July 16, 2026

The Geological Coincidence That Became a Trade Strategy

Not every supply chain partnership begins in a boardroom. Some begin in the earth itself, in the precise chemical composition of ore deposits laid down millions of years ago. The Indonesia Philippines nickel cooperation agreement, formalised in May 2026, is arguably one of those rare cases where geology has written the first draft of trade policy, and human institutions are only now catching up.

Understanding why these two nations are formalising what the market has long suggested makes sense requires looking beyond headlines about trade deals and examining the underlying mineralogical reality, the industrial bottlenecks, and the shifting geopolitical architecture that together make this agreement both logical and strategically significant. Furthermore, the Indonesian nickel industry challenges that have shaped domestic policy are central to understanding this emerging partnership.

When big ASX news breaks, our subscribers know first

What the Indonesia-Philippines Nickel Cooperation Agreement Actually Is

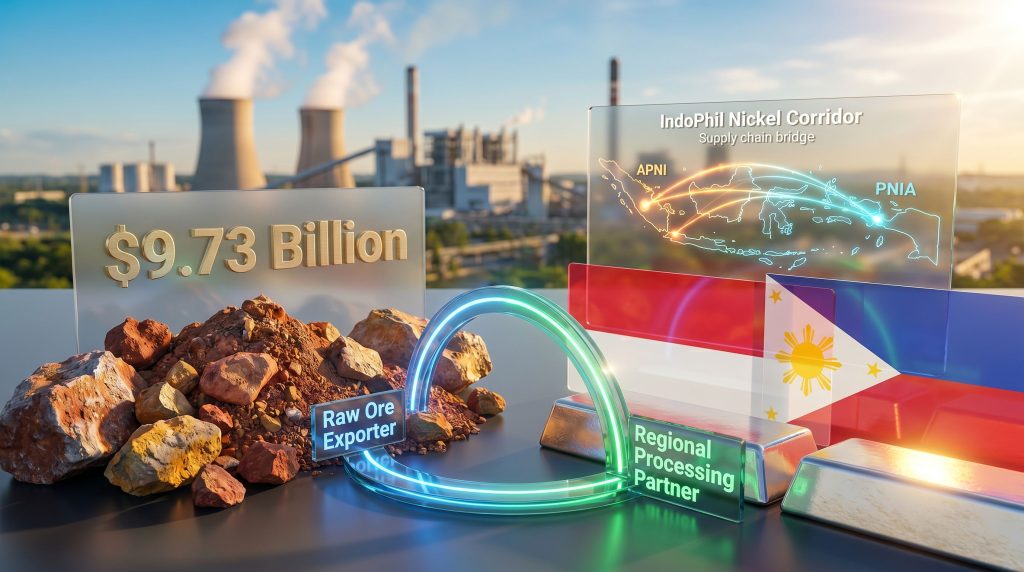

On May 8, 2026, the Indonesian Nickel Miners Association (APNI) and the Philippine Nickel Industry Association (PNIA) signed a memorandum of understanding on nickel cooperation, with the signing witnessed by Indonesia's chief economics minister Airlangga Hartarto and the Philippines' trade and industry minister Cristina Roque. The event was reported by Reuters and published through Mining.com.

The agreement, according to Indonesia's coordinating ministry of economics, covers three core areas:

- Exchange of information between industry associations

- Joint development of nickel downstream processing technology

- Human resource development to support a sustainable regional nickel industry ecosystem

What makes this framework structurally unusual is its deliberate positioning as a business-to-business arrangement between industry associations rather than a formal government-to-government trade agreement. No fixed ore import volumes are stipulated. No government procurement commitments are formalised. The flexibility this creates is intentional, allowing the framework to adapt to shifting market conditions without requiring diplomatic renegotiation every time commercial circumstances change.

The Silicon-to-Magnesium Problem: A Geological Explanation Most Articles Miss

The technical heart of this agreement lies in a specific metallurgical challenge that receives surprisingly little attention in mainstream coverage of the Indonesia Philippines nickel cooperation agreement.

Indonesia's network of nickel smelters, which underpins a downstream processing industry that generated $9.73 billion in nickel product exports in the year preceding the May 2026 agreement, does not simply need any nickel ore. It needs ore with a specific silicon-to-magnesium ratio to operate efficiently.

