June 14, 2026

Industrial Decarbonisation and the Steel Sector's Carbon Challenge

Industrial decarbonisation faces a fundamental challenge: transforming energy-intensive manufacturing processes that have relied on fossil fuels for over a century. The steel industry, responsible for approximately 7% of global carbon emissions, represents one of the most complex puzzles in this transition. Traditional steelmaking has been constrained not only by its dependence on coal-coke chemistry but also by strict requirements for premium iron ore grades that limit both supply flexibility and geographic production options.

The recent hydrogen-based iron-ore-to-green-steel breakthrough in Namibia demonstrates how technological innovation can simultaneously address multiple industrial constraints. By enabling the processing of lower-grade iron ores through hydrogen direct reduction, this development fundamentally alters the economics of green steel production and expands the global resource base available for climate-neutral manufacturing. Furthermore, this breakthrough aligns with broader mining decarbonisation trends reshaping the industry landscape.

When big ASX news breaks, our subscribers know first

Understanding the Industrial Carbon Challenge in Modern Steel Manufacturing

Steel production represents one of the most carbon-intensive industrial processes globally, with the sector accounting for approximately 7% of worldwide CO₂ emissions. This substantial environmental footprint stems from the traditional reliance on coal-coke chemistry for iron ore reduction, a process that has defined steelmaking for over 150 years.

The conventional steelmaking process requires several energy-intensive steps that compound the carbon challenge:

- Coal coking operations that convert coal into metallurgical coke

- High-temperature blast furnace reduction requiring sustained temperatures above 1,500°C

- Limestone flux addition for impurity removal, releasing additional CO₂

- Secondary steelmaking processes for alloy adjustment and purification

These interconnected processes create what industry analysts describe as a "carbon lock-in" effect, where the entire production system has been optimised around fossil fuel inputs over decades of incremental improvement.

Economic Pressures Driving Decarbonisation

Beyond environmental considerations, steel producers face mounting economic pressure to reduce carbon intensity. Carbon pricing mechanisms across major markets are creating direct cost penalties for high-emission production methods. The European Union's Carbon Border Adjustment Mechanism, for instance, will impose tariffs on carbon-intensive steel imports, fundamentally altering global trade dynamics in the sector.

Additionally, major steel consumers in automotive and construction sectors are increasingly demanding low-carbon materials to meet their own sustainability commitments. This demand shift creates premium pricing opportunities for producers capable of delivering verified low-carbon steel products. These decarbonisation economic benefits are driving industry transformation across multiple sectors.

Traditional Process Limitations

The conventional steel production pathway imposes significant constraints on both resource utilisation and operational flexibility. Traditional blast furnace operations require iron ore with iron content typically exceeding 70% to achieve efficient reduction. These premium ores are geographically concentrated and command significant price premiums due to their scarcity.

Furthermore, conventional processes mandate energy-intensive pelletising of iron ore before reduction, adding both capital and operational costs to the production chain. This preprocessing requirement limits the types of ore deposits that can be economically processed and restricts production location options.

Hydrogen Direct Reduction: Redefining Steel Production Chemistry

Hydrogen-based direct reduction represents a fundamental departure from traditional steelmaking chemistry. Instead of using carbon monoxide from coal combustion to strip oxygen from iron ore, this process employs hydrogen gas as the reducing agent, producing water vapour rather than carbon dioxide as the primary byproduct.

