June 25, 2026

When Supply Chain Fragility Meets Commercial Opportunity

The global graphite market is undergoing a structural realignment that few outside the critical minerals sector fully appreciate. For decades, China has functioned as the world's dominant graphite producer, processor, and exporter, supplying well over 80% of the world's natural graphite and an even higher proportion of the processed spherical graphite used in lithium-ion battery anodes. That concentration of supply has long been considered a systemic vulnerability by manufacturers across Northeast Asia, yet little action was taken until geopolitical pressures forced the issue.

When China formally introduced graphite export licensing requirements in late 2023, it triggered a procurement reassessment among Japanese and South Korean industrial manufacturers that continues to reshape how these markets source critical raw materials. The response has not been panic, but it has been deliberate. Buyers in these two nations, both of which host globally significant electric vehicle battery production, advanced electronics manufacturing, and steelmaking industries, have begun actively diversifying away from single-source dependency.

It is within this reconfigured demand environment that the commercial agreement between ASX-listed International Graphite (IG6) and Hong Kong-based trading company Wogen Pacific needs to be understood. Furthermore, the International Graphite Asia Pacific offtake agreement represents a meaningful commercial milestone for an emerging Australian graphite processor seeking to establish a foothold in Northeast Asian industrial supply chains.

When big ASX news breaks, our subscribers know first

What the International Graphite Asia Pacific Offtake Agreement Actually Establishes

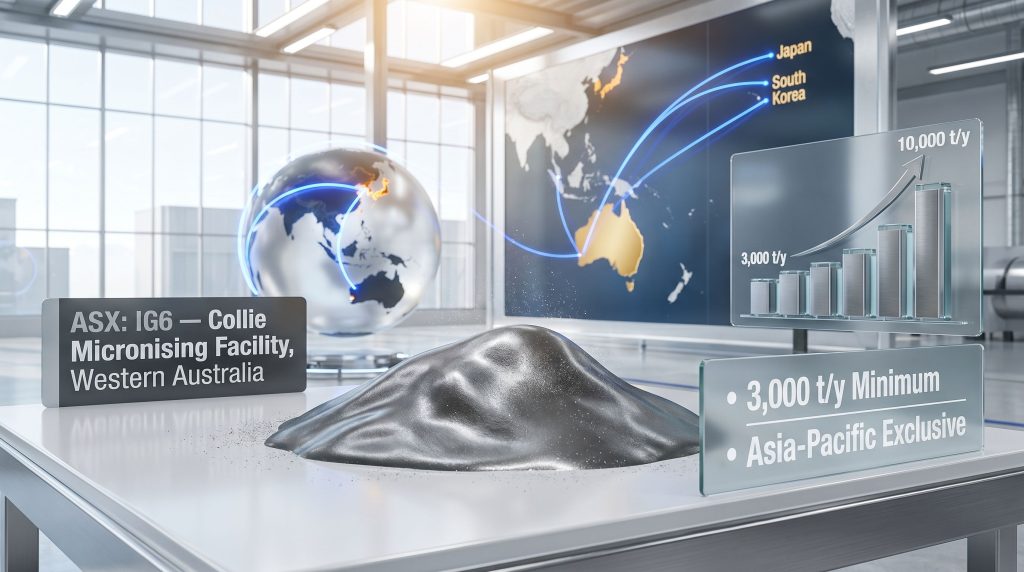

The agreement, structured as a Heads of Terms, sets out a three-year commercial framework intended to govern the supply of micronised graphite from IG6's Collie Micronising Facility in Western Australia to Asia-Pacific markets, with Wogen Pacific acting as the exclusive regional distributor.

The core commercial parameters are worth examining closely:

| Term | Detail |

|---|---|

| Agreement Type | Heads of Terms (non-binding framework) |

| Agreement Duration | Three years from commercial production |

| Minimum Annual Purchase Volume | 3,000 tonnes of micronised graphite per year |

| Maximum Feedstock Sourcing Commitment | Up to 10,000 t/y of flake graphite concentrate |

| Production Facility | Collie Micronising Facility, Western Australia |

| Distribution Territory | Asia-Pacific (exclusive) |

| Pricing Mechanism | Spot basis |

| Primary Target Markets | Japan and South Korea |

Several elements of this structure deserve closer attention. The minimum purchase volume of 3,000 tonnes per year provides IG6 with a baseline demand signal that supports production planning, even before a binding contract is in place. The feedstock sourcing commitment of up to 10,000 tonnes per year of flake graphite concentrate is particularly significant because it addresses one of the less obvious bottlenecks in graphite processing: securing reliable raw material supply to keep a micronising facility operating at scale.