This technical requirement matters enormously and here is why:

Laterite nickel deposits, which dominate the ore geology of both Indonesia and the Philippines, are not homogeneous. They contain varying concentrations of silica (SiO2), magnesium oxide (MgO), iron (Fe), and nickel (Ni) depending on their weathering profile. In the processing of laterite ore through rotary kiln electric furnace (RKEF) technology, which is the dominant smelting method used in Indonesian facilities, the silicon-to-magnesium ratio in the feedstock directly affects:

- Slag chemistry and fluidity during smelting

- Energy consumption per tonne of output

- Refractory lining wear rates inside furnaces

- Nickel recovery efficiency from ore to metal

If the Si/Mg ratio falls outside the optimal operating window for a given furnace configuration, smelter operators face increased energy costs, reduced metal recovery, and accelerated equipment degradation. This is not a minor inconvenience but a meaningful operating cost variable at industrial scale.

Philippine laterite deposits, particularly in the country's major nickel-producing provinces, contain ore compositions that are well-suited to meeting the Si/Mg specifications that Indonesian smelters require, as confirmed by Indonesia's chief economics minister Airlangga Hartarto at the May 2026 signing ceremony.

This compositional complementarity is not coincidental but reflects the distinct geological evolution of the two archipelago nations, whose ore bodies developed under different weathering and depositional conditions despite their geographic proximity.

Why Indonesia Needs Philippine Ore Despite Being a Dominant Producer

A question worth examining carefully is why the world's largest nickel producer requires ore from a neighbouring country at all. The answer reveals a structural tension within Indonesia's resource economy that rarely receives adequate attention.

Indonesia's aggressive push to ban raw nickel ore exports and mandate domestic downstream processing has been enormously successful in generating processing industry investment. The result is a rapidly expanding smelter network that has, in some periods, outpaced the growth of domestic ore supply that meets smelter-specific compositional requirements.

Indonesia's domestic nickel reserves are vast, but individual ore bodies vary significantly in their chemistry. Not every deposit produces ore with the Si/Mg characteristics that all smelter configurations can accommodate efficiently. When domestic ore that meets specific smelter specifications becomes constrained, whether through licensing delays, logistical bottlenecks, or geological variability at operating mines, the economic cost of operating on suboptimal feedstock is substantial.

The Philippines fills a gap that is compositional, not just volumetric. This distinction is critical for understanding the strategic value of the Indonesia Philippines nickel cooperation agreement. Indonesia is not seeking additional ore simply because it lacks quantity. It is seeking ore that meets specific quality parameters its smelter infrastructure depends on. In addition, Indonesian nickel market trends point to sustained feedstock demand pressure as smelter capacity continues to expand.

Repositioning the Philippines: From Raw Ore Exporter to Regional Processing Partner

The Philippines has historically occupied the least profitable position in the global nickel value chain. Large volumes of laterite ore have been excavated and exported with minimal processing, leaving the country exposed to commodity price volatility while capturing almost none of the premium margins available further along the processing chain.

The table below illustrates how the cooperation framework is designed to shift that positioning over time:

| Dimension | Philippines Before May 2026 | Intended Post-Agreement Trajectory |

|---|---|---|

| Primary role | Raw ore exporter | Regional supply chain participant |

| Value capture | Extraction margin only | Integration into mid-chain processing |

| Technology access | Limited domestic capability | Joint development with Indonesian partners |

| Workforce focus | Mining operations | Expanding toward processing and refining |

| ESG benchmarking | Variable and fragmented | Aligned with regional industry standards |

Airlangga Hartarto articulated the directional intent clearly at the signing ceremony: the Philippines is being positioned to transition beyond raw ore exports and into meaningful participation in a higher-value regional supply chain, while Indonesia simultaneously secures reliable, compositionally appropriate feedstock for its battery and stainless steel industries.

This reframing of the relationship from supplier-buyer to integrated regional partners is the most commercially significant aspect of the agreement. The technology transfer and human resource development components are the mechanisms through which this repositioning is intended to occur, building the technical workforce and processing knowledge base within the Philippines that would eventually support domestic value-adding operations.