Technical Process Innovation

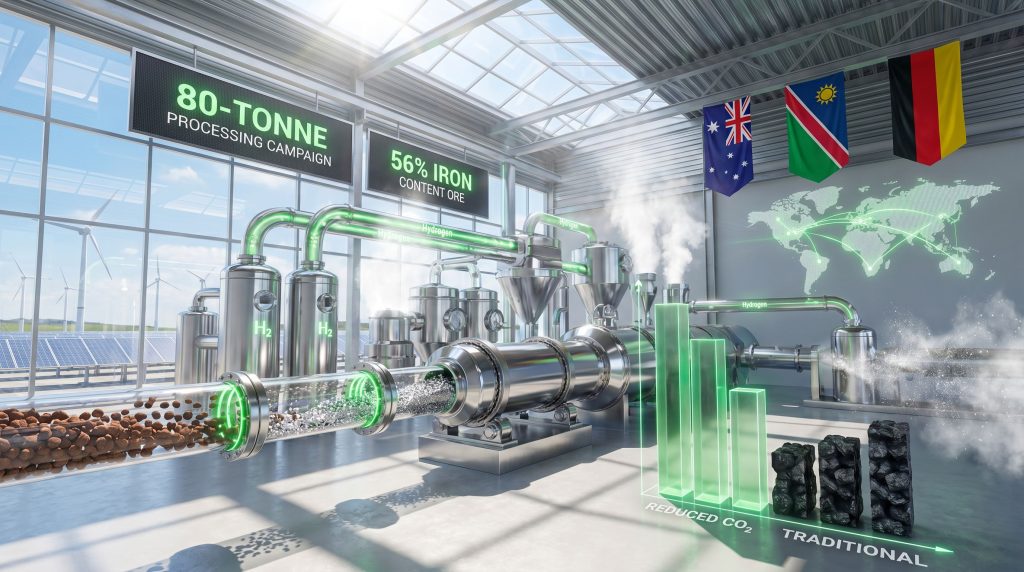

The hydrogen direct reduction process centres on an electrically powered rotary kiln that maintains precise temperature and atmosphere control. Recent industrial pilots have demonstrated successful processing of 80 tonnes of Australian iron ore with 56% iron content at throughput rates of 5 tonnes per hour.

This approach delivers several technical advantages over conventional methods:

| Process Factor | Traditional Method | Hydrogen Reduction | Operational Benefit |

|---|---|---|---|

| Ore Grade Requirement | 70%+ iron content | 56%+ iron content | 20% resource base expansion |

| Preprocessing | Mandatory pelletising | Direct processing | 15-25% capital cost reduction |

| Primary Byproduct | CO₂ emissions | Water vapour | Near-zero carbon output |

| Energy Source | Coal/coke combustion | Renewable electricity | Price stability and scalability |

| Furnace Configuration | Shaft furnace design | Rotary kiln operation | Enhanced operational flexibility |

Energy Integration Advantages

Hydrogen direct reduction enables integration with renewable energy systems in ways impossible with conventional steelmaking. The process can utilise hydrogen produced via electrolysis powered by solar or wind resources, creating a pathway for steel production in regions with abundant renewable energy but limited coal resources.

The electrically powered rotary kiln design also allows for more precise temperature control and energy efficiency optimisation compared to coal-fired blast furnaces. This precision translates into improved metallurgical outcomes and reduced energy consumption per tonne of steel produced.

Quality and Specification Achievement

Industrial pilot campaigns have demonstrated that hydrogen-reduced iron achieves metallurgical specifications comparable to traditional blast furnace output. The direct-reduced iron (DRI) produced through hydrogen reduction can be seamlessly integrated into existing electric arc furnace operations for final steel production.

This compatibility ensures that hydrogen-based production can leverage existing steelmaking infrastructure in downstream processes, reducing the total capital investment required for technology adoption.

Lower-Grade Ore Processing: Expanding Global Resource Accessibility

The ability to process iron ore with 56% iron content rather than the traditional 70%+ requirement represents a paradigm shift in resource utilisation. This 14 percentage point expansion in acceptable ore grades dramatically increases the global reserve base available for steel production.

Geographic Resource Distribution

Lower-grade iron ore deposits are far more widely distributed globally than premium deposits. While high-grade ores are concentrated in specific geological formations in Australia, Brazil, and select other regions, moderate-grade deposits exist across multiple continents and geological settings.

This geographic diversity offers several strategic advantages:

- Supply chain risk reduction through diversified sourcing options

- Transportation cost optimisation by enabling processing closer to end markets

- Regional industrial development in areas previously excluded from steel production

- Resource sovereignty enhancement for nations lacking premium ore deposits

Economic Impact of Ore Grade Expansion

Processing lower-grade ores eliminates the necessity for energy-intensive pelletising operations that traditional methods require. Pelletising typically accounts for 15-20% of total production costs in conventional steelmaking and requires significant capital investment for specialised equipment.

