioning requires deep understanding of market dynamics and customer requirements across different end-use industries.

Strategic positioning elements:

- Premium product development: Focusing on battery-grade and specialty applications

- Customer relationship management: Maintaining supply commitments during constrained periods

- Long-term contract optimisation: Balancing price and volume risk management

- Market diversification: Reducing dependence on single customer segments or geographic markets

- Value-added services: Providing technical support and customised solutions

Customer relationship management during supply constraint periods requires transparent communication, fair allocation systems, and collaborative problem-solving approaches. Strong customer relationships may provide competitive advantages when supply normalises.

Long-term contract structuring becomes more sophisticated as both suppliers and customers seek to manage increased price and volume volatility. Contract innovations may include flexible volume terms, price adjustment mechanisms, and supply security provisions.

Market diversification strategies reduce single-point-of-failure risks by developing customer bases across multiple industries, geographic regions, and application segments. Diversification provides resilience against sector-specific demand variations.

Critical Success Factors

Indonesian processors must simultaneously optimise existing capacity utilisation, secure reliable import supply chains, and invest in technology improvements to maintain global market leadership during this transitional period.

Long-term Competitive Positioning

Innovation investment priorities for next-generation processing efficiency focus on technologies that provide sustainable competitive advantages beyond the current supply constraint period. Companies that successfully navigate current challenges while building future capabilities may emerge stronger in normalised markets.

Competitive advantage development:

• Operational excellence: Superior efficiency and cost management capabilities

• Supply chain mastery: Expertise in managing complex, multi-source procurement

• Technology leadership: Advanced processing capabilities and innovation capacity

• Market intelligence: Deep understanding of global supply-demand dynamics

• Financial resilience: Strong balance sheets capable of weathering volatility

Regional partnership development for supply chain security creates strategic alliances that extend beyond current supply constraints. These partnerships may evolve into integrated supply chain networks providing long-term competitive advantages.

Market diversification strategies that reduce single-point-of-failure risks include geographic expansion, product portfolio broadening, and vertical integration opportunities. Companies with diverse revenue streams demonstrate greater resilience to market disruptions.

The current period of reduced Indonesia nickel processing utilization serves as a catalyst for industry transformation that may produce more efficient, flexible, and resilient processing operations. Companies that successfully adapt may find themselves better positioned for long-term success even after supply constraints are resolved.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and available information. Actual results may vary significantly due to changing regulatory environments, market dynamics, technological developments, and other factors beyond current visibility. Investors and industry participants should conduct independent analysis and consider multiple scenarios when making strategic decisions.

Ready to Invest in the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.