May 21, 2026

Industrial Materials Revolution: China's Critical Path to Manufacturing Dominance

Global manufacturing stands at a critical inflection point where traditional materials science meets geopolitical strategy. While steel production has remained largely unchanged for decades, emerging technologies are reshaping fundamental assumptions about metallurgy, supply chains, and industrial competitiveness. The integration of specialized elemental additions into conventional materials represents more than incremental improvement – it signals a transformation that could redefine global manufacturing hierarchies for generations.

This shift occurs against a backdrop of intensifying competition for technological leadership, where materials innovation serves as both economic driver and strategic weapon. Nations that control advanced materials development increasingly dictate terms for downstream industries ranging from transportation infrastructure to defense manufacturing. Understanding this dynamic reveals why China's recent formalization of a china rare earth steel strategy represents a pivotal moment in global industrial competition.

When big ASX news breaks, our subscribers know first

Understanding Advanced Metallurgical Integration Systems

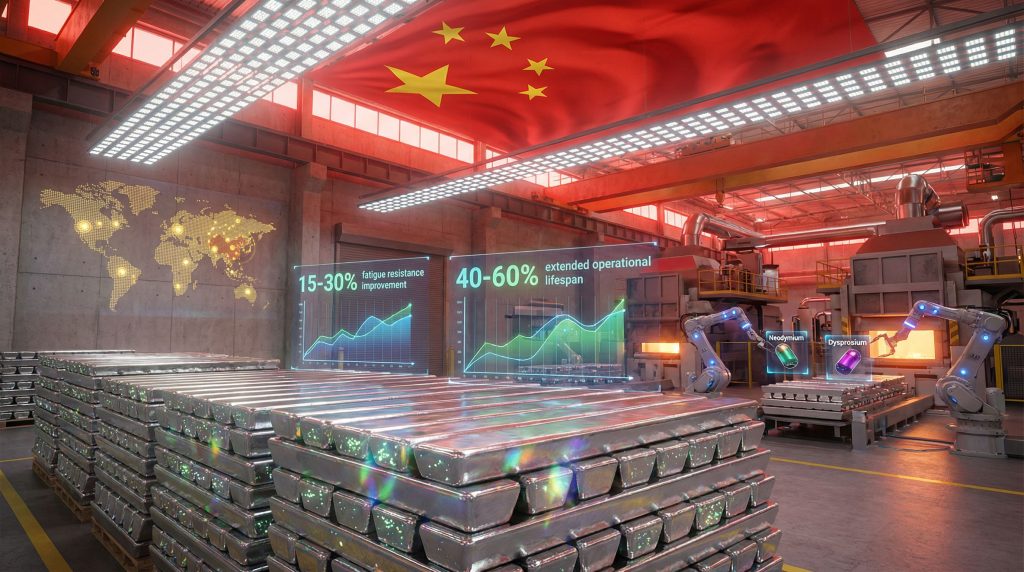

China's systematic incorporation of rare earth elements into steel production represents a fundamental transformation in materials engineering that extends far beyond traditional metallurgy approaches. This methodology combines critical elements such as neodymium, dysprosium, and yttrium with conventional steel alloys to create materials with enhanced operational characteristics that conventional alloying cannot achieve.

The integration process involves precise elemental additions during specific steel production phases, creating molecular-level improvements in material performance. These enhancements occur through controlled crystalline structure modifications that improve strength-to-weight ratios, corrosion resistance mechanisms, and operational longevity under extreme conditions.

Technical Foundation of Enhanced Steel Systems

The molecular-level improvements achieved through rare earth integration create performance advantages across multiple operational parameters. Enhanced fatigue resistance emerges from improved grain boundary cohesion, while corrosion protection results from surface passivation layer formation that extends operational lifespans significantly beyond conventional steel grades.

Temperature stability represents another critical advancement, enabling performance consistency across extreme environmental conditions that would compromise traditional materials. Additionally, specific rare earth additions can impart magnetic properties useful for specialised electromagnetic applications, creating dual-purpose materials serving both structural and functional roles.