The elimination of pelletising delivers multiple economic benefits:

- Capital cost reduction of $50-100 million per facility

- Energy consumption decrease of 200-300 kWh per tonne of steel

- Operational complexity reduction through process simplification

- Maintenance cost savings from fewer mechanical systems

Resource Valuation Transformation

The ability to economically process 56% iron content ore fundamentally alters the valuation of iron ore deposits worldwide. Mining operations that were previously marginal or uneconomical due to ore grade limitations may become viable development prospects.

This shift creates opportunities for Australia green metals development and regional expansion of processing capabilities.

Strategic Multi-National Partnership Models in Green Steel Development

The development of hydrogen-based steel production requires coordination across multiple geographic regions and industrial capabilities. The Australia-Namibia-Germany corridor demonstrates how strategic partnerships can optimise resource access, processing capabilities, and end-market integration.

Consortium Structure and Capabilities

The SuSteelAG consortium integrates 8+ specialised organisations across three continents, each contributing distinct capabilities to the value chain:

Resource and Technology Providers:

- Fortescue (Australia): Iron ore supply and mining expertise

- TS Elino GmbH (Germany): Rotary kiln design and manufacturing

- HyIron Green Technologies: Hydrogen processing facility operations

- BAM (Germany): Materials research and process optimisation

Research and Development Partners:

- RWTH Aachen University: Advanced mineral processing research

- Fraunhofer Institute IST: Surface engineering and thin films

- Fraunhofer Institute IKTS: Ceramic technologies and systems

- Salzgitter Mannesmann Forschung: Steel production integration

Infrastructure and Logistics:

- Hansaport (Germany): Maritime logistics and handling

- Heidelberg Manufacturing (Germany): Industrial equipment

Geographic Optimisation Strategy

The three-region model optimises each location's competitive advantages:

Australia: Premium iron ore resources and established mining infrastructure enable efficient raw material extraction and initial processing. Australia's mining sector expertise and existing logistics networks provide a reliable foundation for resource supply.

Namibia: Abundant solar resources and strategic geographic positioning enable cost-effective hydrogen production and intermediate processing. The country's renewable energy potential allows for climate-neutral processing operations at scale.

Germany: Advanced manufacturing capabilities and proximity to major automotive markets enable efficient integration into existing industrial processes and end-product manufacturing.

Technology Transfer and Knowledge Integration

The partnership model facilitates technology transfer across multiple jurisdictions while maintaining intellectual property protection. German industrial furnace expertise, Australian mining knowledge, and African renewable energy resources combine to create capabilities that no single nation could develop independently.

This knowledge integration extends to:

- Process optimisation through combined research capabilities

- Operational best practices sharing across facilities

- Regulatory compliance coordination across multiple jurisdictions

- Market development strategies for global steel markets

Investment and Risk Sharing Framework

The consortium structure enables risk distribution across multiple partners and geographic regions. The €4.5 million in funding from German research programmes demonstrates how government research support can leverage private sector investment to advance strategic technologies.

This funding model combines:

- Public research grants for technology development

- Private sector investment in infrastructure and operations

- Bilateral cooperation agreements between participating nations

- Industry partnership arrangements for market development

Renewable Energy Geography and Processing Location Economics

The selection of Namibia as the processing location for the hydrogen-based steel pilot demonstrates the critical importance of renewable energy geography in determining optimal production sites. Namibia's abundant solar resources provide a foundation for cost-competitive hydrogen production that enables climate-neutral steel processing.

Solar Resource Advantages in Southern Africa

Namibia's location in the Namib Desert region provides exceptional solar irradiance levels that approach theoretical maximums for photovoltaic energy generation. This geographic advantage enables solar electricity production at costs that make electrolytic hydrogen production economically viable for industrial applications.

The combination of high solar irradiance, low land costs, and stable political conditions creates an ideal environment for large-scale renewable hydrogen projects. These factors position Namibia as a potential hub for green hydrogen production serving both domestic industrial applications and export markets.

