June 23, 2026

How Institutional Money Managers Navigate Precious Metals During Extreme Volatility

Market psychology reveals fascinating patterns when institutional investors face unprecedented volatility in precious metals markets. During February 2026, sophisticated money managers demonstrated classic behavioural responses to extreme price movements, cutting their exposure to gold futures by nearly one-quarter as silver market squeeze experienced daily swings approaching double digits. Understanding these institutional reactions provides critical insights into how professional capital allocators balance risk management with opportunity capture during periods of market stress.

When big ASX news breaks, our subscribers know first

Risk Assessment Frameworks Used by Large Speculators

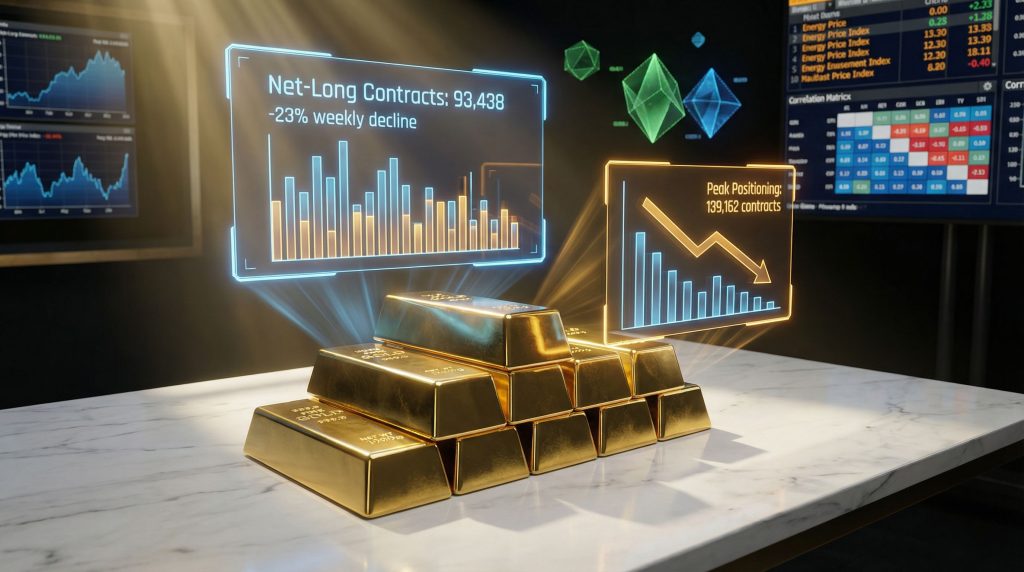

Professional trading operations employ sophisticated analytical models when evaluating precious metals exposure during volatile periods. The recent data from the Commodity Futures Trading Commission shows net-long gold contracts fell to 93,438 for the week ending February 3, 2026, representing a 23% weekly reduction and marking the lowest positioning level in 15 weeks. This dramatic pullback illustrates how hedge funds cut bullish gold wagers when market conditions exceed their risk tolerance parameters.

Volatility-Adjusted Position Sizing Methods

- Dynamic risk budgeting based on realised volatility measurements

- Correlation monitoring across asset classes during stress periods

- Liquidity assessment of futures and options market depth

- Margin requirement escalation impact on position sustainability

The magnitude of recent precious metals moves created unique challenges for institutional position sizing. Gold futures experienced a 3.75% daily change on February 6, 2026, whilst record-high gold prices demonstrated extreme sensitivity with 9.29% daily volatility. These movements forced many hedge funds to recalibrate their risk models and implement emergency position reductions to maintain portfolio-wide risk targets.