The Broader Strategic Architecture: ASEAN, EV Demand, and Supply Chain Repatriation

The Indonesia Philippines nickel cooperation agreement does not exist in isolation. It sits within a broader regional movement to capture greater economic value from Southeast Asia's mineral endowments rather than exporting that value to external processing intermediaries.

Several intersecting forces are accelerating this dynamic:

Electric Vehicle Battery Demand

Nickel is a primary input in NMC (nickel-manganese-cobalt) battery chemistries used in electric vehicles. As global EV adoption accelerates, demand for battery-grade nickel processed to high-purity specifications creates a sustained long-term growth driver for the entire regional processing chain. This demand is further reinforced by battery storage expansion continuing to reshape energy infrastructure investment globally.

Stainless Steel Stability

The stainless steel sector, which consumes the majority of current global nickel production in the form of nickel pig iron, provides a stable baseline demand floor that underpins the economics of Indonesian smelter operations regardless of battery market growth trajectories.

Value Chain Repatriation

A significant portion of value created from Southeast Asian nickel has historically been captured by processing operations outside the ASEAN production zone. A more integrated Indonesia-Philippines supply corridor, if successfully implemented, represents a structural mechanism for retaining more of that value within the region. Consequently, the role of nickel in the energy transition adds further long-term strategic weight to this repatriation effort.

The next major ASX story will hit our subscribers first

Key Risks and Implementation Realities

Understanding the Indonesia Philippines nickel cooperation agreement requires clear-eyed assessment of the obstacles that could constrain its ambitions.

Regulatory Asymmetry

Indonesia and the Philippines operate under distinct mining licensing, environmental permitting, and export regulation frameworks. Harmonising commercial practices across these different regulatory environments will require sustained dialogue and, in some cases, parallel policy adjustments in both jurisdictions.

B2B Model Limitations

The deliberate choice of an industry-association framework, while providing commercial flexibility, also limits enforcement mechanisms. If disputes arise between commercial parties operating under the corridor framework, resolution pathways are less clearly defined than they would be under a government-to-government treaty structure.

Chinese Industrial Stakeholder Dynamics

A substantial portion of Indonesia's existing nickel smelter infrastructure involves Chinese industrial investment. How a Philippines-Indonesia ore supply corridor interacts with existing Chinese procurement relationships and supply chain preferences within those facilities remains an open and commercially complex question.

ESG and Responsible Sourcing Standards

International buyers, particularly those supplying EV manufacturers with formal sustainability commitments, are applying increasingly rigorous responsible sourcing standards to battery material supply chains. Both Indonesian and Philippine nickel operations face scrutiny over environmental and community impact practices. The agreement's human resource and sustainability capacity-building elements address this partially, but implementation timelines for meaningful ESG standards alignment are not yet defined.

Ore Quality Consistency

Maintaining the Si/Mg ratio specifications that Indonesian smelters require demands consistent geological quality control across Philippine mining operations. Natural geological variability and inconsistent sampling or blending practices could create operational friction even where commercial intent is strong.

Comparing the IndoPhil Model to Other Critical Minerals Partnerships

The architecture of the Indonesia Philippines nickel cooperation agreement is distinctive when benchmarked against comparable regional and bilateral frameworks:

| Partnership | Commodity Focus | Agreement Type | Structure |

|---|---|---|---|

| Indonesia-Philippines (IndoPhil Corridor) | Nickel | MOU + Industry Pact | B2B (industry associations) |

| Australia-Japan Critical Minerals Partnership | Lithium, rare earths, nickel | Government framework | G2G |

| ASEAN Critical Minerals Framework (proposed) | Multiple | Multilateral | Intergovernmental |

The industry-association model prioritises commercial agility. It can respond to market shifts, smelter technology changes, and ore quality requirements without requiring formal diplomatic renegotiation. However, this same flexibility means the corridor lacks the enforcement weight that government-backed frameworks carry, which matters significantly when substantial capital investment decisions depend on supply security guarantees. For those assessing the broader battery metals investment landscape, these structural distinctions carry real implications for risk assessment.