Processing Location Strategy Analysis

The decision to locate processing operations in Namibia rather than at the ore source (Australia) or end market (Germany) reflects complex economic calculations involving:

Energy Cost Considerations:

- Renewable electricity costs in Namibia significantly below Australian or German levels

- Hydrogen production costs optimised through abundant solar resources

- Industrial electricity rates favourable for energy-intensive processing

Transportation Economics:

- Shipping costs for direct-reduced iron competitive with raw ore transport

- Reduced shipping volume through processing concentration

- Strategic positioning for both Atlantic and Indian Ocean markets

Infrastructure Development:

- Lower capital costs for industrial facility development

- Access to port facilities for international shipping

- Regulatory environment supportive of industrial development

Grid Integration and Energy Storage

Large-scale hydrogen production requires consistent electricity supply that may exceed the capacity of existing grid infrastructure in developing regions. The Oshivela facility's operations demonstrate how industrial hydrogen production can be integrated with renewable energy systems through:

- Direct solar-to-electrolyser connections bypassing grid constraints

- Industrial-scale energy storage for production smoothing

- Grid-interactive operations that support local electricity networks

- Hybrid energy systems combining multiple renewable sources

Regional Industrial Development Implications

The establishment of hydrogen-based processing facilities creates opportunities for broader industrial development in renewable energy-rich regions. Beyond steel processing, hydrogen production infrastructure can support:

- Ammonia production for fertiliser manufacturing

- Chemical processing operations requiring hydrogen inputs

- Fuel cell vehicle infrastructure development

- Green hydrogen export to international markets

This diversification potential enhances the economic viability of renewable energy infrastructure investment and creates multiple revenue streams for project developers. Moreover, these developments reflect broader mining industry evolution towards sustainable technologies.

The next major ASX story will hit our subscribers first

Market Transformation and Competitive Dynamics in Global Steel

The successful demonstration of hydrogen-based steel production using lower-grade ores creates potential for significant disruption in global steel market dynamics. Traditional competitive advantages based on access to premium ore or low-cost coal may diminish as renewable energy and technology access become determining factors.

Competitive Position Shifts for Steel Producers

The technology breakthrough enables competitive steel production in regions previously excluded due to resource constraints. Countries with abundant renewable energy but limited coal or premium iron ore resources can potentially develop domestic steel industries for the first time.

This geographic expansion of viable steel production creates several competitive implications:

Emerging Market Opportunities:

- African nations with solar resources can develop steel processing capabilities

- Middle Eastern countries can leverage renewable energy for steel production

- Latin American regions can process local iron ore resources domestically

- Asian markets can reduce dependence on imported premium ores

Traditional Producer Challenges:

- Coal-dependent facilities face increasing carbon cost disadvantages

- Premium ore miners may experience demand moderation

- Integrated steel producers require technology transition strategies

- Transportation-dependent supply chains become less competitive

Premium Pricing for Low-Carbon Steel

Major steel consumers, particularly in automotive manufacturing, are increasingly willing to pay premiums for verified low-carbon steel products. This demand shift creates market opportunities for early adopters of hydrogen-based production technology.

Industry analysis suggests potential premium pricing of 10-15% for certified green steel in automotive applications, with premiums potentially reaching 20-25% for specialised applications requiring carbon footprint verification.

Supply Chain Reconfiguration

The ability to process lower-grade ores closer to renewable energy sources enables supply chain reconfiguration that reduces transportation costs and carbon footprints. Regional steel production clusters may emerge around renewable energy resources rather than traditional coal or port locations.

This reconfiguration creates opportunities for:

- Nearshoring of steel production to reduce supply chain risks

- Regional industrial integration between steel and manufacturing

- Transportation cost reduction through proximity to end markets

- Carbon footprint minimisation across entire value chains

Technical Scalability and Commercial Deployment Pathways

The successful 80-tonne pilot campaign at Oshivela provides crucial validation for the commercial viability of hydrogen-based steel production. Operating at 5 tonnes per hour throughput, the facility demonstrates that the technology can achieve industrial-relevant scale while maintaining product quality and economic efficiency.

Pilot Performance Validation

The pilot campaign achieved several critical technical milestones that validate commercial scalability:

Process Reliability:

- Continuous operation at design throughput rates

- Consistent product quality meeting steel industry specifications

- Stable hydrogen consumption and energy efficiency metrics

- Successful processing of untreated 56% iron content ore

Operational Efficiency:

- Direct reduction without mandatory pelletising requirements

- Climate-neutral processing with water vapour as primary byproduct

- Integration with renewable energy systems for hydrogen supply

- Successful operation of electrically powered rotary kiln design

Commercial Scale Development Requirements

Scaling from the 5-tonne-per-hour pilot to commercial production requires systematic capacity expansion while maintaining process efficiency. Commercial steel facilities typically operate at scales of 100-500 tonnes per hour, requiring significant infrastructure investment and operational optimisation.