Technical Momentum Versus Fundamental Analysis

| Risk Factor | Normal Market Impact | Volatile Market Impact | Institutional Response |

|---|---|---|---|

| Daily Price Range | 1-2% typical movement | 3-9% extreme swings | Position size reduction |

| Volume Patterns | Consistent liquidity | Sporadic depth | Execution timing delays |

| Cross-Asset Correlation | Diversification benefit | Correlation breakdown | Portfolio rebalancing |

| Margin Requirements | Stable overnight rates | Sudden escalation | Forced liquidation risk |

Professional money managers prioritise capital preservation during volatility spikes, often accepting reduced profit potential to avoid catastrophic portfolio drawdowns.

Energy Sector Attraction During Metals Market Disruption

Institutional capital often rotates towards energy markets when precious metals exhibit excessive volatility. The price stability comparison on February 6, 2026 illustrates this preference clearly: Brent crude oil showed 0.95% daily movement whilst natural gas declined 2.70%, both representing manageable volatility ranges compared to silver's dramatic 9.29% swing.

Fundamental Clarity in Energy Markets

Energy commodities offer several advantages during precious metals volatility:

- Supply-demand transparency through weekly inventory reports

- Seasonal pattern predictability in natural gas and heating oil

- Geopolitical risk premiums with clearer cause-and-effect relationships

- Production data reliability from established reporting agencies

The February 2026 price data demonstrates energy markets maintained relative stability whilst precious metals experienced extreme moves. Crude oil at $63.55 per barrel showed 0.71% daily change, providing institutional traders with more predictable risk-reward calculations compared to the chaos in silver markets.

Institutional Flow Patterns Between Sectors

Professional capital allocation follows systematic rotation patterns during market stress. Energy futures markets typically maintain deeper liquidity during volatile periods, allowing larger position sizes without significant market impact. Furthermore, the consistent trading volumes in crude oil and natural gas contracts enable institutional investors to deploy substantial capital whilst maintaining execution efficiency.

Market Structure Amplification of Precious Metals Volatility

The extreme price movements in silver and gold markets during early February 2026 resulted from multiple structural factors creating feedback loops. Silver's 9.29% daily volatility and palladium's 6.66% movement exceeded normal trading ranges by significant multiples, triggering systematic responses from market participants.

Electronic Trading System Responses

Modern market infrastructure contains built-in mechanisms that can amplify volatility during stress periods:

- Algorithmic stop-loss triggers activating simultaneously across multiple systems

- Market maker inventory constraints reducing liquidity provision capacity

- Margin call cascades forcing additional selling pressure

- Cross-market arbitrage breakdown eliminating natural price stabilisers

ETF Flow Disruptions

Exchange-traded fund mechanisms face particular strain during extreme precious metals volatility. When underlying futures markets experience rapid price changes, authorised participants must execute large creation or redemption orders that can overwhelm normal market depth. Consequently, the resulting supply-demand imbalances create additional pressure on already stressed markets.

Federal Reserve Policy Transition Effects

Kevin Warsh's nomination as Federal Reserve Chair created specific uncertainty factors affecting institutional precious metals strategies. Policy transition periods historically generate increased volatility as markets attempt to discount potential changes in monetary policy direction, which correlates with gold-stock correlations during these periods.

Interest Rate Expectation Shifts

Professional traders monitor several key indicators during Federal Reserve leadership transitions:

- Fed funds futures curve adjustments reflecting policy expectations

- Real interest rate calculations incorporating inflation expectations

- Dollar strength implications from potential policy divergence

- Quantitative policy stance changes affecting money supply growth

The nomination announcement coincided with the precious metals volatility spike, suggesting institutional investors interpreted the potential policy shift as reducing the attractiveness of zero-yielding assets like gold and silver.

Hedge Fund Policy Adaptation Strategies

| Strategy Type | Implementation Method | Risk Management Goal |

|---|---|---|

| Position Reduction | Systematic size scaling | Limit policy uncertainty exposure |

| Currency Hedging | Dollar index futures | Neutralise exchange rate impacts |

| Metal Diversification | Spreading across precious metals | Reduce single-asset concentration |

| Volatility Targeting | Dynamic position sizing | Maintain consistent risk levels |

Persistent Fundamental Support Factors

Despite the dramatic reduction in speculative positioning, several structural demand sources continue supporting precious metals markets. Central bank gold purchases represent a significant long-term trend that operates independently of short-term speculative flows.