From Heads of Terms to Binding Agreement: What Investors Need to Understand

The non-binding nature of the current agreement is the single most important factor for investors to internalise. In the mining and resources sector, Heads of Terms frameworks are a well-established commercial instrument. They allow two parties to align on intent, structure, and key parameters before committing the legal and financial resources required to execute a fully binding contract.

Because the current agreement remains non-binding, commercial terms including volumes, pricing, and exclusivity remain subject to negotiation as the Collie facility approaches production readiness. The transition to binding agreements will be a critical milestone to monitor.

The transition to binding form is expected to occur as the Collie Micronising Facility approaches commercial production. The intervening period, during which IG6 must complete facility preparation and demonstrate production readiness, represents the window in which both parties will negotiate final binding terms. Delays in facility commissioning could therefore push back this milestone.

The Collie Micronising Facility and the Technical Case for Western Australia

What Micronised Graphite Is and Why It Commands a Premium

Not all graphite is created equal, and this is a distinction that is frequently lost in broader coverage of the critical minerals sector. Natural graphite extracted from the ground is typically classified as flake graphite concentrate, which undergoes further processing before it can serve most high-specification industrial applications.

Micronised graphite is produced by milling flake graphite to precise particle sizes, typically measured in microns. This processing step transforms a bulk commodity into a performance material with defined characteristics suited to specific end uses:

- Battery anode precursor materials used in lithium-ion cell manufacturing

- Refractory applications in steelmaking, foundry operations, and high-temperature industrial processes

- Specialty lubricants where graphite's layered crystal structure reduces friction under extreme conditions

- Conductive coatings and composites used in advanced manufacturing and electronics

The particle size distribution achieved during micronisation directly determines which applications the product can serve, which is why processing capability is as strategically important as the underlying mineral resource.

Collie's Logistical and Infrastructure Advantages

The Collie region in Western Australia carries advantages that extend beyond raw geography. The area has established industrial infrastructure, access to rail and road transport networks, and proximity to the Port of Bunbury, which serves as a practical export gateway to Asia-Pacific markets. For a processing-focused facility rather than a traditional mine, these connectivity attributes materially reduce logistics costs and complexity.

Western Australia more broadly has emerged as a preferred jurisdiction for critical minerals processing. This is partly because of its established mining services ecosystem and workforce, and partly because of the track record it provides to offtake partners and downstream customers seeking supply chain transparency. The Australian graphite industry has, consequently, become increasingly attractive to Northeast Asian buyers seeking supply chain alternatives.

Understanding the Demand Landscape: Why Japan and South Korea Are the Right Target Markets

Japan's Industrial Graphite Consumption Profile

Japan consumes graphite across a range of industrial verticals, several of which are not immediately obvious to observers focused primarily on the battery materials narrative. Refractory graphite remains a significant demand segment given Japan's mature but still operating steelmaking industry. More forward-looking demand is driven by the country's position as home to major lithium-ion battery manufacturers and electric vehicle component suppliers.

Japan's industrial culture places a premium on material specification, traceability, and supply reliability — characteristics that favour established trading relationships with accountable supply chains over spot market opportunism. In addition, the global graphite shortage has accelerated Japan's urgency to formalise alternative sourcing strategies beyond Chinese supply channels.

South Korea's Position as a High-Growth Advanced Materials Market

South Korea's graphite demand profile is heavily shaped by its role as a global hub for battery manufacturing. Korean conglomerates operate some of the world's largest battery cell production facilities, and these operations require consistent, high-specification graphite anode materials. South Korea has also been among the most proactive nations in terms of formalising critical minerals supply chain diversification strategies following China's 2023 export controls.