Capital Investment Analysis:

| Scale Factor | Pilot (5 t/hr) | Commercial (200 t/hr) | Investment Multiple |

|---|---|---|---|

| Rotary Kiln | Single unit | Multiple parallel units | 25-35x |

| Hydrogen Supply | Local production | Industrial-scale electrolysis | 40-50x |

| Power Infrastructure | Grid connection | Dedicated renewable capacity | 30-40x |

| Processing Equipment | Laboratory-scale | Industrial automation | 20-30x |

Technology Licensing and Intellectual Property

The consortium's research and development investments create valuable intellectual property around rotary kiln design, process optimisation, and ore preparation techniques. Technology licensing models could enable global deployment while providing returns to consortium members.

Potential licensing structures include:

- Equipment licensing for rotary kiln and processing technology

- Process licensing for operational parameters and optimisation

- Regional franchising for specific geographic markets

- Joint venture partnerships for facility development and operation

Regulatory Approval and Certification

Commercial deployment requires regulatory approvals across multiple jurisdictions for industrial operations, environmental compliance, and product certification. The pilot success provides regulatory precedent that can accelerate approval processes for subsequent facilities.

Key regulatory considerations include:

- Environmental impact assessments for industrial operations

- Steel product certification for various end-use applications

- Hydrogen handling and safety compliance requirements

- International trade classification for steel products and technology

Investment Strategy Implications for the Mining and Steel Industries

The successful demonstration of hydrogen-based steel production using 56% iron content ore creates significant implications for investment strategies across mining and steel production. Traditional asset valuations and development priorities may require fundamental reassessment based on changing technology capabilities.

Mining Industry Asset Revaluation

The expansion of economically viable ore grades from 70%+ to 56%+ iron content dramatically increases global iron ore reserves. This grade expansion affects multiple categories of mining assets:

Previously Marginal Deposits:

Mining operations with ore grades between 56-70% may transition from marginal to core assets. These deposits, previously considered uneconomical for premium steel production, become viable development targets with significant value creation potential.

Exploration Strategy Redirection:

Mining companies may reallocate exploration budgets toward moderate-grade deposits that were previously ignored. Areas with geological potential for 55-65% iron content ores warrant renewed assessment and potential development investment.

Stranded Asset Risk Mitigation:

Existing operations with declining ore grades may extend mine life projections as lower-grade resources become economically viable. This extension reduces stranded asset risk and improves project economics for mature operations.

Steel Producer Investment Priorities

Steel producers face decisions regarding technology transition timing and capital allocation between conventional and hydrogen-based production methods. Early adopters may secure competitive advantages through lower carbon costs and access to premium green steel markets.

Technology Transition Investment:

- Pilot facility development for technology validation ($50-100 million)

- Commercial facility construction for full-scale production ($500-1,500 million)

- Hydrogen infrastructure development for supply security ($200-500 million)

- Renewable energy investment for cost-competitive operations ($300-800 million)

Joint Venture and Partnership Opportunities

The technical complexity and capital requirements for hydrogen-based steel production encourage partnership formation across the value chain. Successful partnerships combine mining expertise, technology development, renewable energy access, and market knowledge. These joint venture strategies are becoming increasingly important for technology deployment.

Strategic Partnership Models:

- Miner-Steel Producer Alliances for integrated resource development

- Technology-Finance Consortiums for commercial deployment

- Regional Development Partnerships for geographic expansion

- Research-Industry Collaborations for continued innovation

Risk Assessment Framework for Technology Adoption

Investment in hydrogen-based steel technology involves multiple risk categories that require systematic assessment and mitigation strategies:

Technology Risk Factors:

- Commercial scale validation beyond pilot operations

- Long-term equipment reliability and maintenance costs

- Process optimisation for varying ore characteristics

- Integration complexity with existing steel production systems

Market Risk Considerations:

- Green steel demand growth and pricing sustainability

- Carbon pricing policy development and implementation

- Competition from alternative decarbonisation technologies

- Raw material supply chain reliability and costs

Financial Risk Elements:

- Capital cost escalation for large-scale facility construction

- Operating cost competitiveness versus conventional production

- Technology licensing and intellectual property costs

- Currency and political risk for multi-national projects

What Does This Mean for Future Industrial Decarbonisation?