Strategic Industry Applications and Deployment

Four primary sectors have emerged as focal points for rare earth steel implementation, each representing critical infrastructure components with extended service life requirements:

Rail Transit Infrastructure:

- High-speed rail systems requiring superior fatigue resistance

- Extended service life reducing long-term maintenance costs

- Enhanced safety margins for high-velocity operations

- Improved performance under dynamic loading conditions

Energy Equipment Manufacturing:

- Wind turbine components with enhanced durability

- Grid infrastructure requiring electromagnetic properties

- Hydroelectric facility components in corrosive environments

- Solar panel mounting systems with extended lifespans

Construction Machinery Applications:

- Heavy equipment components with improved load-bearing capacity

- Reduced maintenance intervals for critical machinery

- Enhanced performance in harsh operational environments

- Extended equipment lifespans reducing replacement costs

Automotive Manufacturing Systems:

- Electric vehicle chassis with optimised strength-to-weight ratios

- Drivetrain components requiring enhanced durability

- Battery housing systems with improved safety characteristics

- Lightweight structural components maintaining strength requirements

China's Integrated Market Position Strategy

Vertical Supply Chain Dominance

China's approach leverages complete supply chain control spanning from rare earth mining operations through final application deployment. This integration creates multiple competitive advantages that extend far beyond simple cost benefits, establishing technological and strategic moats that competitors struggle to replicate.

The upstream control mechanism encompasses approximately 70% of global rare earth mining capacity, combined with over 90% of refining and separation capabilities. This concentration enables China to control both raw material availability and pricing dynamics across global markets, while maintaining near-monopoly positions in heavy rare earth element processing essential for advanced applications.

Furthermore, this critical minerals strategy approach demonstrates how China's rare earth steel strategy builds upon broader resource control initiatives to secure industrial dominance.

Economic Leverage Through Materials Innovation

By embedding rare earths directly into steel products rather than limiting applications to traditional magnet manufacturing, China transforms raw material advantages into finished goods superiority, making Western substitution efforts significantly more complex and capital-intensive.

This strategy represents a fundamental shift from raw material supplier to advanced materials manufacturer, creating value-added products that command premium pricing while incorporating materials that competitors cannot easily source or substitute. The approach enables China to capture higher margins across the value chain while establishing technological dependencies that extend beyond traditional supply relationships.

Institutional Coordination Mechanisms

The January 2026 establishment of the Rare Earth Steel Application Promotion Working Group under the China Iron and Steel Association demonstrates sophisticated institutional coordination spanning government agencies, state-owned enterprises, research institutions, and universities. This coordinated approach accelerates technology transfer, standardisation development, and commercial deployment across strategic industries.

State-coordinated research and development through organisations such as the Chinese Academy of Engineering provides technical expertise while maintaining strategic direction aligned with national objectives. This coordination enables rapid technology deployment while establishing Chinese technical standards that influence global specifications and requirements.

Geopolitical Implications for Western Industrial Strategy

Strategic Vulnerability Assessment Framework

The rare earth steel initiative creates cascading dependencies extending beyond traditional supply chain concerns into fundamental infrastructure systems. Transportation networks requiring specialised steel grades face potential disruptions if alternative suppliers cannot match performance specifications, while energy infrastructure investments may become stranded if unable to access equivalent materials.

Defence applications represent particularly sensitive exposure points where material performance directly impacts operational capabilities. The extended replacement cycles typical of infrastructure investments mean current material choices influence strategic positioning for decades, creating long-term vulnerability windows that adversaries can exploit through supply manipulation or technology denial.

Additionally, china export controls on critical materials demonstrate how strategic resource management reinforces China's rare earth steel strategy positioning.

Western Response Strategy Analysis

| Response Approach | Implementation Timeline | Capital Requirements | Primary Challenges |

|---|---|---|---|

| Domestic Rare Earth Development | 10-15 years | $15-40 billion | Environmental regulations, technical expertise gaps |

| Allied Partnership Networks | 5-10 years | $8-25 billion | Coordination complexity, technology sharing agreements |

| Alternative Materials Research | 15+ years | $5-20 billion | Technical uncertainty, performance validation requirements |

Domestic Development Challenges:

Western nations attempting to replicate China's rare earth processing capabilities face substantial regulatory, environmental, and capital barriers. Establishing equivalent refining infrastructure requires navigating complex environmental permitting processes while developing technical expertise accumulated over decades in Chinese facilities.

Partnership Network Limitations:

Allied coordination efforts encounter technology transfer restrictions, intellectual property concerns, and varying national priorities that complicate unified responses. Different regulatory frameworks and environmental standards across partner nations create additional coordination challenges that China's unified approach avoids.

Alternative Materials Constraints:

Research into substitute materials faces fundamental performance gaps and uncertain development timelines. Many applications require specific properties that rare earth elements provide naturally, making synthetic alternatives technically challenging and economically unviable within relevant timeframes.

Institutional Framework Acceleration Mechanisms

Coordinated Industrial Policy Architecture

The Rare Earth Steel Application Promotion Working Group represents sophisticated coordination architecture integrating multiple institutional layers to accelerate technology deployment. Government agencies provide policy alignment and regulatory support, while state-owned enterprises contribute production capacity and market access necessary for commercial scale deployment.