China's imposition of graphite export licensing requirements in late 2023 significantly accelerated procurement diversification efforts among Japanese and South Korean manufacturers. This regulatory shift has elevated the strategic value of non-Chinese graphite supply sources, a dynamic that directly benefits Australian producers.

The combined demand from these two markets represents a compelling commercial rationale for why Wogen Pacific has identified them as primary distribution targets. Furthermore, China's export restrictions on graphite have structurally elevated the commercial opportunity for non-Chinese producers such as IG6 to fill the resulting supply gap.

Wogen Pacific's Role and Why the Choice of Trading Partner Matters

What a Commodity Trading Intermediary Brings to an Emerging Producer

For a junior miner or processor approaching commercial production for the first time, the choice of commercial partner carries consequences well beyond the terms printed in an agreement. Wogen Pacific is a Hong Kong-based commodity trading firm with established capabilities across global sourcing, logistics, and market distribution for industrial minerals. The firm's existing presence across major Asian markets means IG6 does not need to build those relationships from scratch.

This model, where an emerging producer partners with an established trading house for regional distribution, is common in the industrial minerals sector for several reasons:

- Market access acceleration — Trading houses have existing buyer relationships that can be activated immediately upon supply availability

- Logistics infrastructure — Established import/export capabilities reduce friction in moving product from Western Australia to Northeast Asian customers

- Credit and counterparty management — Trading companies often absorb counterparty risk in ways that benefit smaller producers

- Market intelligence — Deep market presence provides real-time pricing intelligence that informs production and commercial decisions

Spot Pricing Mechanics and Revenue Predictability

The agreement specifies that pricing will be determined on a spot basis, meaning individual transactions will be priced according to prevailing market rates at the time of sale rather than against a fixed long-term price. This structure has dual implications. For IG6, spot pricing means the company can benefit from upward price movements in the graphite market.

However, it also means revenues will be exposed to downward price cycles, which have characterised graphite markets over the past several years as oversupply from Chinese producers depressed benchmark prices. The battery raw materials market more broadly has experienced this pricing volatility, making revenue predictability a key challenge for emerging processors.

Spot pricing is more common in industrial minerals agreements than many investors realise, particularly in early-stage commercial relationships where neither party wants to be locked into a price that may prove disadvantageous. The transition toward longer-term fixed or indexed pricing arrangements typically occurs once a supply relationship matures and both parties have established confidence in quality and delivery consistency.

How This Agreement Compares Across the ASX Graphite Sector

Benchmarking IG6's Commercial Framework

The ASX hosts a cohort of graphite-focused companies at various stages of development. Placing the International Graphite Asia Pacific offtake agreement in context helps investors assess its relative significance. For instance, completed offtake agreements for large flake graphite by peer companies illustrate how binding frameworks differ structurally from the Heads of Terms stage IG6 currently occupies.

| Company | Partner | Volume Commitment | Market | Agreement Status |

|---|---|---|---|---|

| International Graphite (IG6) | Wogen Pacific | 3,000–10,000 t/y | Asia-Pacific (Japan, South Korea) | Heads of Terms (non-binding) |

| Peer A (generalised) | Regional distributor | Variable | Asia | Binding offtake |

| Peer B (generalised) | End-user manufacturer | Variable | Europe/Asia | MOU stage |

Note: Peer comparisons are illustrative. Readers should verify current agreement statuses independently via ASX announcements.

The exclusive regional distribution arrangement IG6 has structured with Wogen differentiates it from open-market sales models where producers sell to multiple buyers without geographic alignment. Exclusivity, even in a non-binding framework, signals that both parties view the relationship as strategically significant rather than transactional.

The next major ASX story will hit our subscribers first

Key Risks Investors Should Evaluate

Commercial, Technical, and Market Risks in Context

Investors approaching this agreement with enthusiasm should balance that optimism against a clear-eyed assessment of the risks involved:

- Non-binding status means all terms remain subject to renegotiation. If market conditions shift significantly before binding agreements are executed, final terms may differ materially from the current framework.

- Feedstock dependency is a structural risk. The commitment for Wogen to source up to 10,000 t/y of flake graphite feedstock implies that Collie's production scalability depends partly on external supply.