The breakthrough in hydrogen-based steel production using lower-grade iron ore represents more than an incremental improvement in existing technology. It demonstrates a pathway for fundamental transformation of energy-intensive manufacturing that could extend to multiple industrial sectors beyond steel production.

Broader Industrial Applications

The principles demonstrated in the Namibian pilot have potential applications across other metallurgical and chemical industries that currently depend on fossil fuel reducing agents. Industries including aluminium production, cement manufacturing, and chemical processing may benefit from similar hydrogen-based approaches.

The rotary kiln technology and process optimisation developed for iron ore reduction could be adapted for:

- Copper production from oxide ores using hydrogen reduction

- Nickel processing for battery metals applications

- Rare earth extraction with reduced environmental impact

- Industrial mineral processing with lower carbon intensity

Technology Diffusion Timeline

Based on the pilot results and commercial development requirements, industry experts project a 5-10 year timeline for widespread commercial adoption of hydrogen-based steel production. This timeline depends on several factors:

Near-term Developments (2-3 years):

- Additional pilot campaigns in different geographic regions

- Technology licensing agreements for global deployment

- First commercial-scale facility construction projects

- Regulatory framework development for green steel certification

Medium-term Adoption (3-7 years):

- Multiple commercial facilities operational across major steel markets

- Cost competitiveness achievement versus conventional production methods

- Supply chain development for hydrogen and renewable energy inputs

- Market penetration in automotive and construction applications

Long-term Transformation (7-15 years):

- Technology becomes standard for new steel production capacity

- Retrofit of existing facilities with hydrogen-based systems

- Integration with circular economy steel recycling systems

- Extension to other metallurgical and industrial applications

Policy and Regulatory Evolution

The success of hydrogen-based steel production will likely accelerate policy development supporting industrial decarbonisation. Governments may implement supportive frameworks including carbon pricing, technology incentives, and infrastructure development programmes.

Policy Support Mechanisms:

- Carbon border adjustments favouring low-carbon steel imports

- Technology development grants for hydrogen infrastructure

- Industrial transition funding for facility modernisation

- Trade policies supporting green technology deployment

The demonstration of economically viable hydrogen-based iron-ore-to-green-steel breakthrough in Namibia marks a pivotal moment in industrial decarbonisation. By simultaneously addressing carbon emissions, resource constraints, and geographic production limitations, this innovation creates pathways for sustainable steel manufacturing that seemed impossible just years ago.

The success of the 80-tonne pilot campaign proves that technical barriers to hydrogen-based steel production have been overcome at industrial scale. The ability to process 56% iron content ore at 5 tonnes per hour throughput demonstrates both environmental and economic advantages that position hydrogen reduction as a viable alternative to traditional coal-based methods.

For investors and industry stakeholders, the hydrogen-based iron-ore-to-green-steel breakthrough in Namibia signals the beginning of a fundamental transformation in global steel markets. Mining companies with lower-grade iron ore resources may discover significant value in previously marginal assets. Steel producers face strategic decisions about technology transition timing and capital allocation. Equipment manufacturers and technology developers have opportunities to participate in a growing market for hydrogen-based industrial systems.

The multi-national partnership model demonstrated by the SuSteelAG consortium provides a framework for future development that leverages geographic advantages while managing technological and financial risks. As renewable energy costs continue declining and carbon pricing mechanisms expand globally, hydrogen-based steel production is positioned to transition from pilot demonstration to commercial reality.

The successful implementation showcases how green hydrogen technology can transform traditional manufacturing processes. Moreover, the hydrogen-based iron-ore-to-green-steel breakthrough in Namibia demonstrates that international collaboration and strategic resource allocation can overcome seemingly insurmountable technical barriers.

Disclaimer: This analysis contains forward-looking statements regarding technology development, market adoption, and investment opportunities in hydrogen-based steel production. Actual results may differ significantly from projections due to technological, economic, regulatory, and market factors beyond current assessment capabilities. Readers should conduct independent due diligence before making investment decisions related to green steel technologies or related sectors.

Ready to Invest in the Next Major Mining Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, showcasing exceptional outcomes from major mineral breakthroughs.