Research institutions and universities contribute technical development capabilities and talent pipelines essential for sustained innovation. This multi-institutional approach enables rapid technology transfer from research environments to commercial applications while maintaining strategic direction aligned with national objectives.

Moreover, the zijin mining expansion demonstrates how Chinese mining companies leverage institutional coordination to secure global resource access for their china rare earth steel strategy initiatives.

Baogang Group's Central Coordination Role

As China's dominant rare earth steel producer, Baogang Group exemplifies the state-enterprise coordination model through integrated operations spanning steelmaking and rare earth processing. This vertical integration enables optimised material flows, technical coordination, and quality control across the entire production process.

Operational Integration Advantages:

- Combined steelmaking and rare earth operations enabling optimised material flows

- Expanded research capabilities across four strategic application sectors

- Production scaling from pilot projects to commercial deployment volumes

- Standards development influencing global specifications through market leadership

The company's position enables influence over technical standards development while providing commercial scale deployment capabilities essential for market penetration. This combination of technical leadership and production capacity creates competitive advantages that purely private sector competitors struggle to match.

Long-Term Market Transformation Dynamics

How Will Competitive Landscapes Restructure?

The rare earth steel strategy fundamentally alters global competition by establishing performance standards that competitors must match without equivalent resource access. This creates tiered market structures where premium applications increasingly require rare earth-enhanced materials, fragmenting markets based on technical capabilities rather than purely economic factors.

Performance Standards Evolution:

Chinese materials establish benchmarks influencing global specifications, creating situations where infrastructure projects, equipment manufacturers, and technology developers face pressure to source from Chinese suppliers or accept performance disadvantages in competitive markets.

Supply Chain Reconfiguration Pressures:

Downstream manufacturers encounter difficult choices between maintaining competitive performance through Chinese sourcing or accepting reduced capabilities while developing alternative supply relationships. These decisions influence long-term competitiveness across entire industrial sectors.

Consequently, broader mining industry evolution trends demonstrate how China's rare earth steel strategy fits within larger patterns of resource-based competitive advantage.

Investment and Innovation Response Patterns

Western industrial participants explore multiple adaptation strategies reflecting different risk tolerances and strategic priorities:

- Technology Access Partnerships: Joint ventures with Chinese producers providing immediate access to advanced materials while creating dependency relationships

- Alternative Development Investments: Long-term research into substitute materials and production methods with uncertain technical and commercial outcomes

- Supply Diversification Initiatives: Supporting non-Chinese rare earth development projects with extended timelines and substantial capital requirements

Strategic Timeline Consideration: The 15-20 year development timeline required for alternative rare earth supply chains means current Chinese advantages may persist through the 2040s, influencing multiple infrastructure replacement cycles.

The next major ASX story will hit our subscribers first

Global Infrastructure Development Impact Assessment

Performance Standards Evolution Across Critical Sectors

Rare earth-enhanced steel creates new performance baselines influencing infrastructure development decisions across multiple sectors. Transportation infrastructure increasingly requires materials capable of withstanding higher stress levels and longer service lives, while energy infrastructure demands enhanced durability and specialised electromagnetic properties.

Transportation Infrastructure Requirements:

High-speed rail systems require superior fatigue resistance for safe operation at elevated velocities over extended periods. Bridge construction specifications increasingly incorporate extended service life requirements reflecting rare earth steel capabilities, while port facilities in corrosive marine environments benefit from enhanced corrosion protection extending operational lifespans.

Energy Infrastructure Specifications:

Wind turbine components require enhanced durability to withstand extreme weather conditions while maintaining structural integrity. Grid infrastructure increasingly demands materials with specific electromagnetic properties supporting advanced electrical systems, while hydroelectric installations require corrosion resistance in challenging aquatic environments.

Furthermore, energy transition security considerations highlight how China's rare earth steel strategy impacts global renewable energy development timelines.

Cost-Benefit Analysis for Infrastructure Adopters

| Infrastructure Application | Performance Enhancement | Initial Cost Premium | Lifecycle Return |

|---|---|---|---|

| Rail Transportation Systems | 40-60% service life extension | 15-25% higher material cost | Positive ROI over 20+ years |

| Energy Generation Equipment | 30-50% maintenance reduction | 20-30% higher material cost | Positive ROI over 15+ years |

| Marine Infrastructure | 50-70% corrosion resistance improvement | 25-35% higher material cost | Positive ROI over 25+ years |

| Industrial Equipment | 35-45% fatigue resistance improvement | 18-28% higher material cost | Positive ROI over 18+ years |

The lifecycle value proposition becomes increasingly compelling as infrastructure replacement costs continue rising and operational disruption expenses increase. Extended service lives reduce total cost of ownership while improving operational reliability across critical systems.