- Spot pricing exposure creates revenue variability. Graphite markets have been volatile, and benchmark prices for industrial graphite products have faced persistent pressure from Chinese export volumes.

- Facility commissioning timelines will determine when the Heads of Terms can convert to binding form. Delays in achieving commercial production readiness push back revenue realisation.

- Market competition from established Chinese and other Asian producers remains intense, and customer qualification processes for new supply sources can be lengthy in quality-sensitive industries like battery manufacturing.

Moreover, broader critical minerals demand dynamics mean the competitive landscape for graphite supply contracts is intensifying, with multiple jurisdictions vying for the same Northeast Asian customer base.

Frequently Asked Questions: International Graphite Asia Pacific Offtake Agreement

What exactly has International Graphite signed with Wogen Pacific?

International Graphite (ASX: IG6) has executed a Heads of Terms agreement with Wogen Pacific Ltd, a Hong Kong-based commodity trading firm. This non-binding framework establishes the commercial intent for Wogen to purchase a minimum of 3,000 tonnes per year of micronised graphite from IG6's Collie facility in Western Australia, with the potential to source up to 10,000 t/y of flake graphite feedstock to support expanded production.

Is this a binding offtake agreement?

No. As of June 2026, the agreement remains a non-binding Heads of Terms. Both parties intend to replace this framework with formal binding agreements as the Collie Micronising Facility progresses toward commercial production.

Which markets will Wogen Pacific supply?

Wogen Pacific will distribute International Graphite's micronised graphite exclusively across Asia-Pacific, with Japan and South Korea identified as the primary target markets given their significant and growing demand for high-specification industrial graphite materials.

What is micronised graphite used for?

Micronised graphite serves a range of industrial applications including battery anode materials for lithium-ion cells, refractory linings in steelmaking and foundry operations, lubricants, and specialty coatings used in advanced manufacturing processes.

How does this deal benefit International Graphite's path to production?

The agreement provides IG6 with a committed distribution channel and feedstock sourcing support, reducing two of the most significant commercialisation risks for an emerging graphite processor: securing buyers before production begins and ensuring sufficient raw material supply to scale output over time.

Why are Japan and South Korea significant markets for graphite?

Both nations are major hubs for electric vehicle battery manufacturing, steelmaking, and advanced electronics production — all of which are significant consumers of industrial and battery-grade graphite. Ongoing supply chain diversification away from Chinese-sourced graphite has further elevated demand for alternative supply sources in these markets.

Australia's Evolving Role in the Global Graphite Supply Chain

Building a Non-Chinese Supply Corridor to Northeast Asia

Australia's graphite sector occupies a distinctive position in the global critical minerals landscape. The country hosts significant natural graphite resources, a transparent regulatory environment, and well-established trade relationships with both Japan and South Korea. These structural attributes make Australian graphite projects commercially attractive to Asian buyers engaged in active supply chain diversification.

The International Graphite Asia Pacific offtake agreement with Wogen Pacific represents one data point in what is becoming a broader pattern: Australian graphite processors targeting Northeast Asian customers through established trading networks, using Western Australian processing infrastructure as the production base.

Whether this pattern matures into a durable supply corridor will depend on how quickly individual projects like Collie can transition from commercial frameworks to binding agreements and, ultimately, to consistent product delivery. For IG6 specifically, the pathway from Heads of Terms to first shipment involves several critical milestones, each of which will serve as a measurable signal of commercial progress.

The broader investment thesis around Australian graphite hinges on whether non-Chinese supply sources can achieve the cost competitiveness, product quality, and delivery reliability that Japanese and South Korean manufacturers require. Achieving those benchmarks will require more than commercial agreements — it will require operational execution that consistently meets specification.

This article is intended for informational purposes only and does not constitute financial advice. Investors should conduct independent due diligence and consult qualified financial advisers before making investment decisions. Forward-looking statements and commercial projections carry inherent uncertainty and may not reflect actual outcomes.

Want to Stay Ahead of Significant ASX Mineral Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including across the critical minerals and graphite sectors — instantly translating complex data into actionable opportunities for investors at every level. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the broader market.