Market Implications: What Investors and Industry Observers Should Watch

For those tracking nickel markets, the Indonesia Philippines nickel cooperation agreement signals several dynamics worth monitoring.

Near-Term Considerations (2026 to 2028)

- The agreement creates no immediate large-scale volume commitments, so near-term market impact on nickel pricing should be considered minimal

- Incremental stabilisation of feedstock supply to specific Indonesian smelter facilities is the most realistic near-term outcome

- Framework implementation pace will depend heavily on whether the B2B model generates genuine commercial transactions or remains aspirational

Longer-Term Structural Possibilities (2028 and Beyond)

- Successful technology transfer could position the Philippines as a secondary processing hub within Southeast Asia's nickel value chain

- A more integrated regional supply corridor could reduce the leverage of single-nation supply disruptions on global nickel pricing

- If the model proves effective, it could serve as a template for broader ASEAN critical minerals integration across cobalt, manganese, and other battery-relevant materials

Furthermore, as reported by Antara News, Indonesian officials have explicitly framed the corridor as a potential model for wider ASEAN critical minerals cooperation, adding a layer of geopolitical significance beyond its immediate commercial purpose.

Disclaimer: The market projections and scenario analyses above represent analytical assessments based on publicly available information and should not be construed as financial advice. Commodity markets are subject to significant uncertainty, and actual outcomes may differ materially from projections.

Frequently Asked Questions

What is the Indonesia-Philippines nickel cooperation agreement?

It is a memorandum of understanding signed on May 8, 2026, between APNI and PNIA, witnessed by senior ministers from both nations. It covers information exchange, joint downstream processing technology development, and human resource capacity building.

Is this a government-to-government trade deal?

No. The cooperation framework operates as a business-to-business arrangement between industry associations. No formal government-to-government nickel trade commitments have been confirmed as part of this framework.

Why does Indonesia need Philippine nickel ore?

Indonesian smelters require feedstock with specific silicon-to-magnesium ratios to operate efficiently. Philippine laterite deposits are compositionally well-suited to meeting this requirement, creating a natural supply complementarity that domestic Indonesian ore does not always fully satisfy.

How significant is Indonesia's nickel processing industry?

Indonesia generated approximately $9.73 billion in nickel product exports in the year preceding the agreement, reflecting the substantial scale of its downstream processing operations and the economic importance of consistent, quality-appropriate ore supply.

What does this mean for the Philippines?

The agreement creates a framework through which the Philippines can progressively transition from raw ore exporter toward participation in higher-margin processing activities through technology sharing, joint development programmes, and workforce capability building with Indonesian industry partners.

How does this relate to the EV battery supply chain?

Nickel is a critical input in the battery chemistries powering electric vehicles. A more stable and integrated Indonesia-Philippines supply corridor supports feedstock predictability for smelters producing battery-grade nickel, with relevance to both the energy transition and traditional industrial demand sectors.

What the Agreement Signals Beyond Its Immediate Scope

The Indonesia Philippines nickel cooperation agreement is significant not primarily because of the specific commercial commitments it contains, which are relatively modest in scope, but because of what it represents structurally. Two nations whose nickel industries have historically operated in parallel rather than in coordination are now formalising a framework for genuine supply chain integration, driven by the precise technical requirements of industrial processing rather than abstract diplomatic ambition.

The $9.73 billion scale of Indonesia's nickel export economy creates powerful commercial incentives to secure compositionally appropriate feedstock. The Philippines' vast laterite reserves, largely unprocessed at scale, represent an untapped value creation opportunity that integration with Indonesian smelter technology could begin to unlock. The geology made this partnership logical. The industry associations have made it institutional. Whether commercial implementation follows at meaningful scale will determine whether the IndoPhil Nickel Corridor becomes a genuinely transformative structure in Southeast Asia's critical minerals landscape.

Want To Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly translating complex mineral data into actionable investment insights across nickel, battery metals, and over 30 other commodities — exactly the kind of intelligence that matters when supply chain shifts like the IndoPhil Nickel Corridor begin reshaping market dynamics. Explore how historic mineral discoveries have generated substantial returns and start your 14-day free trial today to position yourself ahead of the market.