Strategic Market Preparation Framework

What Risks Should Organizations Assess?

Organisations should evaluate exposure across multiple dimensions encompassing immediate supply relationships, long-term performance requirements, and competitive positioning considerations:

Supply Chain Risk Evaluation:

- Current dependency levels on Chinese steel suppliers

- Alternative sourcing availability and cost implications

- Material substitution feasibility for specific applications

- Supplier diversification options and implementation timelines

Performance Risk Assessment:

- Competitive disadvantages from inferior material performance

- Regulatory compliance requirements with evolving standards

- Customer expectations for enhanced performance characteristics

- Technology obsolescence risks from materials limitations

Strategic Response Development Timeline

Short-Term Adaptation (1-3 years):

- Comprehensive material dependency assessment across operations

- Alternative supplier evaluation and relationship development

- Pilot testing programmes for rare earth-enhanced materials

- Performance benchmarking against Chinese-produced alternatives

Medium-Term Strategy Development (3-7 years):

- Supplier diversification implementation across critical applications

- Alternative materials research investment and partnership development

- Technical expertise building in rare earth applications and alternatives

- Strategic alliance formation for technology access and development

Long-Term Independence Building (7+ years):

- Independent supply chain capability establishment

- Proprietary materials technology development and commercialisation

- Strategic resource access partnerships for long-term security

- Next-generation materials research investment and application

Economic Transformation and Trade Pattern Implications

Global Trade Architecture Shifts

The rare earth steel strategy accelerates China's transition from raw material supplier to advanced manufacturer, fundamentally altering global trade patterns and value distribution. This shift captures higher margins on finished steel products compared to raw rare earth exports while reducing import dependence for domestic infrastructure development.

Export Value Enhancement Mechanisms:

Higher-margin finished products replace lower-value raw material exports, improving trade balance metrics while creating technology export opportunities through licensing and technical cooperation agreements. This value migration enables China to capture premium pricing for advanced materials while maintaining cost competitiveness in volume applications.

For instance, analysis from the US push for reduced China rare earth reliance shows growing Western concerns about strategic dependency on Chinese materials supply chains.

Import Substitution Acceleration:

Reduced reliance on foreign steel for domestic infrastructure projects improves supply security while enabling preferential treatment for Chinese materials in government procurement. This domestic market protection provides scale advantages supporting export competitiveness in international markets.

Innovation Ecosystem Development Dynamics

China's coordinated approach creates positive feedback loops accelerating technological development and market penetration:

- Talent Concentration Effects: Global expertise attraction in materials science through research funding and commercial opportunities

- Capital Investment Multiplication: State and private funding coordination for advanced metallurgy research and development

- Application Development Expansion: Growing use cases across industrial sectors creating market pull for continued innovation

Economic Projection: Rare earth-enhanced steel markets could reach $75-125 billion globally by 2035, with China positioned to capture 60-80% market share without significant Western response initiatives achieving commercial scale.

The economic implications extend beyond direct market share to influence related sectors including equipment manufacturing, infrastructure services, and technology licensing, creating multiplier effects that reinforce China's industrial leadership across multiple domains.

However, concerns about China's growing market control are evidenced by CSIS analysis of defense supply chain threats, highlighting how the china rare earth steel strategy impacts national security considerations.

Strategic Considerations for Global Market Participants

The emergence of rare earth steel as a strategic industrial capability represents more than technological advancement – it demonstrates how materials innovation serves broader geopolitical objectives while creating lasting competitive advantages. Organisations and nations must recognise that current decisions regarding materials sourcing, technology development, and strategic partnerships will influence competitive positioning for decades.

The integration of rare earth elements into conventional steel production exemplifies China's systematic approach to industrial leadership through coordinated state-enterprise cooperation, long-term research investment, and strategic resource control. This model creates competitive moats that traditional market mechanisms struggle to overcome within relevant timeframes.

For Western nations and companies, the challenge extends beyond simply matching Chinese technical capabilities to developing alternative approaches that leverage different competitive advantages while addressing fundamental resource dependencies. Success requires sustained commitment, international cooperation, and recognition that materials competition has become central to broader technological and economic rivalry.

In conclusion, the rare earth steel initiative ultimately represents one component of a larger transformation where materials science increasingly determines industrial competitiveness, infrastructure capabilities, and national strategic positioning in an interconnected global economy.

Ready to Capitalise on Strategic Materials Investments?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including rare earth and critical materials opportunities that could benefit from China's evolving steel strategy. Position yourself ahead of major market movements by exploring Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial returns, then begin your 30-day free trial today to identify actionable investment opportunities before the broader market.