Central Bank Accumulation Patterns

Global monetary authorities maintain systematic precious metals acquisition programmes driven by:

- Reserve diversification away from dollar-dominated assets

- Monetary sovereignty considerations during geopolitical uncertainty

- Inflation hedge mechanisms for sovereign wealth preservation

- Strategic resource accumulation for national security purposes

However, institutional perspectives on gold safe-haven insights remain mixed during volatile periods.

Technology Sector Industrial Demand

| Demand Category | Growth Rate | Sustainability Factor | Impact on Pricing |

|---|---|---|---|

| Semiconductor Applications | Moderate growth | Technology advancement | Steady baseline |

| Solar Panel Manufacturing | High growth | Climate policy support | Increasing trend |

| Electric Vehicle Components | Rapid expansion | Electrification mandate | Strong upward pressure |

| Medical Device Integration | Consistent demand | Healthcare innovation | Stable contribution |

The next major ASX story will hit our subscribers first

Recovery Timing for Institutional Positioning

Historical analysis suggests institutional money managers typically return to precious metals markets after volatility measures normalise and technical indicators show stabilisation. The current extreme readings in both gold and silver markets may actually represent contrarian opportunity signals for patient capital.

Volatility Normalisation Indicators

Professional traders monitor specific metrics when evaluating re-entry timing:

- Realised volatility returning to historical ranges below 20% annualised

- Options market premiums declining from panic levels

- Daily trading ranges stabilising within normal percentile bands

- Cross-asset correlations returning to fundamental relationships

Institutional Memory and Market Cycles

The February 2026 positioning reset creates potential longer-term opportunities as speculative excess clears from markets. When hedge funds cut bullish gold wagers to multi-week lows, it often signals the completion of a speculative cycle rather than the beginning of a fundamental bear market, particularly when considering the broader gold price forecast.

Market structure analysis suggests the current volatility represents a technical correction rather than a fundamental shift in precious metals demand dynamics.

Strategic Implications for Market Participants

Understanding institutional behaviour patterns during volatility provides valuable context for various market participants. The 23% reduction in net-long positioning represents professional risk management in action rather than a negative fundamental assessment of precious metals.

Position Sizing Lessons

The institutional response to February 2026 volatility demonstrates several key principles:

- Systematic risk reduction when volatility exceeds predetermined thresholds

- Correlation monitoring across asset classes during stress periods

- Liquidity preservation maintaining capacity for opportunity capture

- Patience for normalisation waiting for technical stabilisation signals

Long-Term Perspective Integration

Professional money managers distinguish between short-term technical corrections and fundamental trend changes. The current hedge fund positioning reduction likely represents the former, creating potential value opportunities for investors with longer time horizons and different risk tolerance parameters. In addition, analysis from financial industry reports confirms this pattern across multiple institutional managers.

The extreme volatility in precious metals markets during early 2026 illustrates how modern market structure can amplify price movements beyond fundamental justification. Understanding these dynamics helps explain why sophisticated institutional investors systematically reduce exposure during such periods, prioritising capital preservation over profit maximisation when market behaviour becomes unpredictable. Furthermore, when hedge funds cut bullish gold wagers to such significant levels, it often creates conditions for subsequent recovery once technical factors stabilise.

Ready to Capitalise on Precious Metals Market Opportunities?

Whilst institutional investors reduce their exposure during volatile periods, Discovery Alert's proprietary Discovery IQ model identifies significant ASX mineral discoveries in real-time, helping subscribers capitalise on precious metals opportunities ahead of broader market recognition. Begin your 14-day free trial today to gain immediate access to actionable mining discovery alerts that can help you navigate market volatility with confidence.